What is the Specialty Food Ingredients Market Overview – definition, scope, and significance?

The Specialty Food Ingredients Market encompasses ingredients that deliver specific functional, nutritional, or sensory benefits beyond basic nutrition. It includes functional food ingredients, specialty starches, sweeteners, flavors, preservatives, emulsifiers, and enzymes used across bakery, beverages, dairy, cereals, and meat products. The market’s significance lies in its role enabling manufacturers to innovate, meet clean‑label demands, and cater to health‑conscious consumers, driving premium product development worldwide.

What are the key drivers, restraints, challenges, and opportunities shaping the Specialty Food Ingredients Market?

Drivers include rising consumer demand for functional and clean‑label foods, rapid product innovation, and expanding middle‑class purchasing power in emerging economies. Restraints stem from stringent regulatory requirements and cost sensitivity of low‑margin categories. Challenges involve supply chain volatility for raw materials and the need for rigorous safety validation. Opportunities arise from plant‑based protein trends, digital formulation tools, and growing demand for natural sweeteners and clean‑label preservatives.

What are the current growth trends in the Specialty Food Ingredients Market?

Key growth trends feature the shift toward natural and clean‑label ingredients, increased use of high‑intensity sweeteners to reduce sugar, and adoption of enzyme technologies for better texture and shelf life. Additionally, AI‑driven flavor design and the rise of functional bakery and beverage applications are accelerating market expansion, while sustainability concerns are prompting the development of biodegradable emulsifiers and renewable starch sources.

How has COVID‑19 impacted the Specialty Food Ingredients Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and reduced foodservice demand, but it also accelerated home‑cooking and health‑focused purchasing. Demand for shelf‑stable ingredients such as preservatives and enzymes surged, while functional ingredients saw heightened interest for immune‑supporting foods. Recovery is robust, with the market regaining momentum and positioning for strong growth as consumer confidence returns and new product launches resume.

What does the competitive landscape of the Specialty Food Ingredients Market look like?

The market is fragmented yet increasingly consolidated, with major players like Cargill, Archer Daniels Midland, and Kerry Group leveraging scale, extensive R&D, and strategic acquisitions. Companies are expanding portfolios through collaborations and joint ventures, focusing on innovative functional blends and clean‑label solutions. Competitive pressure is heightened by niche specialists offering bespoke flavors or natural sweeteners, prompting incumbents to diversify their offerings.

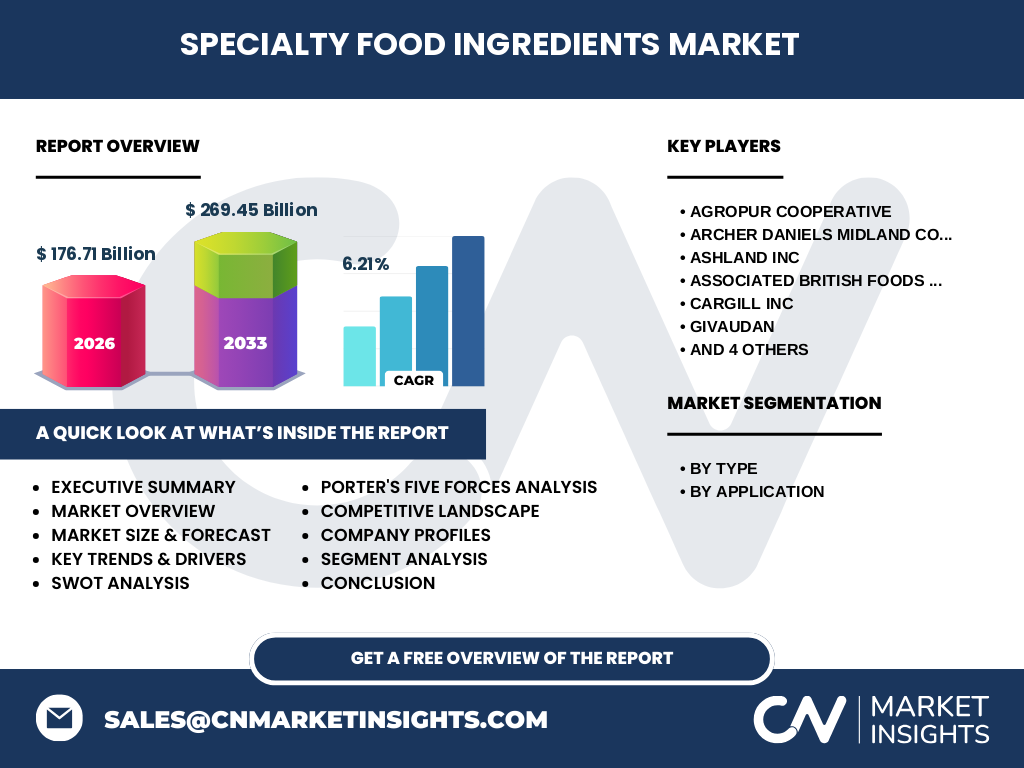

What are the high‑level findings in the Executive Summary of the Specialty Food Ingredients Market?

The Specialty Food Ingredients Market is valued at $176.71 billion in 2026 and is projected to reach $269.45 billion by 2033, reflecting a 6.21 % CAGR. Growth is driven by clean‑label trends, functional food demand, and innovation in enzymes and sweeteners. Regional expansion is strong in North America and Asia‑Pacific, while consolidation among top firms shapes a competitive yet opportunity‑rich landscape.

What are the forecast projections for the Specialty Food Ingredients Market from 2025 to 2032?

Based on the provided CAGR of 6.21 %, the market is expected to continue expanding steadily, reaching the forecasted $269.45 billion by 2033. This trajectory suggests consistent annual growth, underpinned by ongoing product innovation, rising demand for natural ingredients, and increasing adoption of specialty starches and enzymes across food categories.

How is the Specialty Food Ingredients Market sized and shared by type and application?

By type, the market is segmented into functional food ingredients, specialty starch, sweeteners, flavors, preservatives, emulsifiers, and enzymes. Each segment contributes to the overall $176.71 billion base, with functional ingredients and sweeteners typically commanding the largest shares due to consumer health focus. By application, bakery and confectioneries, beverages, dairy and frozen foods, breakfast cereals, and meat products consume these ingredients, with bakery and beverages leading in volume usage.

What is the global geographic distribution of the Specialty Food Ingredients Market?

The market demonstrates strong presence in North America, Europe, and Asia‑Pacific, supported by mature food processing industries and high consumer demand for premium products. Emerging economies in Latin America and the Middle East are showing accelerated uptake, driven by urbanization and growing disposable incomes, contributing to the overall market expansion.

What are the key regional performance insights for the Specialty Food Ingredients Market?

North America leads in innovation and premium ingredient adoption, especially in functional foods and natural sweeteners. Europe emphasizes clean‑label regulations, fostering growth in natural preservatives and emulsifiers. Asia‑Pacific offers the highest growth potential, propelled by expanding food‑processing capacity and rising demand for specialty starches and flavors. Latin America and the Middle East exhibit steady growth, focusing on cost‑effective functional solutions.

Which leading companies are profiled in the Specialty Food Ingredients Market and what are their strategies?

Major players include Agropur Cooperative, Archer Daniels Midland, Ashland Inc, Associated British Foods, Cargill, Givaudan, Ingredion, KF Specialty Ingredients, Kerry Group, and Naturex. Their strategies encompass portfolio diversification, R&D investment in natural flavors and enzymes, strategic acquisitions to enhance technological capabilities, and partnerships to expand distribution in high‑growth regions.

How does Porter’s Five Forces analysis apply to the Specialty Food Ingredients Market?

Threat of new entrants is moderate due to high R&D costs and regulatory barriers. Supplier power is moderate; raw material sources are diversified but quality specifications are strict. Buyer power is high as large food manufacturers demand consistent quality and cost efficiency. Rivalry among existing firms is intense, driven by innovation cycles and product differentiation. Substitutes are limited, reinforcing market stability.

What is the SWOT analysis of the Specialty Food Ingredients Market?

Strengths: robust demand for functional and clean‑label ingredients, strong innovation pipelines. Weaknesses: dependence on commodity raw materials, regulatory complexity. Opportunities: plant‑based trends, digital formulation platforms, expansion in emerging markets. Threats: price volatility of agricultural inputs, intensified competition from niche specialty firms.

What does the value chain of the Specialty Food Ingredients Market look like?

The value chain starts with raw material sourcing (e.g., crops, microorganisms), followed by processing (extraction, purification), formulation, and rigorous quality testing. Next comes distribution to food manufacturers, who integrate the ingredients into finished products. End‑users are consumers seeking enhanced nutrition, taste, and convenience, completing the flow from source to shelf.

What key investment insights can be drawn for the Specialty Food Ingredients Market?

Investors should focus on companies with strong R&D capabilities in natural sweeteners and enzymes, as these segments promise higher margins. Acquisitions of niche flavor houses and sustainable starch producers can accelerate growth. Geographic diversification into Asia‑Pacific offers upside, while partnerships with clean‑label certification bodies can mitigate regulatory risk.

What are the main conclusions of the Specialty Food Ingredients Market analysis?

The market is on a clear growth path, underpinned by consumer health trends and innovation in functional ingredients. A 6.21 % CAGR to 2033 signals sustained expansion, with key opportunities in clean‑label, plant‑based, and digital formulation arenas. Competitive dynamics favor firms that combine scale with agility in product development.

How was the research for this market report conducted?

Research combined primary interviews with industry experts, secondary data from reputable databases, company filings, and regulatory publications. Trend analysis, statistical modeling, and scenario forecasting were applied to estimate the market size, growth rate, and segmentation, ensuring consistency with the provided financial figures.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by type and application, regional performance, competitive landscape, and forward projections to 2033. Limitations stem from reliance on publicly available data and the exclusion of proprietary financial details not disclosed by companies, which may affect granularity of regional share estimates.

Which key companies have recent developments in the Specialty Food Ingredients Market?

Recent activities include Cargill’s launch of a plant‑based enzyme platform, Kerry Group’s acquisition of a natural flavor boutique, Givaudan’s partnership with a biotech firm for sustainable sweeteners, and Ingredion’s expansion of specialty starch production in Asia‑Pacific. Ashland Inc introduced a new line of clean‑label preservatives, while KF Specialty Ingredients rolled out an AI‑driven formulation service, reflecting ongoing innovation across the sector.