1. What is the Personal Care Wipes Market overview, including its definition, scope, and significance?

The Personal Care Wipes market comprises pre‑moistened disposable sheets formulated for hygiene, cleansing, or cosmetic purposes. Products span baby wipes, facial and cosmetic wipes, hand and body wipes, and flushable wipes, reaching consumers through supermarkets, specialty stores, online platforms, and commercial‑industrial channels. The market’s significance lies in its role as a convenient, on‑the‑go solution for personal hygiene and skin care, driving demand across demographics—from infants to active adults—while supporting broader trends of hygiene awareness, sustainability interest, and premium skin‑care routines.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Personal Care Wipes market?

Key drivers include rising consumer focus on hygiene post‑pandemic, expanding disposable‑income levels in emerging economies, and the launch of premium, additive‑enriched wipes (e.g., moisturizing, anti‑bacterial). Restraints stem from heightened environmental concerns over single‑use plastics and regulatory scrutiny on flushable claims. Challenges involve supply‑chain volatility for raw materials such as non‑woven fabrics and the need for cost‑effective reformulations to meet eco‑friendly standards. Opportunities arise from biodegradable substrate innovations, private‑label growth in online retail, and the integration of functional ingredients (vitamins, botanical extracts) that command higher price points.

3. Which growth trends are currently influencing the Personal Care Wipes market?

Current trends include a surge in “clean‑beauty” wipes that avoid parabens, sulfates, and synthetic fragrances, catering to health‑conscious buyers. Another trend is the expansion of flushable wipes marketed for travel and on‑the‑go sanitation, though they face regulatory pushback. Digital acceleration has boosted direct‑to‑consumer (DTC) sales, with subscription models gaining traction. Additionally, manufacturers are leveraging sustainable packaging—recyclable or compostable films—to differentiate products in a crowded shelf space.

4. How did COVID‑19 impact the Personal Care Wipes market, and what is the recovery trajectory?

The pandemic triggered a sharp uptick in demand for hand and body wipes as consumers sought additional protection against pathogens. Supply chains experienced temporary strain, prompting manufacturers to increase production capacity and diversify sourcing. Post‑2020, demand normalized but settled at a higher baseline than pre‑COVID levels, reflecting lasting hygiene habits. Recovery is now characterized by steady growth, supported by continued health awareness and the adoption of premium wipes for everyday use.

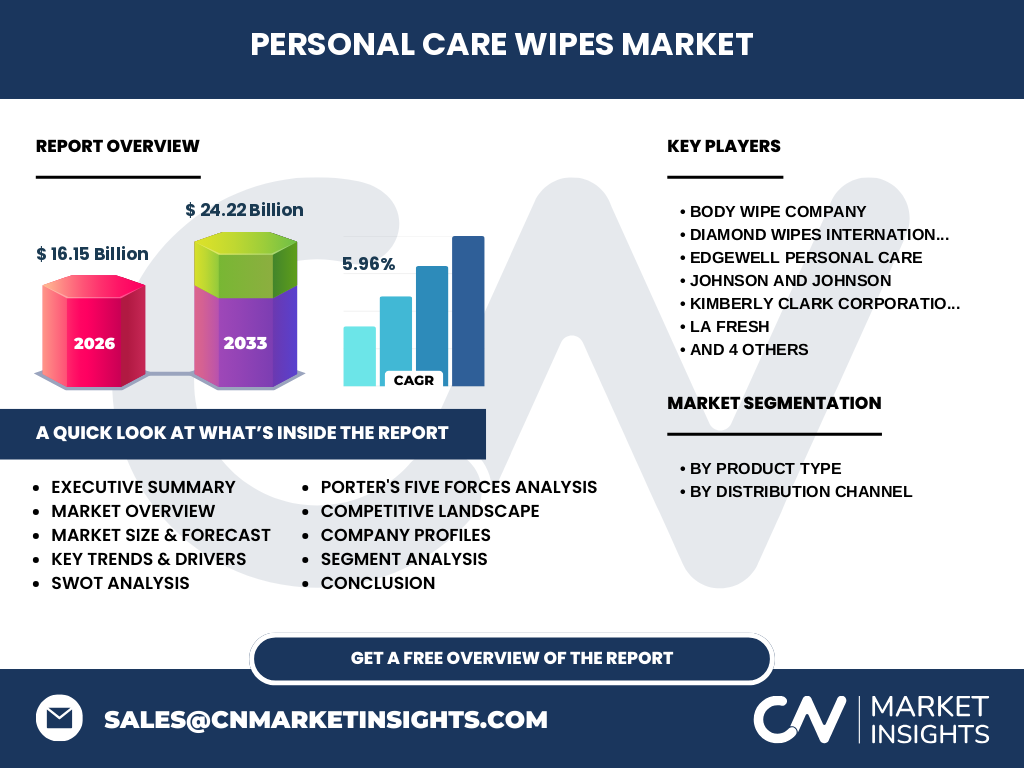

5. Who are the major competitors in the Personal Care Wipes market, and what does the competitive landscape look like?

The market is concentrated among several global players: Body Wipe Company, Diamond Wipes International, Edgewell Personal Care, Johnson & Johnson, Kimberly‑Clark Corporation, La Fresh, Nice‑Pak Products, Inc., Procter & Gamble Co., Rockline Industries, and Unicharm International. These firms compete on product innovation, brand equity, distribution breadth, and sustainability initiatives. Recent years have seen strategic acquisitions and partnership deals, leading to modest consolidation and intensified rivalry in premium and eco‑friendly segments.

6. What are the key findings presented in the Executive Summary of the Personal Care Wipes market report?

The Executive Summary highlights a market valued at $16.15 billion in 2026, projected to reach $24.22 billion by 2033, driven by a 5.96% CAGR. Growth is anchored in expanding product portfolios, higher consumer hygiene consciousness, and robust distribution across both offline and online channels. Competitive dynamics emphasize innovation in biodegradable materials and functional additives. Geographic analysis points to strong performance in North America and Asia‑Pacific, with emerging opportunities in Latin America and the Middle East.

7. What are the forecast expectations for the Personal Care Wipes market from 2025 to 2032?

Based on the provided CAGR of 5.96%, the market is expected to sustain steady expansion through 2032, moving from the 2026 baseline of $16.15 billion toward a 2033 valuation of $24.22 billion. This trajectory suggests consistent year‑over‑year growth, underpinned by product innovation, widening distribution networks, and increasing adoption of sustainable wipes across consumer segments.

8. How is the Personal Care Wipes market sized and shared by product type and distribution channel?

Segmentation by product type includes Baby, Facial & Cosmetic, Hand & Body, and Flushable wipes. While specific monetary shares are not disclosed, each segment contributes to the overall market value, with Baby and Hand & Body categories traditionally holding the largest volumes due to daily usage patterns. Distribution channels comprise Supermarket/Hypermarket, Specialty Store, Online, and Commercial & Industrial segments. Online sales have accelerated, capturing a growing share of transactions, whereas supermarkets remain the dominant offline outlet.

9. What is the global Personal Care Wipes market size and share by region?

The global market totals $16.15 billion in 2026, expanding to $24.22 billion by 2033. Regionally, North America and Asia‑Pacific are the primary contributors, reflecting high consumer purchasing power and large populations respectively. Europe maintains a steady share, while Latin America and the Middle East & Africa exhibit emerging growth potential driven by rising urbanization and disposable income.

10. Can you provide a detailed regional analysis of the Personal Care Wipes market?

In North America, premium and flushable wipes dominate, supported by strong retail networks and consumer willingness to pay for convenience. Asia‑Pacific shows rapid adoption of baby and facial wipes, propelled by increasing birth rates and beauty‑care spending in China, India, and Southeast Asian markets. Europe balances demand across all segments, with a particular focus on eco‑friendly formulations. Latin America experiences incremental growth as middle‑class consumers seek imported brands, while the Middle East‑Africa region benefits from heightened hygiene awareness in institutional settings.

11. What are the profiles of leading companies in the Personal Care Wipes market and their recent strategies?

Key players such as Johnson & Johnson and Procter & Gamble leverage extensive R&D to launch wipes with added skin‑care actives. Kimberly‑Clark focuses on sustainable fiber blends and recycling programs. Edgewell Personal Care expands its portfolio through acquisitions of niche brands. Unicharm International emphasizes Asian market penetration with locally tailored products. Diamond Wipes International and Body Wipe Company target the commercial‑industrial channel, offering bulk‑size solutions for hospitality and healthcare facilities. Recent strategies include multi‑channel roll‑outs, private‑label collaborations, and investment in biodegradable technologies.

12. How does Porter’s Five Forces analysis apply to the Personal Care Wipes market?

Threat of new entrants is moderate; high capital for manufacturing and regulatory compliance creates barriers, yet niche eco‑friendly start‑ups can enter via contract manufacturers. Bargaining power of suppliers is moderate, as raw materials like non‑woven fabrics are sourced from a limited number of suppliers, but volume purchasing mitigates risk. Bargaining power of buyers is high, with retail chains and large e‑commerce platforms demanding price competitiveness and sustainability credentials. Threat of substitutes is low to moderate; alternatives such as reusable cloths exist but lack convenience. Industry rivalry is intense, driven by product innovation, brand loyalty, and promotional activities.

13. What are the SWOT analysis highlights for the Personal Care Wipes market?

Strengths: Established demand for hygiene, broad product applicability, and strong distribution networks.

Weaknesses: Environmental concerns over single‑use plastics and dependence on commodity raw materials.

Opportunities: Development of biodegradable and compostable wipes, premium functional formulations, and expansion in untapped emerging markets.

Threats: Regulatory restrictions on flushable claims, rising raw‑material costs, and competitive pressure from sustainable alternatives.

14. How is the value chain structured in the Personal Care Wipes market?

The value chain begins with raw‑material sourcing (non‑woven fabrics, chemicals, packaging), proceeds to formulation and wet‑process manufacturing, followed by packaging and labeling. Distribution encompasses wholesale to retailers, direct online fulfillment, and bulk sales to commercial users. End‑users include households, healthcare facilities, hospitality, and industrial cleaning services. Value‑added services such as private‑label production and sustainability certifications enhance margins for manufacturers.

15. What key investment insights can be drawn for the Personal Care Wipes market?

Investors should prioritize companies advancing biodegradable substrates, as regulatory trends favor environmentally benign products. Brands with strong e‑commerce capabilities and subscription models exhibit higher growth potential. Partnerships with retail giants for exclusive shelf space can secure stable revenue streams. Finally, tracking M&A activity—especially acquisitions of niche, premium‑wipes firms—offers insight into market consolidation opportunities.

16. What are the main conclusions and takeaways from the Personal Care Wipes market analysis?

The Personal Care Wipes market is poised for robust growth, moving from $16.15 billion in 2026 to $24.22 billion by 2033 at a 5.96% CAGR. Consumer hygiene habits, premiumization, and sustainability are the primary growth engines. Competitive pressure remains high, urging firms to innovate in eco‑friendly materials and functional additives. Regional expansion, particularly in Asia‑Pacific and emerging economies, presents significant upside for proactive players.

17. What research methodology was employed to compile this market report?

The study combined primary interviews with industry executives, surveys of retailers, and secondary data from company filings, trade publications, and reputable market databases. Quantitative analysis applied CAGR calculations based on the provided market size figures, while qualitative assessments derived from trend monitoring, regulatory reviews, and competitor intelligence.

18. What is the scope of this research, and are there any limitations?

The scope encompasses global market sizing, segmentation by product type and distribution channel, regional performance, competitive profiling of the ten listed companies, and strategic analyses (Porter’s Five Forces, SWOT, value chain). Limitations are confined to the use of publicly available information and the provided financial figures; therefore, precise market‑share percentages or undisclosed proprietary data are not included.

19. Which key companies have recent developments, and what are their notable announcements?

Johnson & Johnson launched a line of facial wipes infused with hyaluronic acid targeting anti‑aging consumers. Procter & Gamble introduced a recyclable‑film packaging for its Baby wipes range. Kimberly‑Clark announced a partnership with a biotech firm to develop a plant‑based non‑woven substrate. Edgewell Personal Care completed the acquisition of a boutique flushable‑wipes brand to broaden its premium portfolio. Unicharm International expanded its distribution network in Southeast Asia, adding new e‑commerce platforms. Diamond Wipes International unveiled a commercial‑grade antimicrobial wipe for healthcare facilities, while Body Wipe Company secured a long‑term supply contract with a major hotel chain. La Fresh entered the online subscription market, offering customizable refill kits. Nice‑Pak Products, Inc. began a sustainability pilot using compostable packaging, and Rockline Industries launched a line of industrial‑strength hand wipes for manufacturing plants.