What is the definition, scope, and significance of the North America Video Inspection Equipment Market?

The North America Video Inspection Equipment Market encompasses specialized devices and systems designed for visual examination of infrastructure, pipelines, and industrial assets across the United States, Canada, and Mexico. These systems include cameras, transporters, monitors, recorders, and software solutions used for non-destructive testing and condition assessment. The market serves critical end-user segments including oil & gas, manufacturing & construction, food & beverages, and chemicals & pharmaceuticals. Its significance lies in enabling preventive maintenance, regulatory compliance, and operational safety across aging infrastructure networks, particularly in drain & sewer, electrical conduit & ducts, and pipeline applications where visual access is limited or hazardous.

What are the key drivers, restraints, challenges, and opportunities shaping the North America Video Inspection Equipment Market?

Key drivers include aging infrastructure requiring regular inspection, stringent regulatory mandates for pipeline integrity, and growing adoption of preventive maintenance strategies across industrial sectors. The market benefits from technological advancements in camera resolution, wireless connectivity, and AI-powered defect detection software. Restraints involve high initial equipment costs and the need for skilled operators. Challenges include interoperability issues between legacy systems and new digital platforms, as well as harsh operating environments affecting equipment durability. Opportunities emerge from increasing infrastructure spending bills, rising demand for trenchless inspection technologies, and expansion into food & beverage and pharmaceutical processing facility inspections where hygiene standards mandate video documentation.

What current and emerging trends are shaping the North America Video Inspection Equipment Market?

The market is witnessing a shift toward portable, ruggedized inspection systems with high-definition imaging capabilities and cloud-based data management. Integration of artificial intelligence for automated defect recognition and classification is gaining traction, reducing operator fatigue and improving inspection accuracy. Wireless and battery-operated transporters are replacing tethered systems for greater maneuverability in complex pipe networks. There is growing demand for multi-sensor platforms combining video with laser profiling, sonar, and gas detection. Subscription-based software models and remote inspection capabilities accelerated by pandemic-driven operational changes are reshaping business models. Sustainability focus drives development of energy-efficient LED lighting and recyclable component designs.

How did COVID-19 impact the North America Video Inspection Equipment Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed non-essential infrastructure inspections during 2020 lockdowns, causing temporary project deferrals across municipal and industrial sectors. However, the crisis accelerated adoption of remote inspection technologies and digital collaboration tools, allowing operators to conduct assessments with minimal on-site personnel. This catalyzed long-term demand for connected, cloud-enabled inspection platforms. Recovery has been robust, supported by stimulus-funded infrastructure programs and renewed emphasis on critical infrastructure resilience. The market demonstrated resilience with essential service classification for utility inspections, and the post-pandemic period has seen increased investment in automation to mitigate future workforce disruptions.

What is the competitive landscape and level of market consolidation in the North America Video Inspection Equipment Market?

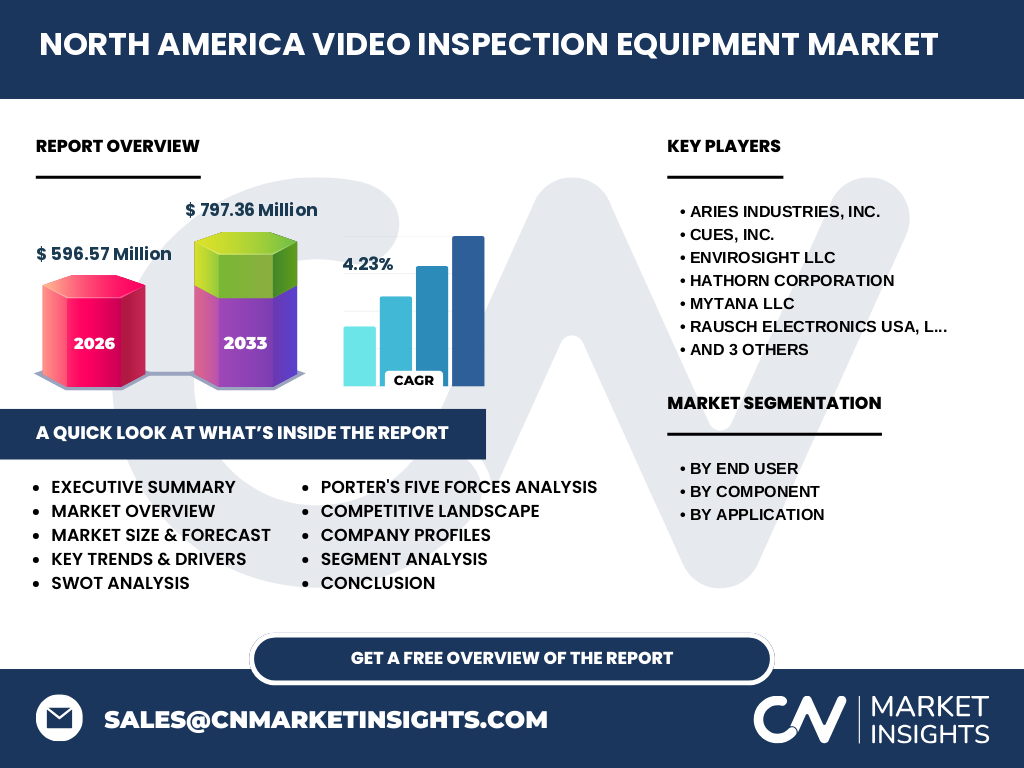

The market features a mix of established specialists and diversified industrial technology providers. Key players include Aries Industries, Inc., CUES, Inc., Envirosight LLC, Hathorn Corporation, MyTana LLC, Rausch Electronics USA, LLC., Subsite Electronics, TechCorr, and Vivax-Metrotech Corporation. Competition centers on product durability, imaging quality, software integration, and after-sales support networks. The market shows moderate consolidation with several players pursuing strategic acquisitions to expand product portfolios and geographic reach. Differentiation occurs through application-specific solutions for oil & gas versus municipal sectors, and through proprietary software ecosystems that create customer retention. Regional distributors play a significant role in market access and service delivery.

What are the key findings and high-level overview of the North America Video Inspection Equipment Market?

The North America Video Inspection Equipment Market is projected to reach $596.57 million in 2026, growing to $797.36 million by 2033 at a CAGR of 4.23%. This growth reflects sustained infrastructure investment, regulatory compliance requirements, and technological advancement across inspection applications. The market is segmented by end user (oil & gas, manufacturing & construction, food & beverages, chemicals & pharmaceuticals), component (cameras, transporters, monitors & recorders, software), and application (drain & sewer, electrical conduit & ducts, pipeline). Key players including Aries Industries, CUES, Envirosight, and Vivax-Metrotech drive innovation in ruggedized, connected inspection systems. The market demonstrates resilience through economic cycles given the essential nature of infrastructure monitoring.

What are the market projections for the North America Video Inspection Equipment Market for the 2025-2032 period?

The market is forecast to expand from $596.57 million in 2026 to $797.36 million by 2033, representing a compound annual growth rate of 4.23% over the forecast period. This projection accounts for continued infrastructure modernization programs, particularly in pipeline integrity management and municipal sewer rehabilitation. Growth will be supported by software and analytics segments outpacing hardware as digital transformation accelerates. The oil & gas and manufacturing & construction end-user segments are expected to maintain dominant revenue shares, while food & beverages and chemicals & pharmaceuticals show accelerating adoption driven by hygiene and safety compliance. Camera and transporter components will see steady demand from fleet replacement and expansion cycles.

How is the North America Video Inspection Equipment Market sized and shared across segmentation categories?

Market segmentation reveals distinct revenue distributions across end users, components, and applications. The oil & gas and manufacturing & construction sectors represent the largest end-user segments due to extensive pipeline networks and regulatory inspection mandates. Food & beverages and chemicals & pharmaceuticals are growing segments driven by sanitary design requirements and contamination prevention. By component, cameras and transporters constitute the core hardware revenue base, while monitors & recorders and software represent higher-margin, recurring revenue opportunities. In applications, drain & sewer inspection leads municipal spending, pipeline inspection dominates oil & gas investment, and electrical conduit & ducts serves utility and construction markets. Exact segment percentages require detailed subscription data.

What is the geographic distribution of the Global North America Video Inspection Equipment Market by region?

The North America Video Inspection Equipment Market specifically covers the United States, Canada, and Mexico as a defined regional segment within the global inspection equipment landscape. The United States represents the largest national market driven by extensive aging infrastructure, stringent PHMSA pipeline regulations, and significant municipal consent decree programs for sewer rehabilitation. Canada follows with substantial oil & gas pipeline inspection requirements and municipal infrastructure programs. Mexico shows growing demand from manufacturing expansion and energy sector development. The regional market size of $596.57 million (2026) reflects the combined demand across these three countries, with the U.S. commanding the predominant share.

How does the North America Video Inspection Equipment Market perform across detailed regional analysis?

Regional performance varies by regulatory environment, infrastructure age, and industrial composition. The U.S. market benefits from federal infrastructure funding, EPA consent decrees driving sewer inspection, and PHMSA integrity management rules for pipelines. Canada's market is propelled by cross-border pipeline integrity requirements and harsh climate necessitating robust equipment. Mexico's growth stems from automotive and aerospace manufacturing expansion requiring facility inspection, plus energy reform opening pipeline opportunities. Urban centers across all three countries show concentrated demand for drain & sewer and electrical conduit inspection. Rural and remote regions drive demand for long-range pipeline inspection capabilities. Each country's standards and certification requirements influence product specifications and market entry strategies.

Who are the leading companies in the North America Video Inspection Equipment Market and what are their strategies?

Leading companies include Aries Industries, Inc., CUES, Inc., Envirosight LLC, Hathorn Corporation, MyTana LLC, Rausch Electronics USA, LLC., Subsite Electronics, TechCorr, and Vivax-Metrotech Corporation. These players compete through product innovation in camera resolution, transporter maneuverability, and software analytics. Strategies include developing application-specific platforms for oil & gas versus municipal markets, building proprietary software ecosystems for data management and reporting, expanding service networks for rapid support, and pursuing strategic acquisitions to broaden product portfolios. Companies differentiate through ruggedization for harsh environments, wireless connectivity for remote operations, and integration with GIS and asset management systems. Customer training and certification programs create switching costs and brand loyalty.

What does Porter's Five Forces Analysis reveal about the North America Video Inspection Equipment Market?

Porter's Five Forces analysis indicates moderate competitive rivalry among established specialists with differentiated product portfolios. Supplier power is moderate, with key components like image sensors and ruggedized housings sourced from multiple electronics suppliers, though specialized transporters have fewer sources. Buyer power is significant for large municipal and oil & gas accounts that purchase fleet quantities and demand service contracts, but fragmented for smaller contractors. Threat of substitutes remains low as video inspection is the primary non-destructive method for internal pipeline and conduit assessment, though robotics and sensor-only systems offer niche alternatives. Threat of new entrants is moderated by high R&D requirements, regulatory certifications, established distribution relationships, and the need for proven field reliability track records.

What are the strengths, weaknesses, opportunities, and threats in the SWOT Analysis of the North America Video Inspection Equipment Market?

Strengths include essential service classification, recurring revenue from software and services, high barriers to entry, and strong regulatory tailwinds. Weaknesses involve high capital expenditure for customers, skilled labor dependency for operation and interpretation, and equipment vulnerability in harsh environments. Opportunities encompass infrastructure stimulus funding, AI-driven analytics adoption, expansion into food & pharmaceutical sanitary inspection, and trenchless technology integration. Threats include economic cyclicality affecting municipal budgets, potential regulatory rollback, competition from rental markets reducing capital sales, and cybersecurity risks in connected inspection platforms. The market's resilience stems from non-discretionary inspection mandates, while growth depends on technology adoption rates across conservative industrial sectors.

How does the value chain analysis describe the North America Video Inspection Equipment Market structure and value flow?

The value chain begins with component suppliers providing image sensors, optics, ruggedized enclosures, crawler motors, and display panels. Manufacturers like Aries Industries, CUES, Envirosight, and others integrate these into complete inspection systems with proprietary software. Value addition occurs through system engineering for specific applications (pipeline, sewer, conduit), software development for data acquisition and analysis, and ruggedization testing. Distribution flows through specialized industrial distributors, manufacturer direct sales, and rental companies. End users in oil & gas, municipal, construction, and industrial sectors deploy systems for inspection services, often through specialized contractors. Service providers add value through inspection execution, data interpretation, and compliance reporting. Feedback loops from field performance drive product iteration.

What are the key investment insights and strategic recommendations for the North America Video Inspection Equipment Market?

Investment opportunities center on software analytics platforms with AI-powered defect detection, which offer higher margins and recurring revenue versus hardware. Companies developing integrated multi-sensor platforms (video, laser, sonar) address growing demand for comprehensive condition assessment. The rental and inspection-as-a-service model lowers customer entry barriers and creates annuity streams. Geographic expansion into Mexico's growing manufacturing and energy sectors presents untapped potential. Strategic acquisitions of niche technology providers (wireless transmission, cloud analytics) can accelerate product roadmaps. Investors should monitor infrastructure bill implementation timelines and regulatory developments in pipeline integrity management. ESG-aligned investments in equipment enabling methane leak detection and water conservation align with sustainability mandates.

What are the summary conclusions and key takeaways for the North America Video Inspection Equipment Market?

The North America Video Inspection Equipment Market demonstrates steady growth at 4.23% CAGR, reaching $797.36 million by 2033 from $596.57 million in 2026. This reflects the non-discretionary nature of infrastructure inspection driven by regulatory compliance, aging asset management, and safety imperatives. The market's segmentation across oil & gas, manufacturing, food & beverage, and pharmaceutical end users provides diversification. Technology trends toward AI analytics, wireless connectivity, and cloud-based data management are reshaping competitive dynamics. Key players including Aries Industries, CUES, Envirosight, and Vivax-Metrotech are well-positioned through established distribution and service networks. The essential service designation ensures resilience, while infrastructure investment cycles provide growth catalysts.

What research methodology was used to conduct this analysis of the North America Video Inspection Equipment Market?

The research employs a comprehensive methodology combining primary and secondary research approaches. Primary research includes interviews with industry executives, product managers, distributors, and end users across oil & gas, municipal, and industrial sectors. Secondary research encompasses company financial reports, regulatory filings, industry association publications, government infrastructure databases, and technical literature. Market sizing utilizes bottom-up aggregation from key player revenues and top-down validation through infrastructure spending data and installed base analysis. Forecasting incorporates driver-based modeling with macroeconomic indicators, regulatory timelines, and technology adoption curves. Data triangulation across multiple sources ensures accuracy. The analysis covers the 2025-2033 period with 2026 as the base year for market size estimation.

What is the research scope and what limitations apply to this North America Video Inspection Equipment Market analysis?

The research scope covers the North America Video Inspection Equipment Market across the United States, Canada, and Mexico for the period 2025-2033. Segmentation analysis includes end users (oil & gas, manufacturing & construction, food & beverages, chemicals & pharmaceuticals), components (cameras, transporters, monitors & recorders, software), and applications (drain & sewer, electrical conduit & ducts, pipeline). Key companies profiled include Aries Industries, CUES, Envirosight, Hathorn, MyTana, Rausch Electronics, Subsite Electronics, TechCorr, and Vivax-Metrotech. The analysis focuses on equipment sales, software licensing, and associated services. Limitations include exclusion of rental market sizing as a separate segment, reliance on publicly available financial data for private companies, and forecasting uncertainty from policy changes and macroeconomic volatility.

Who are the key companies in the North America Video Inspection Equipment Market and what recent developments have they announced?

The key companies shaping the market include Aries Industries, Inc., CUES, Inc., Envirosight LLC, Hathorn Corporation, MyTana LLC, Rausch Electronics USA, LLC., Subsite Electronics, TechCorr, and Vivax-Metrotech Corporation. Recent industry developments reflect a focus on digital transformation: several players have launched cloud-based inspection data platforms with AI-assisted defect coding, reducing reporting time. Wireless transporter systems with extended range have been introduced for long-distance pipeline applications. Strategic partnerships between hardware manufacturers and analytics software providers are creating integrated solutions. Companies are expanding service networks in Mexico to support growing manufacturing inspection demand. Product launches emphasize ruggedized designs for hydrogen-ready pipeline inspection and sanitary-certified cameras for food & beverage applications. Acquisition activity continues to consolidate complementary technology portfolios.