1. What is the Asia Pacific Electric Water Heater Market overview – definition, scope, and significance?

The Asia Pacific Electric Water Heater (EWH) market comprises manufacturers, distributors, and end‑users of electric water heating solutions across the region. It includes both storage‑type and non‑storage (tank‑less) heaters deployed in residential, commercial, and industrial applications. The market’s significance stems from rising urbanisation, growing middle‑class disposable incomes, and stringent energy‑efficiency regulations that drive demand for reliable, low‑emission hot‑water systems.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Electric Water Heater market?

Key drivers include government incentives for energy‑saving appliances, increasing construction of high‑rise residential towers, and consumer preference for clean electricity over fossil fuels. Restraints involve higher upfront costs of premium electric units and limited grid reliability in some remote areas. Challenges arise from competition with gas‑based heaters and the need for skilled installation manpower. Opportunities exist in smart‑connected heaters, renewable‑energy integration, and retro‑fitting programs in older building stock.

3. What growth trends are currently influencing the Asia Pacific Electric Water Heater market?

Current trends feature a shift toward tank‑less designs for space‑constrained apartments, the incorporation of IoT sensors for predictive maintenance, and the rollout of higher‑efficiency standards (e.g., IEC 60335‑2‑15). Manufacturers are also expanding product portfolios with hybrid electric‑heat‑pump models that lower consumption while delivering consistent hot water, aligning with sustainability goals across the region.

4. How has COVID‑19 impacted the Asia Pacific Electric Water Heater market and what is the recovery trajectory?

The pandemic caused a temporary slowdown in construction activity and delayed consumer purchases, resulting in a modest dip in shipments during 2020‑21. However, post‑pandemic stimulus packages and a surge in residential renovation projects accelerated demand in 2022‑23. The market is now on a clear recovery path, supported by pent‑up demand and renewed focus on energy‑efficient home upgrades.

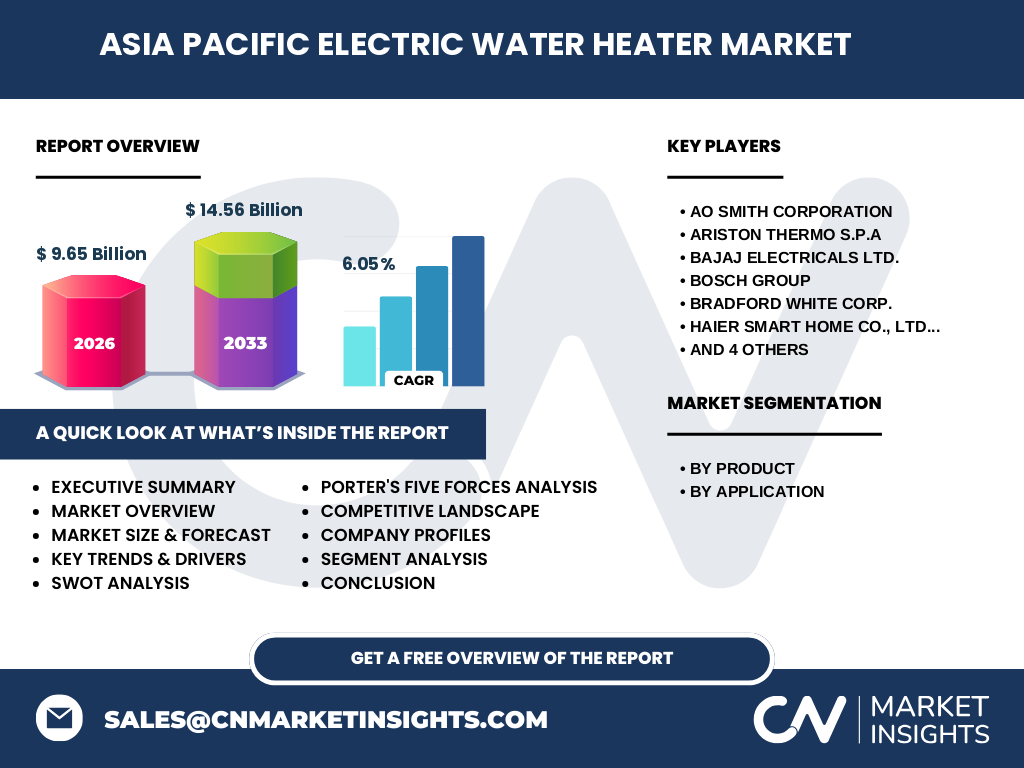

5. Who are the major competitors in the Asia Pacific Electric Water Heater market and what does the competitive landscape look like?

Key players include AO Smith Corporation, Ariston Thermo S.p.A, Bajaj Electricals Ltd., Bosch Group, Bradford White Corp., Haier Smart Home Co., Ltd., Midea Group, Siemens AG, Viesmann Group, and Whirlpool Corporation. The landscape is characterised by strategic alliances, joint ventures for local manufacturing, and frequent product launches aimed at differentiating on efficiency, smart connectivity, and after‑sales service.

6. What are the high‑level takeaways in the executive summary of the Asia Pacific Electric Water Heater market?

The market is valued at USD 9.65 billion in 2026 and is projected to reach USD 14.56 billion by 2033, expanding at a CAGR of 6.05 %. Growth is propelled by urban residential expansion, regulatory pushes for lower carbon emissions, and rapid adoption of advanced storage‑less technologies. Competitive intensity is rising as global OEMs localise production to meet price‑sensitive demand.

7. What are the forecast expectations for the Asia Pacific Electric Water Heater market from 2025 to 2032?

Based on the provided CAGR of 6.05 %, the market is expected to maintain steady expansion throughout 2025‑2032. Revenue will continue to climb beyond the 2027‑2033 forecast horizon, driven by increasing per‑capita hot‑water usage, government‑backed efficiency schemes, and the rollout of smart‑grid compatible heater models across the region.

8. How is the Asia Pacific Electric Water Heater market sized and shared by product and application segments?

Segmenting by product, the market is split between storage heaters—favoured in regions with stable power supply—and non‑storage (tank‑less) units, which are gaining traction in high‑density urban locales. By application, residential use dominates, followed by commercial facilities such as hotels and office complexes, with industrial usage representing a niche but growing segment for process‑heat requirements.

9. What is the geographic distribution of the Asia Pacific Electric Water Heater market by region?

The market’s geographic spread covers major economies such as China, India, Japan, South Korea, and Southeast Asian nations. While China and India together account for the largest share due to sheer population and construction volume, Japan and South Korea demonstrate higher per‑unit adoption rates thanks to mature building codes and consumer awareness of energy efficiency.

10. How does each region within Asia Pacific perform in the electric water heater market?

East Asia (Japan, South Korea) shows strong penetration of high‑efficiency models, driven by stringent standards. South‑East Asia (Indonesia, Vietnam, Thailand) exhibits rapid growth linked to new housing projects and rising electrification rates. South Asia (India, Bangladesh) presents the highest growth potential, with government subsidies encouraging electric heater uptake in both urban and semi‑urban markets.

11. Which leading companies are operating in the Asia Pacific Electric Water Heater market and what are their strategic focuses?

AO Smith leverages advanced coil technology and extensive dealer networks. Ariston focuses on premium design and smart‑home integration. Bajaj emphasizes affordable, locally‑manufactured units for mass‑market penetration. Bosch and Siemens prioritize energy‑saving certifications and industrial‑grade reliability. Haier and Midea expand through aggressive pricing and regional production hubs. Viesmann and Bradford White target niche high‑end segments with specialised features.

12. What does Porter’s Five Forces analysis reveal about the Asia Pacific Electric Water Heater market?

• Threat of new entrants: Moderate, due to high capital requirements and compliance costs. • Bargaining power of suppliers: Low to moderate, as key components (heating elements, control electronics) are sourced globally. • Bargaining power of buyers: High, driven by price‑sensitive residential customers and competitive retail channels. • Threat of substitutes: Moderate, with gas heaters and solar thermal solutions competing in select markets. • Industry rivalry: High, given the presence of numerous global and regional players vying for market share.

13. What are the SWOT insights for the Asia Pacific Electric Water Heater market?

Strengths: Clean energy appeal, growing urban demand, supportive regulations. Weaknesses: Higher upfront cost, dependence on electricity reliability. Opportunities: Smart‑connected devices, hybrid heat‑pump systems, government‑backed rebate programmes. Threats: Gas‑heater price competitiveness, fluctuating electricity tariffs, supply‑chain disruptions for electronic components.

14. How is the value chain structured for the Asia Pacific Electric Water Heater market?

The value chain begins with raw‑material suppliers (copper, steel, electronics), proceeds to component manufacturers (heating elements, thermostats), then to OEM assembly plants often located in China, India, or Vietnam. Distribution channels include wholesale distributors, online marketplaces, and retail chains. After‑sales service, installation, and maintenance form the final value‑adding stages, crucial for customer retention.

15. What investment insights can be drawn for stakeholders interested in the Asia Pacific Electric Water Heater market?

Investors should focus on companies with strong local manufacturing footprints and diversified product portfolios that include smart and hybrid models. Partnerships with utilities for demand‑response programs present upside potential. Funding retro‑fit incentives and green‑finance schemes can accelerate market uptake, making early‑stage capital allocation to innovative OEMs attractive.

16. What are the concluding takeaways from the Asia Pacific Electric Water Heater market analysis?

The market is on a robust growth trajectory, underpinned by a 6.05 % CAGR and expanding demand across residential and commercial sectors. Energy‑efficiency mandates, urbanisation, and technological advancement create a favourable environment for both established OEMs and emerging innovators. Strategic positioning around smart connectivity and cost‑effective solutions will be decisive for long‑term success.

17. How was the research for this market report conducted?

The study combined primary interviews with industry executives, distributors, and end‑users, alongside secondary data from government publications, trade associations, and reputable market databases. Trend analysis, comparative benchmarking, and forecasting models anchored on the provided CAGR were applied to produce the quantitative outlook.

18. What is the scope of this research and are there any limitations?

The scope covers the entire Asia Pacific region, focusing on electric water‑heater products and applications (residential, commercial, industrial). It analyses major manufacturers, segmentation, and forward‑looking forecasts up to 2033. While comprehensive, the study does not include granular country‑level market shares beyond the regional aggregation provided.

19. Which key companies have made notable recent developments in the Asia Pacific Electric Water Heater market?

AO Smith announced a joint‑venture plant in Vietnam to serve Southeast Asian demand. Ariston launched a Wi‑Fi‑enabled tank‑less heater with AI‑based energy optimisation. Bajaj introduced a low‑cost storage heater tailored for the Indian mass market. Bosch released a hybrid heat‑pump water heater for commercial buildings in Japan. Haier and Midea expanded their smart‑home ecosystems, integrating water‑heater control with voice assistants, while Siemens partnered with regional utilities to pilot demand‑response programmes.