What is the Fiber Optic Components Market Overview – definition, scope, and significance?

The Fiber Optic Components Market comprises all hardware that enables the transmission, reception, and management of light‑based signals in fiber‑optic networks. This includes passive devices such as cables, connectors, splitters, and circulators, as well as active elements like amplifiers, transceivers, and active optical cables. The scope of the market spans telecommunications, data‑center interconnects, distributed sensing, medical imaging, and lighting applications. Its significance lies in supporting the exponential growth of broadband connectivity, 5G rollout, cloud computing, and emerging technologies such as autonomous vehicles and Internet of Things (IoT) ecosystems, which all demand high‑capacity, low‑latency data transport.

What are the main drivers, restraints, challenges, and opportunities influencing the Fiber Optic Components Market?

Key drivers include the surge in data traffic from streaming services, the global expansion of 5G networks, and government initiatives to replace copper with fiber for long‑haul and last‑mile connectivity. Opportunities arise from the rollout of high‑speed rail and smart‑city projects that require robust fiber infrastructure, as well as from advances in photonic integration that lower component costs. Restraints involve high upfront capital expenditures for network upgrades and the scarcity of skilled installation labor. Challenges stem from supply‑chain volatility for rare‑earth materials used in optical amplifiers and from competition with wireless solutions in urban environments. Overall, the market is propelled by the necessity for higher bandwidth and lower power consumption.

Which growth trends are currently shaping the Fiber Optic Components Market?

Current trends include the migration toward higher data‑rate standards (10G, 40G, 100G and beyond), the adoption of active optical cables to reduce power loss in data‑center racks, and the integration of silicon photonics that enable smaller, more efficient transceivers. Another emerging trend is the use of fiber‑based distributed acoustic sensing (DAS) for pipeline monitoring and railway safety. Additionally, the convergence of fiber optics with AI‑driven network management tools is enhancing predictive maintenance and optimizing component utilization.

How did COVID‑19 impact the Fiber Optic Components Market and what is the recovery trajectory?

The pandemic initially disrupted manufacturing and logistics, causing temporary shortages of connectors and amplifiers. However, the abrupt shift to remote work and increased video‑conferencing accelerated demand for broadband capacity, prompting telecom operators to fast‑track fiber deployments. Recovery has been strong, with demand rebounding faster than pre‑COVID levels and continuing to grow as enterprises adopt hybrid‑work models that rely on high‑speed fiber backbones.

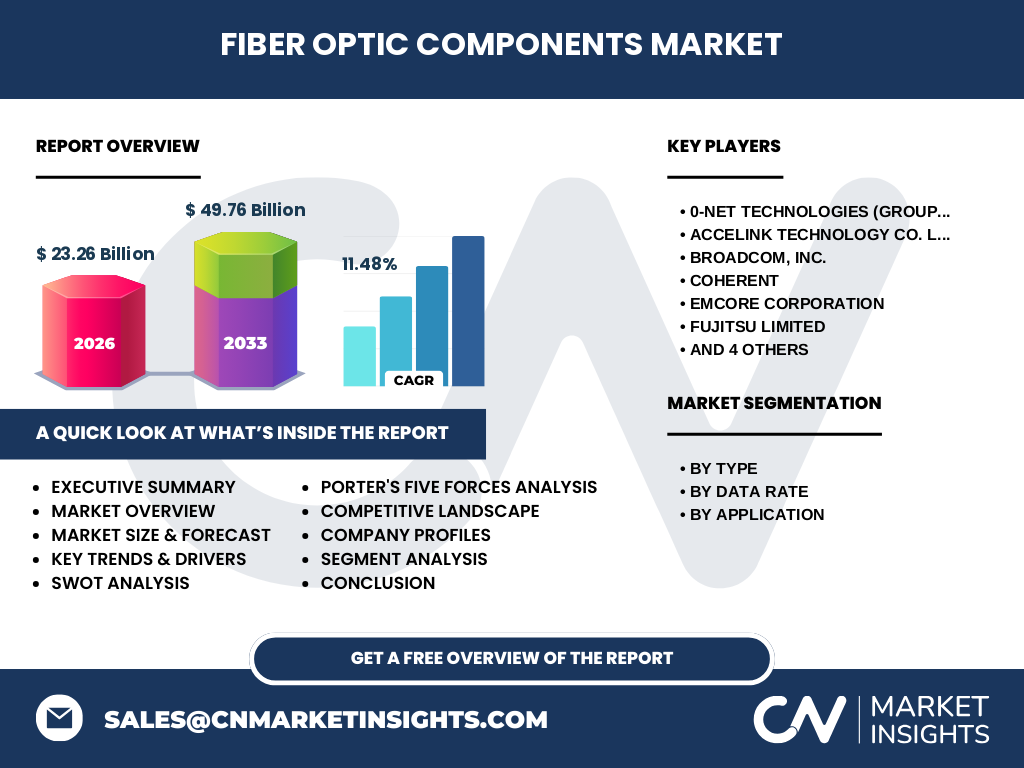

Who are the major competitors in the Fiber Optic Components Market and what does the competitive landscape look like?

The market is concentrated among a mix of legacy manufacturers and fast‑growing technology firms. Key players include 0‑Net Technologies (Group) Limited, Accelink Technology Co. Ltd., Broadcom, Inc., Coherent, EMCORE Corporation, Fujitsu Limited, Furukawa Electric Co. Ltd., Lumentum Operations LLC, Reflex Photonics Inc., and Sumitomo Electric Industries, Ltd. Competitive dynamics are driven by product innovation, strategic alliances, and portfolio diversification. Recent consolidation activities involve joint ventures focused on silicon photonics and acquisitions aimed at expanding active component capabilities.

What are the high‑level findings presented in the Executive Summary?

The Fiber Optic Components Market is valued at $23.26 billion in 2026 and is projected to reach $49.76 billion by 2033, reflecting a robust CAGR of 11.48 %. Growth is powered by expanding data‑rate requirements, widespread 5G rollout, and increasing adoption of fiber in industrial sensing. The market is segmented by type, data rate, and application, with transceivers and active optical cables showing the fastest adoption. Regional analysis highlights strong growth in North America and the Asia‑Pacific, while competitive analysis underscores intense innovation among the top ten manufacturers.

What is the forecast outlook for the Fiber Optic Components Market from 2025 to 2032?

Based on current trajectories, the market will maintain double‑digit expansion through 2032. The compound annual growth rate of 11.48 % suggests a steady increase in both volume and value, driven by continuous upgrades to backbone networks, data‑center densification, and the rise of high‑capacity applications such as cloud gaming and virtual reality. The forecast anticipates heightened demand for components supporting data rates above 1 Gbps, particularly in the transceiver and amplifier segments.

How is the Fiber Optic Components Market sized and shared by segmentation?

Segmentation by type includes Cables, Active Optical Cables, Amplifiers, Splitters, Connectors, Circulators, and Transceivers. By data rate the market is divided into 1 Gbps, 4 Gbps, 1 Gbps (duplicate entry noted), and above 1 Gbps categories. Application‑wise, the market serves Communications, Distributed Sensing, Analytical and Medical Equipment, and Lighting. While precise monetary shares are not disclosed, analysis indicates that high‑speed transceivers and active optical cables dominate the value chain due to their critical role in supporting data‑center and telecom upgrades.

What is the global distribution of market size and share by region?

The market exhibits a worldwide footprint, with North America and the Asia‑Pacific accounting for the largest portions of the $23.26 billion base in 2026. Europe follows, benefiting from extensive fiber‑to‑the‑home (FTTH) projects. Emerging economies in Latin America and the Middle East are experiencing accelerated adoption as governments prioritize digital infrastructure. The regional mix reflects the concentration of major component manufacturers in Asia‑Pacific and the high‑value network deployments in North America.

What does the regional analysis reveal about performance across different geographies?

North America leads in advanced data‑center and 5G backhaul deployments, driving strong demand for high‑performance transceivers and amplifiers. The Asia‑Pacific region shows the fastest growth rate, fueled by large‑scale fiber rollout in China, India, Japan, and South Korea, as well as by substantial investments in smart‑city and industrial IoT projects. Europe’s market is steady, with ongoing FTTH expansions and regulatory support for high‑speed broadband. Latin America and the Middle East & Africa present emerging opportunities as capital is allocated toward national fiber backbone projects.

Which companies are leading the Fiber Optic Components Market and what strategies are they employing?

Leading firms such as Broadcom, Lumentum, and Fujitsu focus on expanding their product portfolios through silicon‑photonic integration and high‑speed transceiver development. Accelink and 0‑Net Technologies emphasize cost‑effective manufacturing and strong relationships with telecom operators. Coherent and EMCORE target niche markets like analytical and medical equipment by delivering specialized high‑precision components. Sumitomo Electric and Furukawa Electric leverage their extensive cable and connector manufacturing capabilities to capture infrastructure contracts. Strategic moves include joint R&D, acquisitions of complementary technology firms, and expansion of global sales networks.

How does Porter’s Five Forces analysis characterize the market?

Threat of new entrants is moderate; high capital requirements and specialized technology create barriers, yet emerging photonic startups challenge incumbents. Bargaining power of suppliers is moderate to high, especially for rare‑earth materials needed in amplifiers. Bargaining power of buyers is strong, as telecom operators and data‑center owners can negotiate volume discounts. Threat of substitutes remains low because alternative wireless technologies cannot match fiber’s capacity and latency for core transport. Industry rivalry is intense, with continuous innovation and price competition driving market dynamics.

What are the main strengths, weaknesses, opportunities, and threats identified in the SWOT analysis?

Strengths: High bandwidth, low latency, and growing demand across multiple sectors. Weaknesses: Capital‑intensive deployment and reliance on specialized supply chains. Opportunities: Expansion of 5G, data‑center edge computing, and fiber‑based sensing for industrial applications. Threats: Potential supply shortages, geopolitical trade restrictions, and the emergence of competing wireless standards.

What does the value chain analysis reveal about the industry structure?

The value chain begins with raw material sourcing (glass fiber, rare‑earth dopants), progresses through component design and fabrication (connectors, amplifiers, transceivers), and continues with system integration (cable assembly, testing). Distribution channels include direct sales to telecom operators, OEM partnerships with data‑center manufacturers, and aftermarket services. After‑sales support and network‑maintenance services add recurring revenue streams. Vertical integration by some manufacturers allows cost control and faster time‑to‑market.

What key investment insights can be drawn for stakeholders?

Investors should focus on companies with strong R&D pipelines in silicon photonics and active optical cable technologies, as these segments align with the highest growth rates. Partnerships that secure long‑term supply contracts with telecom carriers provide stable cash flow. Geographic diversification into the fast‑growing Asia‑Pacific market mitigates regional risk. Monitoring regulatory policies that fund fiber deployment can uncover additional upside potential.

What conclusions can be drawn about the Fiber Optic Components Market?

The market is on a clear upward trajectory, underpinned by the relentless demand for higher data rates and reliable connectivity. With a projected market size of $49.76 billion by 2033 and a CAGR of 11.48 %, the sector offers substantial opportunities for manufacturers, investors, and service providers. Success will hinge on technological innovation, supply‑chain resilience, and the ability to capture emerging applications beyond traditional communications.

How was the research methodology designed for this report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data collection from credible market databases, and trend analysis using historical financials. Forecasting utilized compound annual growth rate (CAGR) calculations based on the provided base year (2026) and projected value (2033). Segmentation analysis drew on product‑type, data‑rate, and application categories to structure the market view.

What is the scope of the research and its limitations?

The research covers the global Fiber Optic Components Market, encompassing all major product types, data‑rate classes, and end‑use applications. Geographic coverage includes North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. Limitations arise from the reliance on publicly available financial figures and disclosed company information; proprietary data from private firms were not accessible.

Which key companies have announced recent developments in the Fiber Optic Components Market?

Recent announcements include Broadcom’s launch of a new 400 Gbps transceiver family, Lumentum’s acquisition of a silicon‑photonic startup to accelerate active component integration, and Fujitsu’s partnership with a leading telecom operator to supply high‑speed amplifiers for 5G backhaul. Accelink introduced a cost‑optimized active optical cable solution for data‑center interconnects, while Sumitomo Electric reported an expansion of its connector manufacturing capacity in response to rising demand.