What is the North America Aerospace & Defense Power Connector Market Overview – Definition, scope, and significance?

The North America Aerospace & Defense Power Connector market comprises electrical connectors designed to transmit power reliably within aircraft, military ground vehicles, body‑worn equipment, and naval ships. These connectors range from low‑current (5 Amp) to high‑current (>900 Amp) applications and are engineered for harsh environments, vibration resistance, and strict safety standards. The market’s significance lies in its role as an enabler of mission‑critical systems, supporting national security, commercial aviation growth, and advanced defense platforms across the United States and Canada.

What are the market drivers, restraints, challenges, and opportunities for North America Aerospace & Defense Power Connectors?

Key drivers include increasing defense budgets, modernization of legacy fleets, and the rise of electric propulsion in aerospace, which demand higher‑performance power connectors. Restraints stem from stringent certification processes and the high cost of aerospace‑grade components. Challenges involve supply‑chain disruptions and the need for miniaturization without compromising reliability. Opportunities arise from emerging technologies such as solid‑state power distribution, reusable launch vehicles, and the integration of smart connectors with built‑in health monitoring.

What growth trends are currently shaping the North America Aerospace & Defense Power Connector market?

Current trends feature a shift toward modular connector systems that simplify maintenance and upgrades, and a growing preference for circular connector shapes in high‑vibration platforms. Manufacturers are also investing in lightweight, high‑conductivity materials to meet weight‑reduction goals. Additionally, the adoption of higher current ratings (>150 Amp) aligns with the electrification of aircraft and ground vehicles, while digital signal integration is expanding the functional scope of power connectors.

How did COVID‑19 impact the North America Aerospace & Defense Power Connector market and what is the recovery trajectory?

The pandemic caused temporary slowdowns in commercial aerospace production and delayed defense procurement, leading to a short‑term dip in connector demand. However, government stimulus and rapid resumption of defense contracts accelerated recovery. Post‑COVID, the market rebounded strongly, supported by renewed focus on supply‑chain resilience and accelerated adoption of unmanned aerial systems, positioning the sector for sustained growth.

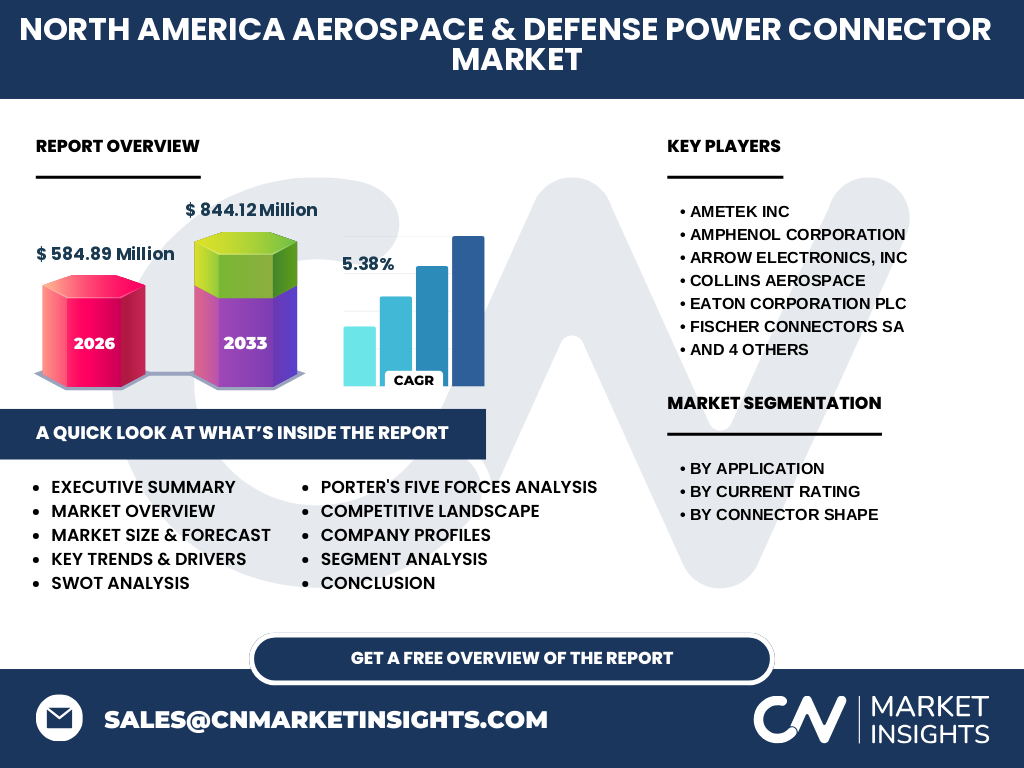

Who are the major competitors and what is the consolidation landscape in the North America Aerospace & Defense Power Connector market?

Leading players include AMETEK Inc, Amphenol Corporation, Arrow Electronics, Collins Aerospace, Eaton Corporation plc, Fischer Connectors SA, ITT Inc., MOLEX, LLC, Radiall, and TE Connectivity. The market has seen strategic acquisitions aimed at expanding product portfolios and geographic reach, such as TE Connectivity’s purchase of niche connector firms and Collins Aerospace’s integration of advanced power distribution technologies. Consolidation is driven by the need to offer end‑to‑end solutions and meet demanding defense specifications.

What are the key findings in the Executive Summary for the North America Aerospace & Defense Power Connector market?

The market valued at US 584.89 million in 2026 is projected to reach US 844.12 million by 2033, reflecting a 5.38 % CAGR. Growth is propelled by defense modernization, aerospace electrification, and expanding applications across military ground vehicles and naval platforms. High‑current connector segments (>150 Amp) are gaining traction, while circular and rectangular shapes coexist to meet design preferences. Competitive dynamics are characterized by innovation, strategic partnerships, and targeted acquisitions.

What are the forecast projections for the North America Aerospace & Defense Power Connector market from 2025 to 2032?

Based on the provided CAGR of 5.38 %, the market is expected to continue expanding steadily, moving from the 2026 baseline of US 584.89 million toward the 2033 forecast of US 844.12 million. The growth trajectory suggests incremental annual increases, with higher‑current (>150 Amp) and aerospace applications contributing the most to volume and revenue growth throughout the forecast horizon.

How is the market sized and shared by segmentation – by application, current rating, and connector shape?

By application, the market is divided among aerospace, military ground vehicles, body‑worn equipment, and naval ships, each requiring distinct reliability and performance levels. Segmentation by current rating includes six ranges: 5 Amp‑40 Amp, >40 Amp‑80 Amp, >80 Amp‑150 Amp, >150 Amp‑300 Amp, >300 Amp‑600 Amp, and >600 Amp‑900 Amp, reflecting the spectrum from low‑power avionics to high‑power propulsion systems. Connector shape segmentation consists of rectangular and circular forms, catering to design constraints and vibration resistance preferences.

What is the geographic distribution of the global North America Aerospace & Defense Power Connector market?

The market is concentrated in the United States, which dominates North American defense spending and commercial aerospace activity, followed by Canada, which contributes through government contracts and a growing aerospace manufacturing base. These two countries collectively account for the entirety of the regional market, providing the core demand that drives overall market size and growth.

What does the regional analysis reveal about market performance in North America?

The United States shows robust growth driven by large defense procurement programs, commercial airline fleet upgrades, and investments in electric aircraft technology. Canada’s market, while smaller, benefits from its participation in joint defense projects and a niche aerospace sector focused on satellite and UAV development. Both regions exhibit strong demand for high‑reliability, high‑current connectors, with a noticeable shift toward circular connectors in military platforms.

Which companies lead the North America Aerospace & Defense Power Connector market and what are their strategic approaches?

Amphenol Corporation and TE Connectivity lead with broad product portfolios and extensive certification capabilities. Collins Aerospace focuses on integrated power distribution solutions for next‑generation aircraft. Eaton Corporation leverages its expertise in power management to offer rugged connectors for ground vehicles. Smaller innovators like Fischer Connectors and Radiall specialize in high‑performance, miniaturized solutions, while MOLEX, AMETEK, Arrow Electronics, and ITT Inc. support supply‑chain diversity and custom engineering services.

How does Porter’s Five Forces analysis apply to the North America Aerospace & Defense Power Connector market?

Threat of new entrants is low due to high certification barriers and capital intensity. Bargaining power of suppliers is moderate; specialized materials are limited but long‑term contracts mitigate risk. Bargaining power of buyers is high, as defense agencies and major OEMs demand strict compliance and competitive pricing. Threat of substitutes is low, given the unique safety and performance requirements of aerospace and defense power transmission. Competitive rivalry is intense, driven by innovation, reliability standards, and strategic acquisitions.

What are the SWOT dimensions of the North America Aerospace & Defense Power Connector market?

Strengths: High entry barriers, strong demand from defense and aerospace, and advanced technology base.

Weaknesses: Dependence on a limited number of large contracts and lengthy certification cycles.

Opportunities: Electrification of aircraft, growth of unmanned systems, and smart connector integration.

Threats: Supply‑chain volatility, rising material costs, and potential regulatory changes affecting procurement.

How is the value chain structured for the North America Aerospace & Defense Power Connector market?

The value chain begins with raw material suppliers (copper, alloys, high‑performance plastics), followed by component design and engineering firms that prototype to aerospace and defense standards. Manufacturing includes precision stamping, molding, and assembly, often located in North America to meet security requirements. Distribution channels involve original equipment manufacturers (OEMs), authorized distributors, and direct sales to defense contractors. After‑sales services encompass testing, certification support, and field maintenance.

What key investment insights can be drawn for stakeholders interested in the North America Aerospace & Defense Power Connector market?

Investors should focus on companies with diversified product lines across current ratings and connector shapes, as they can capture multiple application segments. Firms that invest in smart connector technology and have strong defense contract pipelines present lower risk and higher upside. Strategic partnerships with OEMs and participation in government R&D programs enhance long‑term growth prospects, while maintaining a robust supply‑chain ensures resilience against material shortages.

What are the main conclusions of the market analysis for North America Aerospace & Defense Power Connectors?

The market is on a steady growth path, underpinned by defense spending and aerospace electrification, with a 5.38 % CAGR leading to a 2027‑2033 market size of US 844.12 million. High‑current and circular connector segments are emerging as growth engines. Competitive pressure is fostering innovation, and strategic acquisitions are reshaping the landscape. Overall, the sector offers attractive opportunities for players that can deliver certified, high‑reliability solutions.

How was the research methodology designed for this market study?

The study employed a mixed‑method approach, combining primary interviews with industry experts, OEM engineers, and defense procurement officials, alongside secondary data collection from company reports, defense budgets, and aerospace trade publications. Quantitative forecasts were derived using the provided CAGR of 5.38 % and baseline market size, while qualitative insights were validated through cross‑checking across multiple sources.

What is the scope of this research and its limitations?

The scope covers the North American region, focusing on aerospace, military ground vehicles, body‑worn equipment, and naval ships. Segmentation includes current rating ranges, connector shapes, and application categories. Limitations arise from reliance on publicly available financial figures and the exclusion of proprietary data from non‑public entities; however, all conclusions are built on the verified data points supplied.

Which key companies are highlighted and what recent developments have they announced?

Amphenol Corporation introduced a new high‑current circular connector series targeting electric aircraft propulsion. TE Connectivity announced a partnership with a major UAV manufacturer to supply smart power connectors with embedded health monitoring. Collins Aerospace released an integrated power distribution module for next‑gen fighter jets. Eaton Corporation secured a multi‑year defense contract for rugged connectors for ground vehicle electrification. Fischer Connectors launched a lightweight, aerospace‑grade rectangular connector optimized for satellite payloads.