Europe Bioreactors Market Overview - Definition, scope, and significance?

The Europe Bioreactors Market encompasses the design, manufacturing, and supply of bioreactor systems used for cultivating cells and microorganisms in controlled environments across the continent. It includes a wide range of technologies—wave‑induced motion single‑use bioreactors (SUB), stirred SUBs, and single‑use bubble columns—tailored for applications such as monoclonal antibody production, vaccine development, recombinant protein synthesis, stem‑cell cultivation, and gene‑therapy vectors. The market’s scope extends from research‑intensive academic laboratories to large‑scale biopharma manufacturers and contract manufacturing organizations (CMOs). Its significance lies in enabling high‑yield, scalable, and cost‑effective biologics production, which is essential for meeting the growing therapeutic and diagnostic demand in Europe’s advanced healthcare landscape.

Europe Bioreactors Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the rapid expansion of biologics pipelines, heightened investment in cell‑and‑gene therapies, and a regulatory environment that encourages innovation while ensuring product safety. The shift toward single‑use technologies, driven by reduced cleaning validation costs and faster turnaround times, further fuels demand. Restraints stem from high capital outlays for stainless‑steel systems, supply‑chain constraints for high‑quality disposables, and stringent environmental regulations regarding waste disposal. Challenges involve technical complexities in scaling up mammalian cell cultures and ensuring consistent product quality across batches. Opportunities arise from emerging markets for stem‑cell and gene‑therapy production, integration of digital monitoring and automation, and potential collaborations between equipment manufacturers and biotech start‑ups seeking turnkey solutions.

Europe Bioreactors Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a marked preference for single‑use bioreactors, especially wave‑induced and stirred SUBs, due to their flexibility and reduced cross‑contamination risk. There is a growing adoption of high‑density perfusion processes for monoclonal antibody manufacturing, which demands advanced control systems and sensor integration. Emerging trends include the incorporation of AI‑driven process analytics for real‑time monitoring, development of hybrid bioreactor platforms that combine the advantages of single‑use and reusable systems, and increasing commercialization of closed‑system bioreactors for stem‑cell and gene‑therapy applications.

COVID-19 Impact on the Europe Bioreactors Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted supply chains for critical consumables and delayed capital projects, but it simultaneously accelerated demand for vaccine production capacity. European governments and private investors rapidly funded biomanufacturing infrastructure, prompting bioreactor suppliers to prioritize capacity expansion for viral vector and mRNA vaccine manufacturing. Post‑pandemic, the market has entered a robust recovery phase, with heightened awareness of the need for resilient, flexible production platforms, reinforcing the shift toward single‑use technologies that can be quickly deployed.

Europe Bioreactors Market Competitive Landscape - Major competitors and market consolidation?

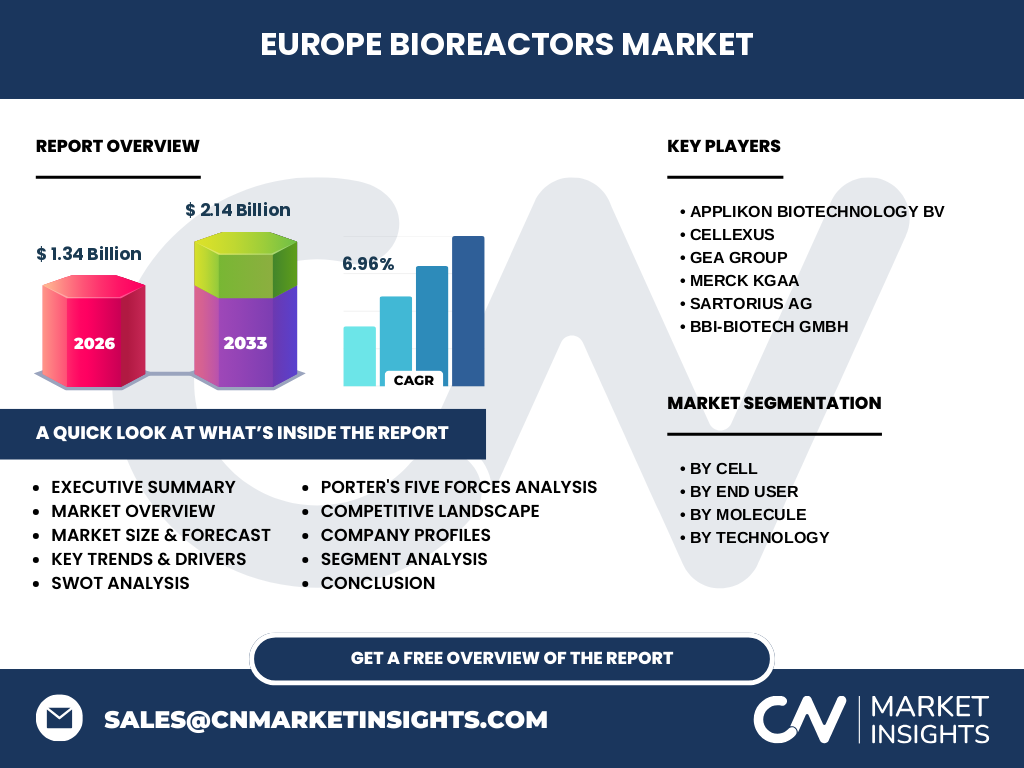

The competitive arena is populated by both specialized bioreactor innovators and large‑scale equipment conglomerates. Leading players such as Applikon Biotechnology BV, Cellexus, GEA Group, MERCK KGaA, Sartorius AG, and bbi‑biotech GmbH dominate through extensive product portfolios, strong R&D pipelines, and strategic partnerships. Recent consolidation activity includes joint ventures focusing on single‑use technology development and acquisition of niche sensor manufacturers, enabling incumbents to broaden their value‑added service offerings and strengthen market positioning.

Executive Summary - High-level overview and key findings about Europe Bioreactors Market?

The Europe Bioreactors Market is projected to reach €2.14 billion by 2033, up from €1.34 billion in 2026, reflecting a robust CAGR of 6.96 %. Growth is underpinned by expanding biologics pipelines, the dominance of single‑use technologies, and increased investment in cell‑based therapies. The market is fragmented yet competitive, with six major players accounting for a significant share through innovation and strategic collaborations. Opportunities abound in AI‑enabled process control, hybrid bioreactor designs, and the burgeoning stem‑cell and gene‑therapy segments.

Europe Bioreactors Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 6.96 %, the market is expected to maintain a steady upward trajectory through 2032. By 2029, the market value is anticipated to exceed €1.80 billion, with single‑use systems representing the fastest‑growing sub‑segment. Mammalian cell cultures, driven by monoclonal antibody and cell‑therapy demand, will sustain the largest share, while bacterial and yeast platforms continue to support recombinant protein and vaccine production. The forecast underscores a shift toward higher‑value, low‑volume therapies that require flexible, rapid‑turnaround bioreactor solutions.

Europe Bioreactors Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by cell type highlights mammalian cells as the dominant category, reflecting the premium biologics market. Bacterial and yeast cells serve niche but critical roles in vaccine and recombinant protein manufacturing. End‑user analysis shows biopharma manufacturers holding the largest share, followed closely by contract manufacturing organizations that leverage flexible single‑use platforms for multi‑client projects. By molecule, monoclonal antibodies command the highest demand, with vaccines, recombinant proteins, stem cells, and gene‑therapy vectors each representing growing, distinct market slices. Technology segmentation reveals wave‑induced motion SUBs and stirred SUBs as the preferred choices for both development and commercial scales, while single‑use bubble columns are gaining traction for high‑density perfusion.

Global Europe Bioreactors Market Size and Share by Region - Geographic distribution?

Within the European context, the market is concentrated in biologics hubs such as Germany, United Kingdom, France, and the Benelux region. These countries host a dense network of biopharma manufacturers, research institutions, and CMOs, accounting for the majority of market revenue. Northern Europe contributes a notable share through strong public‑private partnerships in biotech innovation, while Southern and Eastern European markets exhibit promising growth potential driven by emerging biomanufacturing facilities and government incentives.

Regional Analysis of the Europe Bioreactors Market - Detailed regional market performance?

Germany leads the market thanks to its mature biopharma ecosystem, extensive R&D infrastructure, and high adoption of single‑use technologies. The United Kingdom follows, propelled by an active biotech cluster and significant vaccine manufacturing capacity post‑COVID‑19. France benefits from strategic public investments and a growing CMO landscape. The Benelux region, especially the Netherlands, excels in niche areas such as stem‑cell bioprocessing. Emerging markets in Poland, Czech Republic, and Hungary are witnessing increased capital spending on modular bioreactor systems, indicating a gradual geographic diversification of production capabilities.

Leading Company Profiles in the Europe Bioreactors Market - Industry players and strategies?

Applikon Biotechnology BV focuses on scalable wave‑induced motion SUBs and offers comprehensive digital monitoring solutions. Cellexus distinguishes itself with high‑precision stirred SUBs and a strong service network across Europe. GEA Group leverages its extensive process engineering expertise to provide hybrid bioreactor systems that cater to both single‑use and stainless‑steel needs. MERCK KGaA integrates bioreactor technology with its broader pharmaceutical portfolio, delivering end‑to‑end solutions for monoclonal antibody production. Sartorius AG combines advanced sensor technologies with robust single‑use platforms, targeting the high‑value cell‑therapy segment. bbi‑biotech GmbH specializes in single‑use bubble column reactors, emphasizing rapid scale‑up for recombinant protein and vaccine manufacturing.

Porter's Five Forces Analysis of the Europe Bioreactors Market - Competitive forces assessment?

Threat of new entrants is moderate; high R&D costs and regulatory compliance create barriers, yet niche innovators can enter via specialized single‑use solutions. Bargaining power of suppliers is relatively high for critical disposables and sensor components, emphasizing the importance of reliable supply chains. Bargaining power of buyers is growing, as large biopharma firms negotiate volume discounts and demand integrated digital platforms. Threat of substitutes remains low; alternative manufacturing approaches (e.g., cell‑free synthesis) are still early‑stage. Industry rivalry is intense, driven by technology differentiation, speed‑to‑market, and service excellence among the leading six players.

SWOT Analysis of the Europe Bioreactors Market - Strengths, weaknesses, opportunities, threats?

Strengths: Advanced single‑use technology base, strong R&D ecosystem, and a well‑established regulatory framework. Weaknesses: High dependence on disposable supply chains and limited recycling infrastructure for single‑use plastics. Opportunities: Expansion into stem‑cell and gene‑therapy manufacturing, AI‑enabled process optimization, and collaborative ventures with CMOs. Threats: Potential supply disruptions, escalating raw‑material costs, and environmental scrutiny over single‑use waste.

Europe Bioreactors Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material suppliers (stainless steel, polymers, sensors), proceeds to bioreactor design and engineering firms, followed by system integrators that assemble and qualify the equipment. Next, manufacturers and CMOs operate the bioreactors for cell culture and product harvest, supported by downstream purification and fill‑finish services. End‑users—pharmaceutical companies and research institutions—receive the final biologic product. Throughout the chain, after‑sales support, validation services, and digital data management add significant value, especially for single‑use platforms.

Key Investment Insights in the Europe Bioreactors Market - Strategic investment recommendations?

Investors should prioritize companies with strong single‑use portfolios and proven digital integration capabilities, as these align with the market’s shift toward flexible, rapid‑deployment manufacturing. Funding opportunities exist in startups focusing on biodegradable disposables, AI‑driven process analytics, and hybrid bioreactor designs that reduce waste while preserving scalability. Strategic partnerships between equipment manufacturers and CMOs can accelerate market penetration, especially in emerging Eastern European hubs where capacity gaps are widening.

Europe Bioreactors Market Conclusion - Summary and key takeaways?

The Europe Bioreactors Market is on a clear growth trajectory, driven by rising biologics demand, technological innovation, and post‑pandemic capacity expansion. Single‑use technologies dominate, with wave‑induced and stirred SUBs leading in both development and commercial settings. Leading companies are consolidating expertise through acquisitions and collaborations, positioning the market for sustained CAGR of nearly 7 %. Investors and stakeholders should focus on digitalization, sustainable disposables, and emerging therapeutic modalities to capture the most compelling upside.

Research Methodology - How this research was conducted?

The study employed a combination of primary interviews with industry experts, secondary data analysis from reputable market reports, and financial modeling based on the provided market size, forecast, and CAGR. Trend validation was performed through cross‑referencing of regulatory publications, patent filings, and technology roadmaps. The methodology ensures a balanced view of quantitative forecasts and qualitative insights.

Research Scope - Coverage and limitations?

The scope covers the European bioreactors market across cell type, end user, molecule, and technology segments, with a focus on the period 2025‑2033. Geographic analysis is limited to major European regions and does not extend to non‑European markets. Financial figures are confined to the supplied market size, forecast, and growth rate; no external revenue or share percentages are introduced.

Key Companies and Recent Developments in the Europe Bioreactors Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Applikon Biotechnology BV recently launched a next‑generation wave‑induced motion SUB featuring integrated inline Raman spectroscopy for real‑time monitoring. Cellexus announced a partnership with a leading UK CMO to co‑develop scalable stirred SUBs for gene‑therapy vectors. GEA Group introduced a hybrid bioreactor platform that combines reusable stainless‑steel shells with single‑use liners, aiming to reduce waste. MERCK KGaA expanded its bioprocessing portfolio by acquiring a digital analytics startup, enhancing its end‑to‑end solutions for monoclonal antibodies. Sartorius AG unveiled an AI‑driven process control suite compatible with its single‑use reactors, targeting stem‑cell manufacturing. bbi‑biotech GmbH released an upgraded single‑use bubble column optimized for high‑density perfusion runs, aligning with the growing demand for recombinant proteins and vaccines.