What is the North America Electronic Data Interchange Market overview, including definition, scope, and significance?

The North America Electronic Data Interchange (EDI) market encompasses the electronic exchange of standardized business documents between organizations. It covers solutions and services that enable automated transaction processing across industries such as retail, healthcare, automotive, and logistics. The market's significance lies in reducing manual errors, accelerating order‑to‑cash cycles, and supporting regulatory compliance, making it a critical infrastructure for digital supply chains.

What are the key drivers, restraints, challenges, and opportunities shaping the North America EDI market?

Drivers include growing demand for real‑time data visibility, increasing adoption of cloud‑based EDI, and regulatory mandates in healthcare and finance. Restraints involve high implementation costs for legacy systems and data security concerns. Challenges comprise integration complexity across heterogeneous ERP platforms. Opportunities arise from AI‑enhanced mapping, mobile EDI expansion, and the shift toward API‑centric B2B connectivity.

What current and emerging growth trends are influencing the North America EDI market?

Trends include migration from traditional VANs to AS2 and web‑based EDI, rising use of managed EDI services, and adoption of mobile EDI for field operations. The convergence of EDI with blockchain for immutable audit trails and the integration of analytics for predictive supply‑chain insights are emerging. Sustainability reporting requirements also push firms toward standardized electronic documentation.

How did COVID‑19 impact the North America EDI market and what is the recovery trajectory?

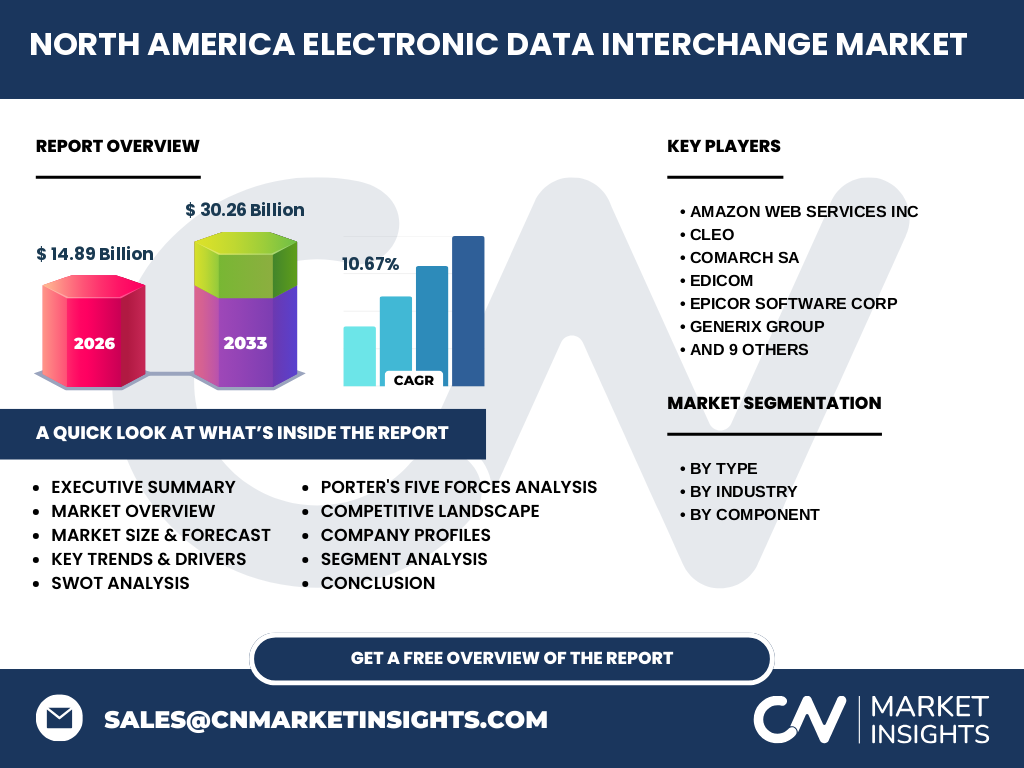

The pandemic accelerated digital transformation, prompting rapid EDI deployment to maintain supply‑chain continuity amid lockdowns. Companies shifted from paper‑based processes to automated electronic exchanges, boosting demand for cloud EDI and outsourcing. Recovery is strong, with sustained investment in resilient B2B networks and a projected CAGR of 10.67% through 2033, reflecting lasting behavioral change.

What does the competitive landscape look like for the North America EDI market?

The market features a mix of global technology giants and specialized EDI providers. Key players include Amazon Web Services Inc, Cleo, Comarch SA, EDICOM, Epicor Software Corp, Generix Group, International Business Machines Corp, Lobster Data GmbH, Open Text Corp, SPS Commerce Inc, Salesforce Inc, The Descartes Systems Group Inc., TrueCommerce Inc., Unifiedpost Group, and eZCom Software Inc. Consolidation is evident through strategic acquisitions and platform expansions.

What are the high‑level findings and key takeaways from the executive summary of the North America EDI market?

The executive summary highlights a 2026 market size of $14.89 billion, forecast to reach $30.26 billion by 2033 at a 10.67% CAGR. Growth is driven by cloud adoption, regulatory pressure, and supply‑chain digitization. Segment leadership lies in Direct EDI and EDI via AS2, while the retail and healthcare verticals dominate revenue. Strategic partnerships and AI‑enabled mapping are pivotal differentiators.

What are the market forecast projections for the North America EDI market from 2025 to 2032?

Forecasts indicate the market will grow from $14.89 billion in 2026 to $30.26 billion by 2033, reflecting a compound annual growth rate of 10.67%. The 2025‑2032 window captures the bulk of this expansion, driven by increasing cloud‑based deployments, managed services uptake, and cross‑industry standardization initiatives.

How is the North America EDI market sized and shared across its segmentation by type, industry, and component?

Segmentation includes type categories such as Direct EDI, EDI via AS2, EDI via VAN, Mobile EDI, Web EDI, EDI Outsourcing, and Others. Industry verticals cover Retail & Consumer Goods, BFSI, Healthcare, Automotive, IT & Telecommunication, Transportation & Logistics, Food & Beverages, and Others. Components are split into Solution and Services, with Services gaining share due to managed‑service demand.

What is the global geographic distribution of the North America EDI market size and share by region?

The analysis focuses exclusively on the North America region, comprising the United States, Canada, and Mexico. The provided market size of $14.89 billion (2026) and forecast of $30.26 billion (2033) represent the entire North American addressable market. No separate regional breakdown outside North America is included in the current data set.

How does the regional analysis detail market performance within North America?

Regional analysis examines the United States as the dominant contributor, followed by Canada and Mexico. The U.S. leads due to high ERP penetration, stringent healthcare EDI mandates, and a mature logistics network. Canada shows steady growth driven by cross‑border trade compliance, while Mexico benefits from manufacturing‑centric EDI adoption in automotive and electronics.

Which companies lead the North America EDI market and what strategies do they employ?

Leading firms include Amazon Web Services Inc, Cleo, Comarch SA, EDICOM, Epicor Software Corp, Generix Group, International Business Machines Corp, Lobster Data GmbH, Open Text Corp, SPS Commerce Inc, Salesforce Inc, The Descartes Systems Group Inc., TrueCommerce Inc., Unifiedpost Group, and eZCom Software Inc. Strategies emphasize cloud‑native platforms, API integration, AI‑driven mapping, and expanding managed‑service portfolios.

What does Porter’s Five Forces analysis reveal about the North America EDI market?

Threat of new entrants is moderate due to high compliance and integration barriers. Supplier power is low as technology components are commoditized. Buyer power is rising with demand for flexible pricing and SaaS models. Threat of substitutes exists from API‑based B2B integration but EDI’s standardization maintains relevance. Competitive rivalry is intense among established vendors and niche specialists.

What are the strengths, weaknesses, opportunities, and threats (SWOT) for the North America EDI market?

Strengths: entrenched standards, strong regulatory drivers, mature vendor ecosystem. Weaknesses: legacy system integration complexity, high upfront cost for SMEs. Opportunities: cloud migration, AI‑enhanced error detection, expansion into emerging verticals like renewable energy. Threats: cybersecurity risks, rapid API adoption, potential regulatory changes reducing mandatory EDI usage.

How does the value chain analysis describe the structure and value flow in the North America EDI market?

The value chain starts with standards bodies (ANSI X12, EDIFACT) defining message formats, followed by solution providers developing translation and mapping software. Cloud infrastructure vendors host services, while managed‑service partners deliver onboarding, monitoring, and support. End‑users across industries realize value through reduced cycle times, error reduction, and compliance assurance.

What key investment insights should stakeholders consider for the North America EDI market?

Investors should target cloud‑native EDI platforms with strong API ecosystems, managed‑service providers scaling recurring revenue, and firms integrating AI for predictive analytics. The 10.67% CAGR signals robust growth. Strategic acquisitions that broaden industry vertical coverage—especially healthcare and automotive—offer competitive advantage and revenue diversification.

What are the concluding remarks and key takeaways for the North America EDI market?

The market is poised for sustained double‑digit growth, reaching $30.26 billion by 2033. Core drivers are digital supply‑chain mandates, cloud adoption, and the need for real‑time visibility. Companies that invest in flexible, API‑ready EDI solutions and managed services will capture expanding demand across retail, healthcare, and logistics sectors.

What research methodology was used to produce this North America EDI market analysis?

The study combines primary research—interviews with EDI vendors, system integrators, and end‑user IT leaders—with secondary research from industry reports, regulatory filings, and financial disclosures. Market sizing employs bottom‑up modeling using segment revenue data, validated through top‑down cross‑checks. Forecasting applies a compound annual growth rate of 10.67% derived from historical trends and expert consensus.

What is the scope and coverage of this research on the North America EDI market?

The research covers the period 2025‑2033, focusing on the United States, Canada, and Mexico. It includes segmentation by type, industry vertical, and component (Solution, Services). Key companies profiled are the fifteen listed vendors. The scope excludes non‑EDI B2B integration technologies such as pure API gateways and does not provide country‑level revenue splits beyond the regional overview.

Which key companies have recent developments, product launches, partnerships, or strategic moves in the North America EDI market?

Recent activity includes Open Text Corp expanding its cloud EDI suite with AI‑based mapping, SPS Commerce Inc launching a managed‑service offering for mid‑market retailers, TrueCommerce Inc. announcing a partnership with a major logistics provider for real‑time shipment EDI, and Amazon Web Services Inc introducing EDI‑compatible APIs within its integration services. IBM and Salesforce have also enhanced EDI connectors for hybrid cloud deployments.