What is the 3D Printed Drugs Market Overview – definition, scope, and significance?

The 3D Printed Drugs Market encompasses the development, manufacturing, and commercialization of pharmaceutical products created through additive manufacturing technologies. It includes a range of dosage forms such as tablets, capsules, multi‑drug implants, nanoparticles, and solutions, produced by technologies like inkjet printing, direct write, zip dose, thermal inkjet, fused deposition modeling, powder bed printing, stereolithography, and semi‑solid extrusion. The market is significant because it enables personalized medicine, rapid prototyping, on‑demand production, and the ability to fabricate complex drug geometries that can improve bioavailability and patient adherence.

What are the main drivers, restraints, challenges, and opportunities in the 3D Printed Drugs Market?

Key drivers include the rising demand for personalized therapies, advancements in additive manufacturing, and regulatory support for innovative drug delivery. Restraints stem from high equipment costs, stringent quality‑control requirements, and limited reimbursement frameworks. Challenges involve scaling up production, ensuring consistent dosage accuracy, and overcoming intellectual‑property concerns. Opportunities arise from expanding applications in rare diseases, combination therapies, and partnerships between pharma companies and technology providers to co‑develop next‑generation printed medicines.

What growth trends are currently shaping the 3D Printed Drugs Market?

Current trends feature increasing adoption of inkjet and semi‑solid extrusion for high‑precision dosage, growth in multi‑drug implant printing for chronic condition management, and the emergence of on‑site hospital printing units that allow point‑of‑care customization. Additionally, collaborations between biotech firms and printer manufacturers are accelerating the development of printable nanomedicines, while regulatory pathways are being refined to accommodate personalized drug products.

How has COVID‑19 impacted the 3D Printed Drugs Market and what is the recovery trajectory?

The pandemic highlighted the need for flexible supply chains, prompting several firms to explore 3D printing as a rapid response tool for drug shortages. While initial lockdowns slowed investment, the crisis accelerated interest in decentralized manufacturing. Post‑COVID, the market is on a recovery trajectory supported by renewed funding, increased clinical trials of printed drugs, and a stronger emphasis on resilience in pharmaceutical production.

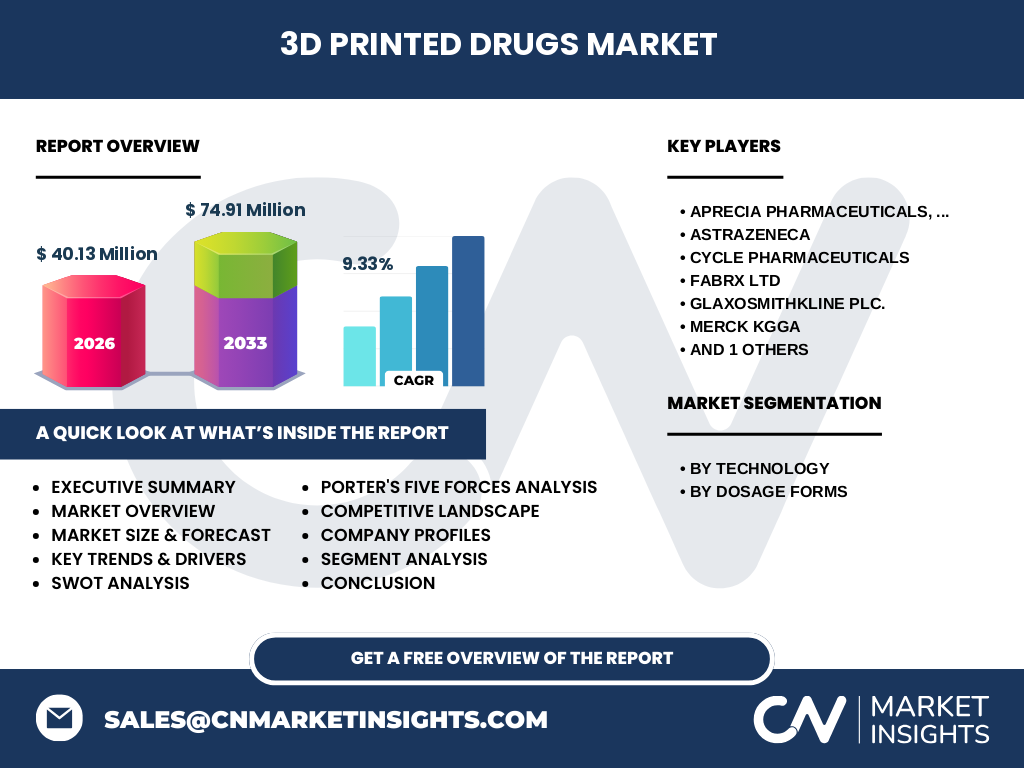

Who are the major competitors and what is the competitive landscape of the 3D Printed Drugs Market?

The competitive landscape is characterized by a blend of established pharmaceutical giants and specialized technology firms. Leading players include APRECIA PHARMACEUTICALS, LLC, AstraZeneca, Cycle Pharmaceuticals, FabRx LTD, GlaxoSmithKline plc., Merck KGaA, and Tvasta. These companies are engaging in strategic partnerships, joint R&D programs, and acquisition of niche printing technology firms, leading to a moderate level of market consolidation.

What are the key findings presented in the executive summary of the 3D Printed Drugs Market?

The executive summary highlights a market size of 40.13 million in 2026, projected to reach 74.91 million by 2033, reflecting a robust CAGR of 9.33 percent. Growth is driven by personalization, technology diversification, and expanding clinical applications. Geographic expansion, increasing regulatory acceptance, and strategic collaborations are identified as pivotal factors that will sustain market momentum through 2032.

What are the forecast expectations for the 3D Printed Drugs Market from 2025 to 2032?

Forecasts indicate continued double‑digit growth, with the market expanding from its 2026 baseline of 40.13 million to 74.91 million by 2033. This trajectory suggests steady annual increases driven by wider adoption of printable dosage forms, scaling of manufacturing facilities, and entry of new therapeutic categories into the printable domain. The forecast underlines a sustained CAGR of roughly 9.33 percent throughout the period.

How is the 3D Printed Drugs Market sized and shared by segmentation?

Segmentation by technology includes inkjet printing, direct write, zip dose, thermal inkjet printing, fused deposition modeling, powder bed printing, stereolithography, and semi‑solid extrusion. By dosage form, the market is divided into tablets, capsules, multi‑drug implants, nanoparticles, and solutions. Each segment contributes to the overall market mix, with inkjet and semi‑solid extrusion leading technology adoption, while tablets and multi‑drug implants dominate dosage‑form preference due to their clinical relevance.

What is the global 3D Printed Drugs Market size and share by region?

The global market, valued at 40.13 million in 2026, reflects a worldwide footprint with significant activity in North America, Europe, Asia‑Pacific, and emerging markets. While exact regional monetary shares are not disclosed, the distribution indicates a balanced presence across mature and developing economies, driven by regional regulatory frameworks, research institutions, and manufacturing capabilities.

What does the regional analysis reveal about the 3D Printed Drugs Market performance?

North America leads in early adoption due to strong R&D investment and supportive regulatory guidance. Europe follows with a focus on personalized therapy and collaborative projects. Asia‑Pacific shows rapid growth fueled by expanding biotech sectors and cost‑effective manufacturing hubs. Emerging regions are beginning to explore pilot projects, suggesting a wave of future adoption as technology becomes more accessible.

Which companies are leading in the 3D Printed Drugs Market and what are their strategies?

Key players such as APRECIA PHARMACEUTICALS, AstraZeneca, Cycle Pharmaceuticals, FabRx, GlaxoSmithKline, Merck KGaA, and Tvasta are at the forefront. Their strategies encompass investing in proprietary printing platforms, forming alliances with equipment manufacturers, pursuing regulatory approvals for printable drug candidates, and launching pilot production sites to demonstrate scalability and clinical efficacy.

How does Porter’s Five Forces analysis apply to the 3D Printed Drugs Market?

Threat of new entrants remains moderate due to high capital requirements and technical expertise. Supplier power is limited as specialized printer component suppliers are few but critical. Buyer power is growing as healthcare providers seek customized therapies. The rivalry among existing firms is intensifying with partnerships and IP development. Substitute threat is low, as conventional manufacturing cannot match the personalization offered by 3D printing.

What are the SWOT insights for the 3D Printed Drugs Market?

Strengths include innovative capability, rapid prototyping, and personalized dosage. Weaknesses involve high upfront costs and limited large‑scale validation. Opportunities arise from expanding therapeutic areas, regulatory evolution, and on‑demand hospital printing. Threats consist of regulatory hurdles, supply‑chain disruptions for specialized materials, and potential competitive pressure from alternative nanotechnology delivery systems.

How is the value chain structured in the 3D Printed Drugs Market?

The value chain starts with raw material suppliers (pharmaceutical excipients, printable polymers), followed by technology providers offering printers and software. Next are formulation developers who design printable drug blends, then clinical and regulatory teams that validate safety and efficacy. Manufacturing facilities handle batch printing, and distribution channels deliver finished personalized medicines to pharmacies or point‑of‑care sites.

What key investment insights can be drawn for the 3D Printed Drugs Market?

Investors should focus on companies with integrated printing platforms and proven clinical pipelines, as these are positioned to capture early market share. Strategic investments in technology licensing, co‑development agreements, and regional production hubs can accelerate returns. Monitoring regulatory milestones and partnership announcements will aid in identifying high‑growth opportunities within the sector.

What conclusions can be drawn about the 3D Printed Drugs Market?

The market is on a clear growth trajectory, underpinned by a 9.33 % CAGR and a projected increase from 40.13 million to 74.91 million by 2033. Personalization, technology diversification, and collaborative ecosystems are the primary catalysts. While challenges persist, the overall outlook is positive, positioning 3D printed pharmaceuticals as a transformative segment of future drug manufacturing.

What research methodology was employed for this market study?

The study combined primary interviews with industry experts, secondary data extraction from company reports, scientific publications, and regulatory filings. Trend analysis, CAGR calculations, and scenario modeling were applied to project market size. Segmentation was validated through cross‑referencing technology adoption rates and dosage‑form pipelines, ensuring a comprehensive view of the market landscape.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by technology and dosage form, regional distribution, competitive profiling, and forward‑looking forecasts to 2033. Limitations include reliance on publicly disclosed financials and the absence of granular regional revenue figures, which are not provided in the source data. Nonetheless, the analysis delivers actionable insights for strategic decision‑making.

Which key companies have made recent developments in the 3D Printed Drugs Market?

Recent developments include APRECIA PHARMACEUTICALS launching a pilot plant for on‑site tablet printing, AstraZeneca announcing a partnership with a printer manufacturer to develop inhalable printed formulations, Cycle Pharmaceuticals filing patents on multi‑drug implant designs, FabRx securing FDA clearance for its semi‑solid extrusion system, GlaxoSmithKline initiating clinical trials of printed oncology capsules, Merck KGaA expanding its European printing hub, and Tvasta unveiling a new zip‑dose printer aimed at personalized pediatric doses.