What is the North America Photovoltaic Market Overview – Definition, scope, and significance?

The North America Photovoltaic (PV) Market encompasses the production, distribution, and installation of solar PV technologies across the United States, Canada, and Mexico. It includes organic and inorganic component manufacturers, cell and optics producers, as well as tracker system suppliers, serving residential, commercial, and utility‑scale applications. The market is a cornerstone of the region’s clean‑energy transition, driving decarbonization, job creation, and energy independence while supporting climate‑policy goals.

What are the key drivers, restraints, challenges, and opportunities shaping the North America Photovoltaic Market?

Primary drivers include strong federal and state incentives, declining solar‑module costs, and expanding corporate sustainability commitments. Restraints involve intermittency concerns, land‑use constraints for utility projects, and supply‑chain volatility for critical raw materials. Challenges arise from permitting delays and grid‑integration complexities. Opportunities stem from emerging organic PV technologies, advanced tracking systems, and growing demand for rooftop residential installations powered by financing innovations.

Which growth trends are currently influencing the North America Photovoltaic Market?

Current trends feature a rapid shift toward utility‑scale solar farms equipped with high‑efficiency trackers, increased adoption of bifacial and organic PV cells, and the integration of energy‑storage solutions to mitigate intermittency. Digital twins and AI‑driven performance monitoring are gaining traction, while economies of scale are pushing module prices lower. Distributed generation, especially in the residential segment, continues to expand due to net‑metering policies.

How did COVID‑19 impact the North America Photovoltaic Market and what is the recovery trajectory?

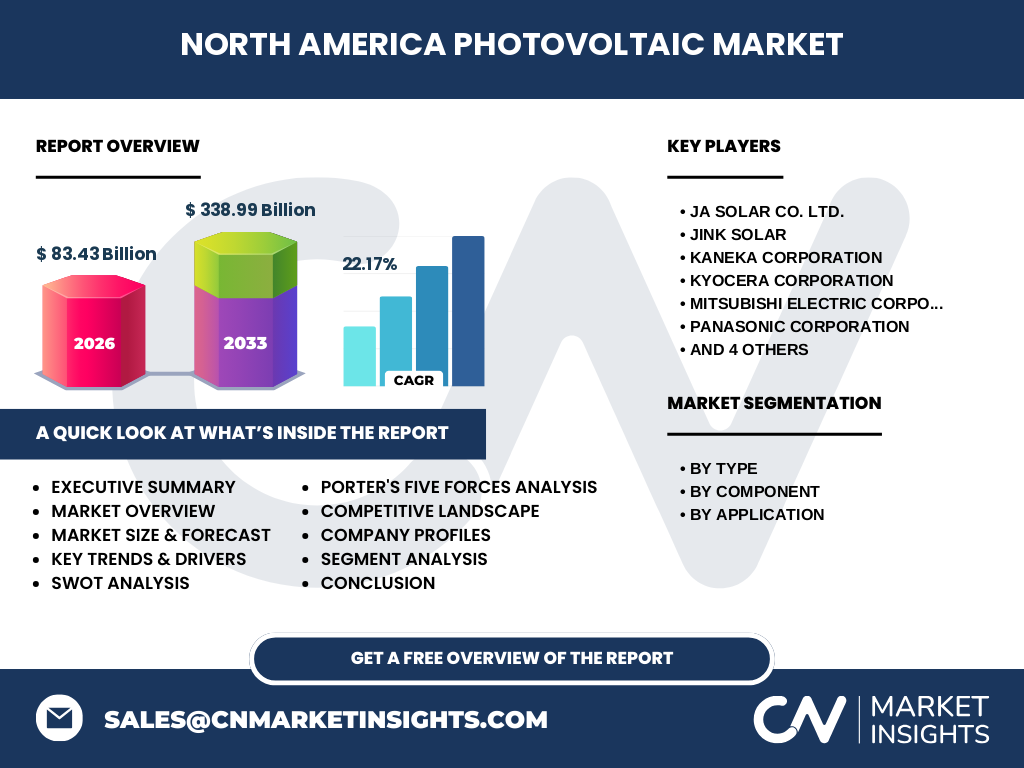

The pandemic temporarily slowed project timelines because of labor shortages and supply‑chain disruptions, leading to a modest dip in installations during 2020. However, stimulus packages and renewed focus on resilient, renewable infrastructure accelerated demand post‑2021. The market rebounded strongly, and the current CAGR of 22.17% reflects a robust recovery, supported by renewed financing and policy support.

Who are the major competitors in the North America Photovoltaic Market and what is the state of market consolidation?

Key players include JA Solar Co. Ltd., Jink Solar, Kaneka Corporation, Kyocera Corporation, Mitsubishi Electric Corporation, Panasonic Corporation, Renesola Co. Ltd., Sharp Corporation, Shunfeng International Clean Energy Co., Ltd., and Trina Solar. The sector is experiencing moderate consolidation as larger manufacturers acquire niche technology firms, especially in organic PV and advanced tracker segments, to broaden product portfolios and achieve cost synergies.

What are the high‑level takeaways in the Executive Summary of the North America Photovoltaic Market?

The market is valued at USD 83.43 billion in 2026 and is projected to reach USD 338.99 billion by 2033, driven by a 22.17% CAGR. Strong policy support, falling component costs, and expanding residential and utility installations underpin growth. Organic PV and smart tracking solutions present high‑value opportunities, while supply‑chain resilience and grid integration remain focal challenges for stakeholders.

What are the forecast expectations for the North America Photovoltaic Market for 2025‑2032?

Based on the stated CAGR of 22.17%, the market is expected to maintain double‑digit expansion throughout the 2025‑2032 horizon, moving from the 2026 baseline of USD 83.43 billion toward the 2033 forecast of USD 338.99 billion. Growth will be propelled by utility‑scale projects, residential financing schemes, and the rollout of next‑generation organic and inorganic component technologies.

How is the North America Photovoltaic Market sized and shared across its segmentation?

Segmentation by type divides the market into organic components and inorganic components, each serving all downstream applications. By component, the market splits among cells, optics, and trackers, with cells representing the largest share due to core module demand. Application‑wise, residential, commercial, and utility segments each capture distinct share portions, with utility installations driving the highest absolute revenue because of large‑scale capacity.

What is the global North America Photovoltaic Market size and share by region?

Within the global PV landscape, the North America region accounts for a substantial share, anchored by a 2026 market size of USD 83.43 billion. While exact global figures are not disclosed, the region’s robust growth trajectory and the projected 2027‑2033 total of USD 338.99 billion illustrate its prominent role in worldwide solar adoption.

What does the regional analysis reveal about the North America Photovoltaic Market’s performance?

United States leads the market, driven by extensive utility‑scale farms and aggressive residential incentives. Canada shows steady growth, focusing on commercial rooftop projects and offshore wind‑solar hybrid initiatives. Mexico’s market is emerging, propelled by large‑scale solar parks supported by government auctions. Each sub‑region contributes uniquely to the collective CAGR, with policy alignment being the common growth catalyst.

Which leading companies operate in the North America Photovoltaic Market and what are their strategies?

JA Solar, Trina Solar, and Panasonic emphasize high‑efficiency module portfolios and strategic joint ventures with local EPC firms. Kyocera and Mitsubishi Electric leverage their diversified electronics base to integrate PV with storage and smart‑grid solutions. Kaneka and Shunfeng focus on organic component R&D to capture emerging niche segments. Across the board, companies pursue vertical integration, regional manufacturing expansion, and strategic partnerships to accelerate market penetration.

How does Porter’s Five Forces analysis apply to the North America Photovoltaic Market?

Threat of new entrants is moderate due to high capital requirements but eased by modular manufacturing. Bargaining power of suppliers is elevated for scarce raw materials such as polysilicon, though organic component suppliers diversify risk. Bargaining power of buyers is strong, especially large utilities demanding cost‑competitive contracts. Threat of substitutes remains low, as solar retains the most favorable levelized cost of electricity among renewables. Industry rivalry is intense, with numerous global players competing on price, efficiency, and service.

What are the SWOT insights for the North America Photovoltaic Market?

Strengths: Strong policy incentives, declining technology costs, and abundant solar resources.

Weaknesses: Intermittency and grid‑integration challenges, reliance on imported raw materials.

Opportunities: Organic PV breakthroughs, advanced tracking systems, and integrated storage.

Threats: Potential policy rollbacks, supply‑chain disruptions, and competitive pressure from other renewables.

What does the value‑chain analysis reveal about the North America Photovoltaic Market?

The value chain begins with raw‑material sourcing (silicon, organic polymers), proceeds to component manufacturing (cells, optics, trackers), then to module assembly and testing. Distribution channels include wholesale distributors and direct EPC contracts, followed by installation, operation, and maintenance services. Emerging nodes such as recycling and second‑life module markets are beginning to add value at the end of the product life cycle.

What key investment insights can be drawn for the North America Photovoltaic Market?

Investors should prioritize companies with vertically integrated supply chains and strong footholds in organic component R&D, as these areas promise margin expansion. Funding opportunities exist in utility‑scale projects supported by long‑term power purchase agreements and in residential financing platforms enabled by tax credits. Strategic M&A in tracker technology and energy‑storage integration can also unlock synergistic growth.

What are the concluding takeaways for the North America Photovoltaic Market?

The market is on a rapid expansion path, underpinned by supportive policy frameworks and a compelling economics case for solar. While supply‑chain resilience and grid modernization are ongoing concerns, the high CAGR and sizable forecast indicate a lucrative landscape for manufacturers, developers, and investors alike.

Which research methodology was employed to develop this market report?

The study combined primary interviews with industry executives, secondary data from company filings, government publications, and reputable market databases. Quantitative analysis employed trend extrapolation based on the provided CAGR of 22.17%, while qualitative insights were derived from expert opinions and technology assessments.

What is the defined scope of this research?

The scope covers the North American region (U.S., Canada, Mexico) and includes segmentation by type (organic, inorganic), component (cells, optics, trackers), and application (residential, commercial, utility). The timeframe spans historical data through 2026, with forecasts to 2033. The analysis excludes unrelated renewable sectors and focuses solely on photovoltaic technologies.

Which key companies are highlighted and what recent developments have they announced?

JA Solar reported a new 1‑GW manufacturing line in Texas aimed at meeting domestic demand. Trina Solar launched a bifacial organic‑hybrid module targeting utility projects. Panasonic announced a partnership with a major U.S. utility to integrate storage with its PV systems. Kyocera introduced an AI‑driven tracker platform to boost energy yield. Shunfeng International Clean Energy secured financing for a 500‑MW Mexican solar park, reflecting cross‑border expansion.