What is the Advanced Distribution Management System Market and why is it significant?

The Advanced Distribution Management System (ADMS) market represents a critical segment of the energy technology sector focused on intelligent grid management solutions. ADMS platforms integrate distribution management systems (DMS), outage management systems (OMS), and supervisory control and data acquisition (SCADA) systems into unified solutions that enable utilities to optimize their distribution networks. These systems provide real-time monitoring, control, and optimization of electrical distribution networks, helping utilities improve reliability, efficiency, and grid resilience. The significance of ADMS lies in its ability to address the growing complexity of modern power grids, which must accommodate increasing renewable energy integration, electric vehicle charging infrastructure, and fluctuating demand patterns while maintaining grid stability and minimizing outages.

What are the key drivers, restraints, challenges, and opportunities in the ADMS market?

The ADMS market is primarily driven by the global push toward smart grid modernization, increasing renewable energy penetration, and the need for enhanced grid reliability. Utilities are investing heavily in ADMS solutions to manage the complexities of bidirectional power flow, distributed energy resources, and real-time grid balancing. However, the market faces restraints including high implementation costs, legacy infrastructure compatibility issues, and cybersecurity concerns. Major challenges include the complexity of integrating ADMS with existing systems, the shortage of skilled personnel, and regulatory hurdles across different regions. Despite these challenges, significant opportunities exist in emerging markets where rapid urbanization is driving infrastructure investments, the growing adoption of cloud-based ADMS solutions, and the potential for AI and machine learning integration to enhance predictive maintenance and grid optimization capabilities.

What are the current and emerging growth trends in the ADMS market?

Current growth trends in the ADMS market include the increasing adoption of cloud-based solutions, which offer scalability and cost-effectiveness compared to traditional on-premise systems. There's a strong trend toward the integration of artificial intelligence and machine learning capabilities to enhance predictive analytics and automated decision-making. Edge computing is emerging as a critical trend, enabling faster data processing and real-time responses at the grid edge. Additionally, the market is witnessing increased demand for mobile workforce management integration, allowing field crews to access real-time grid information. Emerging trends include the convergence of ADMS with distributed energy resource management systems (DERMS), the development of microservices-based architectures for greater flexibility, and the incorporation of digital twin technology for enhanced grid modeling and simulation capabilities.

How did COVID-19 impact the ADMS market and what is the recovery trajectory?

The COVID-19 pandemic initially disrupted the ADMS market through supply chain interruptions, delayed project implementations, and reduced capital expenditure by utilities facing economic uncertainty. However, the pandemic also highlighted the critical importance of resilient and remotely manageable grid infrastructure, accelerating certain aspects of digital transformation in the utility sector. The recovery trajectory has been robust, with utilities recognizing the need for enhanced grid visibility and remote operation capabilities. Post-pandemic, the market has seen accelerated adoption of cloud-based solutions and increased focus on cybersecurity. The recovery has been characterized by a shift toward more agile deployment models and increased emphasis on operational efficiency, driving renewed investment in ADMS solutions as utilities seek to build more resilient and flexible grid infrastructure.

What is the competitive landscape of the ADMS market?

The ADMS market features a mix of established technology giants, specialized grid solutions providers, and innovative startups competing for market share. The competitive landscape is characterized by strategic partnerships, acquisitions, and collaborations as companies seek to expand their technological capabilities and geographic presence. Major players like ABB, Siemens, and Schneider Electric leverage their extensive utility relationships and comprehensive product portfolios, while specialized firms like Survalent Technology and Open Systems International focus on innovative niche solutions. The market is experiencing increasing consolidation as larger companies acquire smaller, innovative firms to enhance their technological capabilities. Competition is intensifying around cloud-based solutions, AI integration, and interoperability standards, with companies differentiating themselves through their ability to offer end-to-end solutions that address the evolving needs of modern utilities.

What are the key findings and high-level overview of the ADMS market?

The ADMS market is experiencing unprecedented growth driven by the global energy transition and smart grid initiatives. The market is transitioning from traditional, siloed systems to integrated, intelligent platforms that can manage the complexities of modern power distribution. Key findings indicate that utilities are increasingly prioritizing ADMS investments to enhance grid reliability, integrate renewable energy sources, and improve operational efficiency. The market is characterized by rapid technological advancements, with AI, machine learning, and cloud computing becoming integral components of next-generation ADMS solutions. Regional analysis shows varying adoption rates, with North America and Europe leading in mature markets, while Asia-Pacific presents significant growth opportunities. The competitive landscape is dynamic, with both established players and innovative newcomers contributing to market evolution through technological innovation and strategic partnerships.

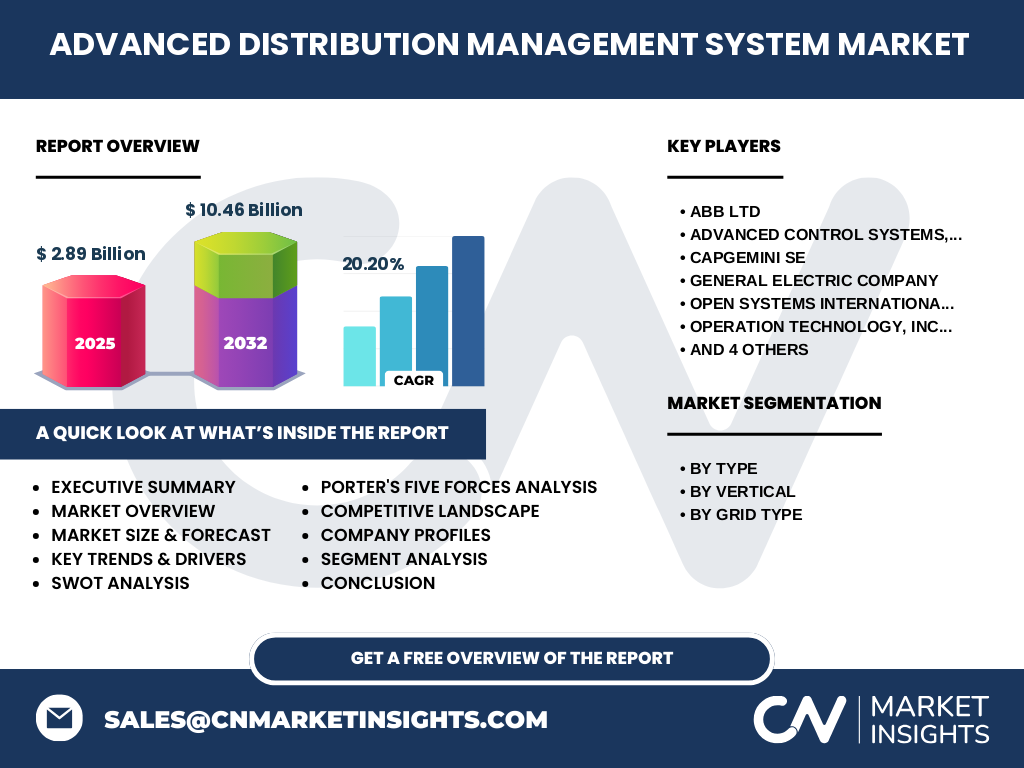

What are the market projections for the ADMS market from 2025 to 2032?

The ADMS market is projected to experience substantial growth from 2025 to 2032, with the market size expected to increase from USD 2.89 billion in 2025 to USD 10.46 billion by 2032, representing a robust CAGR of 20.20%. This growth trajectory reflects the increasing urgency for grid modernization, the accelerating energy transition, and the rising complexity of power distribution networks. The forecast period will likely see accelerated adoption of cloud-based ADMS solutions, increased integration of artificial intelligence and machine learning capabilities, and growing demand for solutions that can manage distributed energy resources. Regional variations in growth rates are expected, with emerging markets in Asia-Pacific and Latin America potentially outpacing mature markets in North America and Europe. The forecast also suggests increasing consolidation in the market as larger players acquire innovative startups to enhance their technological capabilities and market reach.

How is the ADMS market segmented by type and what are the size and share distributions?

The ADMS market is segmented by type into Solutions and Services. The Solutions segment encompasses the core ADMS software platforms, including distribution management, outage management, and SCADA integration capabilities. This segment represents the foundational technology that enables utilities to monitor and control their distribution networks. The Services segment includes implementation, consulting, maintenance, and support services that are essential for successful ADMS deployment and operation. While specific market share data is not provided, the Solutions segment typically accounts for a larger portion of the market value due to the significant investment required for core ADMS platforms. However, the Services segment is experiencing rapid growth as utilities increasingly seek expertise for complex implementations and ongoing support. The balance between these segments is shifting as the market matures, with growing emphasis on value-added services and customization to meet specific utility needs.

How is the ADMS market distributed globally by region?

The global ADMS market exhibits distinct regional characteristics shaped by varying levels of grid modernization, regulatory frameworks, and investment patterns. North America, led by the United States, represents a mature market with high ADMS adoption driven by aging infrastructure replacement and smart grid initiatives. Europe follows closely, with strong government support for renewable energy integration and grid modernization programs. The Asia-Pacific region is emerging as the fastest-growing market, fueled by rapid urbanization, increasing electricity demand, and significant infrastructure investments in countries like China and India. Latin America and the Middle East & Africa represent developing markets with growing potential as utilities in these regions begin to invest in advanced grid management solutions. While specific regional market share data is not provided, the distribution reflects the varying stages of grid development and the differing priorities of utilities across regions in addressing their unique grid management challenges.

What is the detailed regional performance of the ADMS market?

Regional performance in the ADMS market varies significantly based on local market conditions, regulatory environments, and infrastructure maturity. In North America, the market is characterized by high adoption rates driven by stringent reliability standards, aging infrastructure replacement needs, and strong utility investment in smart grid technologies. Europe's performance is bolstered by ambitious renewable energy targets, supportive regulatory frameworks, and collaborative initiatives like the European Network of Transmission System Operators for Electricity (ENTSO-E). The Asia-Pacific region shows the most dynamic growth, with countries like China and India investing heavily in grid modernization to support rapid economic development and increasing electricity demand. Japan and South Korea represent mature markets with advanced technological adoption. Latin America is experiencing gradual growth as utilities begin to address reliability issues and integrate renewable energy sources. The Middle East & Africa region presents unique opportunities driven by the need to support growing populations and diversify energy sources away from fossil fuels.

Who are the leading companies in the ADMS market and what are their strategies?

The ADMS market is dominated by several key players, each employing distinct strategies to maintain and expand their market positions. ABB Ltd leverages its extensive global presence and comprehensive portfolio of automation solutions to offer integrated ADMS platforms. General Electric Company focuses on digital transformation, emphasizing the integration of ADMS with its Predix platform for enhanced analytics capabilities. Schneider Electric differentiates itself through its EcoStruxure architecture, which provides open, interoperable solutions. Siemens AG emphasizes its expertise in both energy and automation, offering ADMS solutions that integrate seamlessly with its broader portfolio. Oracle Corporation leverages its cloud infrastructure and enterprise software expertise to provide cloud-based ADMS solutions. These companies, along with others like Advanced Control Systems, Open Systems International, and Survalent Technology, are pursuing strategies that include strategic acquisitions, partnerships with utilities, investment in R&D for AI and machine learning integration, and expansion into emerging markets to strengthen their competitive positions.

What does Porter's Five Forces analysis reveal about the ADMS market?

Porter's Five Forces analysis of the ADMS market reveals a competitive landscape shaped by several key factors. The threat of new entrants is moderate, as the market requires significant technological expertise, established utility relationships, and substantial capital investment. However, innovative startups can still find opportunities in niche segments or through technological differentiation. The bargaining power of buyers (utilities) is relatively high due to the large investments involved and the availability of multiple vendors, which encourages competitive pricing and service quality. Suppliers (technology component providers) have moderate bargaining power, although this can vary based on the uniqueness of their offerings. The threat of substitutes is low, as ADMS represents a specialized solution for grid management with few direct alternatives. Competitive rivalry is intense, characterized by ongoing technological innovation, strategic partnerships, and mergers and acquisitions as companies seek to differentiate their offerings and expand their market presence.

What are the strengths, weaknesses, opportunities, and threats in the ADMS market?

The ADMS market exhibits distinct strengths including the growing global demand for grid modernization, the increasing complexity of power distribution networks, and the proven benefits of ADMS in improving grid reliability and efficiency. However, weaknesses exist in the form of high implementation costs, integration challenges with legacy systems, and the shortage of skilled personnel to manage advanced ADMS platforms. Significant opportunities are emerging from the accelerating energy transition, the rise of distributed energy resources, and the potential for AI and machine learning to enhance ADMS capabilities. Threats to the market include cybersecurity risks as ADMS platforms become more connected, regulatory uncertainties across different regions, and the potential for economic downturns to impact utility investment budgets. The market's ability to address these factors will be crucial in determining its continued growth and evolution.

How does the value chain in the ADMS market function?

The ADMS market value chain encompasses several interconnected stages, beginning with technology component suppliers who provide the hardware and software building blocks for ADMS solutions. These components are integrated by ADMS platform developers who create comprehensive solutions combining distribution management, outage management, and SCADA capabilities. System integrators play a crucial role in customizing and implementing these solutions for specific utility needs, ensuring compatibility with existing infrastructure. Utilities, as the primary customers, deploy ADMS solutions to optimize their distribution networks, improve reliability, and integrate renewable energy sources. Support and maintenance providers offer ongoing services to ensure system performance and address evolving utility needs. The value chain is increasingly incorporating cloud service providers as more ADMS solutions move to cloud-based deployments. This interconnected ecosystem creates value through technological innovation, customization, and the delivery of solutions that address the complex challenges of modern power distribution.

What are the key investment insights for the ADMS market?

Key investment insights for the ADMS market highlight several strategic opportunities for investors. The market's strong growth trajectory, with a projected CAGR of 20.20% through 2032, presents significant potential for returns. Investors should focus on companies that are leading in technological innovation, particularly those integrating AI, machine learning, and cloud computing capabilities into their ADMS solutions. Companies with strong utility relationships and proven track records in complex implementations represent lower-risk investment opportunities. The trend toward cloud-based solutions and the increasing importance of cybersecurity features in ADMS platforms suggest potential investment areas in these technologies. Additionally, companies expanding into high-growth emerging markets, particularly in Asia-Pacific, may offer attractive growth prospects. Strategic partnerships and acquisitions that enhance technological capabilities or expand geographic reach are indicators of companies positioning themselves for long-term success in this evolving market.

What are the key conclusions and takeaways from the ADMS market analysis?

The ADMS market analysis reveals a sector experiencing robust growth driven by the global energy transition and the increasing complexity of power distribution networks. The market's projected expansion from USD 2.89 billion in 2025 to USD 10.46 billion by 2032 underscores the critical importance of advanced grid management solutions in modern energy systems. Key takeaways include the accelerating adoption of cloud-based and AI-enhanced ADMS solutions, the growing importance of cybersecurity features, and the increasing integration of distributed energy resource management capabilities. The market is characterized by intense competition, technological innovation, and strategic consolidation as companies seek to enhance their offerings and expand their market presence. Regional variations in adoption rates and growth potential highlight the importance of localized strategies, while the overall market trajectory points to ADMS becoming an essential component of future-proof power distribution infrastructure.

How was this research on the ADMS market conducted?

This research on the Advanced Distribution Management System market was conducted through a comprehensive methodology combining primary and secondary research approaches. Primary research involved interviews with industry experts, utility executives, and technology providers to gather firsthand insights into market trends, challenges, and opportunities. Secondary research encompassed extensive review of industry reports, company financial statements, regulatory filings, and market databases to validate and supplement primary findings. The research methodology included detailed analysis of market dynamics, competitive landscapes, and technological trends. Data triangulation techniques were employed to ensure accuracy and reliability of market size and growth projections. The research also incorporated analysis of patent filings, partnership announcements, and product launches to identify emerging trends and competitive strategies. This multi-faceted approach provided a comprehensive understanding of the ADMS market, its key drivers, and future outlook.

What is the scope and coverage of this ADMS market research?

The scope of this ADMS market research encompasses a comprehensive analysis of the global market from 2025 to 2032, covering key market segments, regional dynamics, competitive landscape, and technological trends. The research covers the market by type (Solutions and Services), by vertical (Industrial and Commercial), and by grid type (High Voltage Grid, Medium Voltage Grid, and Low Voltage Grid). Geographic coverage includes major regions such as North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with detailed analysis of market conditions and growth potential in each region. The research also examines key market players, their strategies, and recent developments. While the research provides extensive coverage of market dynamics and trends, it focuses specifically on ADMS solutions and does not extend to other segments of the broader smart grid market. The analysis is based on available data and industry insights, providing a strategic overview of the market's current state and future trajectory.

Who are the key companies in the ADMS market and what are their recent developments?

The key companies in the ADMS market include ABB Ltd, Advanced Control Systems, Inc. (Indra Company), Capgemini SE, General Electric Company, Open Systems International, Inc. (Emerson Electric), Operation Technology, Inc. (Etap), Oracle Corporation, Schneider Electric, Siemens AG, and Survalent Technology Corporation. Recent developments in the market include strategic partnerships and acquisitions aimed at enhancing technological capabilities. For instance, major players are increasingly focusing on cloud-based solutions and AI integration to improve their ADMS offerings. Companies are also investing in expanding their presence in emerging markets, particularly in Asia-Pacific, where rapid urbanization and infrastructure development are driving demand for advanced grid management solutions. Product launches have emphasized enhanced cybersecurity features, improved interoperability with distributed energy resources, and advanced analytics capabilities. These companies are also participating in industry consortiums to develop interoperability standards and promote the adoption of ADMS solutions across the utility sector.