1. What is the Semiconductor Assembly and Testing Services Market and why is it significant?

The Semiconductor Assembly and Testing Services Market encompasses outsourced activities that convert raw silicon wafers into finished semiconductor devices ready for integration into electronic systems. This includes wafer‑level packaging, die‑attach, wire‑bonding, encapsulation, and comprehensive electrical and reliability testing. The market’s significance lies in its role as a critical enabler for rapid product cycles, cost efficiency, and quality assurance across virtually every modern technology sector, from consumer gadgets to automotive safety systems.

2. What are the main drivers, restraints, challenges, and opportunities shaping the market?

Key drivers include the surge in demand for advanced packaged chips, the expansion of high‑performance computing, and the growing complexity of system‑in‑package (SiP) architectures. Restraints stem from high capital intensity and the need for continuous process upgrades. Challenges involve supply‑chain volatility, skilled‑labor shortages, and stringent environmental regulations. Opportunities arise from emerging applications such as 5G, autonomous vehicles, and medical wearables that require miniaturized, high‑density solutions.

3. Which growth trends are currently influencing the market?

Current trends feature a shift toward heterogeneous integration, where multiple functional blocks are combined in a single package, and the adoption of fan‑out wafer‑level packaging (FOWLP) for thinner form factors. There is also increasing automation through AI‑driven inspection and predictive maintenance, as well as a rise in “test‑as‑a‑service” models that provide flexible, on‑demand testing capacity for low‑volume runs.

4. How did COVID‑19 affect the Semiconductor Assembly and Testing Services Market and what is the recovery outlook?

The pandemic disrupted logistics, reduced workforce availability, and caused temporary shut‑downs of fab and test facilities, leading to delayed shipments and inventory imbalances. However, post‑pandemic recovery has been strong, driven by heightened demand for consumer electronics, telecommunication equipment, and automotive electronics. The market has rebounded faster than many peers, positioning it for robust growth in the coming years.

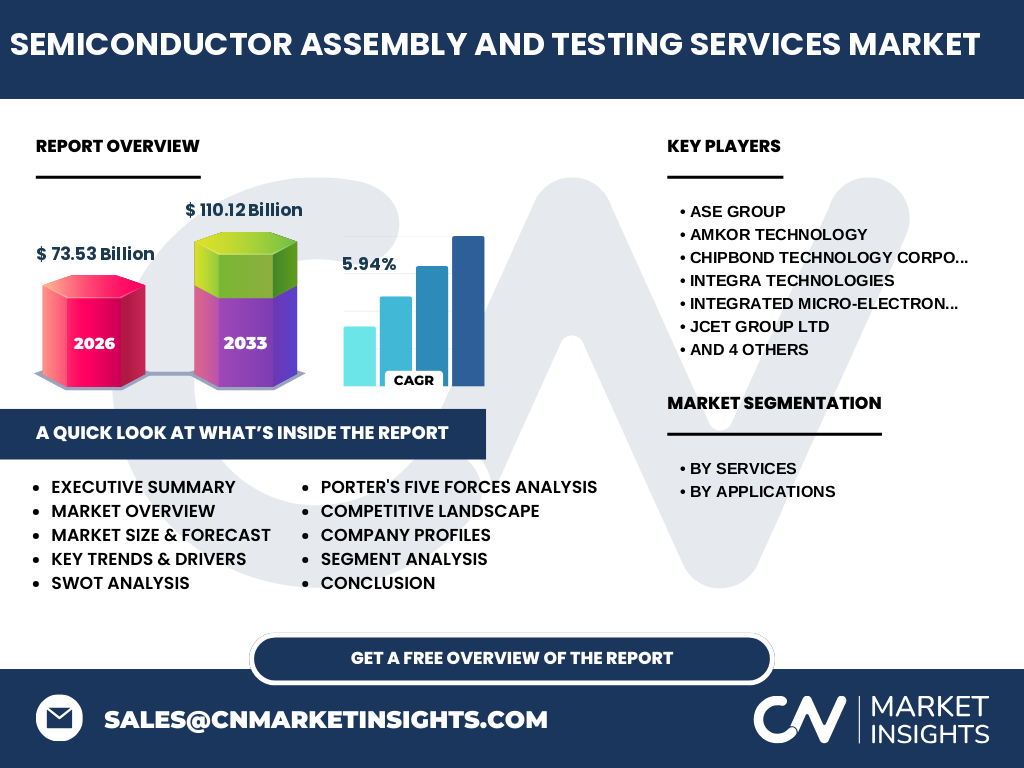

5. Who are the major competitors and what is the state of market consolidation?

Leading competitors include ASE Group, Amkor Technology, Chipbond Technology Corporation, Integra Technologies, Integrated Micro‑Electronics, Inc., JCET Group Ltd, Powertech Technology Inc., Siliconware Precision Industries Co., Ltd, Teledyne Technologies, and Unisem Group. The sector has seen moderate consolidation, with large players acquiring niche firms to broaden service portfolios, enhance geographic reach, and secure advanced packaging capabilities.

6. What are the key findings from the executive summary?

The market is valued at $73.53 billion in 2026 and is projected to reach $110.12 billion by 2033, reflecting a CAGR of 5.94 %. Growth is propelled by expanding applications in consumer electronics and automotive sectors, alongside technological shifts toward advanced packaging and AI‑enabled testing. Competitive dynamics are shaped by a handful of global leaders that are investing heavily in R&D and strategic acquisitions.

7. What are the forecast expectations for 2025‑2032?

Based on the provided CAGR, the market will continue a steady expansion trajectory, maintaining double‑digit billions in annual revenue. Steady demand from high‑growth segments such as automotive electronics and 5G infrastructure will sustain the upward trend, while incremental capacity additions and technology upgrades will support higher value‑added services.

8. How is the market sized and shared by segment?

Segmentation by services divides the market into Assembly & Packaging Services and Testing Services. By application, the market is distributed across Consumer Electronics, Automotive, Medical, Industrial, and Other Applications. While exact monetary shares are not disclosed, the breadth of applications highlights a diversified revenue base, reducing dependence on any single end‑use sector.

9. What is the global market size and share by region?

The global Semiconductor Assembly and Testing Services Market reached $73.53 billion in 2026. Regional distribution covers North America, Europe, Asia‑Pacific, and Rest of World, reflecting the worldwide nature of semiconductor supply chains. Asia‑Pacific, driven by Taiwan, South Korea, and China, traditionally holds the largest proportion, while North America and Europe contribute significant high‑value testing activities.

10. How does each region perform in the market?

Asia‑Pacific leads with extensive manufacturing hubs and a dense ecosystem of foundries and assembly houses. North America focuses on advanced testing, reliability services, and high‑mix low‑volume production for aerospace and defense. Europe emphasizes precision packaging for automotive and industrial automation. Emerging markets in Latin America and the Middle East are beginning to attract investment for localized assembly capabilities.

11. Which companies lead the market and what are their strategies?

ASE Group and Amkor Technology dominate through broad service portfolios and global footprints. Their strategies include expanding capacity for advanced packaging (e.g., TSV, FOWLP), forging long‑term partnerships with OEMs, and investing in automation. Other players like JCET Group and Siliconware Precision Industries pursue niche specialization in SiP and MEMS testing, while Teledyne Technologies leverages its metrology expertise to offer premium test solutions.

12. What does Porter’s Five Forces reveal about market competitiveness?

Threat of new entrants is moderate due to high capital requirements. Bargaining power of suppliers is low, as raw materials are commoditized. Bargaining power of buyers is moderate to high, given OEMs’ focus on cost and quality. Threat of substitutes is limited; alternative manufacturing models cannot fully replace specialized assembly and testing. Rivalry among existing firms is intense, driving continuous innovation and price competition.

13. What are the SWOT insights for the market?

Strengths: Essential role in the semiconductor value chain, high barriers to entry, and growing demand for advanced packaging.

Weaknesses: Capital‑intensive upgrades and dependence on cyclical end‑market demand.

Opportunities: Expansion into AI‑driven testing, growth of automotive electronics, and development of sustainable packaging processes.

Threats: Geopolitical trade tensions, supply‑chain disruptions, and rapid technology shifts that may outpace capacity expansion.

14. How does the value chain of the market function?

The value chain starts with wafer fabrication by foundries, followed by die preparation, assembly & packaging (die‑attach, wire‑bonding, encapsulation), then comprehensive electrical and reliability testing. Post‑test, products move to final inspection, marking, and shipment. Supporting activities include design‑for‑assembly, material sourcing, and after‑sales reliability support.

15. What investment insights can be derived from the market?

Investors should target companies with diversified service portfolios, strong R&D pipelines for next‑generation packaging, and strategic partnerships with leading OEMs. Capital allocation toward automation, AI‑enabled test analytics, and environmentally friendly processes will likely yield higher margins. Emerging regions offering cost‑effective labor and growing domestic demand also present attractive entry points.

16. What are the main conclusions of the market analysis?

The Semiconductor Assembly and Testing Services Market is on a robust growth path, underpinned by rising demand for sophisticated, miniaturized chips across multiple high‑growth sectors. The projected CAGR of 5.94 % positions the market to exceed $110 billion by 2033. Competitive pressures will intensify, emphasizing the need for technological leadership, capacity expansion, and strategic collaborations.

17. How was the research conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data from company reports, and reputable market databases. Trend analysis, competitive benchmarking, and financial modeling were used to derive forecasts and assess market dynamics.

18. What is the scope of the research?

The scope covers global Assembly & Packaging Services and Testing Services, segmented by application across Consumer Electronics, Automotive, Medical, Industrial, and Other Applications. Geographic coverage includes all major regions. Limitations are confined to publicly available data and disclosed financial figures.

19. Which key companies have recent developments worth noting?

ASE Group announced a new 300 mm FOWLP line to serve high‑density IoT devices. Amkor Technology unveiled a joint venture with a leading automotive OEM for safety‑critical chip testing. JCET Group reported acquisition of a niche SiP specialist to broaden its portfolio. Teledyne Technologies introduced AI‑based test analytics that reduce failure detection time by 30 %.