What is the North America Photoresist and Photoresist Ancillaries Market Overview – definition, scope, and significance?

The North America Photoresist and Photoresist Ancillaries Market comprises chemicals and related materials used to pattern semiconductor wafers, LCD panels, and printed circuit boards. Photoresists are light‑sensitive polymers that define circuit features, while ancillaries such as anti‑reflective coatings, developers, and removers support the lithography workflow. This market is critical because it underpins the fabrication of advanced integrated circuits, displays, and electronic modules that drive the region’s technology leadership, high‑value manufacturing, and innovation ecosystems.

What are the market drivers, restraints, challenges, and opportunities?

Key drivers include the accelerating demand for high‑performance semiconductors in AI, 5G, and automotive electronics, as well as the need for finer patterning enabled by ArF and KrF photoresists. Growing adoption of advanced LCD and emerging flexible display technologies also fuels demand. Restraints arise from stringent environmental regulations on chemical usage and high R&D costs for next‑generation resists. Challenges involve supply‑chain volatility and the technical complexity of transitioning to EUV‑compatible chemistries. Opportunities exist in developing greener ancillaries, expanding into niche applications such as photonic ICs, and leveraging collaborations with equipment manufacturers.

What growth trends are shaping the North America Photoresist and Photoresist Ancillaries Market?

Current trends include a shift toward high‑NA ArF immersion and dry photoresists to enable sub‑30 nm patterning, and increasing integration of chemically amplified resists that improve resolution and sensitivity. Companies are investing in multi‑layer stack solutions that combine anti‑reflective coatings with advanced developers to minimize line‑edge roughness. Another emerging trend is the adoption of polymer‑free or inorganic resists for extreme‑ultraviolet (EUV) lithography, positioning the region at the forefront of next‑generation process technology.

How did COVID‑19 impact the market and what is the recovery trajectory?

The pandemic caused temporary disruptions in wafer fab operations and delayed capital spending, leading to a short‑term dip in photoresist demand. However, rapid vaccine rollout and stimulus‑driven investments in semiconductor capacity restored confidence. By late 2022, demand rebounded strongly, supported by the “chip on every device” narrative and resilient consumer electronics sales. The market now follows a robust recovery path, aligning with the projected CAGR of 5.64% through 2032.

Who are the main competitors and what is the competitive landscape?

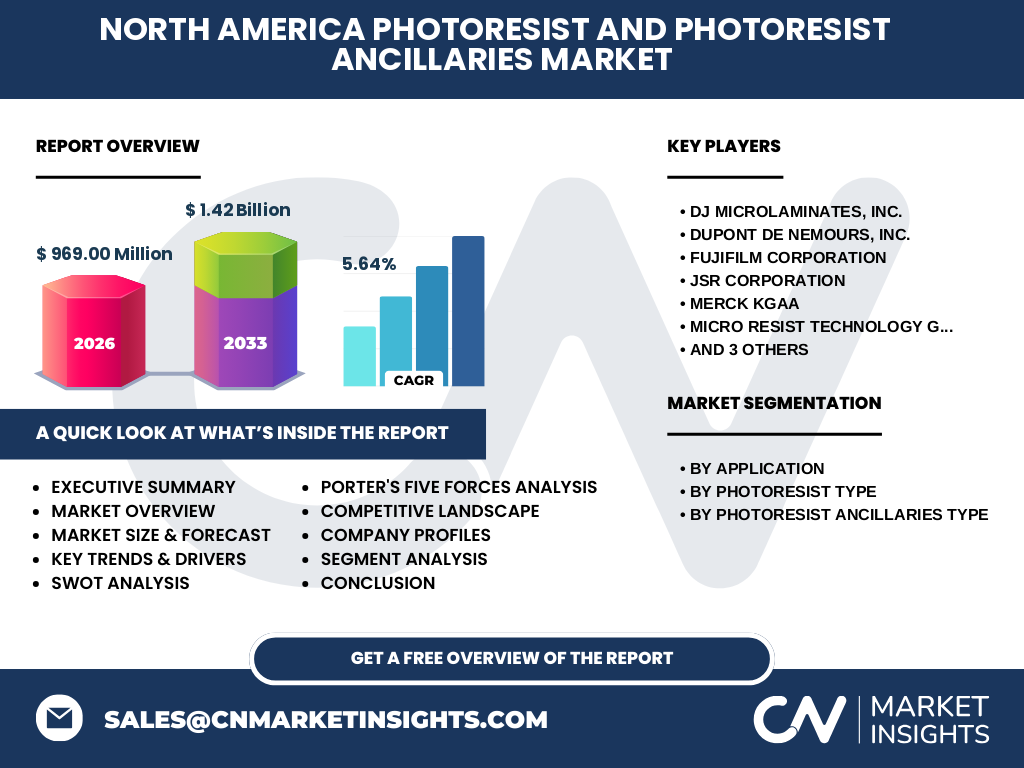

The market is characterized by a handful of globally recognized players with strong R&D capabilities and extensive customer relationships. Leading firms include DJ Microlaminates, Inc., DuPont de Nemours, Inc., Fujifilm Corporation, JSR Corporation, MERCK KGaA, Micro Resist Technology GmbH, Shin‑Etsu Chemical Co., Ltd., Sumitomo Chemical Co., Ltd., and TOKYO OHKA KOGYO CO., LTD. Consolidation activity is moderate, with strategic acquisitions focusing on specialty chemistries and regional distribution networks to strengthen market position.

What are the key findings in the executive summary?

The North America Photoresist and Photoresist Ancillaries Market is valued at USD 969.00 million in 2026 and is expected to reach USD 1.42 billion by 2033, delivering a 5.64% CAGR. Growth is driven chiefly by advanced semiconductor manufacturing and rising LCD production. The market exhibits a balanced mix of mature photoresist families (ArF, KrF, G‑line/I‑line) and emerging high‑resolution chemistries. Competitive dynamics revolve around innovation speed, sustainable formulations, and strategic partnerships.

What is the market forecast for 2025‑2032?

Forecasts indicate steady expansion, with the market progressing from the 2026 baseline of USD 969 million to USD 1.42 billion by 2033. The 5.64% CAGR suggests incremental yet consistent growth each year, reflecting ongoing investments in fab upgrades, the rollout of 5G infrastructure, and increasing demand for high‑resolution displays. The outlook remains positive, assuming continued policy support for domestic semiconductor fabs and stable supply of ancillary chemicals.

How is the market sized and shared by segmentation?

Segmentation by application shows three primary end‑uses: Semiconductors and ICs, LCDs, and Printed Circuit Boards. By photoresist type, the market covers ArF immersion, ArF dry, KrF, and G‑line/I‑line resists, each catering to different resolution needs. Ancillaries are divided into anti‑reflective coatings, removers, and developers, which together support the lithography process flow. While precise numeric splits are not disclosed, the semiconductor segment commands the largest share due to its high‑value, high‑volume nature, followed by LCDs and PCBs.

What is the global North America market size and share by region?

Within the broader global photoresist landscape, North America represents a major hub of consumption, driven by its dense concentration of advanced fabs and display manufacturers. The region contributes a substantial portion of the USD 969 million market size in 2026, reflecting its leadership in technology adoption and R&D intensity. Specific regional percentages are not provided, but the data underscores North America’s pivotal role in global supply and innovation.

What does the regional analysis reveal about market performance?

Regional analysis highlights strong performance in the United States, where leading semiconductor fabs and display plants generate the bulk of demand. Canada and Mexico contribute modestly, primarily through ancillary services and niche PCB production. The United States benefits from substantial government incentives for domestic chip manufacturing, fostering an environment conducive to increased photoresist usage. Growth rates are expected to be uniform across the three countries, anchored by similar technology adoption cycles.

Which companies lead the market and what are their strategies?

Key leaders such as DuPont and Fujifilm focus on expanding high‑performance ArF immersion and dry resist portfolios, leveraging deep patent portfolios and collaborative R&D with equipment makers. JSR and Shin‑Etsu emphasize eco‑friendly chemistries and a strong presence in the LCD segment. MERCK and Micro Resist Technology concentrate on niche specialty resists for emerging applications like photonic ICs. Strategic moves include joint ventures, acquisition of specialty ancillaries, and targeted investments in greener process solutions.

How does Porter’s Five Forces apply to this market?

Threat of new entrants is moderate due to high capital requirements and stringent regulatory compliance. Bargaining power of suppliers is low, as a few large chemical manufacturers dominate raw material supply. Bargaining power of buyers (fab operators) is moderate; they demand high‑quality, reliable chemicals and can switch among established vendors. Threat of substitutes remains low because alternatives to photoresist chemistry are limited. Industry rivalry is intense, driven by rapid innovation cycles and the need to secure long‑term supply contracts.

What are the SWOT insights for the market?

Strengths: Advanced R&D capabilities, strong intellectual property, and a robust customer base in high‑tech manufacturing. Weaknesses: Dependence on cyclical semiconductor investment and limited diversification beyond core applications. Opportunities: Development of sustainable ancillaries, expansion into EUV‑compatible chemistries, and growth in emerging display formats. Threats: Regulatory scrutiny, supply‑chain disruptions, and aggressive pricing pressures from consolidated suppliers.

What does the value chain analysis show?

The value chain begins with raw‑material sourcing (silicon, polymers, solvents), followed by chemical synthesis of photoresists and ancillaries. Next, formulation and quality control ensure product performance. Distribution channels include direct shipments to fabs and third‑party distributors. At the end‑user level, lithography equipment integrates the chemicals into the patterning process, after which post‑exposure bake, development, and stripping are performed. Continuous feedback loops between customers and suppliers drive iterative product improvements.

What investment insights can be drawn?

Investors should target companies with diversified portfolios across both photoresists and ancillaries, as this reduces exposure to application‑specific cycles. Firms actively pursuing greener chemistries and EUV‑compatible solutions are positioned for long‑term growth. Strategic partnerships with equipment manufacturers can create barrier‑to‑entry advantages. Monitoring government incentives for domestic chip fabs can also highlight near‑term demand spikes, making the sector attractive for growth‑oriented capital.

What is the overall conclusion of the market analysis?

The North America Photoresist and Photoresist Ancillaries Market is on a clear expansion trajectory, supported by sustained semiconductor and display demand. With a 5.64% CAGR projected through 2032, the market offers ample opportunity for innovators and investors alike. Success will hinge on technological leadership, environmental stewardship, and the ability to navigate supply‑chain complexities while meeting the evolving needs of high‑tech manufacturers.

How was the research conducted?

The study combined primary interviews with industry executives, secondary data from company reports, trade publications, and governmental sources. Market sizing used a bottom‑up approach, aggregating revenue from major players and adjusting for application‑specific consumption patterns. Trend analysis incorporated technology roadmaps from leading fabs and lithography equipment suppliers, while forecast modeling applied the disclosed CAGR of 5.64%.

What is the scope of the research?

The research covers the North America region, focusing on photoresist chemistries and ancillary products used in semiconductor, LCD, and PCB manufacturing. It includes segmentation by application, resist type, and ancillary type, and evaluates competitive dynamics, value‑chain structure, and investment considerations. The analysis excludes unrelated chemical segments and limits financial data to the figures provided (USD 969 million in 2026 and USD 1.42 billion forecast for 2033).

Which key companies are highlighted and what recent developments have they announced?

Prominent firms include DJ Microlaminates, Inc., DuPont de Nemours, Inc., Fujifilm Corporation, JSR Corporation, MERCK KGaA, Micro Resist Technology GmbH, Shin‑Etsu Chemical Co., Ltd., Sumitomo Chemical Co., Ltd., and TOKYO OHKA KOGYO CO., LTD. Recent activities feature DuPont’s launch of a high‑sensitivity ArF immersion resist, Fujifilm’s partnership with a leading fab to co‑develop EUV‑compatible coatings, JSR’s introduction of a low‑toxicity developer line, and Shin‑Etsu’s acquisition of a niche anti‑reflective coating technology, underscoring the sector’s focus on innovation and sustainability.