What is the Rugged Servers Market overview – definition, scope, and significance?

The Rugged Servers market comprises high‑performance computing platforms engineered to operate reliably in harsh environments such as extreme temperatures, vibration, dust, and moisture. It spans universal and dedicated server models and serves critical sectors—including aerospace, oil & gas, manufacturing, telecom, mining, energy, logistics, and construction. These servers enable continuous data processing and mission‑critical operations where standard IT equipment would fail, making them essential for operational resilience and safety.

What are the Rugged Servers market drivers, restraints, challenges, and opportunities?

Key drivers include the growing need for edge computing in remote locations, expansion of IoT devices, and increasing infrastructure investment in demanding industries. Restraints stem from higher upfront costs and limited awareness of rugged solutions. Challenges involve ensuring compliance with diverse regulatory standards and maintaining supply chain continuity for specialized components. Opportunities arise from the rollout of 5G networks, renewable‑energy projects, and the demand for modular, upgradable designs.

What growth trends are shaping the Rugged Servers market?

Current trends feature a shift toward compact, low‑power rugged servers that support AI and analytics at the edge. Manufacturers are integrating advanced thermal‑management and modular architectures to extend lifespan. There is also a rise in hybrid deployment models combining on‑premise rugged hardware with cloud services, enabling flexible scaling while preserving on‑site reliability.

How did COVID‑19 impact the Rugged Servers market and what is the recovery trajectory?

The pandemic accelerated remote‑site operations, prompting higher adoption of rugged servers for field data collection and uninterrupted communications. Supply‑chain disruptions temporarily slowed production, but demand recovered quickly as industries resumed projects. The market is now on a steady growth path, supported by post‑COVID digital transformation initiatives that prioritize resilient edge infrastructure.

Who are the main competitors and what is the competitive landscape in the Rugged Servers market?

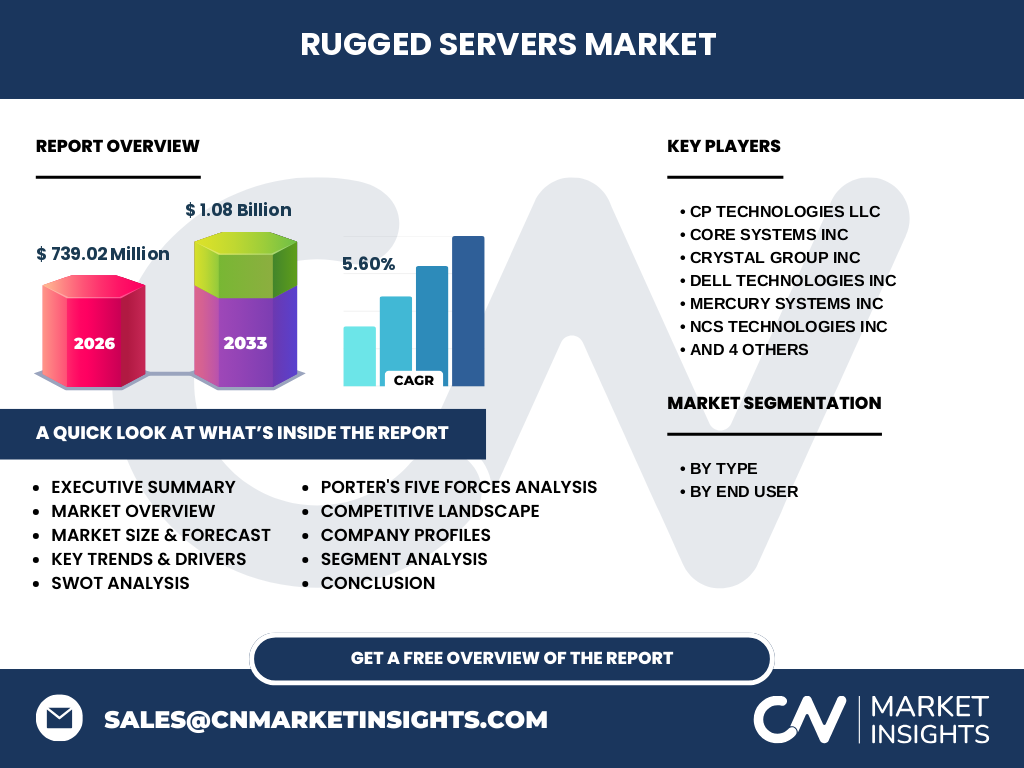

Leading players include CP Technologies LLC, Core Systems Inc, Crystal Group Inc, Dell Technologies Inc, Mercury Systems Inc, NCS Technologies Inc, Sparton Corp, Systel Inc, Trenton Systems Inc, and ZMicro Inc. Competition centers on technology innovation, customization capabilities, and after‑sales support. Recent consolidation trends show strategic partnerships and acquisitions aimed at expanding product portfolios and geographic reach.

What are the key findings in the executive summary of the Rugged Servers market?

The market is projected to grow from a 2026 size of $739.02 million to $1.08 billion by 2033, reflecting a 5.60 % CAGR. Growth is driven by expanding edge‑computing needs across high‑risk sectors and the rollout of 5G. While cost remains a barrier, rapid innovation and increasing awareness are expected to sustain momentum through 2032.

What is the Rugged Servers market forecast for the 2025‑2032 period?

Based on the provided CAGR of 5.60 %, the market is anticipated to maintain steady expansion, reaching approximately $1.08 billion by 2033. Year‑over‑year growth will be supported by rising demand for durable edge devices, increased investment in renewable‑energy infrastructure, and ongoing digitalization of industrial processes.

How is the Rugged Servers market sized and shared by segmentation?

Segmentation by type divides the market into universal and dedicated rugged servers, each catering to different performance and customization requirements. By end‑user, the market is split among aerospace, oil & gas, manufacturing, telecommunications, mining, energy, logistics, and construction, reflecting the broad applicability of rugged systems across sectors that operate in extreme conditions.

What is the global Rugged Servers market size and share by region?

The market’s global footprint is anchored in regions with intensive industrial activity and remote operations. While specific regional monetary values are not disclosed, North America, Europe, and Asia‑Pacific collectively dominate due to mature aerospace, oil & gas, and manufacturing bases, with emerging growth observed in Latin America and the Middle East as infrastructure projects expand.

What does the regional analysis of the Rugged Servers market reveal?

North America leads in technology adoption and hosts several key manufacturers, driving early‑stage innovation. Europe benefits from strong aerospace and defense programs, while Asia‑Pacific shows rapid growth fueled by expanding telecom networks and mining activities. Latin America and the Middle East present emerging opportunities linked to new energy ventures and construction projects.

Which companies are leading in the Rugged Servers market and what are their strategies?

Top players such as Dell Technologies Inc and Mercury Systems Inc leverage extensive R&D budgets to deliver modular, high‑density solutions. niche firms like CP Technologies LLC focus on customized designs for aerospace and defense. Strategic moves include partnerships with component suppliers, acquisition of complementary technologies, and expanding service‑oriented offerings to differentiate in a competitive field.

How does Porter’s Five Forces analysis apply to the Rugged Servers market?

Threat of new entrants is moderate due to high capital requirements and specialized expertise. Bargaining power of suppliers is relatively high because of limited sources for rugged‑grade components. Bargaining power of buyers is moderate; while few large customers exist, they demand tailored solutions. Threat of substitutes is low, as few alternatives match durability. Industry rivalry is intense, driven by innovation cycles and service quality.

What are the strengths, weaknesses, opportunities, and threats (SWOT) of the Rugged Servers market?

Strengths: proven reliability, essential for mission‑critical applications. Weaknesses: higher cost and longer sales cycles. Opportunities: emergence of 5G, AI at the edge, and renewable‑energy projects. Threats: supply‑chain volatility for specialized parts and potential market saturation in mature segments.

What does the value chain of the Rugged Servers market look like?

The value chain begins with raw‑material sourcing for ruggedized components, followed by specialized engineering and design. Manufacturing includes assembly, testing for environmental compliance, and certification. Distribution involves direct sales to large enterprises and channel partners for smaller clients. Post‑sale services—maintenance, upgrades, and technical support—complete the chain, adding recurring revenue streams.

What key investment insights can be drawn from the Rugged Servers market?

Investors should target companies with strong modular platforms and proven service networks, as these generate stable cash flows. Funding R&D in thermal‑management and AI integration offers high upside. Geographic diversification, especially into Asia‑Pacific, can capture emerging demand, while strategic alliances with telecom providers can unlock new revenue channels.

What are the main conclusions of the Rugged Servers market report?

The market is on a clear growth trajectory, driven by expanding edge‑computing needs across rugged environments. Despite cost challenges, the 5.60 % CAGR and a projected size of $1.08 billion by 2033 indicate a robust outlook. Companies that innovate in modularity, serviceability, and integration with emerging technologies will likely lead the market.

How was the research methodology for this Rugged Servers market report conducted?

The study combined primary interviews with industry experts, supplier surveys, and secondary data from company filings, market databases, and trade publications. Quantitative analysis employed trend extrapolation based on the provided CAGR, while qualitative insights were derived from competitor assessments and technology roadmaps.

What is the scope of the Rugged Servers market research?

The research covers global market size, segmentation by type and end‑user, regional distribution, competitive landscape, and forward‑looking forecasts through 2032. It excludes detailed financial breakdowns beyond the supplied figures and does not model scenario‑based projections beyond the standard CAGR assumption.

Which key companies are highlighted and what recent developments have they announced?

Featured companies include CP Technologies LLC, Core Systems Inc, Crystal Group Inc, Dell Technologies Inc, Mercury Systems Inc, NCS Technologies Inc, Sparton Corp, Systel Inc, Trenton Systems Inc, and ZMicro Inc. Recent activities comprise Dell’s launch of a next‑generation modular rugged server, Mercury Systems’ acquisition of a thermal‑management startup, and Trenton Systems’ partnership with a major telecom operator to supply edge‑computing hardware for 5G rollouts.