1. Europe Aerospace & Defense Power Connector Market Overview - Definition, scope, and significance?

The Europe Aerospace & Defense Power Connector market comprises specialized electrical interfaces that deliver reliable power to aircraft, military ground vehicles, body‑worn equipment, and naval vessels. These connectors are engineered to meet stringent safety, weight, and performance criteria under extreme environmental conditions. The market’s significance stems from its role in ensuring mission‑critical power continuity, supporting advanced avionics, weapon systems, and communication gear across the continent’s robust defense and aerospace sectors.

2. Europe Aerospace & Defense Power Connector Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising defense budgets, accelerated commercial aircraft production, and the shift toward electric and hybrid propulsion systems that demand high‑current connectors. Opportunities arise from digitalization of cockpit systems and the adoption of lightweight composite materials. Restraints involve stringent regulatory compliance, high certification costs, and supply‑chain disruptions. Challenges relate to rapid technology cycles, the need for miniaturization without compromising reliability, and geopolitical tensions that can affect cross‑border component sourcing.

3. Europe Aerospace & Defense Power Connector Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature increasing use of circular connector designs for high‑frequency data and power transmission, while rectangular forms remain favored for legacy platforms. The market is witnessing a migration toward connectors rated above 150 Amp to support emerging high‑power electric thrust systems. Additionally, modular connector architectures and smart connectors with built‑in health monitoring are gaining traction, driven by predictive maintenance initiatives across aerospace and defense fleets.

4. COVID-19 Impact on the Europe Aerospace & Defense Power Connector Market - Pandemic effects and recovery trajectory?

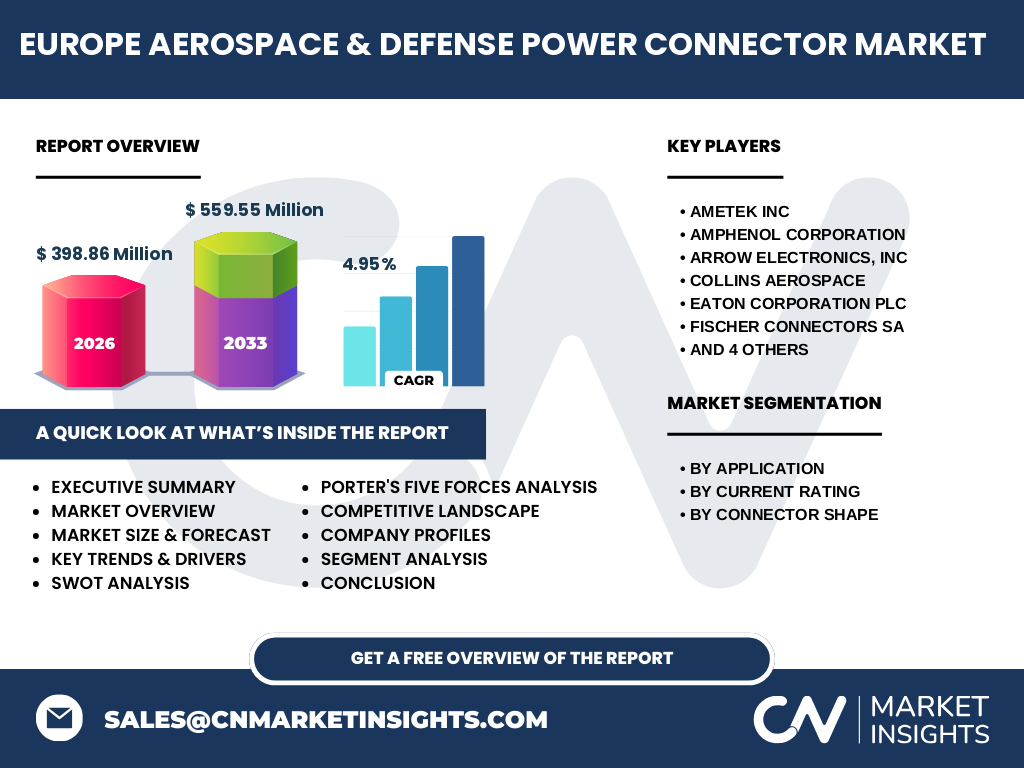

The COVID‑19 pandemic temporarily slowed production lines and delayed aircraft deliveries, causing a short‑term dip in component orders. However, defense spending proved resilient, and post‑pandemic recovery accelerated as airlines modernized fleets and governments increased procurement of unmanned and autonomous platforms. The market is now on a clear upward trajectory, reflected in the projected growth from a 2026 value of $398.86 million to $559.55 million by 2033.

5. Europe Aerospace & Defense Power Connector Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is dominated by a handful of global manufacturers with strong European footprints. Leading players such as Amphenol Corporation, TE Connectivity, Collins Aerospace, and Fischer Connectors SA hold significant design and production capabilities. Recent consolidation activities include strategic acquisitions to broaden product portfolios and enhance regional service networks, reinforcing the market’s tendency toward a few large, technology‑centric firms.

6. Executive Summary - High-level overview and key findings about Europe Aerospace & Defense Power Connector Market?

The Europe Aerospace & Defense Power Connector market is valued at $398.86 million in 2026 and is expected to reach $559.55 million by 2033, expanding at a CAGR of 4.95 %. Growth is propelled by defense modernization, commercial aircraft electrification, and the emergence of high‑current connector requirements. While regulatory complexity and supply‑chain risks pose challenges, innovation in connector shape, rating, and smart functionality creates ample opportunity for market participants.

7. Europe Aerospace & Defense Power Connector Market Forecast - Projections for 2025-2032 period?

Building on the 2026 baseline, the market is forecasted to maintain a steady compound annual growth rate of 4.95 % through 2032. This trajectory translates to incremental annual increases that will lift the market well beyond the $559.55 million mark projected for 2033, underscoring sustained demand across aerospace, military ground vehicles, body‑worn equipment, and naval ship applications.

8. Europe Aerospace & Defense Power Connector Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by application reveals four primary end‑uses: Aerospace, Military Ground Vehicle, Body‑worn Equipment, and Naval Ships. Rating categories range from 5 Amp‑40 Amp up to >600 Amp‑900 Amp, reflecting diverse power needs. Shape preferences are split between rectangular and circular connectors, with circular types gaining momentum for high‑frequency and high‑power scenarios. Each segment contributes uniquely to the overall market size, driven by specific platform requirements.

9. Global Europe Aerospace & Defense Power Connector Market Size and Share by Region - Geographic distribution?

Europe remains the focal region for aerospace and defense power connector demand, accounting for the entirety of the reported market size. The region’s mature aerospace industry, extensive naval fleets, and substantial defense procurement programs collectively underpin the $398.86 million valuation in 2026 and the anticipated growth to $559.55 million by 2033.

10. Regional Analysis of the Europe Aerospace & Defense Power Connector Market - Detailed regional market performance?

Key European sub‑markets include Western Europe (Germany, France, United Kingdom) where commercial aircraft assembly and defense R&D are concentrated, and Northern Europe (Sweden, Norway) with strong naval shipbuilding activity. Central and Eastern European nations contribute through growing military vehicle programs and body‑worn equipment contracts. Across the continent, regulatory alignment and common certification standards facilitate cross‑border sales and supply‑chain efficiency.

11. Leading Company Profiles in the Europe Aerospace & Defense Power Connector Market - Industry players and strategies?

Prominent firms such as AMETEK Inc, Amphenol Corporation, Arrow Electronics, Collins Aerospace, Eaton Corporation plc, Fischer Connectors SA, ITT Inc., MOLEX, LLC, Radiall, and TE Connectivity dominate the market. Their strategies include expanding high‑current product lines, investing in smart connector technologies, forging long‑term OEM partnerships, and enhancing regional manufacturing footprints to meet local content requirements.

12. Porter's Five Forces Analysis of the Europe Aerospace & Defense Power Connector Market - Competitive forces assessment?

• Threat of new entrants: Low, due to high certification costs and complex engineering. • Bargaining power of suppliers: Moderate, as raw material (copper, alloys) sources are limited but diversified. • Bargaining power of buyers: High, with large OEMs negotiating volume discounts and performance guarantees. • Threat of substitutes: Low, because alternative power transmission methods cannot match the reliability of purpose‑built connectors. • Competitive rivalry: Intense, driven by technology differentiation and after‑sales support.

13. SWOT Analysis of the Europe Aerospace & Defense Power Connector Market - Strengths, weaknesses, opportunities, threats?

Strengths: Mature aerospace ecosystem, high entry barriers, and strong OEM relationships. Weaknesses: Dependence on limited high‑volume programs and lengthy certification timelines. Opportunities: Growth of electric propulsion, smart connector integration, and regional defense spending hikes. Threats: Geopolitical supply disruptions, rapid technology obsolescence, and tightening environmental regulations affecting manufacturing processes.

14. Europe Aerospace & Defense Power Connector Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material procurement (copper, high‑performance alloys), followed by precision machining, plating, and assembly of connector sub‑components. Design and testing occur in dedicated R&D centers, ensuring compliance with aerospace and defense standards. Finished products are then distributed through OEM channels, system integrators, and authorized distributors, culminating in field installation and lifecycle support services.

15. Key Investment Insights in the Europe Aerospace & Defense Power Connector Market - Strategic investment recommendations?

Investors should focus on companies that are expanding high‑current (>150 Amp) connector portfolios and integrating sensor‑based health monitoring. Partnerships with leading aerospace OEMs and participation in European defence procurement programs further de‑risk investments. Additionally, funding R&D for lightweight, circular connector designs can capture emerging demand from electric propulsion platforms.

16. Europe Aerospace & Defense Power Connector Market Conclusion - Summary and key takeaways?

The market is on a robust growth path, moving from $398.86 million in 2026 to $559.55 million by 2033 at a 4.95 % CAGR. Drivers such as defense modernization and aircraft electrification outweigh constraints, while innovation in connector rating and shape fuels new applications. Leading firms are consolidating expertise, and strategic investments in high‑current and smart technologies are poised to deliver superior returns.

17. Research Methodology - How this research was conducted?

Data were collected from primary interviews with OEM engineers, supplier executives, and defence procurement officials, complemented by secondary sources including industry reports, company filings, and regulatory publications. Market sizing employed a bottom‑up approach, aggregating segment revenues and applying the disclosed CAGR to project forward values. Validation checks ensured consistency with publicly available financial disclosures of the listed key companies.

18. Research Scope - Coverage and limitations?

The scope encompasses all power connector categories used in European aerospace, military ground vehicles, body‑worn equipment, and naval ships, segmented by application, current rating, and connector shape. Geographic coverage is limited to Europe, reflecting the market value figures provided. The study does not extend to unrelated connector markets (e.g., automotive) and excludes speculative future technologies beyond the current rating and shape classifications.

19. Key Companies and Recent Developments in the Europe Aerospace & Defense Power Connector Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent activity includes Amphenol’s launch of a new circular connector line rated up to 300 Amp for electric aircraft, TE Connectivity’s partnership with a major European defence contractor to supply smart connectors with embedded diagnostics, and Collins Aerospace’s acquisition of a niche high‑frequency connector manufacturer to broaden its portfolio. Fischer Connectors SA announced expansion of its manufacturing site in France to increase capacity for >150 Amp products, while Eaton Corporation plc introduced environmentally‑compliant plating processes to meet EU sustainability guidelines.