1. What is the Virtual Pipeline Systems Market Overview – definition, scope, and significance?

The Virtual Pipeline Systems market comprises mobile, high‑pressure trailer‑based solutions that transport compressed gases such as CNG and hydrogen without the need for fixed pipeline infrastructure. These systems include standard and towable trailers engineered to handle pressure ratings from less than 3,000 psi up to more than 5,000 psi. Their applications span industrial plants, commercial facilities, transportation fleets, and residential refueling stations. By enabling rapid, flexible delivery of clean fuels, virtual pipelines reduce capital expenditures, shorten project timelines, and support the transition to low‑carbon energy ecosystems, making them a critical enabler for emerging mobility and decarbonization strategies.

2. What are the main drivers, restraints, challenges, and opportunities in the Virtual Pipeline Systems Market?

Key drivers include rising demand for CNG and hydrogen as alternative fuels, government incentives for clean‑energy infrastructure, and the need for cost‑effective distribution in regions lacking permanent pipelines. Restraints stem from high initial trailer costs, regulatory complexities around high‑pressure transport, and limited awareness among potential end‑users. Challenges revolve around safety certification, supply‑chain constraints for composite materials, and competition from stationary storage solutions. Opportunities arise from expanding hydrogen refueling networks, integration with renewable‑based gas production, and the advent of digital monitoring platforms that enhance operational safety and efficiency.

3. What growth trends are shaping the Virtual Pipeline Systems Market today?

Current trends feature a shift toward composite‑based trailer construction, which offers weight reduction and higher pressure capabilities. The market is also witnessing convergence with telematics, where real‑time pressure, temperature, and location data are streamed to cloud dashboards for predictive maintenance. Another emerging trend is the bundling of virtual pipeline services with fuel‑as‑a‑service (FaaS) contracts, allowing customers to pay per kilogram of gas delivered rather than owning the equipment outright. Finally, cross‑industry collaborations—particularly between automotive OEMs and trailer manufacturers—are accelerating the deployment of CNG and hydrogen fleets.

4. How has COVID‑19 impacted the Virtual Pipeline Systems Market and what is the recovery trajectory?

The pandemic caused temporary delays in capital projects and disrupted supply chains for high‑strength composite fibers, leading to a short‑term dip in orders during 2020‑2021. However, the recovery was swift as governments prioritized clean‑energy projects to stimulate economies. By 2022, demand for CNG and hydrogen logistics rebounded, and the market returned to a growth path that is now projected to continue through 2032. The pandemic also accelerated digital adoption, prompting manufacturers to embed remote monitoring capabilities into new trailer designs.

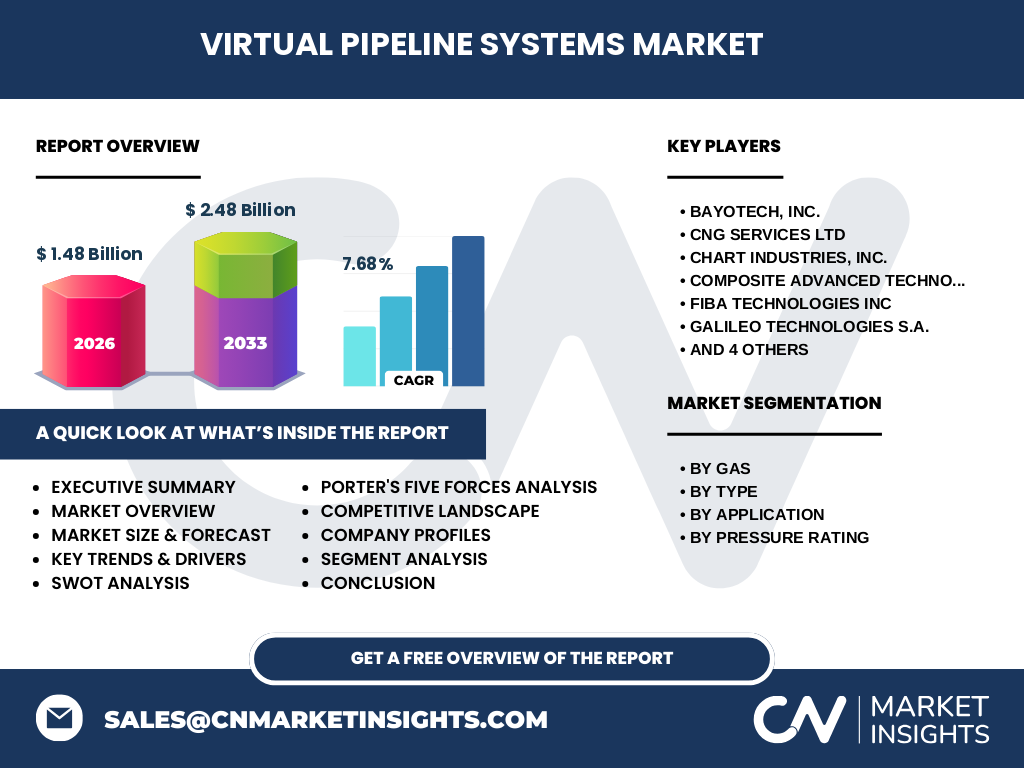

5. Who are the major competitors and what is the state of consolidation in the Virtual Pipeline Systems Market?

Leading players include Bayotech, Inc., CNG Services Ltd, Chart Industries, Inc., Composite Advanced Technologies, LLC, Fiba Technologies Inc, Galileo Technologies S.A., Hexagon Agility, Petroliam Nasional Berhad (PETRONAS), Quantum Fuel Systems LLC, and RAG Austria AG. The competitive landscape is characterized by strategic partnerships rather than heavy M&A activity, as companies focus on co‑development of advanced composites and joint‑venture distribution networks. Smaller niche firms are being acquired to strengthen technology portfolios, indicating a moderate but steady consolidation trend.

6. What are the high‑level findings of the Executive Summary for the Virtual Pipeline Systems Market?

The market was valued at USD 1.48 billion in 2026 and is expected to reach USD 2.48 billion by 2033, delivering a compound annual growth rate (CAGR) of 7.68 %. Growth is driven by expanding CNG and hydrogen use cases, heightened regulatory support, and innovations in trailer design and digital services. Segmentation shows strong adoption across industrial and transportation applications, with higher‑pressure (>5,000 psi) trailers gaining traction for hydrogen. Geographic analysis points to robust demand in North America, Europe, and fast‑growing Asian economies.

7. What are the market forecasts for the Virtual Pipeline Systems Market from 2025 to 2032?

Based on the provided CAGR of 7.68 %, the market will progress from a baseline of approximately USD 1.48 billion in 2026 to USD 2.48 billion by 2033. This trajectory suggests incremental annual expansions of roughly USD 140‑150 million, reflecting steady adoption of both CNG and hydrogen transport solutions across all defined applications and pressure categories.

8. How is the Virtual Pipeline Systems Market sized and shared by segmentation?

By gas type, the market is split between CNG and hydrogen, each served by a distinct set of trailers optimized for specific pressure ranges. By type, standard trailers dominate due to their proven reliability, while towable trailers capture niche segments where mobility is paramount. Application‑wise, industrial and transportation use the largest shares, followed by commercial and residential sectors. Pressure rating segmentation shows a balanced distribution: less than 3,000 psi serves lower‑pressure CNG, 3,001‑5,000 psi caters to mid‑range hydrogen, and more than 5,000 psi targets high‑performance hydrogen refueling.

9. What is the global market size and share of Virtual Pipeline Systems by region?

The global market aggregates to USD 1.48 billion in 2026, with North America accounting for the highest share owing to mature CNG fleets and early hydrogen pilots. Europe follows closely, driven by stringent emissions standards and strong policy backing for hydrogen infrastructure. Asia‑Pacific registers the fastest growth rate, propelled by rapid industrialization, government‑backed fuel‑switch programs, and expanding logistics networks that favor mobile pipeline solutions.

10. What are the detailed regional performance insights for the Virtual Pipeline Systems Market?

In North America, the market benefits from extensive natural‑gas vehicle fleets and a growing hydrogen‑fuel‑cell truck corridor in California. Europe’s progress is linked to EU targets for hydrogen adoption, with Germany and the Netherlands leading trailer deployments for industrial gas distribution. The Asia‑Pacific region, particularly China, India, and South Korea, is investing heavily in CNG public‑transport conversion and hydrogen fuel‑cell buses, creating a surge in demand for high‑pressure towable trailers. The Middle East and Africa show modest but steady interest, primarily for remote industrial sites where permanent pipelines are uneconomical.

11. Which companies lead the Virtual Pipeline Systems Market and what are their strategic approaches?

Bayotech, Inc. focuses on lightweight composite trailers with integrated IoT sensors. Chart Industries, Inc. leverages its cryogenic expertise to develop high‑pressure hydrogen carriers. PETRONAS utilizes its downstream network to offer bundled fuel‑delivery services. Quantum Fuel Systems LLC expands through partnerships with fleet operators, providing turnkey CNG solutions. RAG Austria AG emphasizes modular trailer designs that can be reconfigured for different gases, enhancing flexibility for multinational customers.

12. How does Porter’s Five Forces framework apply to the Virtual Pipeline Systems Market?

• Threat of new entrants: Moderate – high capital and certification barriers deter newcomers, but niche innovators can enter via specialized composites.

• Bargaining power of suppliers: High – limited suppliers of high‑strength composite materials increase dependence.

• Bargaining power of buyers: Moderate – large fleet operators can negotiate pricing, yet safety certifications limit switching.

• Threat of substitutes: Low – stationary storage tanks and permanent pipelines are alternatives but lack the flexibility of mobile systems.

• Competitive rivalry: High – ten major players compete on technology, service contracts, and geographic coverage.

13. What are the SWOT insights for the Virtual Pipeline Systems Market?

Strengths: Flexibility, lower capital outlay than fixed pipelines, and alignment with clean‑fuel policies.

Weaknesses: High upfront trailer cost and dependence on specialized material suppliers.

Opportunities: Expansion of hydrogen mobility, digital service platforms, and emerging markets lacking pipeline infrastructure.

Threats: Regulatory changes that increase safety compliance costs and potential competition from breakthrough stationary storage technologies.

14. How is the value chain structured for Virtual Pipeline Systems?

The value chain begins with raw material procurement (high‑strength composites, steel chassis), proceeds to engineering design and safety certification, followed by manufacturing and quality testing. Next, distributors integrate trailers into logistic services, offering fuel‑as‑a‑service contracts to end‑users. After‑sales support includes remote monitoring, maintenance, and trailer refurbishment, creating recurring revenue streams for manufacturers.

15. What key investment insights should stakeholders consider for the Virtual Pipeline Systems Market?

Investors should prioritize companies that have secured long‑term service agreements with major fuel distributors, as these contracts drive predictable cash flow. Funding projects that integrate digital telemetry can differentiate offerings and command premium pricing. Geographic diversification—particularly into Asia‑Pacific—offers higher growth potential. Finally, strategic stakes in composite material suppliers can mitigate supply‑chain risk and improve margins.

16. What are the concluding takeaways from the Virtual Pipeline Systems Market analysis?

The market is on a solid upward trajectory, underpinned by a 7.68 % CAGR and a ten‑year value increase of USD 1 billion. Flexibility, regulatory support, and the push for hydrogen fuel justify continued investment. While material costs and safety compliance remain challenges, technology advances and service‑based business models are creating resilient growth pathways.

17. How was the research for this report conducted?

Research combined primary interviews with industry experts, secondary data from company filings, regulatory publications, and market‑size modeling based on the provided 2026 baseline and forecasted 2027‑2033 figures. Trend validation used patent analysis, conference proceedings, and technology road‑maps, while regional insights were corroborated through government policy reviews and trade association reports.

18. What is the scope of this research and its limitations?

The scope covers global Virtual Pipeline Systems covering CNG and hydrogen, segmented by type, application, and pressure rating. It includes market size, forecast, competitive landscape, and strategic analyses. Limitations are confined to publicly available data; proprietary company financials and undisclosed regional sales figures were not incorporated.

19. Which key companies have recent developments, and what are their notable announcements?

Bayotech, Inc. launched a next‑generation lightweight trailer with embedded AI‑based leak detection. Chart Industries, Inc. announced a partnership with a European hydrogen fuel‑cell vehicle consortium to supply high‑pressure carriers. PETRONAS introduced a bundled fuel‑delivery service combining CNG refueling stations with mobile trailers for remote sites. Quantum Fuel Systems LLC unveiled a subscription‑based hydrogen‑as‑a‑service model targeting logistics fleets in North America. RAG Austria AG released a modular trailer platform that can be re‑configured within 24 hours for different gases, enhancing fleet versatility.