1. What is the Mission Critical Communication Market and why is it significant?

The Mission Critical Communication (MCC) market encompasses solutions that enable reliable, secure, and real‑time voice, data, and video exchange for organizations where communication failure can endanger lives, public safety, or essential services. Its scope includes hardware (radios, base stations), software (dispatch, management platforms) and services (installation, maintenance). The significance lies in its role as the backbone for public safety agencies, transportation networks, energy grids, and mining operations, ensuring coordinated response, operational continuity, and regulatory compliance.

2. What are the main drivers, restraints, challenges, and opportunities shaping the MCC market?

Key drivers include the increasing adoption of broadband‑enabled LTE for mission‑critical push‑to‑talk, heightened government spending on public safety communications, and the digital transformation of transportation and utilities. Restraints stem from high upfront capital costs and stringent regulatory standards that lengthen deployment cycles. Challenges involve legacy system migration, cybersecurity threats, and spectrum scarcity in densely populated regions. Opportunities arise from the rollout of 5G‑based mission‑critical services, integration of AI‑powered analytics for incident management, and growing demand for managed services in remote mining sites.

3. Which growth trends are currently influencing the MCC market?

Current trends feature a shift from narrowband Land Mobile Radio (LMR) to broadband Long Term Evolution (LTE) platforms, enabling richer data services and video streaming. Vendors are bundling hardware with cloud‑native software and managed services, creating subscription‑based business models. Interoperability standards such as P25 Phase II and NG9‑1‑1 are gaining traction, fostering cross‑agency communication. Additionally, the rise of Internet of Things (IoT) devices is expanding the sensor ecosystem that feeds into mission‑critical command centers.

4. How did COVID‑19 affect the MCC market and what is the recovery outlook?

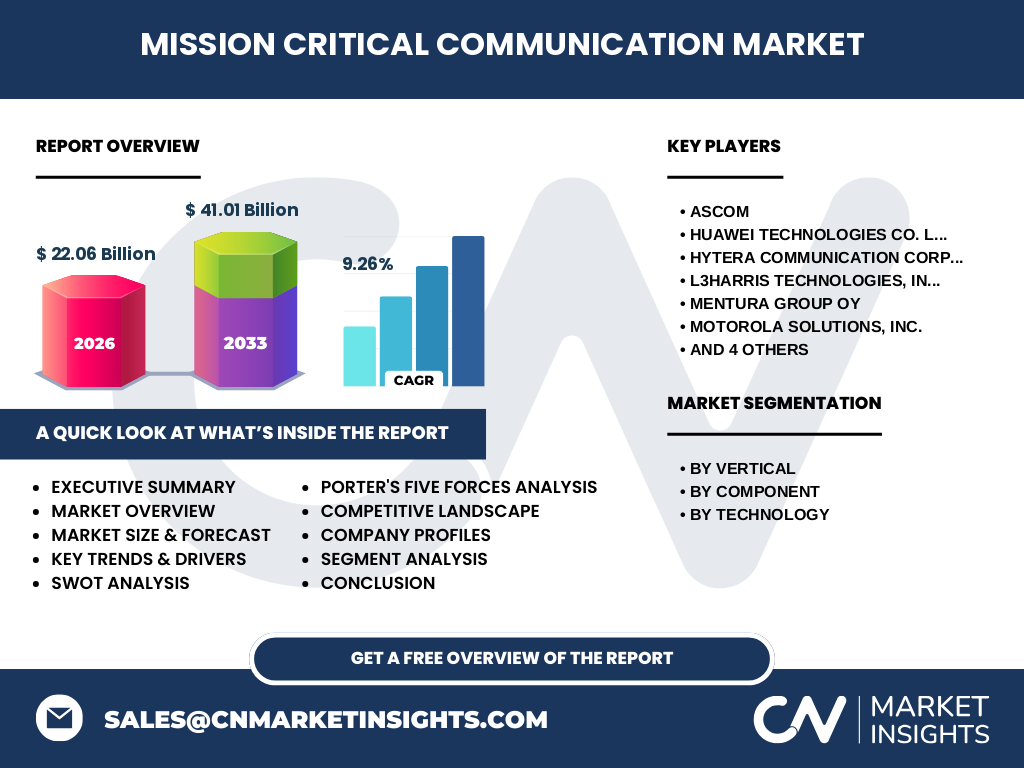

The pandemic accelerated the adoption of resilient communication infrastructures as governments prioritized emergency response capabilities. Procurement cycles slowed in early 2020 due to budget reallocations, but later fiscal stimulus funded upgrades to public safety networks. Remote work also highlighted the need for secure, reliable communication tools. Recovery is robust, with a projected CAGR of 9.26% through 2032, driven by renewed investment in digital public‑safety platforms and post‑pandemic infrastructure resilience programs.

5. Who are the major competitors and how is the MCC market consolidating?

Leading competitors include Ascom, Huawei Technologies, Hytera, L3Harris Technologies, Mentura Group, Motorola Solutions, Nokia, Tassta, Ericsson, and Zenitel. The market is witnessing consolidation through strategic acquisitions—e.g., larger players acquiring niche software firms to expand their service portfolios—and joint ventures that combine hardware expertise with cloud‑service capabilities. This consolidation enhances economies of scale, accelerates technology integration, and strengthens global distribution networks.

6. What are the key findings of the executive summary?

The MCC market is valued at $22.06 billion in 2026 and is forecast to reach $41.01 billion by 2033, reflecting a strong 9.26% CAGR. Growth is propelled by broadband LTE migration, heightened public‑safety spending, and the emergence of AI‑enabled dispatch solutions. While capital intensity and regulatory complexity pose hurdles, opportunities in 5G‑enabled services, managed offerings, and regional expansion—especially in Asia‑Pacific—underscore a promising outlook for investors and vendors alike.

7. What is the market forecast for 2025‑2032?

Based on the given CAGR of 9.26%, the market is expected to maintain double‑digit growth throughout 2025‑2032, expanding from the 2026 baseline of $22.06 billion to surpass $40 billion by the early 2030s. This trajectory suggests continued spending on hardware upgrades, software platforms, and managed services, with higher penetration in transportation and energy‑utility verticals as digital control centers become commonplace.

8. How is the market sized and shared across segments?

Segmentation by vertical shows four primary end‑users: Public Safety and Government Agencies, Transportation, Energy and Utilities, and Mining. By component, the market divides into Hardware, Software, and Services, while technology segmentation distinguishes Land Mobile Radio from Long Term Evolution solutions. Each segment contributes to the overall $22.06 billion base, with broadband LTE and Services expected to capture the fastest growth share as organizations move toward integrated, cloud‑based architectures.

9. What is the geographic distribution of the MCC market?

The market’s global footprint spans North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. While specific regional revenue figures are not disclosed, North America and Europe currently dominate due to mature public‑safety infrastructures. Asia‑Pacific is emerging rapidly, driven by government initiatives in smart cities and extensive railway networks, positioning it as the next major growth engine.

10. How does each region perform within the MCC market?

In North America, strong federal funding and large‑scale LTE public‑safety networks drive demand. Europe benefits from EU‑wide interoperability standards and aggressive 5G rollouts. Asia‑Pacific’s growth is fueled by rapid urbanization, railway modernization, and expanding energy grids. Latin America shows incremental adoption as governments modernize legacy LMR systems, while the Middle East & Africa focus on mission‑critical communications for oil‑and‑gas operations and public‑safety initiatives.

11. Which companies lead the MCC market and what are their strategies?

Key players—Motorola Solutions, L3Harris, Huawei, Nokia, Ericsson, Hytera, Ascom, Zenitel, Mentura, and Tassta—pursue strategies such as expanding broadband LTE product lines, investing in 5G mission‑critical solutions, forging public‑private partnerships, and offering end‑to‑end managed services. Many are enhancing software ecosystems with AI‑driven analytics and integrating cybersecurity features to address rising threats, thereby strengthening their market positioning.

12. What does Porter’s Five Forces reveal about the MCC market?

Threat of new entrants is moderate due to high capital requirements and regulatory barriers. Bargaining power of buyers is growing as large government contracts demand competitive pricing and interoperability. Bargaining power of suppliers is limited; most components are sourced from a few tier‑1 manufacturers. Threat of substitutes remains low because mission‑critical reliability cannot be matched by commodity communication tools. Industry rivalry is intense, driven by technological innovation and consolidation.

13. What are the SWOT highlights for the MCC market?

Strengths: Critical importance to public safety, high entry barriers, and strong long‑term contracts.

Weaknesses: High upfront costs and complex integration with legacy systems.

Opportunities: 5G mission‑critical services, AI analytics, and expansion in emerging markets.

Threats: Cybersecurity vulnerabilities, spectrum constraints, and potential regulatory delays.

14. How does the value chain of the MCC market operate?

The value chain begins with raw component suppliers (RF modules, chips), progresses to hardware manufacturers (radios, base stations), integrates with software developers (dispatch, analytics), followed by system integrators who design end‑to‑end solutions. Services providers then deliver installation, maintenance, and managed‑service contracts, while end users—public‑safety agencies, transport operators, utilities, and miners—consume the final solution. Each stage adds value through customization, compliance testing, and ongoing support.

15. What investment insights are most relevant for stakeholders?

Investors should prioritize companies that combine broadband LTE/5G hardware with subscription‑based software and services, as recurring revenue mitigates capital‑intensive cycles. Target markets with expanding public‑safety budgets, such as Asia‑Pacific, and focus on firms that possess strong cybersecurity portfolios. strategic M&A activity around AI‑enabled dispatch platforms offers upside potential, while monitoring regulatory developments ensures alignment with spectrum allocation policies.

16. What are the concluding takeaways for the MCC market?

The MCC market is on a clear growth trajectory, almost doubling in size by 2033. Broadband LTE and emerging 5G technologies are reshaping product offerings, while managed services and AI analytics create new revenue streams. Despite capital and regulatory challenges, the sector’s essential nature, combined with robust public‑sector spending, ensures sustained demand. Companies that innovate across hardware, software, and services will capture the most value.

17. How was the research conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary analysis of company filings, government procurement databases, and reputable market intelligence sources. Trend extrapolation used the supplied CAGR of 9.26% to project future market size, while segmentation was derived from the provided vertical, component, and technology classifications.

18. What is the scope of this research?

The scope covers global Mission Critical Communication solutions across public safety, transportation, energy & utilities, and mining verticals, evaluated by hardware, software, and services, and differentiated by Land Mobile Radio and LTE technologies. Geographic coverage includes all major regions, but detailed regional revenue figures are limited to the qualitative assessment of market dynamics. The study does not extend to unrelated communication markets such as consumer mobile phones.

19. Which key companies have recently announced developments in the MCC market?

Motorola Solutions launched an LTE‑based public‑safety network platform with integrated AI analytics. Huawei announced a 5G mission‑critical push‑to‑talk solution targeting Asian municipal agencies. Nokia unveiled a cloud‑native command‑and‑control suite for transportation operators. Ericsson introduced a secure, end‑to‑end NG9‑1‑1 service. L3Harris disclosed a partnership with a major North‑American utility to deploy hardened LTE radios in remote substations. These initiatives illustrate the industry’s shift toward broadband, cloud, and AI‑driven capabilities.