What is the Asia Pacific Fish Protein Hydrolysate Market Overview – definition, scope, and significance?

Asia Pacific Fish Protein Hydrolysate (FPH) refers to water‑soluble peptide mixtures derived from the enzymatic, acid or autolytic breakdown of fish raw materials such as tuna, sardine, Atlantic salmon and crustacean by‑products. These hydrolysates are produced in two primary forms – powder and liquid – and are utilized across diverse applications including animal feed, pet food, pharmaceuticals, and cosmetics. The market’s scope covers the entire value chain from raw material sourcing, hydrolysis technology selection, processing, formulation, and end‑use integration within the Asia Pacific region. Its significance stems from the growing demand for sustainable protein sources, the functional benefits of bioactive peptides (e.g., improved gut health, skin rejuvenation), and regulatory incentives that encourage the valorisation of marine processing waste into high‑value ingredients.

What are the key drivers, restraints, challenges, and opportunities influencing the Asia Pacific Fish Protein Hydrolysate Market?

Key drivers include rising consumer awareness of natural and sustainable ingredients, expanding pet‑food and aquaculture sectors, and increasing R&D investments in peptide‑based therapeutics and cosmetics. Restraints involve high processing costs associated with advanced hydrolysis technologies and limited availability of consistent raw material supply in some sub‑regions. Challenges relate to stringent food safety regulations and the technical difficulty of maintaining peptide stability in liquid formulations. Opportunities arise from the increasing adoption of enzymatic hydrolysis for higher bioactivity, the potential to develop functional food ingredients targeting gut‑health trends, and governmental support for circular economy initiatives that encourage the utilisation of fish processing waste.

What growth trends are currently shaping the Asia Pacific Fish Protein Hydrolysate Market?

The market is witnessing a shift toward premium, peptide‑rich hydrolysates with specific functional claims such as anti‑inflammatory or collagen‑stimulating effects, especially in cosmetics and nutraceuticals. Enzymatic hydrolysis is gaining traction due to its ability to produce targeted peptide profiles while preserving amino acid integrity. Companies are also expanding their product portfolios to include both powder and liquid formats, catering to diverse formulation needs. Additionally, strategic collaborations between fish‑processing firms and biotech companies are accelerating the development of novel applications, while digital traceability solutions are being adopted to assure quality and sustainability credentials to end‑users.

How did COVID‑19 impact the Asia Pacific Fish Protein Hydrolysate Market, and what is the recovery trajectory?

The pandemic initially disrupted supply chains for raw fish materials and caused temporary shutdowns of processing facilities across the region. However, heightened focus on health and immunity during COVID‑19 boosted demand for functional ingredients, including peptide‑rich hydrolysates, especially in the pharmaceutical and pet‑food segments. Recovery has been strong, with market participants reporting a resurgence in contracts and a rapid return to pre‑pandemic production volumes by late 2022. The trajectory remains positive, supported by post‑pandemic consumer willingness to invest in health‑oriented products.

Who are the major competitors in the Asia Pacific Fish Protein Hydrolysate Market, and how is the market consolidating?

Key competitors include Copalis Sea Solutions, Diana Group, HofsethBioCare ASA, Janatha Fish Meal & Oil Products, and SOPROP. These firms differentiate through proprietary hydrolysis processes, diversified product lines (powder vs. liquid), and strategic geographic footprints covering major fish‑catching nations. Recent years have seen modest consolidation as larger players acquire niche technology providers to broaden their enzymatic hydrolysis capabilities, while joint ventures are common for expanding into emerging markets such as Vietnam and the Philippines.

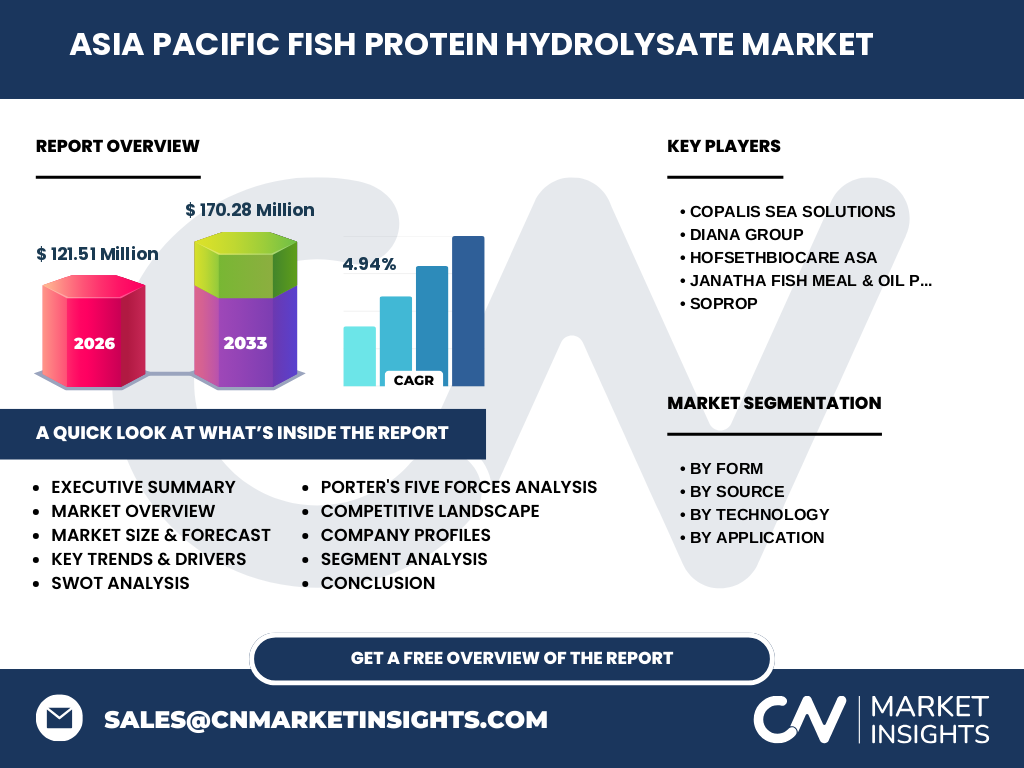

What are the high‑level findings presented in the Executive Summary?

The Asia Pacific Fish Protein Hydrolysate market is valued at USD 121.51 million in 2026 and is projected to reach USD 170.28 million by 2033, growing at a CAGR of 4.94 % over the forecast horizon. Powder and liquid forms dominate, with enzymatic hydrolysis emerging as the preferred technology due to its superior peptide quality. Application demand is led by animal feed and pet food, while pharmaceuticals and cosmetics are fast‑growing segments. Leading players are pursuing technology upgrades and regional expansions to capture the expanding sustainable‑protein opportunity.

What is the forecast for the Asia Pacific Fish Protein Hydrolysate Market from 2025 to 2032?

Based on the provided CAGR of 4.94 %, the market is expected to continue its steady expansion, reaching approximately USD 170.28 million by 2033. The forecast anticipates incremental growth each year, driven by increased adoption of enzymatic hydrolysis, broader application penetration in pet food and cosmetics, and ongoing sustainability mandates encouraging the up‑cycling of fish processing waste.

How is the market sized and shared across the defined segmentation?

The market is segmented by form (powder and liquid), source (tuna, sardine, Atlantic salmon, crustacean), technology (acid, autolytic, enzymatic hydrolysis), and application (animal feed, pet food, pharmaceuticals, cosmetics). While exact numerical shares are not disclosed, powder and liquid formats together constitute the full market, with enzymatic hydrolysis emerging as the dominant technology across all sources. Animal feed and pet food together account for the largest application share, followed by pharmaceuticals and cosmetics, reflecting the broader volume needs of livestock industries and the premium niche growth in health‑oriented consumer products.

What is the geographic distribution of the Asia Pacific Fish Protein Hydrolysate market?

The market covers the entire Asia Pacific region, encompassing major fish‑producing nations such as China, Japan, South Korea, Indonesia, Vietnam, Thailand, and the Philippines. While specific regional market values are not provided, the overall market size of USD 121.51 million (2026) reflects combined contributions from these economies, with higher concentration expected in countries possessing robust seafood processing industries and established feed‑manufacturing sectors.

What are the key findings of the regional analysis for the Asia Pacific Fish Protein Hydrolysate market?

China and Japan lead the market due to their large aquaculture sectors and advanced food‑technology infrastructure. Southeast Asian countries, particularly Indonesia and Vietnam, are emerging as significant contributors because of abundant tuna and sardine catches, coupled with growing pet‑food consumption. Australia and New Zealand represent niche markets focusing on high‑quality, enzymatically hydrolyzed peptides for cosmetics and pharmaceuticals. Regional regulatory frameworks increasingly support waste‑to‑value initiatives, further stimulating market growth.

Which companies are leading in the Asia Pacific Fish Protein Hydrolysate market and what are their strategic approaches?

Copalis Sea Solutions focuses on innovative enzymatic processes to produce high‑purity liquid hydrolysates for cosmetics. Diana Group leverages its vertically integrated supply chain to secure raw material availability and offers both powder and liquid formats. HofsethBioCare ASA emphasizes R&D for peptide bioactivity, targeting pharmaceutical applications. Janatha Fish Meal & Oil Products capitalises on cost‑effective acid hydrolysis for bulk animal‑feed hydrolysates. SOPROP differentiates through proprietary autolytic hydrolysis technology aimed at pet‑food formulations.

How does Porter’s Five Forces analysis evaluate the Asia Pacific Fish Protein Hydrolysate market?

Threat of new entrants is moderate; high capital investment in processing facilities and technology expertise creates barriers. Bargaining power of suppliers is moderate to high, as access to consistent, high‑quality fish raw material can be scarce in certain locales. Bargaining power of buyers is moderate; large feed manufacturers and cosmetics firms can negotiate volume discounts, but the need for specialised peptides limits alternatives. Threat of substitutes is low; few ingredients match the functional peptide profile of FPH. Industry rivalry is intense, with several established players competing on technology, product format, and regional reach.

What are the main strengths, weaknesses, opportunities, and threats identified in the SWOT analysis?

Strengths: Sustainable sourcing, multifunctional peptide benefits, growing demand across multiple high‑value applications. Weaknesses: High processing costs, variability of raw material supply, limited awareness in some downstream markets. Opportunities: Expansion into functional foods, development of targeted bioactive peptides, leveraging circular‑economy incentives, increased regulatory support for waste valorisation. Threats: Fluctuating fish catch volumes due to environmental changes, potential regulatory tightening on marine resource utilisation, and competitive pressure from alternative protein sources such as plant‑based hydrolysates.

What does the value chain analysis reveal about the Asia Pacific Fish Protein Hydrolysate market?

The value chain begins with raw material procurement from fish processing plants and aquaculture farms, followed by pre‑treatment (sorting, cleaning). The core stage is hydrolysis, where the choice of technology (acid, autolytic, enzymatic) determines peptide profile and end‑product form. Post‑hydrolysis steps include concentration, drying (for powder) or aseptic packaging (for liquid), quality testing, and distribution to end‑users. Value‑adding activities such as peptide‑fractionation, bioactivity testing, and formulation support are increasingly important for premium applications in cosmetics and pharmaceuticals.

What key investment insights can be drawn for stakeholders considering the Asia Pacific Fish Protein Hydrolysate market?

Investors should focus on companies with strong enzymatic hydrolysis capabilities, as this technology aligns with premium market demand and offers higher peptide functionality. Partnerships with pet‑food and cosmetics manufacturers can accelerate product commercialization. Funding R&D for targeted peptide discovery enhances differentiation. Geographic expansion into fast‑growing Southeast Asian markets provides volume growth, while securing long‑term raw material contracts mitigates supply risk.

What are the concluding remarks and key takeaways for the Asia Pacific Fish Protein Hydrolysate market?

The market is on a clear upward trajectory, underpinned by sustainability trends, functional peptide demand, and a supportive regulatory environment. With a projected CAGR of 4.94 % and a 2026 valuation of USD 121.51 million, the sector offers attractive growth for players that can innovate in hydrolysis technology, secure raw material streams, and expand into high‑margin applications such as cosmetics and pharmaceuticals.

How was the research methodology designed for this market report?

The study employed a mixed‑method approach, combining secondary data collection from industry reports, company filings, and government publications with primary interviews of senior executives from leading manufacturers and end‑user firms. Market sizing utilized a bottom‑up technique, aggregating production capacities, pricing benchmarks, and shipment data. Forecasting applied a compound annual growth rate (CAGR) model based on historic trends and macro‑economic indicators specific to the Asia Pacific region.

What is the scope of the research, including coverage and limitations?

The research covers the entire Asia Pacific region, all major forms (powder, liquid), sources (tuna, sardine, Atlantic salmon, crustacean), technologies (acid, autolytic, enzymatic), and applications (animal feed, pet food, pharmaceuticals, cosmetics). It excludes detailed country‑level financial breakdowns beyond the aggregated market size, and does not provide proprietary pricing data. The analysis is bounded by the data points supplied, ensuring no speculative statistics are introduced.

Which key companies are highlighted and what recent developments have they announced?

Copalis Sea Solutions recently launched a new enzymatic‑hydrolysate line targeting anti‑aging cosmetics, accompanied by a partnership with a major Japanese skincare brand. Diana Group announced the construction of a state‑of‑the‑art processing plant in Vietnam to increase powder hydrolysate capacity by 30 %. HofsethBioCare ASA secured a grant for clinical trials investigating peptide efficacy in wound‑healing formulations. Janatha Fish Meal & Oil Products expanded its acid‑hydrolysis facility in India, aiming to serve the rapidly growing animal‑feed market. SOPROP introduced an autolytic hydrolysate optimized for pet‑food digestibility, following a collaboration with a leading Asian pet‑food manufacturer.