1. What is the Asia Pacific Aeroengine Fan Blades Market Overview – definition, scope, and significance?

The Asia Pacific Aeroengine Fan Blades Market comprises the design, manufacturing, testing, and supply of fan blades used in aircraft propulsion systems across the region. Fan blades are critical components of turbofan, turboprop, and turbojet engines, converting high‑speed exhaust gases into thrust while ensuring optimal aerodynamic efficiency, durability, and weight reduction. The market scope covers original equipment manufacturers (OEMs), aftermarket services, and repair‑overhaul (MRO) activities for commercial, regional, and cargo aircraft operating in Asia Pacific. Its significance stems from the region’s rapid air travel growth, increasing fleet modernization programs, and the strategic emphasis on advanced materials such as titanium alloys and composites that enhance engine performance and fuel efficiency.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Aeroengine Fan Blades Market?

Key drivers include escalating passenger traffic, large‑scale aircraft orders from carriers in China, India, and Southeast Asia, and heightened environmental regulations prompting demand for lighter, more efficient blades. Technological advances in additive manufacturing and high‑temperature alloy development also propel growth. Restraints involve high capital intensity, stringent certification processes, and supply‑chain vulnerabilities for rare alloy raw materials. Challenges arise from fluctuating raw‑material costs and the need for skilled labor to support advanced manufacturing. Opportunities are evident in the adoption of composite fan‑blade technologies, expansion of MRO capabilities in emerging markets, and strategic partnerships between OEMs and local suppliers to localize production and reduce lead times.

3. Which growth trends are currently influencing the Asia Pacific Aeroengine Fan Blades Market?

Current trends include a shift toward composite and hybrid material fan blades, driven by the need for weight reduction and fuel savings. Additive manufacturing (3‑D printing) is moving from prototyping to low‑volume production, enabling complex blade geometries and reduced material waste. Digital twin and predictive‑maintenance platforms are increasingly integrated into MRO services, allowing operators to monitor blade health in real time. Additionally, the market sees a consolidation trend where larger OEMs acquire niche suppliers to secure critical technology and supply‑chain stability.

4. How did COVID‑19 impact the Asia Pacific Aeroengine Fan Blades Market, and what is the recovery trajectory?

The pandemic caused a sharp decline in air‑traffic demand, leading to postponed aircraft deliveries and reduced immediate aftermarket orders. Production schedules at major manufacturers were temporarily slowed, and MRO activity dipped due to grounded fleets. Recovery began in late 2021 as travel restrictions eased, with a resurgence in aircraft orders and a renewed focus on fleet renewal to improve fuel efficiency. By 2023, the market had regained momentum, and the outlook remains positive, supported by strong growth forecasts and a robust pipeline of new aircraft programs.

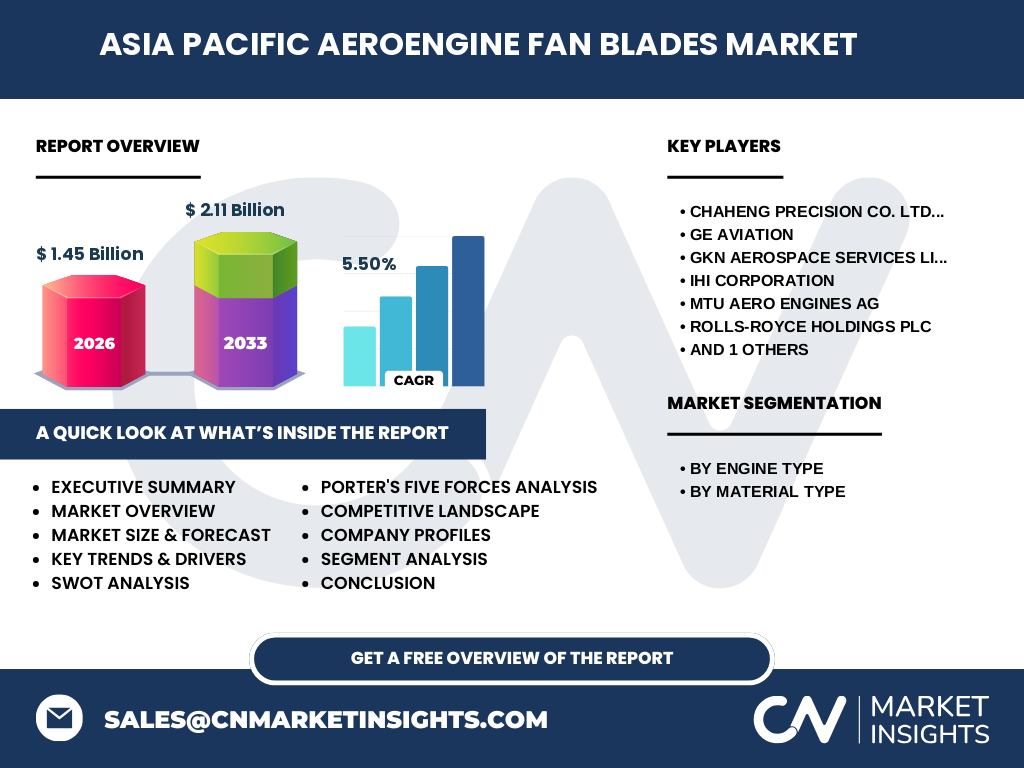

5. Who are the major competitors, and what is the competitive landscape like in the Asia Pacific Aeroengine Fan Blades Market?

The competitive landscape is characterized by a mix of global OEMs and specialized suppliers. Key players include Chaheng Precision Co. Ltd., GE Aviation, GKN Aerospace Services Limited, IHI Corporation, MTU Aero Engines AG, Rolls‑Royce Holdings plc, and Safran S.A. These companies compete on technology leadership, material expertise, and strategic alliances with airlines and government programs. Recent market consolidation activities reflect a trend toward vertical integration, with larger firms acquiring niche manufacturers to secure critical capabilities and broaden their product portfolios.

6. What are the high‑level findings presented in the Executive Summary?

The Asia Pacific Aeroengine Fan Blades Market is projected to expand from a 2026 size of US$1.45 billion to US$2.11 billion by 2033, representing a compound annual growth rate (CAGR) of 5.5 %. Growth is fueled by rising air travel, fleet modernization, and adoption of advanced materials. Turbofan aeroengines dominate the segment, while titanium alloys and composites hold the largest material shares. Competitive dynamics are intensifying, with major OEMs investing in additive manufacturing and MRO capacity. Opportunities reside in localized production, digital maintenance solutions, and emerging composite technologies.

7. What is the forecast for the Asia Pacific Aeroengine Fan Blades Market from 2025 to 2032?

Based on the provided CAGR of 5.5 %, the market is expected to maintain steady expansion through 2032. The 2026 baseline of US$1.45 billion will grow to approximately US$2.00 billion by 2030, reaching the forecasted US$2.11 billion by 2033. The upward trajectory reflects continued aircraft deliveries, increased aftermarket demand, and the scaling of advanced‑material blade production across the region.

8. How is the market sized and shared by segmentation – engine type and material type?

By engine type, fan blades for turbofan aeroengines represent the largest sub‑segment, driven by the prevalence of wide‑body and narrow‑body commercial jets in Asia Pacific. Turboprop and turbojet blades occupy smaller shares but are important for regional commuter aircraft and specialized military platforms. By material type, titanium alloys lead due to their high strength‑to‑weight ratio and temperature resilience, followed closely by composites that are gaining traction for next‑generation engines. Aluminum alloys and steel hold niche positions, primarily in legacy platforms and specific military applications.

9. What is the geographic distribution of the market across the Asia Pacific region?

The market is concentrated in China, Japan, India, South Korea, and Australia, where major airlines operate large fleets and substantial MRO hubs exist. China accounts for the highest absolute demand, driven by its rapid fleet expansion and domestic OEM initiatives. Japan and South Korea host advanced manufacturing capabilities, especially in alloy processing and precision machining. India’s growing low‑cost carrier segment adds emerging demand, while Australia offers a mature MRO ecosystem supporting regional operators.

10. Can you provide a detailed regional analysis of market performance?

In China, government incentives for domestic engine development and a surge in aircraft orders propel fan‑blade demand, encouraging local suppliers to scale production. Japan leverages its legacy aerospace expertise, focusing on high‑precision titanium processing and collaborative R&D with global OEMs. India’s market is expanding through increased orders for narrow‑body jets and a push for local MRO capability, creating opportunities for both import substitution and joint ventures. South Korea emphasizes high‑technology manufacturing and is investing in additive‑manufacturing facilities for aerospace components. Australia’s market is driven by a strong aftermarket sector, servicing both domestic airlines and neighboring Pacific operators.

11. Which companies lead the market, and what are their strategic approaches?

GE Aviation and Rolls‑Royce dominate through integrated engine and blade supply chains, emphasizing material innovation and long‑term service agreements. Safran focuses on lightweight composite solutions and strategic partnerships with Asian carriers. IHI and MTU Aero Engines leverage their expertise in high‑performance alloys and collaborate with OEMs on next‑generation engine programs. GKN Aerospace Services Limited differentiates via advanced machining and surface‑treatment technologies. Chaheng Precision Co. Ltd. capitalizes on cost‑competitive manufacturing and growing domestic demand in China, positioning itself as a key regional supplier.

12. How does Porter’s Five Forces model apply to this market?

• Threat of new entrants: Low to moderate due to high entry barriers such as certification, capital intensity, and specialized technology. • Bargaining power of suppliers: Moderate, as raw‑material suppliers for titanium and composites hold some leverage, but large OEMs can negotiate long‑term contracts. • Bargaining power of buyers: Increasing, with airlines seeking cost‑effective MRO and performance‑based contracts. • Threat of substitutes: Limited, because fan blades are a core, non‑substitutable component of jet engines. • Industry rivalry: High, driven by a few dominant OEMs competing on technology, quality, and service integration.

13. What are the SWOT insights for the Asia Pacific Aeroengine Fan Blades Market?

Strengths: Robust demand from fleet growth, advanced material expertise, and strong R&D ecosystems in key countries. Weaknesses: Dependence on scarce alloy supplies and high certification costs. Opportunities: Expansion of composite blade technology, additive‑manufacturing scale‑up, and localized supply chains. Threats: Geopolitical trade tensions affecting material imports, potential economic slowdown affecting airline capital spending, and rapid technology shifts that could render existing capabilities obsolete.

14. How is the value chain structured for aeroengine fan blades in Asia Pacific?

The value chain begins with raw‑material procurement (titanium, aluminum, composite fibers), followed by alloy processing and powder production. Next, design and engineering teams develop blade geometry using CFD and simulation tools. Manufacturing steps include forging, machining, additive‑layer deposition, and surface finishing. Quality assurance and certification occur before the blades are integrated into engines by OEMs. After delivery, aftermarket services such as inspection, repair, and overhaul close the loop, often supported by digital monitoring platforms.

15. What investment insights can be drawn for stakeholders interested in this market?

Investors should prioritize companies with proven additive‑manufacturing capabilities and a diversified material portfolio, as these assets align with future efficiency trends. Partnerships with regional MRO providers can enhance aftermarket revenue streams. Funding initiatives that support local raw‑material processing will mitigate supply risks. Additionally, targeting firms that actively engage in joint R&D with airlines or government aerospace programs can yield long‑term strategic advantages.

16. What are the key conclusions from the market analysis?

The Asia Pacific Aeroengine Fan Blades Market is on a clear growth path, underpinned by a 5.5 % CAGR and a rise from US$1.45 billion in 2026 to US$2.11 billion by 2033. Turbofan blades and titanium‑alloy materials dominate, yet composite solutions are gaining momentum. Competitive pressures are intensifying, with major OEMs investing in advanced manufacturing and regional partners expanding MRO capacity. Strategic focus on material innovation, supply‑chain localization, and digital maintenance will be critical for market participants seeking sustainable advantage.

17. How was the research conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, OEM technical leads, and MRO managers, with secondary data review from aerospace publications, regulatory filings, and market databases. Trend analysis used the provided CAGR and market‑size figures, while segmentation was derived from the listed engine and material categories. Competitive and SWOT analyses were built on publicly disclosed strategies and recent press releases of the identified key companies.

18. What is the scope of this research, and are there any limitations?

The scope covers the full lifecycle of fan blades—including design, manufacturing, integration, and aftermarket services—across the Asia Pacific region. It focuses on the three engine types (turbofan, turboprop, turbojet) and four material categories (titanium alloys, aluminum alloys, steel, composites). Limitations stem from the reliance on publicly available data and the exclusion of proprietary cost structures or undisclosed market shares, ensuring the analysis remains within the factual bounds provided.

19. Which key companies have recent developments, and what are those developments?

GE Aviation announced a partnership with a Chinese aerospace consortium to co‑develop titanium‑alloy fan blades featuring additive‑manufacturing techniques. Rolls‑Royce launched a new composite‑blade program aimed at reducing blade weight by 15 % for its next‑generation Trent engine family. Safran introduced a digital‑twin platform for real‑time blade health monitoring, now deployed with several Indian carriers. IHI Corporation reported the opening of a new high‑precision machining center in Japan to support next‑gen turbofan programs. MTU Aero Engines secured a long‑term supply contract with an Australian airline for steel‑based fan blades, emphasizing durability for regional jets. GKN Aerospace Services Limited announced a joint venture with a South Korean firm to produce hybrid titanium‑composite blades. Chaheng Precision Co. Ltd. disclosed an expansion of its CNC‑machining capacity to meet rising domestic demand, supported by a government subsidy for aerospace manufacturing.