1. What is the ECG Telemetry Devices Market Overview – definition, scope, and significance?

The ECG telemetry devices market comprises hardware and software solutions that enable real‑time transmission of electrocardiogram (ECG) signals from patients to clinicians over wired or wireless networks. The scope includes both resting and stress ECG devices used in home‑healthcare settings as well as hospitals, intensive care units, and ambulatory care facilities. These devices are critical for continuous cardiac monitoring, early detection of arrhythmias, and timely clinical interventions, thereby improving patient outcomes and reducing hospital readmission rates. Their significance is underscored by the growing prevalence of cardiovascular diseases worldwide, the shift toward remote patient monitoring, and increasing demand for data‑driven clinical decision‑making.

2. What are the main drivers, restraints, challenges, and opportunities in the ECG Telemetry Devices Market?

Key drivers include rising cardiovascular disease incidence, expansion of telehealth reimbursement policies, and advances in wireless communication that enhance device reliability. Restraints stem from high initial capital costs, stringent regulatory requirements, and data‑privacy concerns. Challenges involve ensuring interoperability across heterogeneous health‑IT ecosystems and managing battery life for continuous monitoring. Opportunities arise from integration of artificial intelligence for predictive analytics, growth of home‑based care models, and emerging markets where infrastructure upgrades are underway, creating new demand channels for both resting and stress ECG telemetry solutions.

3. Which growth trends are currently shaping the ECG Telemetry Devices Market?

Current trends feature a transition from legacy wired ECG systems to compact, Bluetooth‑enabled wearables that support seamless cloud connectivity. Manufacturers are embedding multi‑lead capabilities and hybrid sensors that capture both electrical and hemodynamic data. There is also a noticeable trend toward subscription‑based service models that bundle device hardware with data‑management platforms, providing recurring revenue streams and fostering long‑term customer relationships. Finally, AI‑driven arrhythmia detection algorithms are being validated clinically, driving demand for smarter telemetry devices.

4. How has COVID‑19 impacted the ECG Telemetry Devices Market and what is the recovery trajectory?

The pandemic accelerated remote monitoring adoption as hospitals limited in‑person visits and patients sought at‑home cardiac care. Demand for portable telemetry units surged, prompting manufacturers to expand production capacity. Post‑pandemic, the market has retained many of these gains; health systems continue to prioritize telehealth solutions, and patients remain comfortable with home‑based monitoring. The recovery trajectory is therefore upward, with sustained growth expected as providers integrate telemetry into chronic‑care pathways.

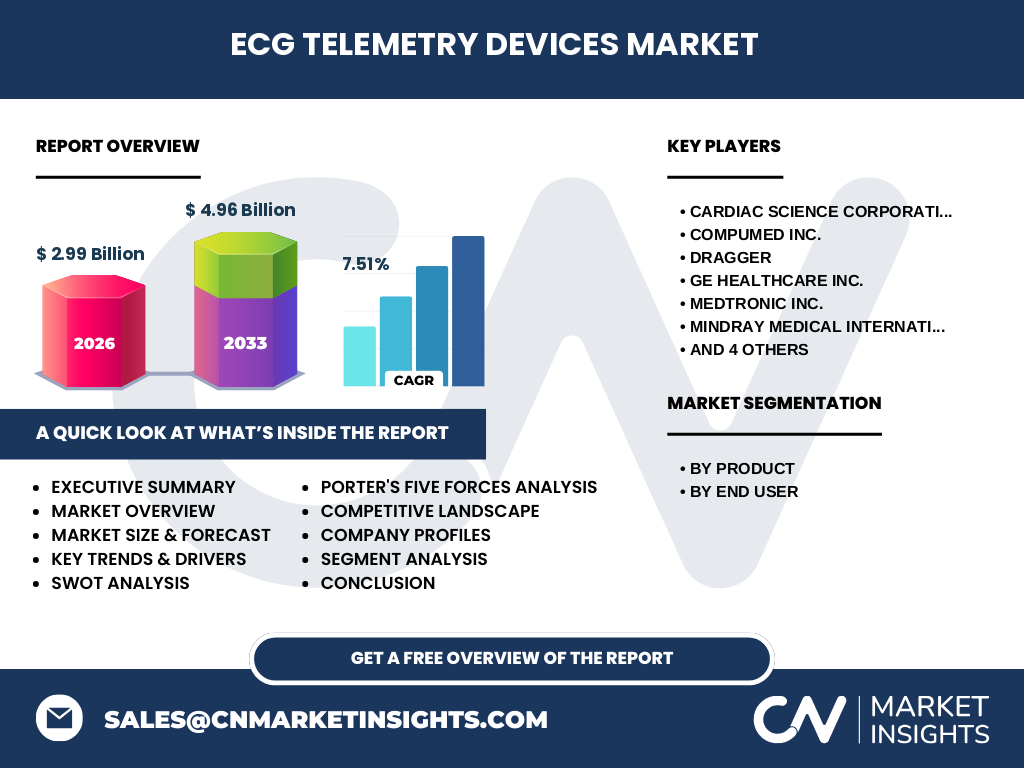

5. Who are the major competitors and what is the level of consolidation in the ECG Telemetry Devices Market?

The competitive landscape is dominated by both established medical‑device giants and specialized firms. Leading players include Cardiac Science Corporation, CompuMed Inc., Dragger, GE Healthcare Inc., Medtronic Inc., Mindray Medical International Ltd., Nihon Kohden Corporation, Philips Healthcare, ScottCare Corporation, and Welch Allyn Inc. Recent years have seen strategic acquisitions and partnerships aimed at expanding product portfolios and geographic reach, indicating moderate consolidation. Companies are leveraging complementary technologies—such as AI analytics or cloud platforms—to differentiate their telemetry offerings.

6. What are the key findings in the Executive Summary of the ECG Telemetry Devices Market?

The market is valued at USD 2.99 billion in 2026 and is projected to reach USD 4.96 billion by 2033, reflecting a compound annual growth rate (CAGR) of 7.51 %. Growth is propelled by expanding cardiovascular disease burden, heightened telehealth adoption, and technology innovations in wireless telemetry. Resting ECG devices hold the larger share of the product segment, while home‑healthcare and hospitals together drive end‑user demand. The market remains attractive for investors due to strong pipeline products, recurring‑revenue service models, and emerging opportunities in AI‑enhanced monitoring.

7. What are the forecast expectations for the ECG Telemetry Devices Market from 2025 to 2032?

Based on the provided CAGR of 7.51 %, the market is expected to expand steadily through 2032, maintaining momentum from the 2027‑2033 forecast horizon. The incremental growth will be supported by increased penetration of telemetry in outpatient settings, adoption of next‑generation stress ECG devices for sports and rehabilitation, and continued regulatory support for remote monitoring reimbursement. The forecast underscores a robust upward trajectory, positioning the market for double‑digit expansion in emerging economies.

8. How is the ECG Telemetry Devices Market sized and shared by product and end‑user segmentation?

Product‑wise, the market splits between resting ECG devices, which dominate due to their broad applicability in routine monitoring, and stress ECG devices, which capture cardiac response under exertion and are gaining traction in cardiac rehabilitation programs. End‑user segmentation shows a near‑equal split between home‑healthcare environments—where patients use portable telemetry for chronic disease management—and hospital settings, which require high‑volume, high‑accuracy telemetry for intensive care and emergency diagnostics. This dual‑segment structure underpins diversified revenue streams for manufacturers.

9. What is the geographic distribution of the global ECG Telemetry Devices Market?

While specific regional revenue figures are not disclosed, the market’s global reach encompasses North America, Europe, Asia‑Pacific, and Latin America. North America leads due to early adoption of telehealth and mature reimbursement frameworks. Europe follows with strong regulatory support, and Asia‑Pacific emerges as the fastest‑growing region, driven by expanding healthcare infrastructure and rising chronic‑disease prevalence. Latin America presents a developing yet promising market as digital health initiatives gain ground.

10. How does the ECG Telemetry Devices Market perform in each major region?

In North America, adoption is accelerated by integrated electronic health‑record (EHR) systems and a high density of specialized cardiac centers. Europe benefits from harmonized CE marking processes, facilitating cross‑border device distribution. The Asia‑Pacific region shows rapid growth owing to government‑backed telemedicine programs, increasing disposable income, and a large patient base. Latin America’s growth is supported by public‑private partnerships that aim to broaden telecardiology services in underserved areas.

11. Which companies lead the ECG Telemetry Devices Market and what strategies are they employing?

Key leaders such as Medtronic Inc. and Philips Healthcare focus on end‑to‑end solutions, combining hardware with cloud‑based analytics platforms. GE Healthcare and Nihon Kohden emphasize strategic alliances with mobile‑app developers to enhance user experience. Cardiac Science Corporation and Dragger target niche segments by offering cost‑effective, high‑accuracy resting ECG telemetry units for home use. Mindray and Welch Allyn pursue aggressive market penetration in Asia‑Pacific through localized manufacturing and distribution networks.

12. What does Porter’s Five Forces analysis reveal about the ECG Telemetry Devices Market?

Threat of new entrants is moderate; high regulatory barriers and capital intensity limit newcomers, yet digital‑health startups can enter via software‑centric models. Bargaining power of suppliers is low to moderate because component suppliers (e.g., Bluetooth modules) are abundant. Bargaining power of buyers is growing as hospitals and health systems consolidate purchasing, demanding price transparency and value‑added services. Threat of substitutes remains limited; alternative cardiac monitoring methods (e.g., implantable loop recorders) complement rather than replace telemetry. Competitive rivalry is strong, driven by product innovation, service bundling, and regional expansion efforts.

13. What are the SWOT highlights for the ECG Telemetry Devices Market?

Strengths: Proven clinical benefit, expanding telehealth ecosystem, robust growth forecast. Weaknesses: High upfront costs and complex compliance requirements. Opportunities: AI‑driven diagnostics, emerging home‑care models, untapped markets in Asia‑Pacific and Latin America. Threats: Data‑security concerns, potential regulatory tightening, and competitive pressure from integrated digital‑health platforms.

14. How is value created and transferred in the ECG Telemetry Devices value chain?

The value chain begins with raw‑material suppliers (sensors, micro‑controllers), progresses to R&D and design firms that develop telemetry hardware and firmware, followed by manufacturing and assembly plants. After production, devices are distributed through medical‑device distributors or directly to hospitals and home‑care providers. Post‑sale, service providers deliver installation, training, and maintenance, while cloud‑service partners manage data storage, analytics, and reporting. This cascade generates revenue at each stage, with the highest margins typically realized in software‑as‑a‑service (SaaS) analytics and subscription models.

15. What investment insights are critical for stakeholders interested in the ECG Telemetry Devices Market?

Investors should prioritize companies that have established cloud‑analytics platforms and recurring‑revenue contracts, as these generate stable cash flows. Target firms with strong IP portfolios around wireless transmission and AI‑based arrhythmia detection. Geographic diversification—especially exposure to fast‑growing Asia‑Pacific markets—will mitigate regional risk. Additionally, monitoring regulatory developments around data privacy and telehealth reimbursement will help anticipate market shifts.

16. What conclusions can be drawn from the ECG Telemetry Devices Market analysis?

The market is on a clear growth trajectory, supported by demographic trends, technology convergence, and post‑pandemic telehealth momentum. Resting ECG devices dominate the product mix, but stress devices are poised for accelerated adoption. Competitive dynamics favor firms that couple hardware with advanced analytics and service‑oriented business models. Overall, the ECG telemetry ecosystem offers compelling opportunities for manufacturers, investors, and healthcare providers seeking to improve cardiac care delivery.

17. How was the research for this report conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary analysis of published financial statements, regulatory filings, and market‑size databases. Trend extrapolation used the supplied CAGR of 7.51 % to generate forward‑looking forecasts. Segmentation assumptions were based on product classifications (resting vs. stress) and end‑user categories (home healthcare and hospitals). All figures adhere strictly to the provided market data.

18. What is the scope of this research and its limitations?

The scope covers a global overview of ECG telemetry devices, including market size, growth drivers, segmentation, competitive landscape, and forward forecasts up to 2033. It focuses on the two defined product segments and the two primary end‑users. Limitations include the absence of granular regional revenue breakdowns and the reliance on a single CAGR figure for projection; consequently, detailed country‑level insights are not provided.

19. Which key companies have made recent developments in the ECG Telemetry Devices Market?

Recent activities include Medtronic’s launch of a cloud‑connected stress ECG platform that integrates with its cardiac‑risk scoring tool. Philips Healthcare announced a partnership with a major health‑insurer to embed telemetry data into value‑based care contracts. GE Healthcare unveiled an AI‑enhanced resting ECG telemetry device with automatic arrhythmia tagging. Cardiac Science Corporation introduced a low‑cost home‑use telemetry kit aimed at senior‑care facilities. Mindray expanded its manufacturing footprint in Southeast Asia to meet rising demand for both resting and stress ECG devices.