Data Center Cooling Market Overview - Definition, scope, and significance

Data center cooling refers to the systems and technologies designed to regulate temperature, humidity, and air quality within data center facilities where servers and IT infrastructure generate substantial heat. This market encompasses various cooling solutions including air conditioning systems, chillers, cooling towers, heat exchangers, and specialized cooling units tailored for different data center architectures. The significance of this market has grown exponentially as data centers have become the backbone of digital infrastructure, supporting cloud computing, artificial intelligence, big data analytics, and the increasing demand for real-time data processing. Effective cooling solutions are critical for maintaining optimal operating temperatures, preventing equipment failure, reducing energy consumption, and ensuring business continuity for organizations that depend on uninterrupted digital services.

Data Center Cooling Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The data center cooling market is primarily driven by the exponential growth in data generation, the proliferation of cloud computing services, and the increasing adoption of energy-efficient cooling technologies. The rising demand for hyperscale data centers and edge computing facilities creates significant opportunities for innovative cooling solutions. However, the market faces restraints including high initial investment costs for advanced cooling systems, the complexity of retrofitting existing facilities, and the need for specialized technical expertise. Challenges include managing the increasing power density of modern servers, addressing water scarcity concerns in cooling tower operations, and meeting stringent environmental regulations. Opportunities exist in developing liquid cooling technologies, AI-driven cooling optimization systems, and sustainable cooling solutions that reduce carbon footprints while improving energy efficiency.

Data Center Cooling Market Growth Trends - Current and emerging trends shaping the market

The data center cooling market is experiencing transformative growth trends driven by technological advancements and changing infrastructure requirements. One prominent trend is the shift toward liquid cooling solutions, including direct-to-chip and immersion cooling technologies, which offer superior heat removal efficiency compared to traditional air cooling. The adoption of AI and machine learning for predictive cooling management is enabling data centers to optimize energy consumption and reduce operational costs. Edge computing expansion is driving demand for compact, efficient cooling solutions in distributed facilities. Additionally, the integration of renewable energy sources with cooling systems and the development of free cooling techniques are gaining traction. The market is also witnessing increased focus on modular and scalable cooling architectures that can adapt to rapidly changing IT workloads and density requirements.

COVID-19 Impact on the Data Center Cooling Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a paradoxical impact on the data center cooling market, initially causing supply chain disruptions and project delays while simultaneously accelerating demand for digital infrastructure. As lockdowns and remote work became widespread, the reliance on cloud services, video conferencing, and online platforms surged dramatically, driving rapid expansion of data center capacity. This unexpected demand spike created urgent requirements for additional cooling infrastructure to support increased server loads and higher power densities. While some projects faced delays due to component shortages and logistical challenges, the overall market demonstrated resilience and accelerated growth as organizations prioritized digital transformation initiatives. The pandemic ultimately highlighted the critical importance of robust, scalable data center infrastructure, leading to sustained investment in cooling technologies that support higher efficiency and reliability.

Data Center Cooling Market Competitive Landscape - Major competitors and market consolidation

The data center cooling market features a mix of established industrial giants and specialized technology providers competing for market share through innovation and strategic partnerships. Major players like Carrier Global Corp, Daikin Industries Ltd, and Trane Technologies Plc leverage their extensive HVAC expertise and global distribution networks, while companies such as Vertiv Group Corp and Schneider Electric SE focus on integrated data center infrastructure solutions. The market is witnessing consolidation through mergers and acquisitions as larger companies acquire specialized cooling technology firms to expand their product portfolios. Competitive differentiation is achieved through technological innovation, energy efficiency improvements, and the development of sustainable cooling solutions. Companies are also competing on their ability to provide customized solutions for specific data center types, from hyperscale facilities to edge computing locations, while building strong service and maintenance capabilities to ensure long-term customer relationships.

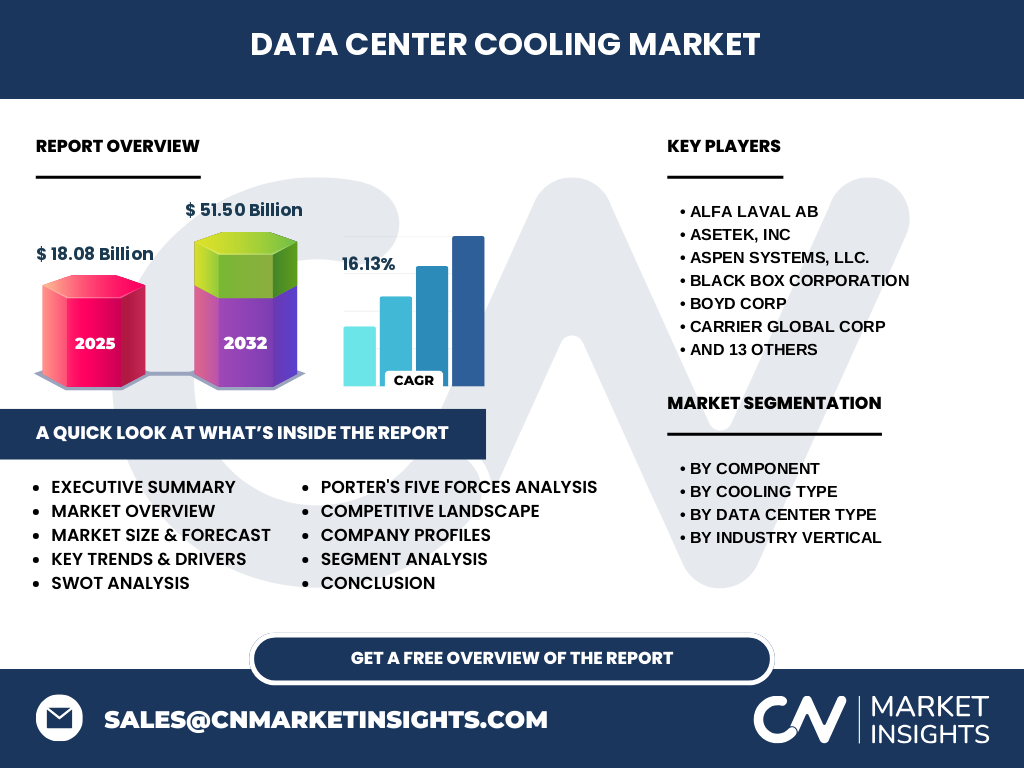

Executive Summary - High-level overview and key findings about Data Center Cooling Market

The global data center cooling market is experiencing robust growth, driven by the exponential expansion of digital infrastructure and the increasing demand for energy-efficient cooling solutions. With a market size of 18.08 Billion in 2025 and projected to reach 51.50 Billion by 2032, representing a CAGR of 16.13%, the market demonstrates strong growth potential across all segments and regions. The shift toward higher-density computing, the proliferation of AI and machine learning applications, and the expansion of cloud services are creating unprecedented demand for advanced cooling technologies. Liquid cooling solutions and AI-driven optimization systems are emerging as key differentiators in the competitive landscape. The market is characterized by rapid technological innovation, strategic partnerships, and increasing focus on sustainability, with companies investing heavily in R&D to develop next-generation cooling solutions that address both performance and environmental concerns.

Data Center Cooling Market Forecast - Projections for 2025-2032 period

The data center cooling market is projected to experience substantial growth from 2025 to 2032, expanding from 18.08 Billion to 51.50 Billion, representing a compound annual growth rate of 16.13%. This growth trajectory is driven by several factors including the continued expansion of cloud computing infrastructure, the increasing adoption of AI and high-performance computing, and the growing emphasis on energy efficiency and sustainability. The forecast period will likely see accelerated adoption of advanced cooling technologies such as liquid cooling and AI-optimized systems, particularly in hyperscale data centers and regions with high computational demands. Market growth will be influenced by technological advancements, regulatory pressures for energy efficiency, and the ongoing digital transformation across industries. The Asia-Pacific region is expected to show particularly strong growth due to rapid digitalization and increasing data center construction, while North America and Europe will continue to lead in technology adoption and innovation.

Data Center Cooling Market Size and Share by Segmentation - Breakdown by {segmentData}

The data center cooling market segmentation reveals distinct growth patterns across different components, cooling types, data center types, and industry verticals. By component, air conditioning systems and chillers dominate the market due to their widespread adoption in traditional data centers, while emerging segments like cooling towers and heat exchangers are gaining traction in large-scale facilities. Room-based cooling currently holds the largest share, but row-based and rack-based cooling solutions are experiencing rapid growth as data centers adopt more granular cooling approaches. Hyperscale data centers represent the fastest-growing segment, driven by major cloud providers' expansion, while enterprise data centers continue to invest in modernization. The IT and telecom sector leads in cooling demand, followed closely by BFSI and healthcare industries, with manufacturing and government sectors showing increasing adoption as they digitize operations and require robust data infrastructure.

Global Data Center Cooling Market Size and Share by Region - Geographic distribution

The global data center cooling market exhibits significant regional variations in growth rates and adoption patterns, influenced by factors such as digital infrastructure development, energy costs, and regulatory environments. North America currently dominates the market, driven by the presence of major cloud service providers, advanced technological infrastructure, and substantial investments in data center construction. Europe follows closely, with strong emphasis on energy efficiency and sustainable cooling solutions due to stringent environmental regulations. The Asia-Pacific region is emerging as the fastest-growing market, fueled by rapid digitalization, increasing internet penetration, and significant investments in data center infrastructure across countries like China, India, and Singapore. Latin America and the Middle East & Africa regions are experiencing steady growth, driven by digital transformation initiatives and the establishment of new data center facilities to support growing digital economies.

Regional Analysis of the Data Center Cooling Market - Detailed regional market performance

Regional analysis of the data center cooling market reveals distinct market dynamics and growth drivers across different geographic areas. North America, particularly the United States, leads in market maturity and technology adoption, with a strong focus on innovative cooling solutions and sustainable practices. The region benefits from established data center infrastructure and significant investments from major technology companies. Europe emphasizes energy efficiency and environmental sustainability, with countries like Germany, the UK, and the Nordic nations leading in the adoption of free cooling and renewable energy integration. The Asia-Pacific region, led by China, Japan, and Singapore, shows the highest growth potential due to rapid digitalization, increasing data consumption, and substantial investments in new data center construction. Emerging markets in Southeast Asia and India present significant opportunities for cooling solution providers as these regions expand their digital infrastructure to support growing economies.

Leading Company Profiles in the Data Center Cooling Market - Industry players and strategies

The data center cooling market features several prominent players employing diverse strategies to maintain competitive advantage and capture market share. Alfa Laval AB specializes in heat transfer technologies and has expanded its data center cooling portfolio through innovative plate heat exchanger solutions. Asetek, Inc leads in liquid cooling solutions, particularly for high-performance computing applications, while Vertiv Group Corp offers comprehensive infrastructure solutions including advanced cooling systems and services. Schneider Electric SE integrates cooling solutions with its broader data center infrastructure offerings, emphasizing energy efficiency and sustainability. Daikin Industries Ltd leverages its HVAC expertise to provide scalable cooling solutions for various data center types. These companies focus on strategic partnerships, R&D investments, and geographic expansion to strengthen their market positions. Many are also investing in sustainable cooling technologies and AI-driven optimization systems to address evolving customer needs and regulatory requirements.

Porter's Five Forces Analysis of the Data Center Cooling Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the data center cooling market. The threat of new entrants is moderate due to high capital requirements and the need for technical expertise, though innovative startups focusing on specialized cooling technologies can still enter the market. Bargaining power of buyers is increasing as data center operators become more knowledgeable about cooling technologies and demand customized, energy-efficient solutions. The bargaining power of suppliers is moderate, with component suppliers having some influence, particularly for specialized cooling equipment. The threat of substitutes is relatively low, as traditional cooling methods remain essential, though emerging technologies like liquid cooling are gradually replacing conventional air-based systems. Competitive rivalry is intense, with numerous established players and regional competitors competing on technology, price, and service quality. The market is characterized by rapid technological innovation, making continuous R&D investment crucial for maintaining competitive advantage.

SWOT Analysis of the Data Center Cooling Market - Strengths, weaknesses, opportunities, threats

The data center cooling market exhibits distinct strengths including the essential nature of cooling solutions for data center operations, continuous technological innovation, and growing demand driven by digital transformation. The market benefits from strong growth fundamentals and the increasing complexity of IT infrastructure requiring sophisticated cooling solutions. However, weaknesses include high initial costs for advanced cooling systems, dependence on energy prices, and the complexity of integrating new technologies with existing infrastructure. Opportunities abound in the form of emerging technologies like liquid cooling and AI-driven optimization, expansion into developing markets, and the growing focus on sustainable and energy-efficient solutions. Threats include potential economic downturns affecting IT spending, regulatory changes regarding energy consumption and environmental impact, and the rapid pace of technological change that could render existing solutions obsolete. The market must also navigate challenges related to water scarcity and the environmental impact of cooling operations.

Data Center Cooling Market Value Chain Analysis - Industry structure and value flow

The data center cooling market value chain encompasses multiple stages from raw material suppliers to end-users, with each segment playing a crucial role in delivering comprehensive cooling solutions. Raw material suppliers provide essential components such as copper, aluminum, and specialized polymers used in heat exchangers and cooling equipment. Component manufacturers produce critical parts including compressors, pumps, and heat transfer units that form the foundation of cooling systems. Original Equipment Manufacturers (OEMs) assemble these components into complete cooling solutions, incorporating advanced technologies and design innovations. System integrators and solution providers customize and implement cooling systems for specific data center requirements, while distributors and channel partners facilitate market reach and customer support. End-users, primarily data center operators and IT companies, represent the final stage, driving demand through their infrastructure expansion and modernization initiatives. Service providers offering maintenance, optimization, and support services complete the value chain, ensuring long-term system performance and customer satisfaction.

The data center cooling market presents compelling investment opportunities driven by strong growth fundamentals and technological innovation. Investors should focus on companies developing advanced cooling technologies such as liquid cooling, AI-driven optimization systems, and sustainable solutions that address both performance and environmental concerns. Strategic investments in emerging markets, particularly in Asia-Pacific and developing regions, offer significant growth potential as digital infrastructure expands. The market also presents opportunities in companies offering integrated solutions that combine cooling with power management and monitoring capabilities. Investors should consider companies with strong R&D capabilities, established customer relationships, and proven track records in innovation and market expansion. Additionally, investments in companies focusing on energy-efficient and environmentally sustainable cooling solutions are likely to benefit from increasing regulatory pressures and customer demand for green technologies. The market's projected CAGR of 16.13% and expansion from 18.08 Billion to 51.50 Billion by 2032 indicate strong long-term investment potential.

Data Center Cooling Market Conclusion - Summary and key takeaways

The data center cooling market stands at a critical juncture, characterized by rapid technological advancement, strong growth projections, and increasing emphasis on sustainability and efficiency. With a projected CAGR of 16.13% and market expansion from 18.08 Billion to 51.50 Billion by 2032, the market demonstrates robust growth potential driven by the exponential increase in data generation, cloud computing adoption, and the proliferation of AI and high-performance computing applications. The shift toward advanced cooling technologies, particularly liquid cooling and AI-optimized systems, represents a fundamental transformation in how data centers manage thermal loads. Companies that can innovate effectively, address sustainability concerns, and provide integrated solutions across different data center types and regions are well-positioned for success. The market's future will be shaped by technological innovation, regulatory pressures, and the ongoing digital transformation across industries, making it a dynamic and essential component of the global digital infrastructure ecosystem.

Research Methodology - How this research was conducted

This comprehensive market research was conducted using a rigorous methodology combining primary and secondary research approaches to ensure accuracy and reliability. Primary research involved interviews with industry experts, data center operators, technology providers, and key stakeholders across the value chain to gather firsthand insights and validate market trends. Secondary research included extensive analysis of company annual reports, financial statements, industry publications, market databases, and regulatory documents to establish market size, growth rates, and competitive landscape. The research methodology employed both top-down and bottom-up approaches to estimate market size and validate findings across different segments and regions. Data triangulation techniques were used to cross-verify information from multiple sources, ensuring consistency and reliability. The research also incorporated analysis of patent filings, technology trends, and regulatory developments to provide comprehensive market intelligence and future projections.

Research Scope - Coverage and limitations

This research provides comprehensive coverage of the global data center cooling market, encompassing all major segments including components, cooling types, data center types, and industry verticals across key geographic regions. The scope includes detailed analysis of market size, growth trends, competitive landscape, and future projections from 2025 to 2032. However, the research has certain limitations, including the exclusion of highly specialized niche cooling technologies and emerging experimental solutions still in early development stages. The study focuses primarily on commercial data center applications and may not fully capture cooling requirements for specialized research facilities or military installations. Additionally, while regional analysis is comprehensive, certain developing markets may have limited available data due to information constraints. The research also assumes continued technological advancement and market stability, which may be affected by unforeseen economic, regulatory, or technological disruptions.

Key Companies and Recent Developments in the Data Center Cooling Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The data center cooling market features several key players driving innovation and market expansion through strategic initiatives and technological advancements. Alfa Laval AB recently announced expansion of its heat exchanger portfolio specifically designed for high-density data center applications, focusing on improved thermal efficiency. Asetek, Inc launched new direct-to-chip liquid cooling solutions targeting AI and high-performance computing facilities, while Vertiv Group Corp introduced integrated cooling systems with advanced monitoring and optimization capabilities. Schneider Electric SE formed strategic partnerships with major cloud providers to develop sustainable cooling solutions and announced AI-driven cooling optimization software. Daikin Industries Ltd expanded its presence in emerging markets through new manufacturing facilities and distribution partnerships. Carrier Global Corp acquired several specialized cooling technology companies to enhance its data center portfolio, while Trane Technologies Plc launched next-generation chillers with improved energy efficiency ratings. These companies continue to invest in R&D, pursue strategic acquisitions, and form partnerships to strengthen their market positions and address evolving customer needs in the rapidly growing data center cooling market.