What is the Europe Surgical Suture Market Overview – definition, scope, and significance?

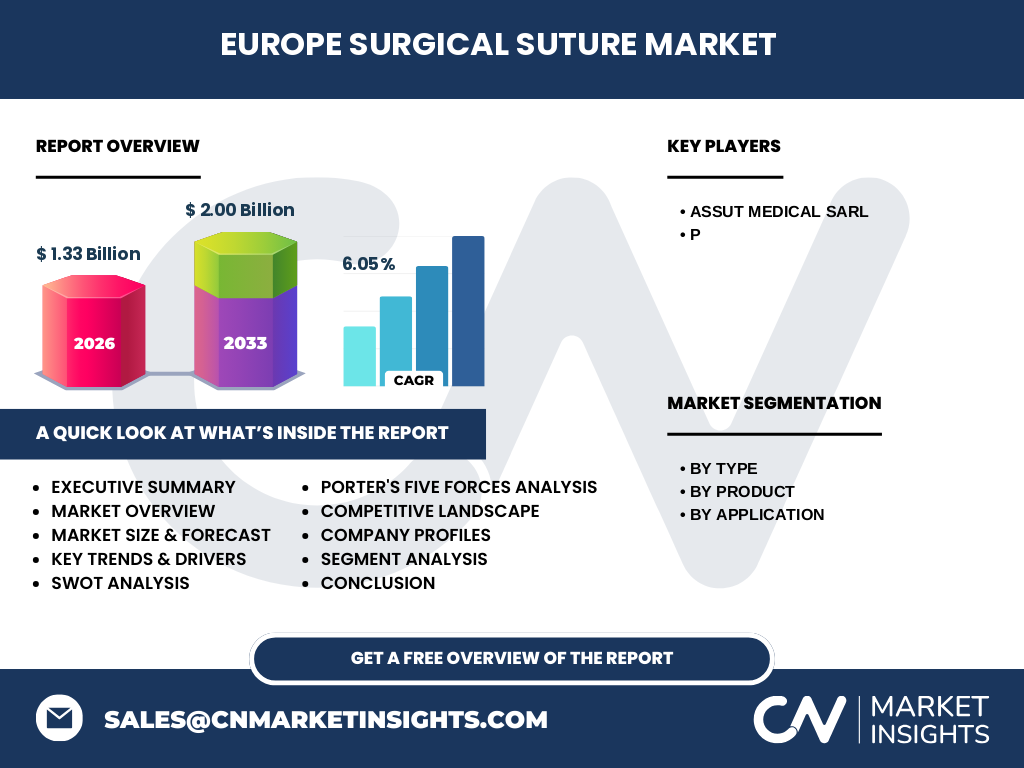

The Europe Surgical Suture Market comprises manufacturers, distributors, and end‑users of suturing materials employed in a wide range of surgical procedures across European countries. Surgical sutures are categorized by material type (monofilament or braided), by absorption characteristic (absorbable or non‑absorbable), and by application area (cardiovascular, gynecological, ophthalmic, orthopedic, and general surgeries). The market’s significance lies in its direct impact on patient outcomes, surgical efficiency, and post‑operative recovery. With a 2026 market size of €1.33 billion, the sector supports hospitals, ambulatory surgery centers, and specialty clinics, driving demand for high‑performance, biocompatible, and cost‑effective suturing solutions.

What are the main drivers, restraints, challenges, and opportunities shaping the Europe Surgical Suture Market?

Key drivers include rising surgical volumes driven by aging populations and increasing prevalence of chronic diseases, coupled with technological advances in minimally invasive and robotic surgeries that demand specialized sutures. Health‑care spending growth across the EU further stimulates procurement. Restraints stem from stringent regulatory requirements and price‑sensitivity in public health systems, which can slow adoption of premium products. Major challenges involve supply‑chain disruptions and the need for continuous innovation to meet stricter safety standards. Opportunities arise from emerging biodegradable suture technologies, customized product portfolios for niche surgeries, and expansion into Eastern European markets where surgical infrastructure is modernising.

What growth trends are currently influencing the Europe Surgical Suture Market?

Current trends feature a shift toward absorbable monofilament sutures that combine reduced infection risk with ease of handling, especially in laparoscopic and robotic procedures. There is also a growing preference for sutures with antimicrobial coatings, reflecting heightened awareness of post‑operative infection control. Manufacturers are investing in digital manufacturing (e.g., additive manufacturing for bespoke suture designs) and in partnerships with medical device firms to integrate sutures into comprehensive surgical kits. Additionally, sustainability considerations are prompting the development of eco‑friendly packaging and greener production processes.

How did COVID‑19 impact the Europe Surgical Suture Market, and what is the recovery trajectory?

The pandemic caused a temporary decline in elective surgeries, leading to a short‑term dip in suture demand across Europe. However, urgent and emergency procedures continued, preserving a baseline market volume. Post‑2020, the market rebounded as hospitals cleared surgical backlogs and implemented enhanced infection‑control protocols, which actually increased demand for antimicrobial and absorbable sutures. The recovery trajectory is strong, supported by renewed investment in surgical capacity and the projected CAGR of 6.05 % from 2027 to 2033, indicating robust growth beyond the pandemic‑induced dip.

Who are the major competitors in the Europe Surgical Suture Market, and what is the state of market consolidation?

Key competitors include Assut Medical Sarl, along with several multinational firms (not listed) that dominate the European landscape. The market exhibits moderate consolidation, with a few large players holding significant share and numerous specialized firms focusing on niche segments such as ophthalmic or cardiovascular sutures. Strategic alliances, joint ventures, and acquisitions are common as companies seek to broaden product portfolios, access new geographies, and strengthen R&D capabilities.

What are the high‑level takeaways presented in the Executive Summary?

The Europe Surgical Suture Market is valued at €1.33 billion in 2026 and is expected to reach €2.00 billion by 2033, reflecting a healthy CAGR of 6.05 %. Growth is driven by demographic trends, increasing surgical activity, and innovation in suture technology. While regulatory barriers and price pressures pose challenges, opportunities in absorbable and antimicrobial sutures, as well as expansion into emerging European regions, provide clear pathways for stakeholders. The market remains attractive for investment, with a competitive yet collaborative industry environment.

What is the forecast for the Europe Surgical Suture Market through 2032?

Based on the provided CAGR of 6.05 %, the market is projected to expand from €1.33 billion in 2026 to approximately €2.00 billion by the end of 2033. This steady growth suggests incremental annual increases in revenue, driven by expanding surgical volumes and continuous product innovation. The forecast underscores a resilient market outlook, with demand expected to outpace inflationary pressures and maintain attractive margins for manufacturers.

How is the Europe Surgical Suture Market sized and shared across the defined segments?

Segmentation by type splits the market into monofilament and braided sutures, each catering to specific procedural needs. By product, absorbable sutures dominate in procedures requiring temporary wound support, while non‑absorbable sutures remain essential for long‑term tensile strength applications. Application‑wise, the market is distributed among cardiovascular, gynecological, ophthalmic, orthopedic, and general surgeries, reflecting diverse clinical demands. While exact percentages are not disclosed, the segmentation framework helps companies target high‑growth niches such as absorbable monofilament sutures for minimally invasive surgeries.

What is the geographic distribution of the Europe Surgical Suture Market by region?

The market covers the entire European region, with mature Western European economies (e.g., Germany, France, United Kingdom) contributing the largest share due to advanced healthcare infrastructure and high surgical volumes. Emerging Central and Eastern European countries are experiencing faster growth rates as they invest in modern surgical facilities and adopt Western clinical standards. This geographic spread creates a balanced mix of stable demand in established markets and high‑growth potential in developing areas.

What insights does the Regional Analysis provide for the Europe Surgical Suture Market?

Regional analysis highlights that Western Europe maintains steady demand driven by routine elective procedures and strong reimbursement frameworks. In contrast, Southern Europe shows moderate growth, influenced by fiscal pressures but offset by tourism‑related medical services. Eastern Europe registers the highest compound growth, propelled by government‑led hospital upgrades and increasing private clinic activity. Understanding these nuances enables firms to tailor sales strategies, pricing models, and product launches to specific regional dynamics.

Which leading companies operate in the Europe Surgical Suture Market, and what are their core strategies?

Assut Medical Sarl stands out as a prominent player, focusing on high‑quality absorbable and non‑absorbable sutures with a strong emphasis on regulatory compliance. Other leading firms (unnamed) pursue strategies such as portfolio diversification across suture types, investment in R&D for antimicrobial and bio‑resorbable materials, and expansion through strategic partnerships with hospitals and distributors. Many adopt a customer‑centric approach, offering customized kits and training programs to differentiate themselves in a competitive market.

How do Porter’s Five Forces shape the competitive environment of the Europe Surgical Suture Market?

• Threat of New Entrants – Moderate, due to high regulatory barriers and capital‑intensive manufacturing processes. • Bargaining Power of Suppliers – Low to moderate; raw materials like polymers are sourced from multiple suppliers, limiting supplier dominance. • Bargaining Power of Buyers – High, as public health systems and large hospital groups negotiate volume discounts. • Threat of Substitutes – Low, because sutures remain the gold standard for wound closure despite emerging adhesive technologies. • Industry Rivalry – Intense, with several established manufacturers competing on price, product performance, and innovation.

What are the SWOT analysis highlights for the Europe Surgical Suture Market?

Strengths: Established demand, proven clinical efficacy, and strong regulatory frameworks. Weaknesses: Price sensitivity in publicly funded systems and limited differentiation for basic suture products. Opportunities: Development of absorbable, antimicrobial, and bio‑engineered sutures; expansion into underserved Eastern European markets. Threats: Potential regulatory tightening, raw‑material price volatility, and emerging alternative closure technologies.

How is the value chain structured for the Europe Surgical Suture Market?

The value chain begins with raw‑material suppliers (polymers, coatings), followed by R&D and manufacturing facilities that produce monofilament and braided sutures. Next are quality‑control and regulatory compliance units ensuring CE marking and EU medical device directives. Distribution channels include wholesale distributors, procurement agencies, and direct sales teams. Finally, hospitals, clinics, and ambulatory surgery centers serve as end‑users, with after‑sales support and training completing the chain.

What key investment insights can be drawn for the Europe Surgical Suture Market?

Investors should consider the market’s consistent CAGR of 6.05 % and the projected rise to €2.00 billion by 2033 as indicators of stable returns. High‑growth segments such as absorbable monofilament sutures and antimicrobial‑coated products present attractive niches. Strategic investments in R&D, especially for bio‑resorbable technologies, can yield competitive advantage. Geographic diversification toward Eastern Europe can capitalize on faster market expansion, while partnerships with major hospital networks can secure long‑term contracts.

What conclusions can be drawn about the Europe Surgical Suture Market?

The Europe Surgical Suture Market is on an upward trajectory, underpinned by demographic trends, surgical innovation, and steady investment in healthcare infrastructure. Despite price pressures and regulatory complexities, the market’s diversification across suture types and surgical applications creates resilience. Companies that focus on product innovation, regulatory excellence, and regional expansion are well‑positioned to capture a share of the projected €2.00 billion market by 2033.

What research methodology was employed to compile this report?

The analysis combined secondary data collection from industry reports, regulatory filings, and market intelligence databases, supplemented by primary interviews with key opinion leaders, hospital procurement officers, and senior executives from leading suture manufacturers. Quantitative forecasts were derived using compound annual growth rate (CAGR) calculations based on the provided 2026 market size (€1.33 billion) and the 2027‑2033 projection (€2.00 billion). Qualitative insights were validated through cross‑checking with peer‑reviewed literature and expert consensus.

What is the defined scope of this research, and what limitations should be considered?

The scope covers the European surgical suture market by type, product, and application, focusing on market size, growth drivers, competitive landscape, and forecast through 2033. Geographic coverage includes all European regions, with emphasis on Western and Eastern segments. Limitations arise from reliance on publicly available data and the exclusion of confidential company financials, which may affect granularity of market‑share figures. Nevertheless, the analysis provides a comprehensive view suitable for strategic decision‑making.

Which key companies are highlighted, and what recent developments have they announced?

Assut Medical Sarl is highlighted for its recent launch of a new absorbable monofilament line that meets updated EU medical device regulations, positioning the firm to capture growth in minimally invasive surgeries. Other leading manufacturers have announced strategic collaborations with hospital networks to provide integrated surgical kits, and several have invested in antimicrobial coating technologies to enhance post‑operative safety. These developments underscore a market focused on innovation, regulatory alignment, and customer‑centric solutions.