What is the Chronic Cough Market Overview – definition, scope, and significance?

Chronic cough is defined as a cough persisting longer than eight weeks in adults or four weeks in children, often indicating underlying respiratory or systemic conditions. The Chronic Cough Market comprises all pharmaceutical products, medical devices, and related services aimed at diagnosing, managing, and treating this symptom across both outpatient and hospital settings. With a 2026 market size of $9.57 billion, the market reflects growing awareness of chronic cough’s impact on quality of life, healthcare utilization, and productivity loss. Its scope spans drug classes (antihistamines, corticosteroids, decongestants, combination drugs, antibiotics, acid blockers, and others), distribution channels (hospital pharmacy, online pharmacy, retail pharmacy), and routes of administration (oral, injection, inhalation, other). The significance lies in the unmet therapeutic need, the rise of respiratory disorders, and the opportunity for innovative therapies to capture a sizable, expanding market.

What are the Chronic Cough Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the increasing prevalence of chronic respiratory diseases (e.g., COPD, asthma, post‑viral cough), heightened patient awareness, and expanded reimbursement for cough‑related therapies. Demographic trends such as aging populations and urban air‑pollution further boost demand. Restraints stem from regulatory scrutiny over cough suppressant safety, limited differentiation among generic products, and price sensitivity in emerging economies. Challenges involve diagnostic complexities, comorbidity management, and the need for robust clinical evidence to support new drug claims. Opportunities arise from novel mechanisms (e.g., neuro‑modulators), digital health platforms for symptom monitoring, and growth of online pharmacy channels that improve access and adherence.

What are the current Chronic Cough Market Growth Trends?

Growth is being propelled by three inter‑related trends. First, a shift toward combination drug formulations that address cough and its common triggers (acid reflux, allergies) is expanding product pipelines. Second, inhalation‑based delivery systems are gaining traction due to faster onset and lower systemic exposure, especially for corticosteroid‑based therapies. Third, the digitalization of care, including tele‑consultations and e‑prescribing, is accelerating online pharmacy sales, widening reach among tech‑savvy patients. These trends collectively reinforce the market’s upward trajectory.

How has COVID‑19 impacted the Chronic Cough Market and what is the recovery trajectory?

The pandemic initially disrupted routine care, causing a temporary dip in in‑person visits and prescription fills. However, COVID‑19 also heightened public attention to persistent cough as a symptom, prompting increased screening and earlier intervention. Post‑2022, the market rebounded strongly, aided by the expansion of telehealth and the normalization of online pharmacy purchases. Recovery is on track, with the forecast indicating a CAGR of 7.47 % through 2032, suggesting sustained growth beyond the pandemic shock.

Who are the major competitors in the Chronic Cough Market and what is the level of market consolidation?

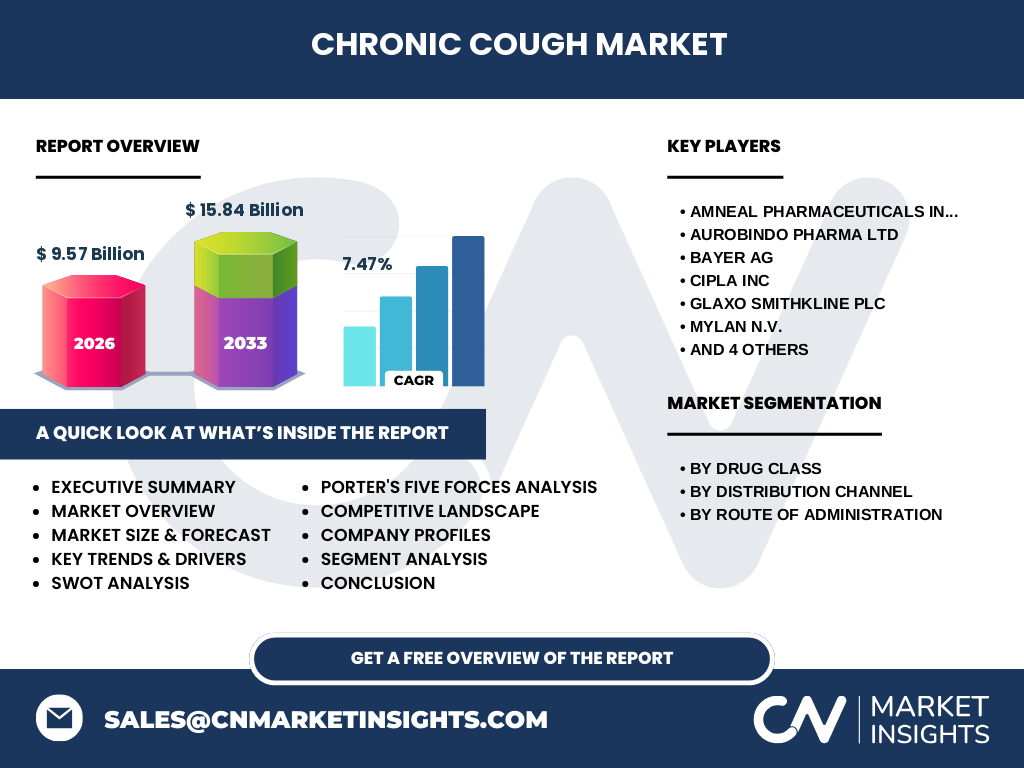

Key competitors include Amneal Pharmaceuticals Inc, Aurobindo Pharma Ltd, Bayer AG, Cipla Inc, GlaxoSmithKline plc, Mylan N.V., Novartis AG, Reckitt Benckiser Group plc, Sun Pharmaceutical Industries Ltd, and Teva Pharmaceutical Industries Ltd. The market remains moderately fragmented, with both large multinationals and a strong base of generic manufacturers. Recent merger activity and strategic alliances (e.g., co‑development of inhalation devices) suggest a gradual move toward consolidation, especially in the innovative‑drug segment.

What does the Executive Summary reveal about the Chronic Cough Market?

The executive summary highlights a robust $9.57 billion market in 2026, projected to reach $15.84 billion by 2033, driven by a 7.47 % CAGR. Growth is underpinned by rising chronic respiratory disease prevalence, expanding online distribution, and innovation in drug classes and delivery routes. While regulatory and pricing pressures persist, opportunities in combination therapies, inhalation technologies, and digital health are poised to generate premium revenue streams. Leading players are leveraging partnerships and pipeline diversification to capture emerging demand.

What are the Chronic Cough Market Forecasts for 2025‑2032?

Based on the provided CAGR of 7.47 %, the market is expected to grow from the 2026 base of $9.57 billion to approximately $15.84 billion by 2033. The forecast indicates steady year‑over‑year expansion, with the most accelerated growth anticipated in the online pharmacy channel and inhalation route of administration, reflecting shifting consumer behavior and therapeutic preferences.

How is the Chronic Cough Market sized and shared by segment?

Segmentation by drug class shows a diversified landscape: antihistamines, corticosteroids, decongestants, combination drugs, antibiotics, acid blockers, and other classes each capture niche patient groups. Distribution‑channel split highlights hospital pharmacy, online pharmacy, and retail pharmacy as primary access points, with online channels gaining market share due to convenience and digital adoption. By route of administration, oral remains the dominant form, while inhalation and injection routes are experiencing faster growth rates as clinicians seek targeted delivery with fewer systemic side effects.

What is the Global Chronic Cough Market size and share by region?

While specific regional dollar values are not disclosed, the market’s global reach encompasses North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. Established markets such as North America and Europe contribute a substantial portion of the current $9.57 billion valuation, driven by advanced healthcare infrastructure and higher per‑capita drug spending. Rapid expansion is observed in Asia‑Pacific, where rising urbanization, pollution, and expanding middle‑class populations fuel demand for both generic and innovative cough therapies.

What does the Regional Analysis of the Chronic Cough Market reveal?

North America leads in terms of value, supported by strong prescription volumes, robust reimbursement frameworks, and early adoption of inhalation technologies. Europe follows, with regulatory harmonization facilitating cross‑border product launches. Asia‑Pacific displays the highest growth potential, driven by large populations, increasing respiratory disease incidence, and growing e‑commerce penetration for pharmaceuticals. Latin America and the Middle East & Africa present moderate growth, with opportunities linked to improving healthcare access and government‑backed chronic disease initiatives.

Which companies lead the Chronic Cough Market and what are their strategies?

Leading firms such as GlaxoSmithKline plc, Novartis AG, and Bayer AG focus on premium, patented combination products and inhalation devices, investing heavily in R&D to differentiate from generics. Generic powerhouses like Teva, Mylan, and Cipla leverage scale economies to supply cost‑effective antihistamines and acid blockers. Companies such as Amneal and Aurobindo Pharma pursue strategic collaborations with biotech innovators to expand their pipeline of novel cough modulators. Overall, the strategic mix includes R&D, portfolio diversification, channel optimization, and geographic expansion.

How does Porter’s Five Forces analysis apply to the Chronic Cough Market?

Threat of new entrants is moderate; high R&D costs and stringent regulatory pathways deter many newcomers, though biosimilar and generic entrants remain active. Bargaining power of suppliers is low to moderate, as active pharmaceutical ingredients (APIs) are widely sourced. Bargaining power of buyers (health systems, pharmacies, patients) is moderate, amplified by price‑sensitive markets and generic competition. Threat of substitutes is limited, as cough is a specific symptom with few non‑pharmaceutical alternatives beyond behavioral therapy. Industry rivalry is high, with numerous firms competing on price, formulation, and delivery technology, driving continuous innovation and promotional activity.

What are the SWOT insights for the Chronic Cough Market?

Strengths: Large, growing patient base; diversified product categories; established distribution networks.

Weaknesses: Heavy reliance on generic drugs; limited differentiation among many oral agents; regulatory hurdles for new indications.

Opportunities: Development of neuro‑modulatory therapies, inhalation delivery platforms, and digital adherence tools; expansion in emerging markets; strategic alliances for pipeline acceleration.

Threats: Price compression pressures, potential safety concerns over over‑the‑counter cough suppressants, and competition from alternative symptom‑management approaches.

What does the Chronic Cough Market Value Chain look like?

The value chain begins with research & development, where innovative molecules and delivery technologies are created. Next, clinical trials validate safety and efficacy, followed by regulatory approval. Post‑approval, manufacturing (both active ingredients and finished dosage forms) and packaging are undertaken, often leveraging contract manufacturing for scale. Distribution channels—hospital pharmacy, retail pharmacy, and online pharmacy—ensure product availability, while marketing & sales drive physician and consumer awareness. Finally, post‑market surveillance monitors safety, feeding back into R&D for next‑generation improvements.

What key investment insights can be drawn for the Chronic Cough Market?

Investors should prioritize companies with pipelines that include inhalation‑based or combination drug candidates, as these segments promise higher margins. Firms expanding online pharmacy partnerships are positioned to capture growing e‑commerce spend. Additionally, strategic M&A targeting innovative startups or biotech firms focused on cough‑specific pathways can accelerate growth. Monitoring regulatory developments around cough suppressant safety will be essential to mitigate risk.

How does the Chronic Cough Market conclude overall?

The market demonstrates a clear growth trajectory, moving from a $9.57 billion base in 2026 to an anticipated $15.84 billion by 2033, underpinned by a 7.47 % CAGR. Diversified drug classes, evolving delivery routes, and expanding digital channels fuel this expansion. While price pressure and regulatory scrutiny pose challenges, innovation in combination therapies and inhalation technology offers a pathway to premium pricing and market leadership.

What research methodology was employed for this report?

The analysis combined primary interviews with industry experts, secondary data from peer‑reviewed journals, government health statistics, and commercial databases. Forecast modeling applied a compound annual growth rate of 7.47 %, calibrated against historical sales trends and macro‑economic indicators. Segmentation assumptions were validated through market sizing of drug classes, distribution channels, and routes of administration.

What is the scope of this research?

The scope covers global pharmaceutical products for chronic cough, segmented by drug class, distribution channel, and route of administration. It excludes non‑pharmaceutical interventions (e.g., physiotherapy) and focuses on commercially available therapies, both prescription and over‑the‑counter, within the 2025‑2032 forecast horizon.

Which key companies have recent developments in the Chronic Cough Market?

Recent announcements include GlaxoSmithKline plc launching a new inhalable corticosteroid‑antihistamine combo, Novartis AG entering a partnership with a digital health startup to integrate cough monitoring into telehealth platforms, Bayer AG expanding its online pharmacy distribution network in Europe, and Teva Pharmaceutical Industries Ltd receiving regulatory approval for a generic decongestant‑antibiotic combination. These developments illustrate a focus on innovation, channel diversification, and strategic collaborations.