What is the Europe Photoresist and Photoresist Ancillaries Market overview – definition, scope, and significance?

The Europe Photoresist and Photoresist Ancillaries Market comprises chemicals and related materials used to pattern semiconductor wafers, LCD panels, and printed circuit boards (PCBs). Photoresists include ArF immersion, ArF dry, KrF, and G‑line/I‑line formulations, while ancillaries cover anti‑reflective coatings, developers, and removers. This market is critical to Europe’s advanced manufacturing ecosystem because it underpins the production of high‑performance chips, displays, and electronic assemblies that drive the region’s digital economy and export strength.

What are the key drivers, restraints, challenges, and opportunities shaping the Europe Photoresist and Photoresist Ancillaries Market?

Growth is driven by rising demand for semiconductor‑based solutions, expansion of 5G infrastructure, and increasing adoption of high‑resolution displays. Investments in EU‑wide chip initiatives and sustainability mandates also stimulate demand for advanced, low‑defect photoresists. Restraints stem from high raw‑material costs and strict environmental regulations on chemical handling. Challenges include supply‑chain disruptions and the need for continuous innovation to meet sub‑10 nm node requirements. Opportunities arise from emerging applications such as automotive electronics, AI accelerators, and the shift toward EUV‑compatible photoresist chemistries.

What are the current growth trends in the Europe Photoresist and Photoresist Ancillaries Market?

Key trends include a shift toward extreme‑ultraviolet (EUV) compatible resists, increased use of ArF immersion and dry photoresists for sub‑20 nm patterning, and a growing preference for eco‑friendly ancillaries that reduce waste water load. OEMs are consolidating design‑for‑manufacturing (DFM) processes, prompting suppliers to offer integrated material suites. The market is also seeing collaborative R&D projects funded by the European Commission to accelerate next‑generation lithography solutions.

How did COVID‑19 impact the Europe Photoresist and Photoresist Ancillaries Market, and what is the recovery trajectory?

The pandemic caused temporary plant shutdowns and logistics bottlenecks, leading to a short‑term dip in order volumes. However, pent‑up demand for consumer electronics and rapid rollout of 5G networks accelerated a rebound in 2022‑2023. The market has entered a recovery phase, supported by increased capital expenditure on new fab expansions and a robust pipeline of advanced node projects, positioning it for sustained growth.

Who are the major competitors and what is the level of market consolidation in the Europe Photoresist and Photoresist Ancillaries Market?

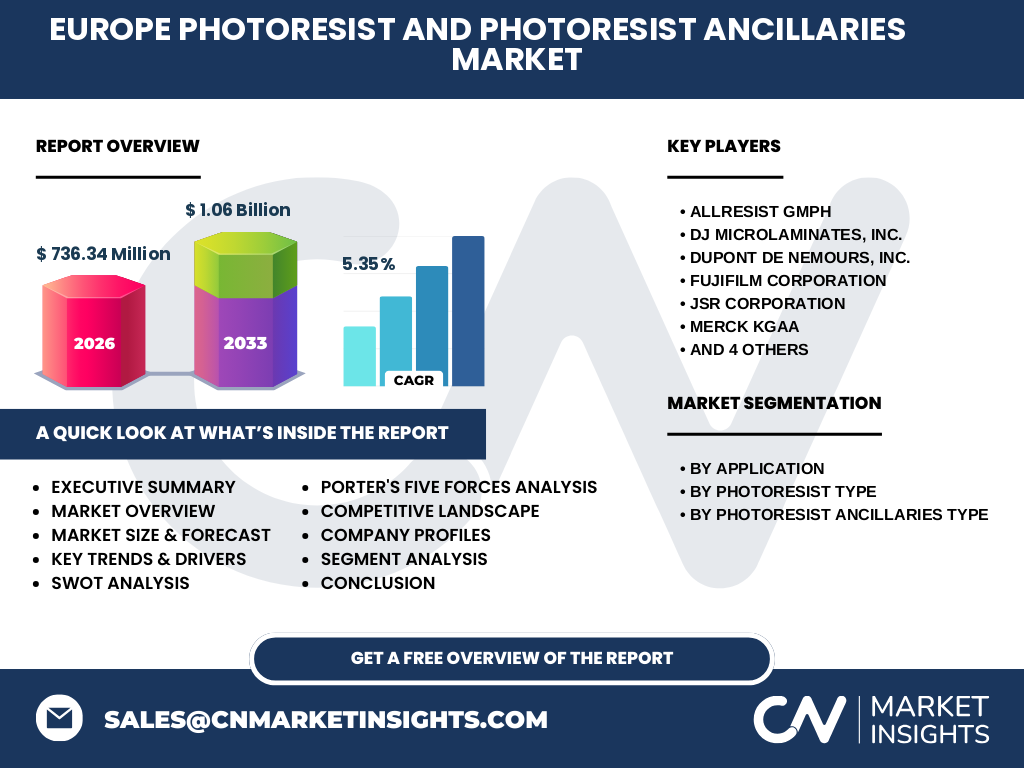

Key players include ALLRESIST GmbH, DJ Microlaminates, Inc., DuPont de Nemours, Inc., Fujifilm Corporation, JSR Corporation, Merck KGaA, Micro Resist Technology GmbH, Shin‑Etsu Chemical Co., Ltd., Sumitomo Chemical Co., Ltd., and Tokyo Ohka Kogyo Co., Ltd. The market exhibits moderate consolidation, with a few large multinational firms holding significant influence, while niche specialists focus on specialty formulations and ancillary products.

What are the high‑level findings in the executive summary of the Europe Photoresist and Photoresist Ancillaries Market?

The market was valued at €736.34 million in 2026 and is projected to reach €1.06 billion by 2033, delivering a CAGR of 5.35 %. Growth is powered by semiconductor demand, 5G rollout, and EU sustainability goals. The segment mix shows strong performance in semiconductor/IC applications, with ArF immersion and dry resists leading the technology frontier. Competitive dynamics are shaped by innovation, strategic partnerships, and portfolio diversification.

What are the forecasted market dynamics for the Europe Photoresist and Photoresist Ancillaries Market from 2025 to 2032?

Based on the stated CAGR of 5.35 %, the market is expected to expand steadily, reaching the €1.06 billion mark by 2033. The forecast anticipates accelerated adoption of EUV‑compatible resists, higher spend on anti‑reflective coatings, and incremental growth in developer and remover sales as node complexity increases. The outlook remains positive, with demand from automotive electronics and AI‑focused chips providing additional lift.

How is the market sized and shared by segmentation – by application, photoresist type, and ancillaries type?

Segmentation reveals three primary application groups: Semiconductors and ICs, LCDs, and Printed Circuit Boards. By photoresist type, the portfolio includes ArF immersion, ArF dry, KrF, and G‑line/I‑line resists. Ancillaries are divided into anti‑reflective coatings, removers, and developers. While exact monetary shares are not disclosed, the semiconductor/IC segment commands the largest proportion, followed by LCDs, with PCBs representing a smaller but growing niche.

What is the geographic distribution of the Europe Photoresist and Photoresist Ancillaries Market?

The market is concentrated within Europe, with leading activity in Germany, France, the United Kingdom, and the Benelux region where major fab sites and research centers are located. These areas benefit from strong governmental support for semiconductor manufacturing and a dense network of academic‑industry collaborations that fuel demand for advanced lithography materials.

What are the regional performance insights for the Europe Photoresist and Photoresist Ancillaries Market?

Germany leads in volume due to its large automotive and industrial electronics sectors, while France shows robust growth in display manufacturing for LCDs. The United Kingdom’s chip design ecosystem drives demand for high‑performance resists, and the Benelux region benefits from logistics hubs that support ancillary distribution. Each region exhibits a blend of mature fab capacity and emerging start‑ups focusing on next‑generation lithography.

Which companies are leading in the Europe Photoresist and Photoresist Ancillaries Market and what are their strategic approaches?

ALLRESIST GmbH focuses on high‑purity resist chemistries for EUV nodes. DuPont leverages its broad material platform to offer integrated resist‑ancillary kits. Fujifilm emphasizes sustainable development through low‑VOC formulations. JSR and Shin‑Etsu invest heavily in R&D for ArF and KrF resists. Merck and Sumitomo expand their ancillary portfolios, targeting anti‑reflective coatings that improve yield. Collaboration with fab operators and participation in EU research consortia are common strategic themes.

How does Porter’s Five Forces analysis apply to the Europe Photoresist and Photoresist Ancillaries Market?

Threat of new entrants is moderate due to high R&D costs and regulatory barriers. Bargaining power of suppliers is limited because raw‑material sources are diversified, though specialty chemicals can command premium pricing. Bargaining power of buyers (fab operators) is strong, driving demand for performance and cost efficiencies. Threat of substitutes remains low as alternative patterning technologies (e.g., directed self‑assembly) are still emerging. Competitive rivalry is intense, with firms racing to launch next‑generation resists and ancillary solutions.

What are the SWOT insights for the Europe Photoresist and Photoresist Ancillaries Market?

Strengths: Established supplier base, advanced R&D capabilities, and alignment with EU chip initiatives.

Weaknesses: High production costs and stringent environmental regulations.

Opportunities: EUV‑compatible chemistries, green ancillary products, and growth in automotive and AI chip segments.

Threats: Supply‑chain volatility, rapid technology cycles, and potential trade restrictions.

What does the value chain for the Europe Photoresist and Photoresist Ancillaries Market look like?

The value chain starts with raw‑material procurement (silicon‑based monomers, solvents), moves through formulation development, pilot scaling, and large‑scale manufacturing. Next are quality‑control labs that test resist performance, followed by distribution to fabs and downstream ancillary suppliers (coatings, developers, removers). End‑users provide feedback that informs iterative R&D, completing the loop.

What key investment insights can be drawn for stakeholders interested in the Europe Photoresist and Photoresist Ancillaries Market?

Investors should target companies with strong EUV roadmaps and environmentally compliant ancillaries, as these segments are poised for premium pricing. Strategic partnerships with fab operators and participation in EU research funding programs can de‑risk capital deployment. Diversifying across resist types and ancillary offerings reduces exposure to single‑node cycles, while focusing on firms with robust IP portfolios enhances long‑term returns.

What are the concluding takeaways from the Europe Photoresist and Photoresist Ancillaries Market analysis?

The market is on a steady growth trajectory, underpinned by a 5.35 % CAGR and a projected size of €1.06 billion by 2033. Semiconductor demand, EU sustainability goals, and advances in EUV lithography drive the outlook. Competitive pressure is high, but companies that invest in next‑gen chemistries and green ancillaries are best positioned to capture value.

How was the research for this market report conducted?

The methodology combined primary interviews with industry experts, secondary data extraction from company reports, trade publications, and EU research databases, followed by quantitative modeling to extrapolate the 2026 base figure to the 2033 forecast using the stated CAGR of 5.35 %.

What is the scope of this research and its limitations?

The study covers the European photoresist and ancillary ecosystem, focusing on applications in semiconductors, LCDs, and PCBs, and on the four defined resist types and three ancillary categories. It does not extend to non‑European markets or to emerging patterning technologies outside the lithography chemical space.

Who are the key companies and what recent developments have they announced?

ALLRESIST GmbH launched a low‑VOC ArF immersion resist for 3 nm nodes. DuPont introduced a bundled resist‑developer‑remover kit aimed at reducing process steps. Fujifilm announced a partnership with a German fab for co‑development of KrF resists. JSR unveiled a new G‑line photoresist with enhanced adhesion. Shin‑Etsu reported a joint venture with a French research institute to explore sustainable ancillaries. Merck rolled out a new anti‑reflective coating that lowers line‑edge roughness, while Sumitomo released a developer formulation optimized for high‑density via patterns.