Advanced Driver Assistance System Market Overview - Definition, scope, and significance

An Advanced Driver Assistance System (ADAS) refers to a collection of electronic technologies designed to enhance vehicle safety and improve the driving experience through automated assistance features. These systems utilize sensors, cameras, radar, and sophisticated algorithms to monitor the vehicle's surroundings and provide warnings or take corrective actions to prevent accidents. The scope of ADAS encompasses a wide range of applications including adaptive cruise control, lane departure warning, blind spot detection, automatic emergency braking, parking assistance, and more. The significance of ADAS has grown exponentially as it represents a critical stepping stone toward fully autonomous vehicles, with governments worldwide implementing stricter safety regulations and consumers demanding enhanced safety features. As the automotive industry undergoes a technological transformation, ADAS has become a fundamental component in modern vehicles, bridging the gap between traditional driving and autonomous mobility solutions.

Advanced Driver Assistance System Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The ADAS market is primarily driven by increasing road safety concerns, stringent government regulations mandating safety features, and growing consumer awareness about vehicle safety technologies. The rising number of road accidents globally has created an urgent need for preventive safety measures, while government mandates in regions like Europe and North America require new vehicles to be equipped with specific ADAS features. Additionally, the increasing adoption of electric vehicles and the growing trend of connected cars present significant opportunities for market expansion. However, the market faces several restraints including high implementation costs, concerns about system reliability and cybersecurity vulnerabilities, and the complexity of integrating multiple sensors and technologies. Challenges such as the need for extensive testing and validation, consumer acceptance of autonomous features, and the requirement for standardized communication protocols across different manufacturers also impact market growth. Despite these challenges, opportunities exist in emerging markets, technological advancements in sensor technologies, and the potential for integration with smart city infrastructure.

Advanced Driver Assistance System Market Growth Trends - Current and emerging trends shaping the market

The ADAS market is experiencing several transformative trends that are reshaping the automotive technology landscape. One prominent trend is the shift toward higher levels of automation, with manufacturers increasingly focusing on Level 2 and Level 3 autonomous driving capabilities. The integration of artificial intelligence and machine learning algorithms is enabling more sophisticated decision-making capabilities in ADAS systems, allowing for better object recognition and predictive analysis. Another significant trend is the convergence of ADAS with vehicle-to-everything (V2X) communication technologies, enabling vehicles to communicate with infrastructure and other vehicles for enhanced safety. The miniaturization of sensors and the development of solid-state LiDAR technology are making ADAS more cost-effective and easier to implement across different vehicle segments. Additionally, the growing emphasis on software-defined vehicles is driving the development of over-the-air update capabilities for ADAS features, allowing manufacturers to continuously improve system performance and add new functionalities post-purchase.

COVID-19 Impact on the Advanced Driver Assistance System Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the ADAS market through supply chain interruptions, manufacturing shutdowns, and reduced consumer spending on automotive technologies. The automotive industry experienced a significant slowdown as lockdowns and social distancing measures affected production and sales across major markets. However, the pandemic also accelerated certain trends that benefited the ADAS market, including increased focus on personal vehicle ownership as consumers became more cautious about public transportation, and the growing emphasis on safety features in vehicles. The recovery trajectory has been marked by a strong rebound in automotive sales, particularly in emerging markets, and renewed investments in autonomous driving technologies as mobility companies adapt to post-pandemic transportation needs. The crisis has also highlighted the importance of resilient supply chains and has led to increased localization of component manufacturing, which is expected to benefit the ADAS market in the long term.

Advanced Driver Assistance System Market Competitive Landscape - Major competitors and market consolidation

The ADAS market features a diverse competitive landscape comprising traditional automotive suppliers, technology companies, and emerging startups. Major players like Continental AG, Robert Bosch GmbH, and Harman International leverage their extensive automotive industry experience and established relationships with vehicle manufacturers to maintain strong market positions. Technology giants such as NVIDIA Corporation are disrupting the market with their advanced computing platforms and AI capabilities, while companies like Cypress Semiconductor Corporation and TE Connectivity focus on sensor technologies and electronic components. The market is witnessing significant consolidation through strategic partnerships, mergers, and acquisitions as companies seek to expand their technology portfolios and geographic presence. For instance, traditional automotive suppliers are increasingly collaborating with technology companies to enhance their software capabilities, while tech companies are acquiring automotive expertise through strategic acquisitions. This consolidation trend is expected to continue as the market matures and competition intensifies.

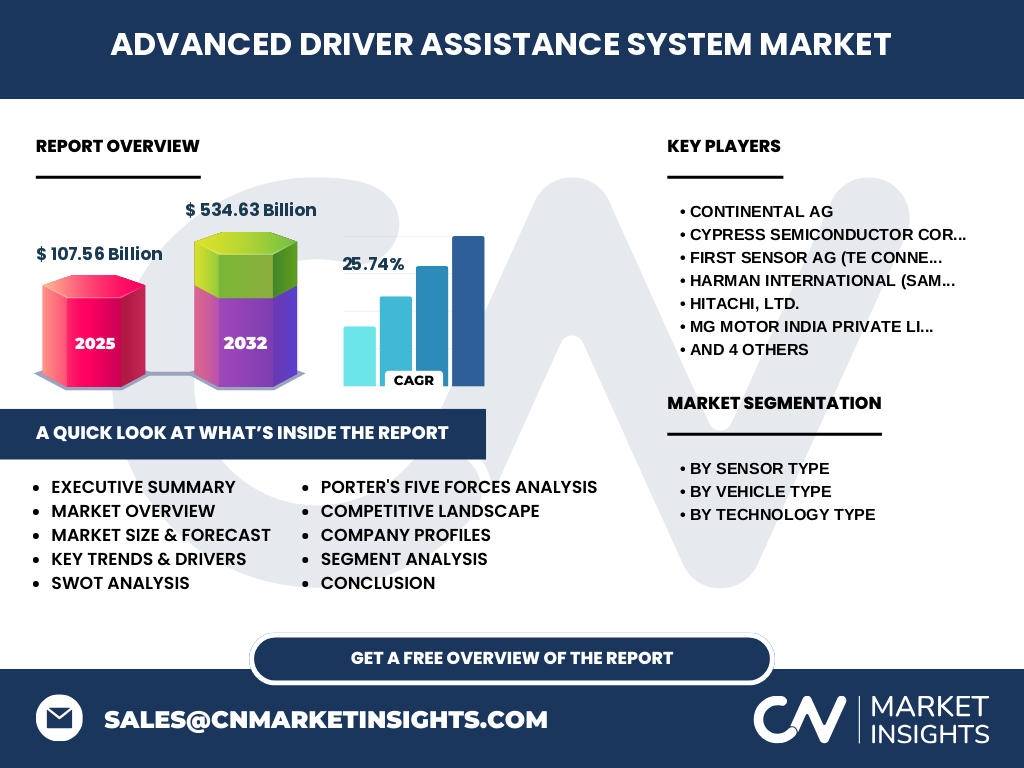

Executive Summary - High-level overview and key findings about Advanced Driver Assistance System Market

The Advanced Driver Assistance System market is experiencing unprecedented growth, driven by technological advancements, regulatory mandates, and increasing consumer demand for vehicle safety features. With a projected CAGR of 25.74% from 2025 to 2032, the market is expected to grow from USD 107.56 billion in 2025 to USD 534.63 billion by 2032. This remarkable growth is fueled by the convergence of multiple factors including the push toward autonomous driving, the integration of artificial intelligence in automotive systems, and the increasing adoption of electric vehicles. The market is characterized by rapid technological innovation, with continuous improvements in sensor technologies, computing capabilities, and software algorithms. While challenges exist in terms of cost, reliability, and consumer acceptance, the overall trajectory points toward widespread adoption of ADAS technologies across all vehicle segments. The competitive landscape remains dynamic, with both established automotive suppliers and new technology entrants competing for market share through innovation and strategic partnerships.

Advanced Driver Assistance System Market Forecast - Projections for 2025-2032 period

The ADAS market is projected to experience substantial growth over the forecast period from 2025 to 2032, with the market size expected to increase from USD 107.56 billion in 2025 to USD 534.63 billion by 2032, representing a compound annual growth rate of 25.74%. This growth trajectory is supported by several factors including the increasing penetration of ADAS features in both premium and mass-market vehicles, the expansion of electric vehicle production, and the ongoing development of autonomous driving technologies. The forecast period will likely see continued technological advancements that reduce the cost of ADAS components while improving their performance and reliability. Regional markets are expected to show varying growth rates, with Asia-Pacific emerging as a particularly strong growth region due to the rapid expansion of automotive production in countries like China and India. The forecast also anticipates increased integration of ADAS with other vehicle systems, leading to more comprehensive safety solutions and new business models around connected vehicle services.

Advanced Driver Assistance System Market Size and Share by Segmentation - Breakdown by {segmentData}

The ADAS market segmentation reveals distinct patterns in technology adoption and market dynamics across different categories. By sensor type, image sensors currently dominate the market due to their widespread use in camera-based systems, followed by ultrasonic sensors for parking assistance applications. LiDAR technology, while currently representing a smaller segment, is expected to experience rapid growth as costs decrease and performance improves. In terms of vehicle type, passenger cars account for the largest market share, driven by higher adoption rates of safety features in this segment, while commercial vehicles represent a growing opportunity as fleet operators recognize the benefits of ADAS for operational efficiency and safety. The technology type segmentation shows adaptive cruise control and automatic emergency braking as leading applications, with parking assistance and lane departure warning systems also showing strong adoption rates. This segmentation analysis indicates that while certain technologies and vehicle types currently dominate, growth opportunities exist across all segments as the technology matures and becomes more cost-effective.

Global Advanced Driver Assistance System Market Size and Share by Region - Geographic distribution

The global ADAS market exhibits significant regional variations in terms of adoption rates, regulatory frameworks, and market maturity. North America leads in terms of technology adoption and market sophistication, driven by stringent safety regulations and high consumer awareness about vehicle safety features. Europe represents another mature market, with the European Union's General Safety Regulation mandating advanced safety features in new vehicles, creating a strong regulatory push for ADAS adoption. The Asia-Pacific region is emerging as the fastest-growing market, with countries like China, Japan, and South Korea investing heavily in autonomous driving technologies and electric vehicle production. China, in particular, is becoming a major player in the ADAS market, with both domestic manufacturers and international companies establishing significant operations in the country. The regional distribution of the market is also influenced by factors such as local manufacturing capabilities, government support for autonomous vehicle development, and the presence of key technology companies and automotive suppliers.

Regional Analysis of the Advanced Driver Assistance System Market - Detailed regional market performance

Regional analysis of the ADAS market reveals distinct characteristics and growth patterns across different geographic areas. In North America, the market is characterized by early adoption of advanced technologies, strong regulatory support for vehicle safety, and the presence of major technology companies and automotive manufacturers. The region benefits from a well-established automotive supply chain and significant investments in autonomous driving research and development. Europe's market is driven by stringent safety regulations, with the EU's General Safety Regulation requiring advanced safety features in new vehicles, creating a strong regulatory push for ADAS adoption. The region also benefits from a highly developed automotive industry and strong government support for connected and autonomous vehicle initiatives. The Asia-Pacific region presents a unique combination of rapid growth and technological innovation, with China emerging as a major market for ADAS due to its large automotive industry, government support for electric vehicles, and ambitious plans for autonomous driving development. Japan and South Korea also contribute significantly to the regional market, with their advanced automotive industries and strong focus on technological innovation.

Leading Company Profiles in the Advanced Driver Assistance System Market - Industry players and strategies

The ADAS market features several prominent companies with distinct strategies and competitive advantages. Continental AG leverages its extensive automotive industry experience and comprehensive product portfolio to maintain a strong market position, focusing on integrated ADAS solutions that combine hardware and software capabilities. Robert Bosch GmbH emphasizes its expertise in sensor technologies and system integration, offering a wide range of ADAS components and complete systems to vehicle manufacturers. NVIDIA Corporation has established itself as a key player through its advanced computing platforms and AI capabilities, providing the computational power necessary for sophisticated ADAS applications. Harman International, as part of the Samsung Group, combines its automotive audio and infotainment expertise with ADAS technologies to create integrated solutions. These companies, along with others like TE Connectivity, Hitachi, and MG Motor India, are pursuing various strategies including technological innovation, strategic partnerships, and geographic expansion to strengthen their market positions and capitalize on the growing demand for ADAS technologies.

Porter's Five Forces Analysis of the Advanced Driver Assistance System Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the ADAS market. The threat of new entrants remains moderate due to the high capital requirements, technical expertise needed, and established relationships between existing players and automotive manufacturers. However, technology companies with substantial resources and expertise in AI and computing are increasingly entering the market, intensifying competition. The bargaining power of buyers, primarily automotive OEMs, is significant as they have multiple suppliers to choose from and can influence pricing and technology development. Supplier bargaining power varies depending on the specific component, with specialized sensor manufacturers holding more power than suppliers of more commoditized components. The threat of substitute products is relatively low as ADAS technologies are becoming standard requirements in modern vehicles, though alternative safety technologies could emerge. Competitive rivalry is intense, with numerous players competing on technology, price, and integration capabilities. The analysis indicates that while the market presents significant opportunities, success requires substantial investment in technology development and strong relationships with automotive manufacturers.

SWOT Analysis of the Advanced Driver Assistance System Market - Strengths, weaknesses, opportunities, threats

The ADAS market demonstrates several key strengths including strong technological capabilities, growing regulatory support, and increasing consumer demand for safety features. The market benefits from continuous technological advancements in sensors, computing, and AI algorithms, enabling more sophisticated and reliable ADAS solutions. However, weaknesses exist in terms of high implementation costs, cybersecurity vulnerabilities, and the complexity of integrating multiple systems. Opportunities abound in emerging markets, the growing electric vehicle segment, and the potential for new business models around connected vehicle services. The market also benefits from increasing government support for autonomous vehicle development and the potential integration with smart city infrastructure. Threats include intense competition, rapid technological changes that could render existing solutions obsolete, and potential regulatory changes that could impact market dynamics. Additionally, concerns about system reliability and consumer acceptance of autonomous features present ongoing challenges that could affect market growth.

Advanced Driver Assistance System Market Value Chain Analysis - Industry structure and value flow

The ADAS value chain encompasses multiple stages from component manufacturing to final vehicle integration and aftermarket services. At the foundation of the value chain are component manufacturers who produce sensors, processors, and other electronic components essential for ADAS functionality. These components are then integrated by system suppliers who develop complete ADAS solutions combining hardware and software elements. Automotive OEMs serve as the primary integrators, incorporating ADAS systems into their vehicle platforms and often working closely with suppliers to customize solutions for specific models. The value chain also includes software developers who create the algorithms and AI models that enable ADAS functionality, as well as testing and validation services that ensure system reliability and compliance with safety standards. Distribution channels include both OEM installations during vehicle manufacturing and aftermarket solutions for existing vehicles. The value chain is characterized by increasing collaboration and integration among different players, with growing emphasis on software capabilities and data analytics as key value drivers.

Key Investment Insights in the Advanced Driver Assistance System Market - Strategic investment recommendations

Investment opportunities in the ADAS market are abundant, driven by the sector's strong growth trajectory and technological innovation. Strategic investments should focus on companies with strong technological capabilities in key areas such as sensor technologies, AI and machine learning algorithms, and system integration. Particular attention should be paid to companies developing solid-state LiDAR technology, as this represents a significant advancement that could reduce costs and improve performance across the ADAS market. Investments in software capabilities are increasingly important as vehicles become more software-defined, with opportunities in areas such as over-the-air update technologies and data analytics platforms. Geographic diversification is recommended, with particular emphasis on the rapidly growing Asia-Pacific market, especially China, which offers significant growth potential. Investors should also consider companies that are developing solutions for electric vehicles and those working on higher levels of autonomous driving capabilities, as these areas represent the future direction of the automotive industry.

Advanced Driver Assistance System Market Conclusion - Summary and key takeaways

The Advanced Driver Assistance System market represents a dynamic and rapidly evolving sector at the intersection of automotive and technology industries. With a projected market size of USD 534.63 billion by 2032 and a CAGR of 25.74%, the market offers substantial growth opportunities driven by technological advancements, regulatory mandates, and changing consumer preferences. The market is characterized by intense competition, continuous innovation, and increasing integration of ADAS with other vehicle systems and emerging technologies. While challenges exist in terms of cost, reliability, and consumer acceptance, the overall trajectory points toward widespread adoption of ADAS technologies across all vehicle segments. Success in this market requires a combination of technological expertise, strong industry relationships, and the ability to adapt to rapidly changing market conditions. As the automotive industry continues its transformation toward autonomous driving, ADAS will remain a critical component, offering significant opportunities for companies that can innovate and deliver reliable, cost-effective solutions.

Research Methodology - How this research was conducted

The research methodology employed for this market analysis combines multiple approaches to ensure comprehensive and accurate insights. Primary research involved interviews with industry experts, automotive manufacturers, and technology providers to gather firsthand information about market trends, challenges, and opportunities. Secondary research included analysis of industry reports, company financial statements, regulatory documents, and academic publications to validate findings and provide historical context. Market size and forecast calculations were based on a combination of bottom-up and top-down approaches, considering factors such as vehicle production volumes, ADAS penetration rates, and component costs. Data triangulation was employed to cross-verify information from multiple sources and ensure accuracy. The research also incorporated competitive analysis, examining company strategies, product portfolios, and market positioning to provide a comprehensive view of the competitive landscape. Special attention was given to emerging trends and technological developments that could impact future market dynamics.

Research Scope - Coverage and limitations

The research scope for this ADAS market analysis encompasses the period from 2025 to 2032, with a particular focus on market size, growth trends, competitive landscape, and regional dynamics. The analysis covers key market segments including sensor types, vehicle types, and technology types, providing a comprehensive view of the market structure. Geographic coverage includes major automotive markets across North America, Europe, Asia-Pacific, and other regions, with detailed analysis of regional market characteristics and growth drivers. The research examines both established players and emerging companies in the ADAS space, considering their strategies, product offerings, and market positioning. Limitations of the research include the rapidly evolving nature of the technology, which can make long-term forecasting challenging, and the potential impact of unforeseen regulatory changes or technological breakthroughs that could significantly alter market dynamics. Additionally, the analysis focuses primarily on hardware and software components of ADAS systems, with less emphasis on infrastructure requirements and regulatory frameworks that also play crucial roles in market development.

Key Companies and Recent Developments in the Advanced Driver Assistance System Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The ADAS market features several key companies that are driving innovation and shaping market dynamics through strategic initiatives and technological advancements. Continental AG has recently announced expanded partnerships with electric vehicle manufacturers to integrate its latest ADAS technologies, while also launching new sensor solutions with improved performance and reduced costs. Robert Bosch GmbH continues to strengthen its market position through significant investments in AI and machine learning capabilities, with recent product launches focusing on enhanced object recognition and predictive safety features. NVIDIA Corporation has made headlines with its latest DRIVE platform updates, offering increased computational power for more sophisticated ADAS applications and autonomous driving capabilities. Harman International, leveraging its Samsung Group backing, has announced new integrated cockpit solutions that combine ADAS with advanced infotainment systems. TE Connectivity has expanded its sensor portfolio with new solid-state LiDAR solutions, while MG Motor India has introduced advanced ADAS features in its latest vehicle models, targeting the growing Asian market. These companies, along with others in the sector, continue to pursue strategic partnerships, product innovations, and geographic expansions to capitalize on the growing demand for ADAS technologies and maintain their competitive positions in this rapidly evolving market.