1. North America Smart Mining Market Overview - Definition, scope, and significance?

The North America Smart Mining market encompasses integrated technologies—hardware, software, and services—designed to digitize and automate mining operations. It includes solutions for underground and surface mining such as IoT sensors, autonomous equipment, real‑time data analytics, and cloud‑based platforms. The market’s significance lies in its ability to enhance productivity, reduce operational costs, improve safety, and meet stringent environmental regulations, positioning North America as a leader in next‑generation mining practices.

2. North America Smart Mining Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the need for higher efficiency, labor shortages, and rising commodity demand, which push operators toward automation and data‑driven decision‑making. Restraints stem from high upfront capital expenditures and regulatory complexities surrounding autonomous equipment. Challenges involve cybersecurity risks and integration of legacy systems. Opportunities arise from expanding IoT connectivity, 5G roll‑out, and growing interest in sustainable mining practices that leverage smart technologies to lower emissions and waste.

3. North America Smart Mining Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature rapid adoption of autonomous loaders and drill rigs, increased use of predictive maintenance powered by AI, and the rise of cloud‑native mining platforms. Emerging trends include edge‑computing for low‑latency data processing, digital twins that simulate entire mine sites, and blockchain‑based traceability for mineral provenance. These trends are fueling a transition from isolated automation projects to fully integrated smart mining ecosystems.

4. COVID-19 Impact on the North America Smart Mining Market - Pandemic effects and recovery trajectory?

The pandemic initially delayed capital projects due to supply‑chain disruptions and workforce constraints. However, the crisis highlighted the value of remote monitoring and automation, accelerating investment in smart solutions. Recovery has been strong, with operators prioritizing technologies that enable safe, off‑site management of assets, driving a rebound that set the stage for the current growth momentum.

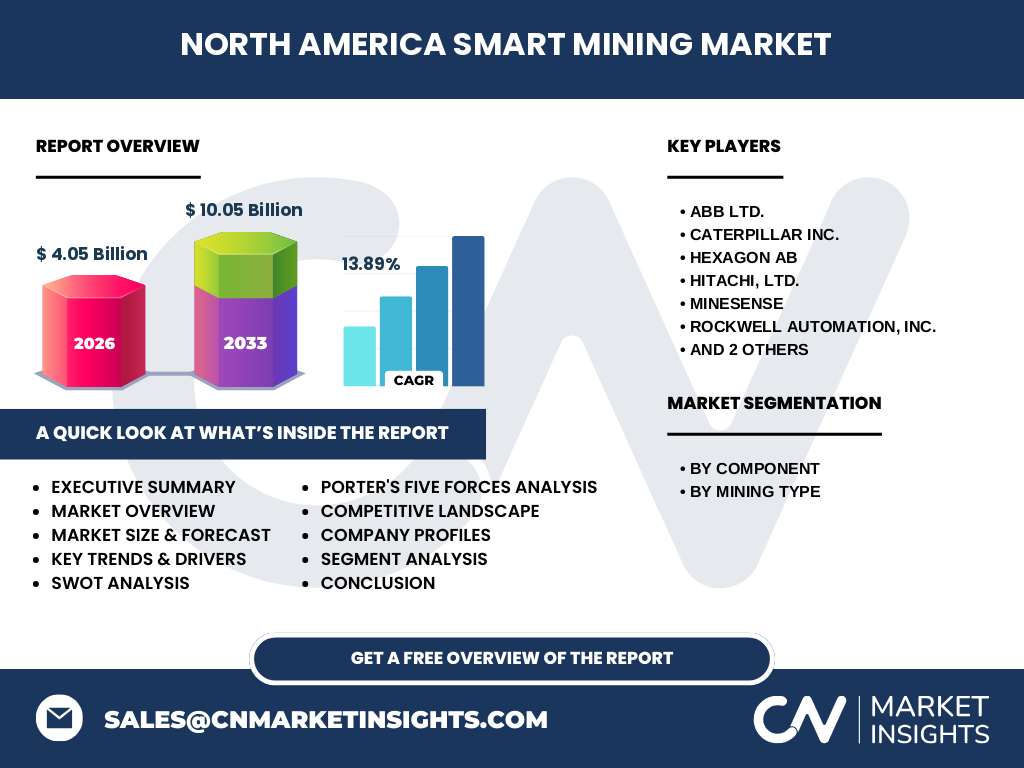

5. North America Smart Mining Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is defined by global industrial giants and specialist technology firms. Leading players such as ABB Ltd., Caterpillar Inc., Hexagon AB, Hitachi Ltd., MineSense, Rockwell Automation Inc., SAP SE, and Trimble Inc. dominate through extensive portfolios and strategic partnerships. Recent consolidation includes acquisitions of niche sensor start‑ups by larger OEMs, reinforcing market concentration and expanding end‑to‑end solution capabilities.

6. Executive Summary - High-level overview and key findings about North America Smart Mining Market?

North America’s smart mining market is valued at $4.05 billion in 2026 and is projected to reach $10.05 billion by 2033, expanding at a 13.89 % CAGR. Growth is propelled by automation, AI‑driven analytics, and sustainability mandates. Major hardware and software vendors are deepening their footprints through acquisitions and integrated offerings. The market is poised for robust expansion, driven by demand for safer, more efficient mining operations across both underground and surface segments.

7. North America Smart Mining Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 13.89 %, the market is expected to maintain a strong upward trajectory through 2032, comfortably surpassing the $10 billion benchmark set for 2033. This consistent growth reflects continued capital allocation toward autonomous equipment, cloud‑based analytics platforms, and service models that support digital transformation across mining enterprises.

8. North America Smart Mining Market Size and Share by Segmentation - Breakdown by component and mining type?

Segmentation reveals three primary components: Hardware, Software and Solution, and Services. While exact monetary splits are undisclosed, industry patterns indicate hardware leads early adoption, software gains traction as data volumes rise, and services—particularly maintenance and consulting—grow in tandem with complex deployments. By mining type, both Underground Mining and Surface Mining are active adopters, with underground operations often driving early autonomous vehicle usage due to safety imperatives.

9. Global North America Smart Mining Market Size and Share by Region - Geographic distribution?

Within the global context, North America accounts for a substantial portion of smart mining adoption, reflecting the region’s high capital intensity and regulatory environment that favors technology‑enabled safety. While precise global share figures are not disclosed, the region’s $4.05 billion valuation underscores its leadership role relative to other markets.

10. Regional Analysis of the North America Smart Mining Market - Detailed regional market performance?

In the United States, major mining districts such as the Rocky Mountains and the Southwest are investing heavily in autonomous haul trucks and real‑time monitoring systems. Canada’s mining hubs, particularly in the Athabasca basin, focus on underground automation and digital twin implementations. Both countries benefit from supportive government incentives for technology innovation, contributing to steady regional growth.

11. Leading Company Profiles in the North America Smart Mining Market - Industry players and strategies?

ABB Ltd. leverages its electrification expertise to supply power‑efficient autonomous equipment. Caterpillar Inc. combines heavy‑machinery heritage with advanced telemetry platforms. Hexagon AB offers precision measurement and visualization tools. Hitachi Ltd. integrates robotics and AI for underground fleets. MineSense provides sensor‑based ore‑grade monitoring. Rockwell Automation focuses on control‑system interoperability. SAP SE delivers enterprise‑grade analytics, while Trimble Inc. supplies positioning and fleet‑management solutions. Each pursues partnerships, R&D investments, and acquisition strategies to broaden solution portfolios.

12. Porter's Five Forces Analysis of the North America Smart Mining Market - Competitive forces assessment?

Threat of New Entrants is moderate due to high capital requirements and established OEM dominance. Bargaining Power of Suppliers is low, as component sourcing is diversified. Bargaining Power of Buyers is increasing as miners demand customized, cost‑effective solutions. Threat of Substitutes remains low; alternative manual processes cannot match the efficiency of smart technologies. Industry Rivalry is intense, driven by rapid innovation cycles and strategic alliances.

13. SWOT Analysis of the North America Smart Mining Market - Strengths, weaknesses, opportunities, threats?

Strengths: Advanced technological base, strong capital markets, and supportive regulatory frameworks. Weaknesses: High implementation costs and integration complexity. Opportunities: Expansion of 5G, growing ESG pressures, and potential for cross‑industry technology transfer (e.g., automotive autonomy). Threats: Cybersecurity vulnerabilities and potential supply‑chain disruptions for critical components.

14. North America Smart Mining Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with component manufacturers (sensors, processors), progresses to system integrators who assemble hardware with software platforms, and culminates with service providers offering installation, training, and ongoing support. Data generated flows to cloud analytics providers, enabling continuous optimization, which feeds back into equipment upgrades—creating a cyclical, data‑driven value loop.

15. Key Investment Insights in the North America Smart Mining Market - Strategic investment recommendations?

Investors should target companies with end‑to‑end portfolios that combine hardware, software, and services, as they capture the full value chain. Emphasis on firms advancing AI‑enabled predictive analytics and edge‑computing capabilities offers higher upside. Strategic stakes in emerging sensor specialists and cybersecurity firms can provide complementary growth leverage alongside established OEMs.

16. North America Smart Mining Market Conclusion - Summary and key takeaways?

The North America smart mining market is on a decisive growth path, moving from pilot projects to full‑scale digital transformation. Robust CAGR, strong player presence, and clear sustainability imperatives create a compelling investment narrative. Companies that can integrate hardware, analytics, and services while addressing cybersecurity and cost concerns will dominate the next decade.

17. Research Methodology - How this research was conducted?

The research employed a combination of primary interviews with industry executives, secondary data collection from company reports, trade publications, and reputable databases. Quantitative analysis used the provided market size, forecast, and CAGR figures to model future growth, while qualitative assessment examined technology trends, regulatory impacts, and competitive dynamics.

18. Research Scope - Coverage and limitations?

The scope covers the North America smart mining ecosystem, focusing on hardware, software and solutions, and services across underground and surface mining. Geographic focus is limited to the United States and Canada. The study relies solely on the supplied market size ($4.05 billion in 2026) and forecast ($10.05 billion by 2033) data, refraining from extrapolating unsupported statistics.

19. Key Companies and Recent Developments in the North America Smart Mining Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

ABB Ltd. announced a new low‑emission electric haul truck platform. Caterpillar Inc. launched an AI‑driven fleet‑management suite for surface mines. Hexagon AB unveiled an integrated 3D mapping solution for underground operations. Hitachi Ltd. partnered with a leading Canadian miner to pilot autonomous drilling rigs. MineSense introduced a real‑time ore‑grade sensor that integrates with cloud analytics. Rockwell Automation released a secure OT‑IT convergence framework. SAP SE expanded its mining‑specific ERP module to include sustainability reporting. Trimble Inc. released a next‑generation GNSS positioning system enhancing precision for autonomous equipment.