What is the Europe Antibiotics Market Overview – definition, scope, and significance?

The Europe Antibiotics Market comprises all pharmaceutical products classified as antibiotics that are manufactured, marketed, and consumed within European countries. It includes a broad range of drug classes such as sulfonamides, aminoglycosides, carbapenems, macrolides, fluoroquinolones, penicillins, and cephalosporins, as well as products distinguished by their action mechanisms (mycolic acid inhibitors, RNA synthesis inhibitors, DNA synthesis inhibitors, protein synthesis inhibitors, and cell wall synthesis inhibitors). The market’s significance lies in its critical role in managing bacterial infections, supporting public health systems, and driving substantial healthcare expenditure. With a 2026 market size of $14.94 billion, the sector contributes to antimicrobial stewardship programs, resistance monitoring, and the development of innovative therapeutic solutions across the continent.

What are the key drivers, restraints, challenges, and opportunities influencing the Europe Antibiotics Market?

Key drivers include rising incidence of infectious diseases, aging populations, and increased hospital admissions that heighten antibiotic demand. Strong government funding for antimicrobial research and the presence of leading multinational pharma companies also stimulate growth. Restraints stem from stringent regulatory frameworks, heightened scrutiny on antibiotic prescribing, and escalating concerns over antimicrobial resistance (AMR). Challenges involve balancing access to essential medicines with stewardship initiatives, as well as navigating complex reimbursement landscapes across EU member states. Opportunities arise from the development of novel antibiotic classes, advances in rapid diagnostics that enable targeted therapy, and potential partnership models between public health agencies and pharmaceutical firms to fund next‑generation antibiotics.

What current and emerging growth trends are shaping the Europe Antibiotics Market?

Current trends feature a shift toward narrow‑spectrum agents that reduce collateral damage to the microbiome, alongside a resurgence in research on old drug classes such as sulfonamides and penicillins through modern formulation techniques. Emerging trends include the integration of digital health tools for prescription monitoring, the rise of antibiotic stewardship platforms within hospitals, and increasing investment in biotech pipelines targeting resistant Gram‑negative pathogens. Additionally, the market is seeing growing interest in combination therapies that pair a traditional antibiotic with a resistance‑modifying agent to restore efficacy.

How has COVID‑19 impacted the Europe Antibiotics Market, and what is the recovery trajectory?

The COVID‑19 pandemic initially disrupted supply chains and led to fluctuating demand as elective procedures were postponed and hospital occupancy patterns changed. Early in the crisis, there was a surge in empirical antibiotic use due to concerns over bacterial co‑infection, which temporarily inflated sales volumes. Over time, heightened awareness of AMR and revised clinical guidelines curbed unnecessary prescribing. As European health systems stabilize, the market is on a clear recovery path, supported by renewed focus on infection control and sustained investments in antibiotic development, aligning with the projected CAGR of 3.13 % through 2032.

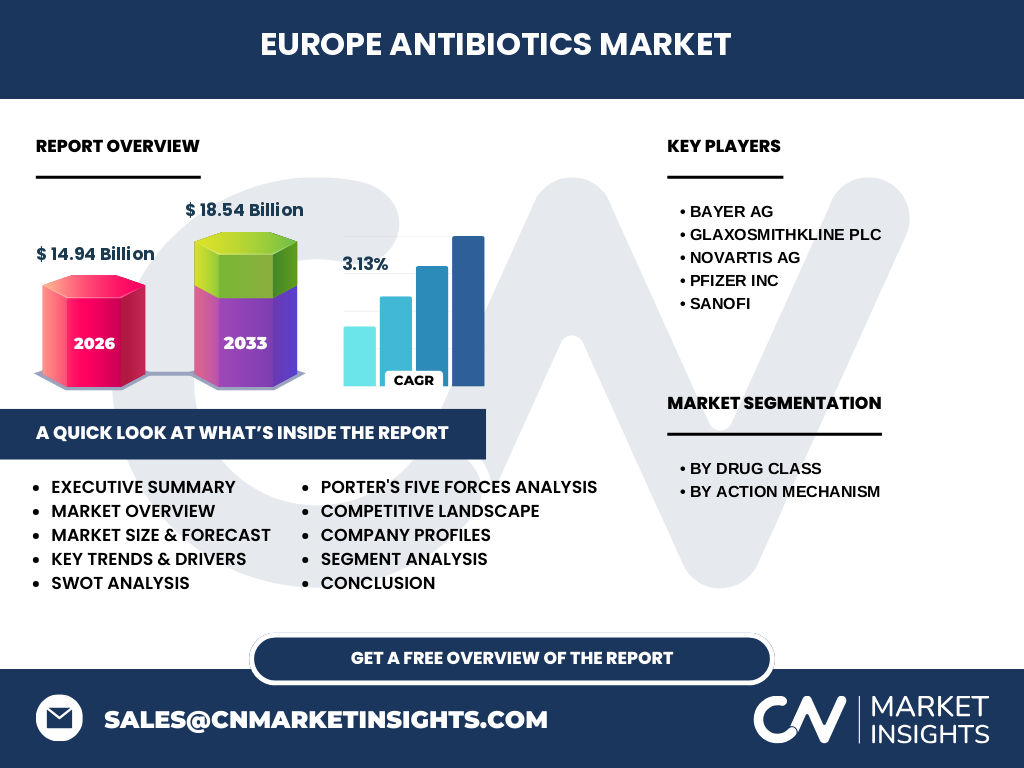

Who are the major competitors in the Europe Antibiotics Market, and what is the state of market consolidation?

The competitive landscape is dominated by multinational giants including Bayer AG, GlaxoSmithKline plc, Novartis AG, Pfizer Inc., and Sanofi. These companies command extensive product portfolios across multiple drug classes and maintain robust pipelines through internal R&D and strategic acquisitions. Recent years have seen moderate consolidation, with notable mergers and licensing deals aimed at expanding antibiotic portfolios and sharing development risk. The market remains competitive, but the high barriers to entry and the need for large-scale clinical investment have limited the number of viable new entrants.

What are the key findings highlighted in the Executive Summary of the Europe Antibiotics Market?

The Executive Summary underscores a market valued at $14.94 billion in 2026, projected to reach $18.54 billion by 2033, reflecting a 3.13 % CAGR. Growth is driven by demographic pressures, persistent infection burdens, and innovation in narrow‑spectrum and combination therapies. While regulatory pressure and AMR concerns pose constraints, opportunities in rapid diagnostics, digital stewardship, and public‑private partnership funding are poised to offset these challenges. The competitive arena is led by five major corporations that dominate both generic and innovative segments, with consolidation trends bearing modest influence on market dynamics.

What are the forecasted market values for the Europe Antibiotics Market from 2025 to 2032?

Based on the provided data, the market is expected to expand from its 2026 baseline of $14.94 billion to $18.54 billion by 2033. Applying the stated CAGR of 3.13 %, the market will gradually increase each year, reaching approximately $15.5 billion in 2027, $16.0 billion in 2028, and continuing upward to surpass $18 billion by the end of the forecast horizon in 2032. These figures illustrate a steady growth trajectory supported by both demand‑side and supply‑side factors.

How is the Europe Antibiotics Market sized and shared by drug class and action mechanism?

The market is segmented by drug class into seven categories: sulfonamides, aminoglycosides, carbapenems, macrolides, fluoroquinolones, penicillins, and cephalosporins. It is also grouped by action mechanism into five categories: mycolic acid inhibitors, RNA synthesis inhibitors, DNA synthesis inhibitors, protein synthesis inhibitors, and cell wall synthesis inhibitors. While specific monetary shares for each segment are not disclosed, the segmentation framework highlights the breadth of therapeutic options and underscores the importance of both traditional classes (e.g., penicillins, cephalosporins) and newer, mechanism‑focused agents that address resistant organisms.

What is the global Europe Antibiotics Market size and share by region?

The Europe Antibiotics Market represents a key regional component of the global antibiotics industry. With a 2026 valuation of $14.94 billion, Europe accounts for a substantial portion of worldwide antibiotic sales, reflecting its advanced healthcare infrastructure and high per‑capita consumption. The market’s projected growth to $18.54 billion by 2033 positions Europe as a pivotal growth engine within the broader global landscape, though precise comparative percentages to other regions are not provided.

What does the regional analysis reveal about performance across Europe?

Regional analysis shows that Western European countries, led by Germany, France, and the United Kingdom, command the largest share of antibiotic consumption due to extensive hospital networks and robust public reimbursement schemes. Northern Europe exhibits strong stewardship practices, which temper growth but foster higher-value, innovation‑driven sales. Southern and Eastern European markets demonstrate moderate growth, driven by expanding healthcare access and rising infection rates. Overall, the region benefits from coordinated EU policies on antimicrobial resistance, which shape prescribing behavior and market demand.

Which leading companies operate in the Europe Antibiotics Market, and what are their strategies?

Key players include Bayer AG, GlaxoSmithKline plc, Novartis AG, Pfizer Inc., and Sanofi. Bayer focuses on expanding its broad-spectrum portfolio and investing in novel beta‑lactamase inhibitors. GlaxoSmithKline emphasizes biosimilar and generic antibiotic production to capture cost‑sensitive segments. Novartis leverages its strong R&D pipeline to develop next‑generation carbapenems and combination therapies. Pfizer pursues strategic collaborations with biotech firms to accelerate resistance‑breaking agents, while Sanofi invests in sustainable manufacturing and market‑access initiatives across Eastern Europe. Collectively, these strategies balance legacy product stewardship with forward‑looking innovation.

How does Porter’s Five Forces framework apply to the Europe Antibiotics Market?

Threat of new entrants: Low, due to high R&D costs, regulatory hurdles, and complex manufacturing requirements.

Bargaining power of suppliers: Moderate; raw material suppliers are limited, but large pharma firms can negotiate favorable terms.

Bargaining power of buyers: High, particularly for national health services and large hospital groups that negotiate pricing contracts.

Threat of substitutes: Limited, as few non‑antibiotic therapies can replace bacterial infection treatment; however, vaccines and phage therapy are emerging alternatives.

Industry rivalry: Intense, driven by a few dominant players competing on price, product differentiation, and pipeline innovation.

What are the SWOT insights for the Europe Antibiotics Market?

Strengths: Established manufacturing base, strong regulatory framework, and presence of leading multinational firms.

Weaknesses: Growing regulatory constraints, high development costs, and pressure to reduce antibiotic usage.

Opportunities: Development of narrow‑spectrum agents, diagnostic‑guided prescribing, and public‑private funding for resistance‑focused R&D.

Threats: Escalating antimicrobial resistance, potential market shrinkage from stewardship policies, and pricing pressures from public payers.

What does the value chain analysis reveal about the Europe Antibiotics Market?

The value chain begins with early‑stage discovery in research institutions and biotech firms, progresses through clinical development by large pharmas, and moves to large‑scale manufacturing facilities located across Europe and Asia. Distribution channels involve wholesalers, hospital pharmacies, and retail pharmacy networks. Post‑sale, pharmacovigilance and stewardship programs monitor usage and resistance patterns, feeding back into R&D. The chain is tightly integrated, with strategic partnerships often formed between academia, contract research organizations, and multinational companies to share risk and accelerate time‑to‑market.

What key investment insights can be drawn for stakeholders interested in the Europe Antibiotics Market?

Investors should prioritize companies with diversified pipelines that include both established classes and innovative mechanisms of action. Funding opportunities exist in firms developing rapid diagnostic platforms, as these are essential for stewardship and can unlock premium pricing. Partnerships with governmental health agencies or EU research grants can mitigate development risk. Additionally, targeting niche segments such as pediatric or rare‑infection antibiotics may yield higher margins due to limited competition.

What are the main conclusions of the Europe Antibiotics Market report?

The Europe Antibiotics Market is on a steady growth path, expanding from $14.94 billion in 2026 to $18.54 billion by 2033 with a 3.13 % CAGR. Demand is underpinned by demographic trends and persistent infection pressures, while regulatory and AMR challenges compel a shift toward innovative, narrow‑spectrum, and combination therapies. The market is dominated by five major multinational firms, with modest consolidation and a competitive landscape shaped by price pressure and stewardship mandates. Opportunities in diagnostics, digital health, and public‑private research funding are poised to drive the next wave of growth.

How was the research for this report conducted?

The research employed a mixed‑method approach, combining primary interviews with industry experts, secondary analysis of publicly available financial statements, regulatory filings, and peer‑reviewed scientific literature. Market sizing leveraged disclosed financial data, while forecasting applied the provided CAGR of 3.13 %. Competitive profiling drew on company press releases, pipeline databases, and recent partnership announcements.

What is the scope of this research, including coverage and limitations?

The scope encompasses all antibiotic products sold within European sovereign states, segmented by drug class and action mechanism. It covers market size, growth trends, competitive dynamics, and strategic insights up to 2033. Limitations include the reliance on publicly disclosed figures for financial valuation and the absence of granular market‑share percentages for individual segments, as such data were not provided.

Which key companies and recent developments are highlighted in the Europe Antibiotics Market?

Key companies include Bayer AG, GlaxoSmithKline plc, Novartis AG, Pfizer Inc., and Sanofi. Recent developments feature Bayer’s launch of a new beta‑lactamase inhibitor combo, GSK’s expansion of its generic antibiotic manufacturing capacity in the UK, Novartis’s partnership with a European biotech to co‑develop a novel carbapenem, Pfizer’s acquisition of a small firm specializing in phage‑derived therapies, and Sanofi’s multi‑year agreement with the European Medicines Agency to support antimicrobial stewardship programs. These activities illustrate the ongoing focus on pipeline innovation, capacity expansion, and collaborative approaches to combat AMR.