1. Asia Pacific Autotransfusion Devices Market Overview - Definition, scope, and significance?

The Asia Pacific Autotransfusion Devices market encompasses all equipment and consumables used to collect, process, and reinfuse a patient’s own blood during or after surgery. This includes whole‑blood salvage systems, cell‑salvage devices, and related accessories such as collection reservoirs, filters, and anticoagulant kits. The scope covers deployment across hospitals, specialty clinics, and ambulatory surgery centers for a wide range of procedures, notably cardiac, orthopedic, organ transplantation, and trauma surgeries. Autotransfusion reduces the reliance on allogenic blood, lowers transfusion‑related complications, and aligns with cost‑containment strategies—making it a critical component of modern peri‑operative care in the rapidly expanding Asia Pacific healthcare ecosystem.

2. Asia Pacific Autotransfusion Devices Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Drivers: Growing surgical volumes driven by rising prevalence of cardiovascular disease and trauma; increasing governmental emphasis on blood safety and reduction of transfusion‑associated risks; expanding reimbursement frameworks for advanced medical devices; and heightened awareness of autotransfusion benefits among clinicians. Restraints: High upfront capital cost of autotransfusion systems, limited availability of trained personnel in rural settings, and regulatory heterogeneity across APAC nations. Challenges: Integration with existing blood management protocols and convincing stakeholders of long‑term cost savings despite initial investment. Opportunities: Development of compact, single‑use devices for ambulatory centers, digital integration for real‑time monitoring, and strategic partnerships with hospital networks to drive adoption in emerging economies such as Vietnam, Philippines, and Indonesia.

3. Asia Pacific Autotransfusion Devices Market Growth Trends - Current and emerging trends shaping the market?

The market is witnessing a shift toward miniaturized, disposable autotransfusion kits that cater to high‑turnover surgical suites and ambulatory settings. There is also a rising trend of integrating autotransfusion data with electronic health records (EHR) to enhance patient safety and enable analytics‑driven blood management. Partnerships between device manufacturers and regional distributors are accelerating market penetration, especially in China and India where private‑sector hospital growth is robust. Finally, increasing clinical studies that demonstrate reduced infection rates and shorter hospital stays are reinforcing the value proposition of autotransfusion.

4. COVID-19 Impact on the Asia Pacific Autotransfusion Devices Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially constrained elective surgeries, leading to a temporary dip in device utilization. However, the crisis amplified concerns about blood supply chain disruptions, prompting hospitals to adopt autotransfusion to conserve donor blood. Post‑pandemic, surgical backlogs combined with heightened awareness of blood safety have accelerated demand, positioning the market on a clear recovery path that aligns with the projected CAGR of 4.50% through 2032.

5. Asia Pacific Autotransfusion Devices Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is dominated by multinational firms such as BD, Haemonetics, Medtronic, and Fresenius SE & Co. KGaA, alongside specialized regional players like Braile Biomedica and Zimmer Biomet. Recent years have seen strategic acquisitions—e.g., larger firms acquiring niche technology startups—to broaden product portfolios and strengthen distribution networks. Joint ventures with local OEMs are also common, enabling faster regulatory clearance and market entry across diverse APAC jurisdictions.

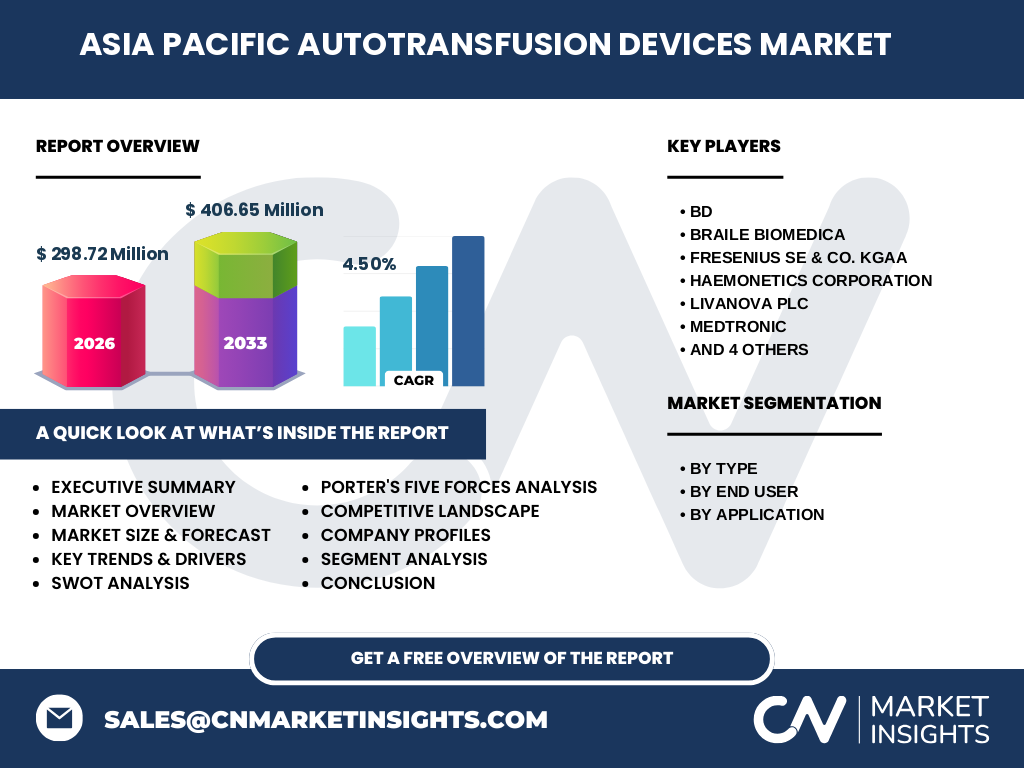

6. Executive Summary - High-level overview and key findings about Asia Pacific Autotransfusion Devices Market?

The Asia Pacific Autotransfusion Devices market was valued at USD 298.72 million in 2026 and is forecast to reach USD 406.65 million by 2033, expanding at a CAGR of 4.50%. Growth is propelled by expanding surgical volumes, government initiatives on blood safety, and technological innovations that lower device complexity. While capital intensity and fragmented regulatory environments pose challenges, opportunities abound in disposable device formats and digital integration. Leading players are consolidating through acquisitions and partnerships, positioning the market for sustained growth.

7. Asia Pacific Autotransfusion Devices Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 4.50%, the market is expected to progress steadily from the 2026 baseline of USD 298.72 million to approximately USD 406.65 million by 2033. This trajectory suggests a compound increase of roughly USD 108 million over seven years, reflecting steady adoption across hospital networks and the expanding role of ambulatory surgery centers. The forecast underscores a consistent upward trend, with each annual increment reinforced by incremental regulatory approvals and expanding clinical evidence.

8. Asia Pacific Autotransfusion Devices Market Size and Share by Segmentation - Breakdown by segment?

By Type: Products and accessories currently dominate, reflecting the recurring demand for consumables such as filters and anticoagulants. By End‑User: Hospitals account for the largest share, given the volume of cardiac and orthopedic surgeries, followed by specialty clinics and ambulatory surgery centers, which are gaining traction due to portable device solutions. By Application: Cardiac surgeries hold the strongest demand, driven by high blood loss and critical need for rapid reinfusion; orthopedic procedures follow, with trauma and organ transplantation representing niche but growing segments as surgical techniques evolve.

9. Global Asia Pacific Autotransfusion Devices Market Size and Share by Region - Geographic distribution?

The Asia Pacific region contributes the majority of global autotransfusion device revenues, reflecting its large population, expanding middle‑class, and rapid hospital infrastructure development. While exact regional split figures are not disclosed, the market’s growth driver is clearly the surge in surgical activities across China, Japan, India, and Southeast Asian economies.

10. Regional Analysis of the Asia Pacific Autotransfusion Devices Market - Detailed regional market performance?

China: The largest single‑country market, propelled by government‑backed initiatives to modernize operating rooms and improve blood management. India: Fastest‑growing due to increasing private hospital investments and a rising number of cardiac and orthopedic procedures. Japan & South Korea: Mature markets with high adoption of advanced autotransfusion technologies and strong regulatory frameworks. Southeast Asia (Indonesia, Vietnam, Philippines): Emerging markets where affordability and compact device designs are critical for market entry.

11. Leading Company Profiles in the Asia Pacific Autotransfusion Devices Market - Industry players and strategies?

BD: Leverages a broad product suite and strong service network to target tertiary hospitals. Haemonetics: Focuses on integrated blood management solutions and digital monitoring. Medtronic: Utilizes its cardiovascular portfolio to cross‑sell autotransfusion systems in cardiac centers. Fresenius SE & Co. KGaA: Emphasizes cost‑effective disposable kits for emerging markets. Zimmer Biomet: Aligns autotransfusion with its orthopedic implant business, offering bundled solutions. Other players such as Braile Biomedica and LivaNova pursue region‑specific product adaptations and strategic collaborations with local distributors.

12. Porter's Five Forces Analysis of the Asia Pacific Autotransfusion Devices Market - Competitive forces assessment?

Threat of New Entrants: Moderate; high capital requirements and regulatory barriers limit newcomers, but niche innovators can enter with disposable technologies. Bargaining Power of Suppliers: Low to moderate; component suppliers are numerous, though specialized filter media can command premium pricing. Bargaining Power of Buyers: Growing; large hospital groups negotiate volume discounts and demand integrated solutions. Threat of Substitutes: Low; allogenic blood transfusion remains a substitute but carries higher risk and cost. Industry Rivalry: High; established global players compete on technology, service contracts, and regional partnerships.

13. SWOT Analysis of the Asia Pacific Autotransfusion Devices Market - Strengths, weaknesses, opportunities, threats?

Strengths: Proven clinical benefits, alignment with patient‑safety agendas, and strong backing from leading medical‑device manufacturers. Weaknesses: High upfront equipment cost and need for skilled operators. Opportunities: Expansion into ambulatory surgery centers, development of single‑use compact systems, and integration with digital health platforms. Threats: Economic fluctuations affecting capital expenditure, regulatory delays in emerging economies, and potential competitive pressure from innovative blood‑conservation technologies.

14. Asia Pacific Autotransfusion Devices Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material suppliers (e.g., polymer films for filters), progresses to component manufacturers, then to device assemblers who integrate hardware with software for monitoring. After assembly, distributors and local importers handle regional logistics, followed by sales to hospitals and clinics. Post‑sale services—including training, maintenance contracts, and consumable replenishment—complete the chain, creating a recurring revenue stream that sustains long‑term relationships.

15. Key Investment Insights in the Asia Pacific Autotransfusion Devices Market - Strategic investment recommendations?

Investors should prioritize companies that offer a balanced portfolio of capital‑intensive systems and high‑margin consumables. Strategic investments in firms with strong distribution networks in China and India can accelerate market penetration. Additionally, funding R&D focused on disposable, portable autotransfusion kits aligns with the rising demand from ambulatory surgery centers, presenting a high‑growth niche. Partnerships or minority stakes in local innovators can also provide regulatory shortcuts and cultural insight.

16. Asia Pacific Autotransfusion Devices Market Conclusion - Summary and key takeaways?

The Asia Pacific Autotransfusion Devices market is on a solid growth path, moving from a USD 298.72 million base in 2026 to an anticipated USD 406.65 million by 2033, driven by a 4.50% CAGR. Core drivers include expanding surgical volumes, heightened focus on blood safety, and technological advances that lower device complexity. While capital costs and regulatory diversity pose challenges, opportunities in disposable technologies and digital integration create compelling upside. Leading global players are consolidating and localizing to capture the region’s vast potential.

17. Research Methodology - How this research was conducted?

The study combined primary interviews with key opinion leaders, hospital procurement officers, and regional distributors, together with secondary analysis of company annual reports, regulatory filings, and industry publications. Market sizing used a bottom‑up approach, aggregating revenue data from major manufacturers and adjusting for known market penetrations. Forecasting applied the provided CAGR of 4.50% and incorporated macro‑economic indicators for the Asia Pacific health‑care sector.

18. Research Scope - Coverage and limitations?

The report covers the full spectrum of autotransfusion devices—including hardware, consumables, and accessories—across hospitals, specialty clinics, and ambulatory surgery centers in the Asia Pacific region. Segmentation by type, end‑user, and application is included. Limitations stem from the confidentiality of exact regional revenue splits; therefore, the analysis relies on qualitative assessments and aggregated figures provided.

19. Key Companies and Recent Developments in the Asia Pacific Autotransfusion Devices Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent highlights include BD’s launch of an AI‑enabled monitoring module for its autotransfusion platform, aimed at enhancing real‑time decision making. Haemonetics announced a partnership with a leading Indian hospital chain to supply bundled autotransfusion kits and training services. Medtronic introduced a compact, single‑use system designed for ambulatory cardiac centers in Japan. Fresenius SE & Co. KGaA released a cost‑optimized disposable cartridge series targeting emerging markets in Southeast Asia. Zimmer Biomet integrated its autotransfusion devices with its flagship orthopedic implants, offering a seamless workflow for joint replacement surgeries. Braile Biomedica secured regulatory approval for a next‑generation cell‑salvage system in Brazil, positioning it for export to APAC. LivaNova and Teleflex have jointly explored digital connectivity solutions to link autotransfusion data with hospital EHR systems, reflecting the market’s move toward integrated health‑technology ecosystems.