North America Advanced Distribution Management System Market Overview - Definition, scope, and significance

The North America Advanced Distribution Management System (ADMS) market represents a critical segment of the utility technology landscape, encompassing sophisticated software solutions that integrate distribution management systems (DMS), outage management systems (OMS), and supervisory control and data acquisition (SCADA) technologies. These systems enable electric utilities to monitor, control, and optimize their distribution networks in real-time, providing enhanced visibility into grid operations and improving overall system reliability. The market's significance stems from its role in modernizing aging electrical infrastructure, facilitating the integration of renewable energy sources, and supporting the transition toward smart grid technologies. As utilities across North America face increasing pressure to improve grid resilience, reduce outage durations, and accommodate distributed energy resources, ADMS solutions have become indispensable tools for achieving operational excellence and meeting evolving regulatory requirements.

North America Advanced Distribution Management System Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The North America ADMS market is primarily driven by the urgent need to upgrade aging electrical infrastructure, the increasing penetration of renewable energy sources, and growing regulatory mandates for grid modernization. Utilities are investing heavily in ADMS solutions to improve grid reliability, reduce operational costs, and enhance customer satisfaction through faster outage response times. However, the market faces significant restraints including high implementation costs, cybersecurity concerns, and the complexity of integrating legacy systems with modern ADMS platforms. Key challenges include the shortage of skilled personnel to operate advanced systems, interoperability issues between different vendor solutions, and the need for substantial upfront capital investment. Despite these obstacles, numerous opportunities exist in the form of technological advancements in artificial intelligence and machine learning, the emergence of cloud-based ADMS solutions, and the growing demand for grid modernization in both urban and rural areas across North America.

North America Advanced Distribution Management System Market Growth Trends - Current and emerging trends shaping the market

The North America ADMS market is experiencing several transformative growth trends that are reshaping the industry landscape. The integration of artificial intelligence and machine learning capabilities into ADMS platforms is enabling predictive analytics and automated decision-making, significantly improving grid optimization and fault detection. Cloud-based ADMS solutions are gaining traction due to their scalability, cost-effectiveness, and ease of deployment, particularly for smaller utilities. The market is also witnessing increased adoption of mobile workforce management applications that integrate seamlessly with ADMS platforms, enhancing field operations efficiency. Additionally, the growing emphasis on cybersecurity features within ADMS solutions reflects the increasing threat landscape facing critical infrastructure. The convergence of ADMS with other smart grid technologies, such as advanced metering infrastructure (AMI) and distributed energy resource management systems (DERMS), is creating comprehensive grid management ecosystems that offer utilities unprecedented operational capabilities.

COVID-19 Impact on the North America Advanced Distribution Management System Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the North America ADMS market through supply chain interruptions, project delays, and budget constraints faced by utilities. However, the crisis ultimately accelerated digital transformation initiatives within the utility sector, as remote work requirements and the need for operational resilience highlighted the importance of advanced grid management solutions. Utilities increasingly recognized the value of ADMS platforms in enabling remote monitoring and control capabilities, leading to renewed investment in these technologies. The pandemic also emphasized the critical nature of reliable electricity supply, particularly for healthcare facilities and remote workers, reinforcing the business case for ADMS implementation. As the industry emerges from the pandemic, the market is experiencing a robust recovery trajectory, with utilities prioritizing ADMS investments as part of their post-pandemic infrastructure modernization strategies and resilience-building efforts.

North America Advanced Distribution Management System Market Competitive Landscape - Major competitors and market consolidation

The North America ADMS market features a competitive landscape characterized by both established technology giants and specialized utility software providers. Major players such as Siemens AG, General Electric Company, and Schneider Electric SE leverage their extensive resources and global presence to maintain dominant market positions. Meanwhile, specialized companies like Survalent Technology Corporation and Open Systems International Inc. focus on niche solutions and deep domain expertise to compete effectively. The market has witnessed increasing consolidation through strategic acquisitions and partnerships, as larger companies seek to expand their ADMS capabilities and smaller firms look for growth opportunities. This consolidation trend is creating a more integrated competitive environment where companies are developing comprehensive smart grid portfolios that extend beyond traditional ADMS functionality. The competitive dynamics are further shaped by the entry of cloud service providers and technology companies from adjacent industries, introducing new business models and innovation approaches to the market.

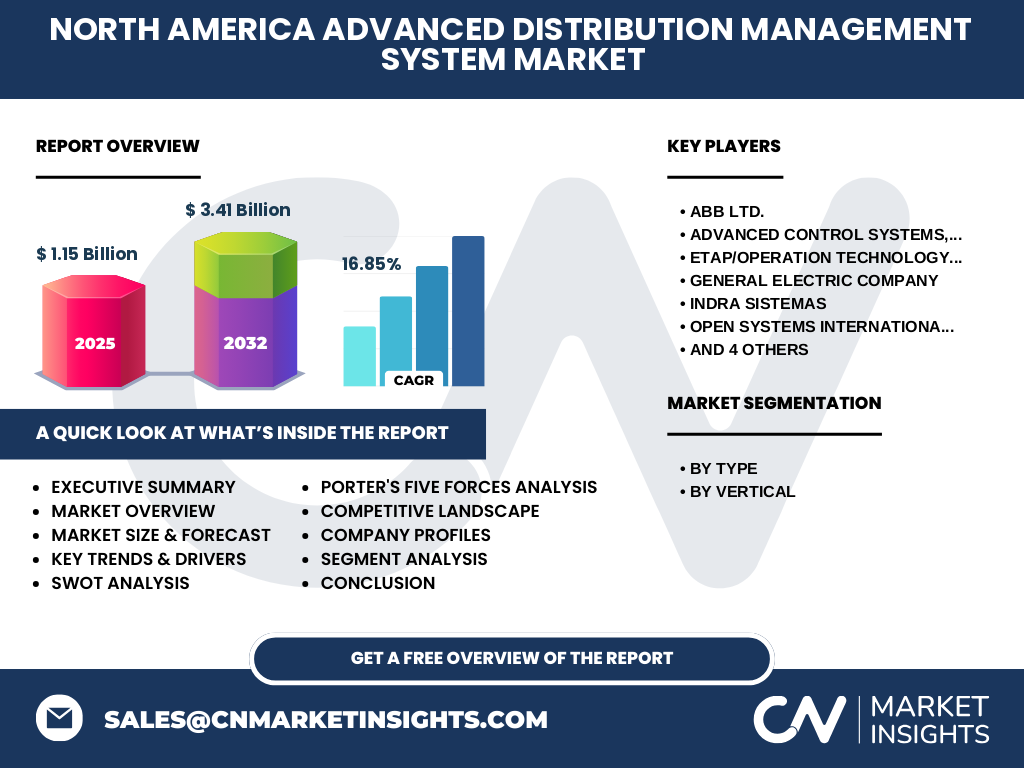

Executive Summary - High-level overview and key findings about North America Advanced Distribution Management System Market

The North America ADMS market is experiencing robust growth, driven by the critical need for grid modernization, renewable energy integration, and enhanced operational efficiency. With a market size of $1.15 billion in 2025 and projected to reach $3.41 billion by 2032, representing a CAGR of 16.85%, the market demonstrates strong growth potential. The commercial and industrial vertical segment is emerging as a key growth driver, while solution-based ADMS offerings continue to dominate the market. Leading companies including ABB Ltd., General Electric Company, and Siemens AG are investing heavily in R&D to enhance their product portfolios and maintain competitive advantages. The market is characterized by increasing technological sophistication, with AI and cloud computing becoming integral components of modern ADMS solutions. Despite challenges related to implementation complexity and cybersecurity concerns, the overall market outlook remains positive, supported by favorable regulatory environments and growing utility investments in smart grid infrastructure.

North America Advanced Distribution Management System Market Forecast - Projections for 2025-2032 period

The North America ADMS market is projected to experience substantial growth over the 2025-2032 period, with the market expanding from $1.15 billion in 2025 to $3.41 billion by 2032, representing a compound annual growth rate of 16.85%. This robust growth trajectory is underpinned by several factors, including the accelerating pace of grid modernization initiatives, increasing renewable energy integration requirements, and the growing emphasis on grid resilience and reliability. The forecast period will likely see continued technological advancements, with AI-driven analytics, cloud-based deployments, and enhanced cybersecurity features becoming standard components of ADMS solutions. Market expansion will be particularly strong in the commercial and industrial segment, as businesses increasingly adopt distributed energy resources and require sophisticated grid management capabilities. Geographic growth will be driven by both greenfield implementations in rapidly developing regions and brownfield upgrades in established utility territories, with regulatory mandates and incentive programs playing crucial roles in accelerating adoption rates across the forecast period.

North America Advanced Distribution Management System Market Size and Share by Segmentation - Breakdown by {segmentData}

The North America ADMS market segmentation reveals distinct patterns in solution preferences and vertical adoption. By type, the solution segment currently dominates the market, driven by comprehensive ADMS platforms that integrate DMS, OMS, and SCADA functionalities into unified systems. The service segment, while smaller, is experiencing faster growth as utilities increasingly seek implementation support, training, and ongoing maintenance services. In terms of vertical segmentation, the commercial and industrial sector represents a significant and growing market share, as businesses deploy ADMS solutions to manage complex energy consumption patterns and integrate distributed energy resources. The utility sector continues to be the largest vertical market, with electric distribution companies investing heavily in ADMS to improve grid reliability and operational efficiency. Regional variations in market share are influenced by factors such as regulatory requirements, utility infrastructure maturity, and the pace of renewable energy adoption, with certain regions demonstrating stronger growth potential based on their specific market conditions and policy frameworks.

Global North America Advanced Distribution Management System Market Size and Share by Region - Geographic distribution

The North American ADMS market exhibits distinct regional characteristics across the United States, Canada, and Mexico, each with unique drivers and adoption patterns. The United States represents the largest market share, driven by its extensive utility infrastructure, stringent regulatory requirements, and significant investments in grid modernization. California, Texas, and the Northeastern states are particular hotspots for ADMS adoption, reflecting their aggressive renewable energy targets and grid resilience initiatives. Canada's market is characterized by its focus on remote area electrification and integration of hydroelectric resources, with utilities in provinces like Ontario and British Columbia leading ADMS implementation. Mexico's market is experiencing rapid growth as the country modernizes its electrical infrastructure and attracts foreign investment in renewable energy projects. Regional differences in market size and share are influenced by factors such as population density, energy consumption patterns, regulatory frameworks, and the maturity of existing utility infrastructure, creating diverse opportunities and challenges across the North American landscape.

Regional Analysis of the North America Advanced Distribution Management System Market - Detailed regional market performance

The North American ADMS market demonstrates varied performance across different regions, reflecting diverse utility landscapes and regulatory environments. The Western region, particularly California and the Pacific Northwest, leads in ADMS adoption due to aggressive renewable energy mandates and wildfire mitigation requirements. These states have implemented some of the most advanced ADMS deployments, focusing on real-time grid monitoring and automated fault location capabilities. The Northeastern region shows strong market performance driven by aging infrastructure replacement needs and high electricity demand density, with utilities investing in ADMS to improve reliability and reduce outage durations. The Midwest region exhibits steady growth, supported by wind energy integration and rural electrification initiatives. The Southern region, while traditionally slower in ADMS adoption, is experiencing accelerated growth due to increasing population centers and the need to modernize distribution networks. Regional performance variations are also influenced by utility ownership structures, with investor-owned utilities generally showing faster ADMS adoption rates compared to municipal and cooperative utilities.

Leading Company Profiles in the North America Advanced Distribution Management System Market - Industry players and strategies

The North American ADMS market features several prominent players employing diverse strategies to capture market share and drive innovation. Siemens AG leverages its extensive utility industry experience and global reach to offer comprehensive ADMS solutions integrated with its broader smart grid portfolio. General Electric Company focuses on digital transformation initiatives, combining its Predix platform with advanced analytics capabilities to deliver intelligent ADMS solutions. Schneider Electric SE emphasizes energy management expertise, integrating ADMS with its EcoStruxure architecture to provide end-to-end grid optimization. ABB Ltd. differentiates through its strong focus on automation and robotics, bringing advanced control capabilities to ADMS platforms. Oracle Corporation leverages its enterprise software expertise to deliver cloud-based ADMS solutions with robust data management capabilities. These companies, along with specialized providers like Survalent Technology Corporation and Open Systems International Inc., are pursuing strategies that include strategic partnerships, acquisitions, and continuous product innovation to strengthen their market positions and address evolving utility needs.

Porter's Five Forces Analysis of the North America Advanced Distribution Management System Market - Competitive forces assessment

The North American ADMS market presents a complex competitive landscape when analyzed through Porter's Five Forces framework. The threat of new entrants remains moderate due to high barriers to entry, including substantial R&D requirements, established customer relationships, and complex regulatory compliance needs. However, technology companies from adjacent industries pose an increasing threat by leveraging their software expertise and cloud infrastructure capabilities. The bargaining power of buyers, primarily utilities, is significant given the large contract values and the importance of ADMS systems to their operations. This power is somewhat mitigated by the specialized nature of ADMS solutions and the high switching costs associated with changing vendors. Supplier power is relatively low for core technology components but increases for specialized hardware and integration services. The threat of substitutes is limited, as ADMS solutions offer unique capabilities that are difficult to replicate with alternative technologies. Competitive rivalry is intense, characterized by price competition, feature differentiation, and the pursuit of strategic partnerships to enhance product offerings and expand market reach.

SWOT Analysis of the North America Advanced Distribution Management System Market - Strengths, weaknesses, opportunities, threats

The North American ADMS market exhibits distinct strengths, weaknesses, opportunities, and threats that shape its competitive dynamics. Key strengths include the region's advanced technological infrastructure, strong regulatory support for grid modernization, and the presence of major industry players with substantial R&D capabilities. The market benefits from high utility awareness of ADMS benefits and increasing investment in smart grid technologies. However, significant weaknesses exist, including the high cost of implementation, integration challenges with legacy systems, and cybersecurity vulnerabilities that concern utilities. Opportunities abound in the form of growing renewable energy integration, the emergence of distributed energy resources, and the potential for AI and machine learning to enhance ADMS capabilities. The market also benefits from increasing utility focus on operational efficiency and customer service improvements. Threats include economic uncertainties that could impact utility capital expenditure, potential regulatory changes that might affect investment incentives, and the rapid pace of technological change that could render current solutions obsolete. Additionally, the market faces challenges from skilled workforce shortages and the complexity of managing increasingly distributed grid architectures.

North America Advanced Distribution Management System Market Value Chain Analysis - Industry structure and value flow

The North American ADMS market value chain encompasses multiple interconnected stages, from technology development through end-user implementation and ongoing support. At the foundation, component suppliers provide essential hardware and software building blocks, including sensors, communication devices, and development tools. System integrators and solution providers combine these components into comprehensive ADMS platforms, incorporating domain-specific functionalities and ensuring interoperability. Value-added resellers and distributors play crucial roles in market access, particularly for reaching smaller utilities and specialized applications. Implementation partners and consulting firms provide critical services for system deployment, integration with existing infrastructure, and change management support. At the apex of the value chain, utilities and commercial/industrial end-users derive value through improved grid operations, enhanced reliability, and operational cost savings. The value flow is characterized by increasing sophistication at each stage, with significant value creation occurring through system integration, customization, and the application of advanced analytics and AI capabilities that transform raw data into actionable insights for grid management.

Key Investment Insights in the North America Advanced Distribution Management System Market - Strategic investment recommendations

The North American ADMS market presents compelling investment opportunities driven by strong growth projections and technological evolution. Strategic investors should focus on companies demonstrating robust R&D capabilities in AI and machine learning applications for grid optimization, as these technologies represent the next frontier in ADMS functionality. Cloud-based ADMS solutions offer attractive investment potential due to their scalability, lower upfront costs, and alignment with utility digital transformation strategies. The integration of distributed energy resource management capabilities presents another key investment theme, as utilities increasingly need to manage bidirectional power flows and complex grid interactions. Investors should also consider opportunities in cybersecurity-focused ADMS solutions, given the critical nature of grid infrastructure and increasing cyber threat landscape. Strategic partnerships and acquisitions that expand geographic coverage or enhance technological capabilities represent additional investment avenues. The market's strong CAGR of 16.85% and the fundamental need for grid modernization support a positive long-term investment thesis, particularly for companies positioned at the intersection of traditional utility expertise and emerging digital technologies.

North America Advanced Distribution Management System Market Conclusion - Summary and key takeaways

The North American ADMS market stands at a pivotal juncture, characterized by strong growth potential, technological innovation, and evolving utility needs. With the market projected to grow from $1.15 billion in 2025 to $3.41 billion by 2032 at a CAGR of 16.85%, the industry presents significant opportunities for stakeholders across the value chain. Key takeaways include the accelerating pace of grid modernization initiatives, the increasing importance of renewable energy integration, and the growing role of AI and cloud technologies in shaping ADMS capabilities. The commercial and industrial vertical segment is emerging as a key growth driver, while the utility sector continues to be the primary market force. Despite challenges related to implementation complexity and cybersecurity concerns, the overall market trajectory remains positive, supported by favorable regulatory environments and the fundamental need for more resilient and efficient electrical distribution systems. Success in this market will require companies to balance technological innovation with practical implementation considerations, while addressing the unique needs of diverse utility landscapes across North America.

Research Methodology - How this research was conducted

This comprehensive market research on the North American ADMS market was conducted using a robust, multi-faceted methodology that combines primary and secondary research approaches. Primary research involved extensive interviews with industry experts, utility executives, technology providers, and regulatory officials to gather firsthand insights into market dynamics, technology trends, and implementation challenges. Secondary research encompassed a thorough analysis of industry reports, company financial statements, regulatory filings, trade publications, and government databases to validate and supplement primary findings. The research methodology employed both top-down and bottom-up approaches to market sizing, ensuring accuracy and reliability in the projections. Data triangulation techniques were utilized to cross-verify information from multiple sources, while advanced analytical tools were applied to identify growth patterns and market trends. The research team also conducted competitive landscaping exercises and value chain analyses to provide a comprehensive understanding of the market structure and dynamics. Special attention was given to regional variations and emerging technological developments to ensure the research captures the full complexity of the North American ADMS market landscape.

Research Scope - Coverage and limitations

This research report on the North American ADMS market provides comprehensive coverage of the industry landscape, focusing on market size, growth trends, competitive dynamics, and technological developments from 2025 through 2032. The scope encompasses all major segments including solution and service types, vertical applications, and regional markets across the United States, Canada, and Mexico. The research specifically examines key market drivers, restraints, challenges, and opportunities while providing detailed company profiles of leading industry players. However, certain limitations exist in the research scope, including the exclusion of specific financial metrics and market share percentages that were not publicly available. The report also does not cover every minor player in the highly fragmented market, focusing instead on major companies and emerging trends. Additionally, while the research provides regional analysis, it does not delve into hyper-local market variations or specific utility-level implementations. The scope is limited to the North American region and does not include global comparisons or emerging market analyses, maintaining a focused approach on the unique characteristics and dynamics of the North American ADMS market.

Key Companies and Recent Developments in the North America Advanced Distribution Management System Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The North American ADMS market features several key companies that are driving innovation and shaping industry trends through strategic initiatives and technological advancements. ABB Ltd. has recently announced the expansion of its Ability™ Electrical Distribution Control System, incorporating advanced AI capabilities for predictive grid management and enhanced cybersecurity features. Advanced Control Systems, Inc. has launched a new cloud-native ADMS platform designed specifically for smaller utilities, addressing the market gap for scalable, cost-effective solutions. ETAP/Operation Technology, Inc. has formed strategic partnerships with major cloud service providers to deliver hybrid ADMS solutions that combine on-premise reliability with cloud-based analytics capabilities. General Electric Company has introduced its latest GridIQ* ADMS platform, featuring enhanced distributed energy resource integration and real-time load forecasting capabilities. Indra Sistemas has expanded its presence in North America through the acquisition of a regional utility software provider, strengthening its market position and local support capabilities. Open Systems International Inc. has launched a next-generation ADMS solution with advanced mobile workforce management integration, addressing the growing need for field operations optimization. Oracle Corporation has announced the integration of its ADMS platform with its enterprise resource planning suite, providing utilities with unified operational and financial management capabilities. Schneider Electric SE has introduced its EcoStruxure™ ADMS, featuring enhanced interoperability with third-party systems and improved user interface design. Siemens AG has unveiled its Spectrum Power ADMS platform with advanced self-healing capabilities and improved renewable energy integration features. Survalent Technology Corporation has launched a new ADMS solution specifically designed for rural electric cooperatives, addressing the unique needs of this market segment. These developments reflect the industry's focus on cloud adoption, AI integration, enhanced cybersecurity, and improved user experiences as key strategic priorities for market leadership.