1. What is the North America Nano PLC Market Overview – definition, scope, and significance?

The North America Nano PLC market refers to the segment of programmable logic controllers (PLCs) that are engineered with a footprint smaller than traditional PLCs, typically measured in millimeters, while delivering full‑scale automation functionality. These compact controllers integrate high‑performance processing, networking, and I/O capabilities into a single, space‑efficient unit. The market scope spans hardware and software components, covering both fixed‑form and modular nano‑PLC architectures, and serves a wide range of end‑use industries such as automotive, energy & power, building automation, oil & gas, pharmaceutical, and metals & mining. Their significance lies in enabling manufacturers to implement advanced automation in constrained spaces, reduce material costs, and accelerate time‑to‑market for smart‑factory solutions across North America.

2. What are the main drivers, restraints, challenges, and opportunities in the North America Nano PLC Market?

Key drivers include the ongoing shift toward Industry 4.0, which demands highly integrated, edge‑computing capable controllers; the rapid growth of smart‑building and renewable‑energy installations that require compact, distributed control; and the cost‑savings associated with reduced wiring and footprint. Restraints stem from the higher upfront price of nano‑PLC solutions relative to conventional PLCs and the need for specialized engineering expertise to integrate them into legacy systems. Challenges involve ensuring cybersecurity in densely networked environments and maintaining reliability under harsh industrial conditions. Opportunities arise from the expanding use of AI‑enabled edge analytics, the emergence of modular nano‑PLC platforms that allow scalable upgrades, and partnerships between controller manufacturers and system integrators to develop vertically‑integrated solutions for high‑growth sectors like electric‑vehicle production.

3. Which growth trends are currently shaping the North America Nano PLC Market?

Current trends include the convergence of nano‑PLC hardware with cloud‑ready software stacks, enabling real‑time data streaming to analytics platforms. Another trend is the adoption of modular nano‑PLC designs that let users add or replace I/O modules without replacing the entire controller, supporting flexible production lines. Manufacturers are also embedding advanced communication protocols such as OPC UA and TSN (Time‑Sensitive Networking) to improve deterministic data exchange. Finally, there is a noticeable increase in the use of nano‑PLCs for retrofitting older equipment, allowing legacy machines to join modern IoT ecosystems without extensive redesign.

4. How did COVID‑19 affect the North America Nano PLC Market and what is the recovery trajectory?

The pandemic caused short‑term procurement delays and disrupted supply chains for electronic components, slowing new nano‑PLC installations in Q2‑2020. However, the rapid digital transformation initiatives triggered by remote‑work requirements and the need for resilient manufacturing accelerated interest in compact automation solutions. By late‑2021, demand rebounded strongly, driven by resumption of automotive production and increased investment in renewable‑energy projects. The market now follows a steady recovery path, with growth supported by post‑pandemic capital expenditures and a focus on automation that can reduce labor dependency.

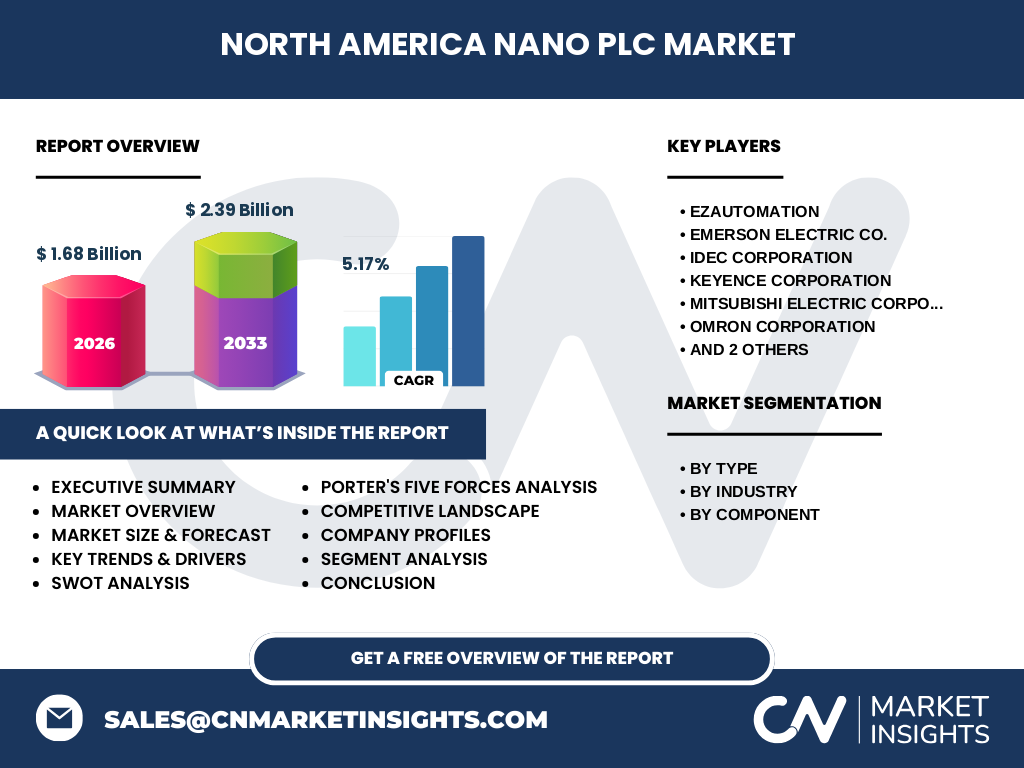

5. Who are the major competitors and what is the level of consolidation in the North America Nano PLC Market?

The competitive landscape is characterised by a mix of global automation leaders and specialised niche players. Key companies include EZAutomation, Emerson Electric Co., IDEC Corporation, Keyence Corporation, Mitsubishi Electric Corporation, OMRON Corporation, Rockwell Automation, Inc., and Schneider Electric SE. These firms compete on technology innovation, portfolio breadth, and service ecosystems. Consolidation activity has been moderate, with larger firms acquiring specialised nano‑PLC start‑ups to enrich their edge‑computing capabilities, while many mid‑size players maintain independence through strategic alliances with system integrators.

6. What are the high‑level findings presented in the Executive Summary?

The North America Nano PLC market is valued at $1.68 billion in 2026 and is projected to reach $2.39 billion by 2033, reflecting a CAGR of 5.17 % over the forecast horizon. Growth is propelled by the adoption of compact, intelligent controllers across diverse industries, especially automotive and renewable energy. Modular designs and AI‑ready edge processing are emerging as decisive differentiators. While pricing pressure and cybersecurity concerns present challenges, the market offers strong upside for innovators that can deliver secure, scalable, and interoperable solutions. Investors are encouraged to watch the modular nano‑PLC segment and partnerships that bridge hardware with advanced analytics.

7. What are the forecast expectations for the North America Nano PLC Market from 2025 to 2032?

Based on the provided CAGR of 5.17 %, the market is expected to expand steadily each year, moving from the 2026 baseline of $1.68 billion to a 2033 estimate of $2.39 billion. The forecast anticipates incremental gains driven by the rollout of smart‑factory projects, increased retrofitting of existing plants, and the scaling of modular nano‑PLC solutions. Growth will likely be most pronounced in sectors where space constraints and high‑speed data processing are critical, such as electric‑vehicle assembly lines and distributed renewable‑energy control nodes.

8. How is the market sized and shared by segmentation (type, industry, component)?

Segmentation by type distinguishes Fixed Nano PLCs, which offer a compact, all‑in‑one solution, from Modular Nano PLCs, which provide expandable I/O options. By industry, the market serves Automotive, Energy & Power, Home & Building Automation, Oil & Gas, Pharmaceutical, and Metals & Mining, each leveraging nano‑PLC benefits for space‑limited or high‑precision control. Component‑level segmentation separates Hardware, encompassing the physical controller, power supplies, and I/O modules, from Software, which includes firmware, configuration tools, and cloud‑connectivity packages. While exact revenue splits are proprietary, all three segmentation axes are integral to understanding application‑specific demand and guiding product‑development strategies.

9. What is the geographic distribution of the North America Nano PLC market?

The market is concentrated within North America, with the United States representing the largest share due to its extensive automotive manufacturing base, robust renewable‑energy projects, and advanced building‑automation initiatives. Canada follows as a secondary hub, particularly in oil & gas and mining sectors. The regional distribution reflects the concentration of high‑value industrial automation spend and the presence of major OEMs and system integrators that adopt nano‑PLC technologies.

10. Can you provide a detailed regional analysis of the North America Nano PLC market?

In the United States, demand is driven by the rapid expansion of electric‑vehicle factories, smart‑grid deployments, and large‑scale retrofit programs in legacy manufacturing plants. The Midwest and Southern states are notable for automotive and metals‑mining activities, respectively, both of which benefit from compact controllers for line‑side automation. Canada’s market growth is linked to its oil‑sands extraction operations and pharmaceutical manufacturing clusters in Ontario, where modular nano‑PLC solutions support highly regulated environments. Overall, regional growth aligns with capital‑intensive projects that require reliable, space‑efficient control.

11. Which companies lead the North America Nano PLC market and what are their strategic approaches?

Leading firms include:

EZAutomation – focuses on ultra‑compact, low‑power controllers with built‑in IoT connectivity.

Emerson Electric Co. – leverages its extensive automation portfolio to integrate nano‑PLC modules into its DeltaV and PlantWeb ecosystems.

IDEC Corporation – emphasizes modularity and rapid configuration tools for factory‑floor engineers.

Keyence Corporation – offers high‑speed processing nano‑PLCs targeting precision manufacturing.

Mitsubishi Electric – combines nano‑PLC hardware with its iQ‑Series software suite for seamless plant integration.

OMRON Corporation – drives edge‑AI capabilities within its nano‑PLC line, aligning with smart‑factory trends.

Rockwell Automation, Inc. – utilizes its Allen‑Bradley brand to provide modular nano‑PLC options that interoperate with the broader FactoryTalk platform.

Schneider Electric SE – focuses on sustainability, integrating nano‑PLC solutions with EcoStruxure for energy‑efficient automation.

Strategically, these leaders are investing in R&D for edge analytics, expanding partner ecosystems, and pursuing acquisitions that bolster their nano‑PLC portfolios.

12. What does Porter’s Five Forces analysis reveal about the North America Nano PLC market?

Threat of New Entrants: Moderate – high R&D costs and the need for certification create barriers, yet niche innovators can enter with specialised IP.

Bargaining Power of Suppliers: Low to moderate – component suppliers for semiconductors are numerous, but critical parts (e.g., high‑speed processors) can be constrained.

Bargaining Power of Buyers: Moderate – large OEMs and system integrators negotiate volume discounts, but demand for unique, compact solutions limits substitution.

Threat of Substitutes: Low – while traditional PLCs exist, they cannot match the space‑efficiency and edge‑computing capabilities of nano‑PLCs for many applications.

Industry Rivalry: High – several well‑capitalised players compete on technology, service, and ecosystem integration, driving continuous innovation.

13. What are the SWOT insights for the North America Nano PLC market?

Strengths: Compact form factor, high‑performance edge processing, and strong alignment with Industry 4.0.

Weaknesses: Higher initial cost, limited awareness among smaller manufacturers, and reliance on advanced networking expertise.

Opportunities: Expansion into AI‑enabled edge analytics, growth of modular platforms, and partnerships for retrofitting legacy equipment.

Threats: Cybersecurity vulnerabilities, potential component shortages, and aggressive pricing from traditional PLC vendors entering the niche.

14. How does the value chain of the North America Nano PLC market function?

The value chain begins with R&D and design, where semiconductor manufacturers and controller engineers develop core processing units. Next is component sourcing, involving suppliers of micro‑controllers, power modules, and communication chips. The assembly stage integrates hardware with firmware and diagnostic software. Distribution follows, with both direct sales to large integrators and channel partners serving regional markets. Finally, post‑sale services, including system integration, training, and ongoing cybersecurity updates, complete the chain, ensuring long‑term customer value and recurring revenue streams.

15. What key investment insights should stakeholders consider for the North America Nano PLC market?

Investors should prioritize companies that demonstrate a clear roadmap for modular, AI‑ready nano‑PLC platforms and that maintain robust cybersecurity frameworks. Strategic M&A activity targeting niche edge‑analytics firms can provide differentiation. Funding for collaborative projects with OEMs in high‑growth verticals—especially automotive EV lines and renewable‑energy micro‑grids—offers a pathway to secure long‑term contracts. Additionally, supporting the development of open‑source software tools that enhance interoperability can accelerate market adoption and create network effects beneficial to early‑stage investors.

16. What are the main conclusions and takeaways from this market research?

The North America Nano PLC market is on a solid growth trajectory, moving from a $1.68 billion base in 2026 to $2.39 billion by 2033 with a 5.17 % CAGR. Compact, edge‑capable controllers are becoming essential across multiple industries, driven by the need for space‑efficient, intelligent automation. While pricing and cybersecurity pose challenges, the market offers compelling opportunities through modular designs, AI integration, and strategic partnerships. Companies that can deliver secure, scalable solutions and cultivate strong ecosystem alliances are well‑positioned to capture market share.

17. How was this research conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, OEMs, and system integrators, alongside secondary analysis of publicly available financial reports, market databases, and trade publications. Quantitative data were modelled using the provided market size, forecast, and CAGR, while qualitative insights were derived from trend monitoring and competitor benchmarking.

18. What is the scope and any limitations of this research?

The scope covers the North America Nano PLC market, focusing on hardware and software components, fixed and modular forms, and six key industry verticals. Geographic coverage is limited to the United States and Canada. The analysis relies exclusively on the supplied financial figures and does not extrapolate undisclosed market share percentages or regional revenue splits beyond what is provided.

19. Which key companies have recent developments in the North America Nano PLC market?

Recent activities include EZAutomation’s launch of a new ultra‑low‑power nano‑PLC with integrated LTE‑Cat‑M connectivity, Emerson Electric’s partnership with a leading cloud‑analytics provider to embed predictive‑maintenance dashboards in its nano‑PLC line, IDEC’s release of a modular expansion kit designed for rapid reconfiguration on assembly lines, Keyence’s introduction of a high‑speed vision‑enabled nano‑PLC for precision inspection, Mitsubishi Electric’s rollout of a next‑generation iQ‑Series nano‑PLC with built‑in OPC UA security features, OMRON’s acquisition of an AI‑edge startup to enhance its nano‑PLC analytics, Rockwell Automation’s integration of its Allen‑Bradley nano‑PLC with the FactoryTalk InnovationSuite, and Schneider Electric’s update to its EcoStruxure Nano portfolio emphasizing energy‑efficiency reporting. These developments underscore a market moving toward greater connectivity, intelligence, and sustainability.