1. What is the Asia Pacific Endodontic Reparative Cement Market Overview – definition, scope, and significance?

The Asia Pacific Endodontic Reparative Cement market encompasses the production, distribution, and consumption of specialized cement materials used to repair and seal root canals, support dental restorations, and line cavities. It covers a range of product types—bioceramic‑based sealers, zinc oxide eugenol‑based, epoxy resin based, and calcium‑hydroxide based—served to end users such as hospitals, dental clinics, and ambulatory surgical centers. This market is significant because reparative cement improves treatment outcomes, reduces post‑operative complications, and drives demand for advanced endodontic procedures across rapidly urbanizing Asia Pacific economies.

2. What are the market drivers, restraints, challenges, and opportunities in the Asia Pacific Endodontic Reparative Cement market?

Key drivers include rising prevalence of dental disorders, increasing adoption of minimally invasive endodontic techniques, and growing health‑care expenditure in China, India, and Southeast Asian nations. Restraints stem from high product costs, stringent regulatory approvals, and limited reimbursement frameworks in some countries. Challenges involve skill gaps among dental practitioners and competition from alternative materials. Opportunities arise from emerging bioceramic technologies, expanding dental tourism, and potential partnerships with governmental oral‑health programs to broaden access.

3. What growth trends are shaping the Asia Pacific Endodontic Reparative Cement market?

Current trends feature a shift toward bioceramic‑based sealers due to superior biocompatibility and easier handling. Digital dentistry integration is prompting manufacturers to develop cement formulations compatible with CAD/CAM workflows. Additionally, there is a growing preference for single‑visit endodontic procedures, which boosts demand for fast‑setting, high‑strength cements. Emerging markets such as Vietnam and the Philippines are showing accelerated adoption, contributing to the region’s overall momentum.

4. How has COVID‑19 impacted the Asia Pacific Endodontic Reparative Cement market and what is the recovery trajectory?

The pandemic temporarily reduced elective dental visits, causing a short‑term dip in cement consumption across the region. Supply‑chain disruptions affected raw‑material availability, delaying product launches. Recovery began in late 2021 as clinics reopened and infection‑control protocols increased patient confidence. Since then, the market has rebounded robustly, supported by pent‑up demand for restorative care and heightened awareness of oral health’s role in overall immunity.

5. Who are the major competitors and what is the competitive landscape of the Asia Pacific Endodontic Reparative Cement market?

Leading players include Coltene Group, Dentsply Maillefer, IvoclarVivadent AG, Parkell, Inc., and Septodont Holding. These firms compete on product innovation, portfolio breadth, and strategic distribution networks. Recent consolidation activity shows partnerships with regional distributors and acquisitions of niche bioceramic technology firms, indicating a trend toward strengthening market presence and expanding product lines to capture emerging demand.

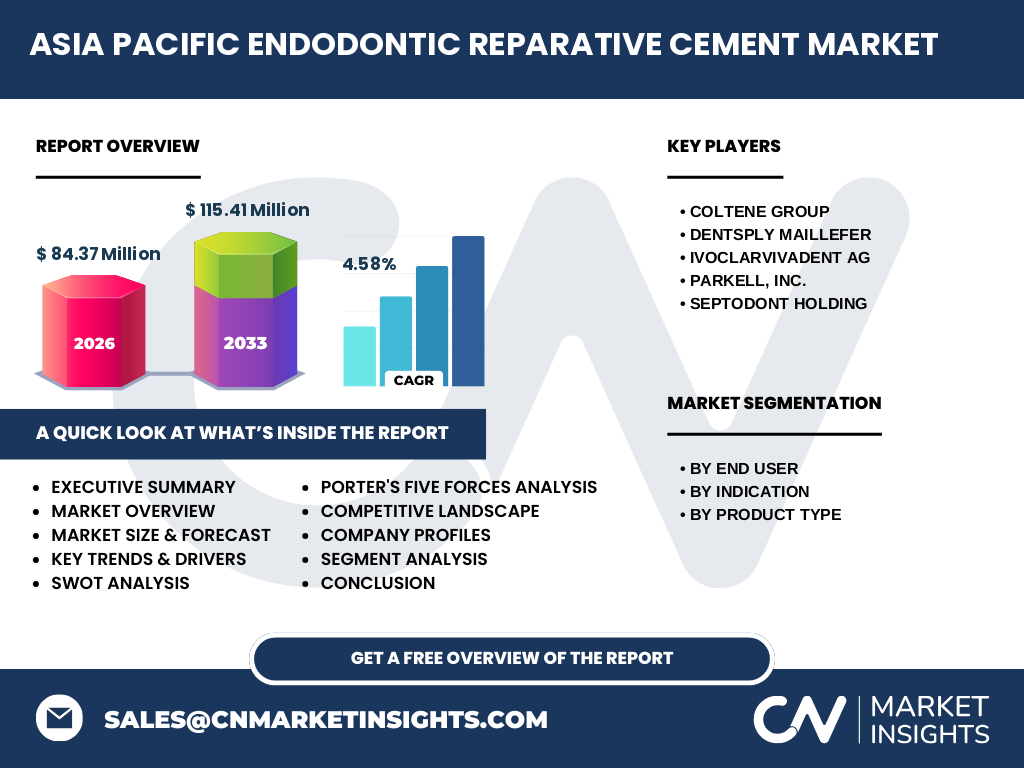

6. What are the high‑level findings in the executive summary of the Asia Pacific Endodontic Reparative Cement market?

The market is projected to grow from a 2026 value of USD 84.37 million to USD 115.41 million by 2033, reflecting a CAGR of 4.58 %. Growth is driven by expanding end‑user bases, especially dental clinics, and a clear preference for bioceramic‑based products. Competitive dynamics are intensifying, with major manufacturers investing in R&D and regional partnerships. Opportunities exist in untapped markets and in the development of cost‑effective, high‑performance cements.

7. What is the forecast for the Asia Pacific Endodontic Reparative Cement market from 2025 to 2032?

Based on the provided CAGR of 4.58 %, the market is expected to continue expanding steadily through 2032. Each successive year will see incremental growth, supported by rising oral‑health awareness, increased procedural volumes in hospitals and clinics, and the ongoing introduction of next‑generation cement formulations that address clinicians’ efficiency and patient safety concerns.

8. How is the market size and share broken down by segmentation?

Segmentation by end user reveals hospitals, dental clinics, and ambulatory surgical centers as distinct channels, with dental clinics holding the largest share due to the high volume of routine endodontic procedures. By indication, root canal obturation leads the demand, followed by dental restoration and cavity lining. Product‑type segmentation shows bioceramic‑based sealers gaining the fastest growth, while zinc oxide eugenol‑based and epoxy resin‑based cements retain steady demand, and calcium‑hydroxide based products occupy a niche segment for specialized clinical cases.

9. What is the geographic distribution of the market size and share across the Asia Pacific region?

The market is concentrated in major economies such as China, Japan, South Korea, India, and Australia, which together account for the majority of the USD 84.37 million base value. Emerging Southeast Asian markets contribute a growing share, reflecting increasing dental infrastructure investment and rising disposable incomes. While specific country‑level figures are not disclosed, the overall regional mix underscores both mature and high‑growth sub‑regions.

10. What are the key insights from the regional analysis of the Asia Pacific Endodontic Reparative Cement market?

China leads in volume due to its large population and expanding private dental chains. Japan and South Korea exhibit high per‑procedure spending, favoring premium bioceramic products. India shows rapid growth driven by governmental oral‑health initiatives and an expanding middle class. Southeast Asian countries, notably Indonesia and Thailand, are transitioning from import‑reliant markets to localized production, creating new supply‑chain opportunities.

11. Which companies are leading in the Asia Pacific Endodontic Reparative Cement market and what are their strategies?

Coltene Group focuses on expanding its bioceramic portfolio and leveraging digital marketing to educate clinicians. Dentsply Maillefer emphasizes strategic acquisitions of niche technology firms to enhance product differentiation. IvoclarVivadent AG invests in R&D for faster‑curing cements compatible with CAD/CAM systems. Parkell, Inc. pursues channel partnerships with regional distributors, while Septodont Holding concentrates on clinical training programs to drive product adoption.

12. How does Porter’s Five Forces analysis apply to this market?

Threat of new entrants is moderate due to high regulatory barriers and capital intensity. Bargaining power of buyers is growing as clinics demand cost‑effective yet high‑performance cements. Bargaining power of suppliers remains low because raw materials are commoditized. Threat of substitutes is limited, given the specialized nature of reparative cements. Rivalry among existing firms is intense, with frequent product launches and promotional activities shaping competitive dynamics.

13. What are the SWOT factors for the Asia Pacific Endodontic Reparative Cement market?

Strengths: Established product portfolios, increasing clinical evidence supporting bioceramics, and robust distribution networks.

Weaknesses: High cost relative to traditional materials and limited reimbursement in some jurisdictions.

Opportunities: Expansion into underserved Southeast Asian markets, development of low‑cost bioceramic alternatives, and integration with digital dentistry workflows.

Threats: Regulatory delays, price competition from generic manufacturers, and potential supply‑chain disruptions.

14. What does the value chain analysis reveal for this market?

The value chain starts with raw‑material sourcing (silica, calcium phosphates, polymers), moves through formulation and manufacturing (high‑precision mixing, sterile packaging), proceeds to distribution via specialized dental distributors, and ends with clinical use and post‑sale service (training, technical support). Value is added most significantly during R&D and product differentiation phases, while logistics and regulatory compliance represent critical cost centers.

15. What key investment insights can be drawn for stakeholders?

Investors should prioritize companies with strong bioceramic pipelines and proven regulatory clearance in multiple jurisdictions. Partnerships with local distributors in high‑growth markets such as India and Indonesia can accelerate market entry. Funding R&D for cost‑efficient formulations will address price sensitivity, while digital‑marketing initiatives can enhance clinician adoption rates, delivering higher return on investment.

16. What are the concluding takeaways from the Asia Pacific Endodontic Reparative Cement market analysis?

The market is on a clear growth trajectory, underpinned by a 4.58 % CAGR and expanding end‑user base. Bioceramic‑based sealers are reshaping product preferences, while regional expansion beyond the core economies offers sizable upside. Competitive intensity will heighten, rewarding firms that combine innovative product development with strategic regional partnerships and robust clinical education programs.

17. How was the research for this market conducted?

The study employed a mix of primary interviews with dental professionals, distributors, and key opinion leaders, alongside secondary data extraction from industry reports, regulatory filings, and company disclosures. Quantitative forecasting utilized CAGR extrapolation from the base‑year market size of USD 84.37 million, aligned with the provided growth rate of 4.58 % to project the 2033 outlook.

18. What is the scope of the research and its limitations?

The scope covers product types, end users, and indications within the Asia Pacific region, focusing on market size, growth drivers, and competitive dynamics up to 2033. Limitations include the absence of granular country‑level revenue breakdowns and the reliance on publicly available data for emerging markets, which may evolve as new regulatory approvals occur.

19. Which key companies have recent developments in the Asia Pacific Endodontic Reparative Cement market?

Coltene Group announced the launch of a next‑generation bioceramic sealer with enhanced radiopacity. Dentsply Maillefer reported a partnership with a leading Indian dental chain to supply its epoxy resin based cement series. IvoclarVivadent AG introduced a fast‑curing calcium‑hydroxide cement designed for single‑visit procedures. Parkell, Inc. unveiled a training academy in Japan focusing on digital workflow integration. Septodont Holding completed an acquisition of a niche Southeast Asian distributor to strengthen its regional foothold.