Asia Pacific Tax Software Market Overview - Definition, scope, and significance?

The Asia Pacific Tax Software Market comprises solutions that automate tax calculation, filing, compliance, and reporting for entities operating in the Asia‑Pacific region. It includes both software products (stand‑alone applications, modules, and platforms) and services (implementation, consulting, and support). The market serves a diverse set of end‑users, ranging from individual taxpayers to commercial enterprises across various tax types such as sales tax, income tax, and corporate tax. Deployment options span cloud‑based and on‑premise models, enabling flexibility for organizations of all sizes. The significance of this market lies in its ability to reduce manual tax processing errors, ensure regulatory compliance in a region characterized by rapidly evolving tax legislations, and provide real‑time analytics that support strategic financial decision‑making.

Asia Pacific Tax Software Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the increasing complexity of tax regimes in countries like China, India, and Australia, coupled with heightened enforcement and digital filing mandates. Growing adoption of cloud computing and digital transformation initiatives among enterprises accelerate demand for scalable tax solutions. Meanwhile, restraints arise from legacy system integration issues and data security concerns, especially for on‑premise deployments. Challenges stem from a fragmented regulatory landscape, requiring vendors to continuously update software for each jurisdiction. Opportunities are evident in the expansion of SME‑focused cloud offerings, the rise of AI‑driven compliance analytics, and cross‑border e‑commerce growth, which creates a need for multi‑jurisdictional tax engines.

Asia Pacific Tax Software Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward cloud‑native architectures, enabling real‑time tax calculation and seamless integration with ERP and accounting suites. Vendors are embedding machine‑learning algorithms to predict audit risks and automate anomaly detection. An emerging trend is the adoption of API‑first platforms that allow companies to connect tax engines with custom applications, supporting the burgeoning gig‑economy and platform‑based businesses. Additionally, there is a growing focus on mobile‑enabled compliance, giving taxpayers the ability to file returns and access reports from smartphones.

COVID-19 Impact on the Asia Pacific Tax Software Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic accelerated digital adoption as businesses shifted to remote operations, prompting a surge in demand for cloud‑based tax solutions that support distributed workforces. Regulatory bodies also introduced temporary relief measures and new filing timelines, creating a need for agile software updates. While the initial lockdowns caused short‑term project delays, the overall market rebounded quickly, with a robust recovery trajectory that contributed to the strong CAGR of 13.03% projected through 2033.

Asia Pacific Tax Software Market Competitive Landscape - Major competitors and market consolidation?

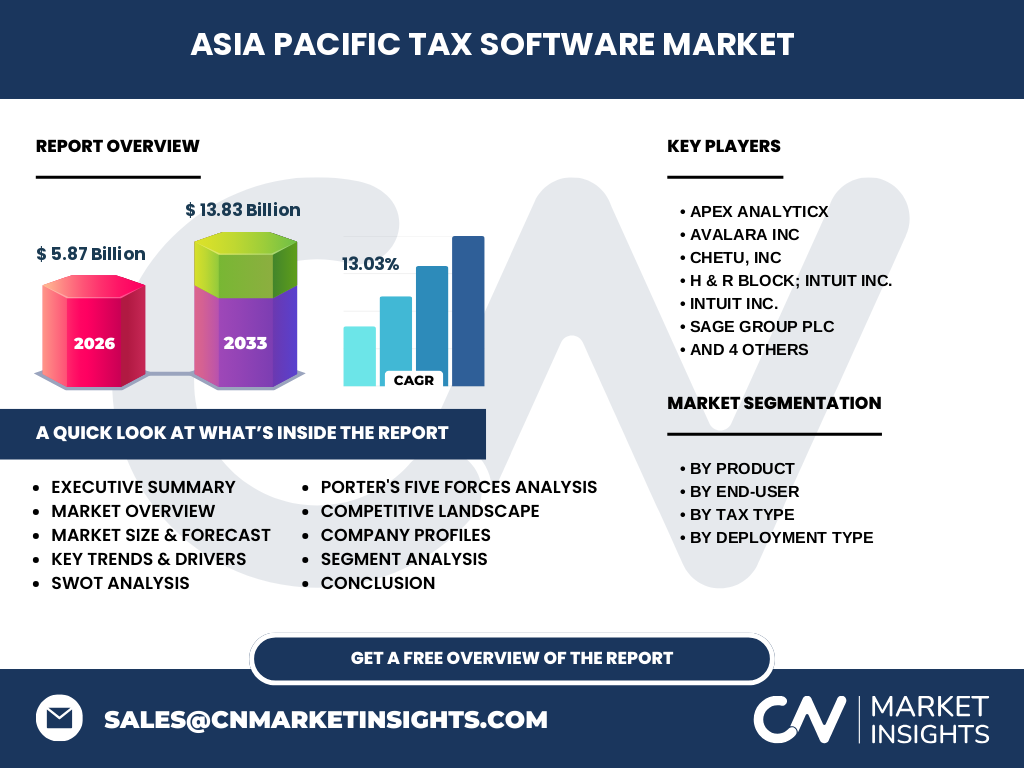

The market is fragmented with several global and regional players competing on breadth of coverage and depth of functionality. Leading firms include Apex Analyticx, Avalara Inc., Chetu, Inc., H&R Block; Intuit Inc., Sage Group PLC, Thomson Reuters Corporation, Vertex, Inc., Wolters Kluwer N.V., and Xero Limited. Recent years have witnessed strategic mergers and acquisitions, such as larger providers acquiring niche cloud start‑ups to broaden jurisdictional coverage and enhance AI capabilities, leading to gradual consolidation among the top‑tier vendors.

Executive Summary - High-level overview and key findings about Asia Pacific Tax Software Market?

The Asia Pacific Tax Software Market is valued at US$5.87 billion in 2026 and is projected to reach US$13.83 billion by 2033, driven by a 13.03% CAGR. Growth is propelled by escalating tax complexity, cloud adoption, and regulatory digitalization. Cloud deployment dominates due to scalability, while SMEs represent a rapidly expanding segment. Competitive dynamics are shaped by a blend of multinational incumbents and innovative niche players, with consolidation activities intensifying. The market presents strong investment potential, especially in AI‑enhanced, API‑centric solutions.

Asia Pacific Tax Software Market Forecast - Projections for 2025-2032 period?

Building on the provided CAGR of 13.03%, the market is expected to maintain a high‑single‑digit to low‑double‑digit growth rate throughout the 2025‑2032 horizon. By 2032, the market size is anticipated to approach US$12 billion, reflecting continued expansion of cloud services, increased compliance requirements, and digital transformation initiatives across the region.

Asia Pacific Tax Software Market Size and Share by Segmentation - Breakdown by segment?

Segmentation analysis reveals that software accounts for the larger share of the market, driven by continuous product upgrades and feature expansions. Service revenue grows steadily as clients seek implementation and support. By end‑user, commercial enterprises dominate due to complex tax obligations, while individuals show modest but steady growth fueled by user‑friendly filing apps. Regarding tax type, corporate tax solutions hold the highest value, followed by sales tax and income tax modules. Deployment trends indicate a clear preference for cloud solutions, with on‑premise still relevant for regulated industries requiring data residency.

Global Asia Pacific Tax Software Market Size and Share by Region - Geographic distribution?

The Asia Pacific region accounts for the majority of the market’s revenue, underpinned by large economies such as China, India, Japan, and Australia. Within the region, East Asia (China, Japan, South Korea) contributes the highest share, while South‑East Asia (Singapore, Malaysia, Indonesia) shows the fastest growth rate due to expanding e‑commerce and digital tax initiatives.

Regional Analysis of the Asia Pacific Tax Software Market - Detailed regional market performance?

In China, strict VAT reforms and digital invoice mandates drive demand for integrated tax engines. India’s GST regime fuels adoption of cloud tax platforms that can handle multi‑state compliance. Japan emphasizes robust audit trails, prompting vendors to enhance security features. Australia focuses on real‑time tax reporting for businesses, spurring growth in SaaS offerings. Southeast Asian markets benefit from government push for electronic filing, creating fertile ground for both local and global vendors.

Leading Company Profiles in the Asia Pacific Tax Software Market - Industry players and strategies?

Avalara Inc. leverages a vast network of tax content partners and a cloud‑first model to provide real‑time tax calculation across 200+ jurisdictions. Intuit Inc. integrates tax filing into its popular accounting suite, targeting small businesses and individuals. Thomson Reuters Corporation offers comprehensive corporate tax solutions with strong analytics capabilities for large enterprises. Wolters Kluwer N.V. focuses on regulatory intelligence and compliance reporting. Xero Limited differentiates through a seamless user experience for SMEs, coupling accounting and tax functions in a single platform. Each company pursues strategic partnerships, acquisitions, and AI‑driven product enhancements to deepen market penetration.

Porter's Five Forces Analysis of the Asia Pacific Tax Software Market - Competitive forces assessment?

Threat of new entrants is moderate; high development costs and the need for extensive tax content across jurisdictions create barriers. Bargaining power of buyers is growing as enterprises demand multi‑jurisdictional, scalable solutions, prompting vendors to offer tiered pricing. Bargaining power of suppliers (technology providers, data aggregators) is low to moderate, given multiple sourcing options. Threat of substitutes remains low because alternative compliance methods (manual processing) are inefficient and risky. Industry rivalry is intense, fueled by product differentiation, service quality, and aggressive pricing strategies among the leading firms.

SWOT Analysis of the Asia Pacific Tax Software Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong demand driven by regulatory complexity; increasing cloud adoption; AI‑enhanced compliance capabilities.

Weaknesses: Fragmented tax regulations requiring continuous updates; integration challenges with legacy ERP systems.

Opportunities: Expansion into underserved SME segment; development of AI‑based audit risk modules; cross‑border e‑commerce tax solutions.

Threats: Data privacy regulations affecting cloud deployment; rapid technological changes requiring constant innovation; competitive pressure from emerging regional startups.

Asia Pacific Tax Software Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with tax data aggregation (government APIs, third‑party data providers), followed by software development (core tax engine, UI/UX, AI modules). Next, implementation services (consulting, customization) add value for enterprise clients. Distribution occurs via SaaS platforms, reseller networks, and direct sales. Ongoing support and maintenance, including regulatory updates, form the final value‑adding stage, ensuring customer retention and recurring revenue.

Key Investment Insights in the Asia Pacific Tax Software Market - Strategic investment recommendations?

Investors should target cloud‑native vendors with robust API ecosystems, as they are positioned to capture the growing SME and e‑commerce segments. Companies that integrate machine‑learning analytics for audit risk and offer multi‑jurisdictional coverage present higher upside. Strategic M&A in niche AI or region‑specific tax content providers can accelerate market entry and expand product portfolios.

Asia Pacific Tax Software Market Conclusion - Summary and key takeaways?

The Asia Pacific Tax Software Market is on a rapid growth trajectory, underpinned by regulatory complexity, digital transformation, and strong cloud adoption. With a projected market size of US$13.83 billion by 2033 and a 13.03% CAGR, the sector offers substantial opportunities for vendors and investors alike. Success will depend on delivering scalable, AI‑enabled, and jurisdiction‑rich solutions that address both enterprise and SME needs.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, vendor executives, and end‑user representatives, alongside secondary data collection from annual reports, regulatory publications, and market databases. Quantitative projections were derived using the provided baseline figures (2026 market size of US$5.87 billion) and the stipulated CAGR of 13.03% to estimate future values.

Research Scope - Coverage and limitations?

The scope encompasses the full spectrum of tax software solutions across the Asia Pacific, segmented by product, end‑user, tax type, and deployment model. Geographic coverage includes major economies and emerging markets within the region. The analysis focuses on market size, growth drivers, competitive dynamics, and forward‑looking forecasts up to 2033. While comprehensive, the study does not extend to detailed country‑level revenue breakdowns beyond the regional trends outlined.

Key Companies and Recent Developments in the Asia Pacific Tax Software Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Avalara Inc. announced a partnership with major cloud ERP providers to embed real‑time tax calculation APIs. Intuit Inc. launched an AI‑powered self‑service tax filing module for individuals in India. Thomson Reuters Corporation acquired a regional tax content specialist to enhance its corporate tax offering in Southeast Asia. Wolters Kluwer N.V. introduced a cloud‑based compliance dashboard tailored for Japanese corporations. Xero Limited expanded its SME tax suite with localized sales tax rules for Australia and New Zealand. These developments illustrate the industry's focus on AI, localization, and ecosystem integration.