What is the definition, scope, and significance of the Data Center Generator Market?

The Data Center Generator Market encompasses the dedicated backup power generation systems engineered to secure continuous power to critical IT operations during main grid failures. The scope of this market includes system configurations classified by Tier (Tier 1 and 2, Tier 3, Tier 4), Capacity (Below 1 MW, 1-2 MW, Greater than 2 MW), and Product Type (Diesel, Natural Gas). The significance of this market is exceptionally high, as data center operators require ultra-reliable power systems to maintain strict operational continuity and prevent catastrophic financial losses associated with network downtime.

What are the primary drivers, restraints, challenges, and opportunities in the Data Center Generator Market?

The primary driver of the market is the massive global acceleration of cloud services, digital platforms, and enterprise data requirements. However, strict environmental regulations governing carbon emissions from large-capacity power sources represent a notable restraint. The primary industry challenge is to balance critical power availability with green energy targets, while substantial opportunities lie in the adoption of clean-burning alternative fuels and high-efficiency hybrid backup technologies.

What are the current and emerging growth trends shaping the Data Center Generator Market?

A major emerging trend in the market is the rapid deployment of high-capacity systems, specifically units of Greater than 2 MW, to meet the massive power demands of hyperscale facilities. Additionally, there is a visible transition toward environmentally sustainable power backup setups, driving the growth of natural gas generators. Operators are also increasingly leveraging smart monitoring technologies to enable real-time predictive maintenance.

How did the COVID-19 pandemic affect the Data Center Generator Market, and what is its recovery trajectory?

The COVID-19 pandemic acted as an accelerator for the digital infrastructure market, as remote work and online services created an urgent need for data center capacity. While raw material shortages and logistical disruptions initially hindered generator manufacturing, the industry quickly entered a strong recovery trajectory. This recovery continues to be fueled by sustained investments in highly reliable Tier 3 and Tier 4 digital facilities.

What is the overall competitive landscape of the Data Center Generator Market?

The market exhibits a competitive and moderately consolidated structure led by major global manufacturing entities. Competition is driven by continuous innovations in product fuel efficiency, emission standards, noise reduction, and startup reliability. Leading competitors focus on securing large supply agreements with global hyperscale and colocation providers, supported by extensive post-sale maintenance networks.

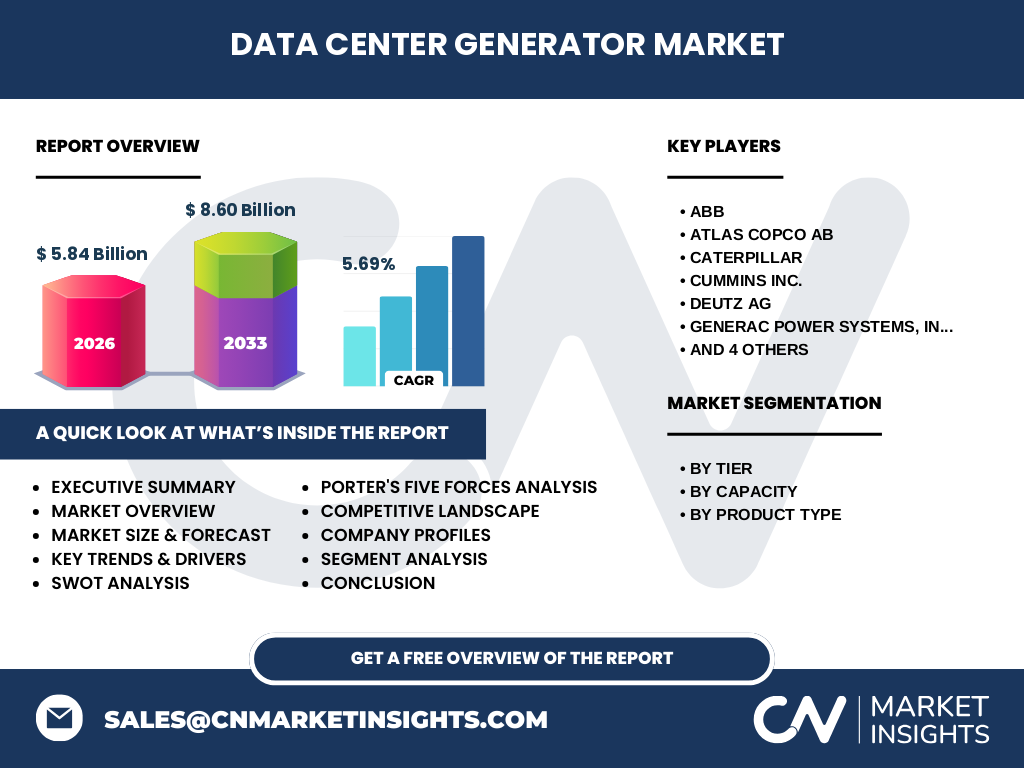

Can you provide an executive summary of the Data Center Generator Market?

The Data Center Generator Market is on a robust expansion path driven by the global wave of digitalization. The market is valued at 5.84 Billion in 2026 and is projected to reach 8.60 Billion by the end of 2033, expanding at a steady CAGR of 5.69%. The ongoing expansion of Tier 3 and Tier 4 data storage complexes is central to this steady growth, positioning backup power as an indispensable infrastructure component.

What is the growth forecast for the Data Center Generator Market for the 2027 to 2033 period?

The global Data Center Generator Market is forecast to grow from its baseline of 5.84 Billion in 2026 to a projected value of 8.60 Billion by 2033. This forecast reflects a steady compound annual growth rate (CAGR of 5.69%). This growth is supported by rising demand for robust, mission-critical power systems designed to handle the load requirements of modern server farms.

How is the Data Center Generator Market segmented, and what are the key dynamics?

The market is segmented By Tier (Tier 1 and 2, Tier 3, Tier 4); By Capacity (Below 1 MW, 1-2 MW, Greater than 2 MW); and By Product Type (Diesel, Natural Gas). Tier 3 and Tier 4 facilities represent highly critical segments due to their strict uptime regulations, while high-capacity units (Greater than 2 MW) are increasingly preferred to support dense server architectures.

What is the global distribution of size and share for the Data Center Generator Market by region?

The geographical distribution of the market is heavily tied to the concentration of major data networks and tech hubs globally. Regions with extensive cloud infrastructure and major corporate headquarters hold a significant share of the market. Demand is further influenced by local grid reliability and regional regulatory frameworks regarding backup energy emissions.

What does a detailed regional analysis of the Data Center Generator Market reveal?

Regional analysis shows that industrial regions characterized by rapid cloud adoption exhibit strong demand for high-capacity backup systems. In areas with strict carbon mandates, there is a clear strategic push toward natural gas generators. Conversely, regions experiencing rapid infrastructure development rely heavily on robust diesel backup systems to combat grid instability and secure critical cloud platforms.

Who are the leading companies in the Data Center Generator Market, and what are their primary strategies?

Key industry leaders include prominent names such as Caterpillar, Cummins Inc., and Kohler Co.. Their primary strategies focus on developing highly efficient engines, expanding high-capacity product portfolios, and establishing strategic partnerships with large colocation providers. They also invest heavily in clean emissions technology to meet shifting regional compliance mandates.

What does Porter's Five Forces analysis indicate for the Data Center Generator Market?

Porter's Five Forces highlights high barriers to entry due to advanced technology, compliance standards, and capital demands. Bargaining power of buyers is strong among hyperscale data center operators. Rivalry among existing players is intense, while the threat of substitutes remains low, as alternative large-scale grid storage solutions are not yet cost-competitive for extended standby periods.

What is the SWOT analysis for the Data Center Generator Market?

The market SWOT analysis reveals strong Strengths in proven engineering reliability and high baseline demand. Weaknesses include high upfront procurement and maintenance costs. Emerging Opportunities exist in the commercialization of low-emission natural gas models, while Threats stem from tightening global environmental laws and eventual advances in grid-scale battery storage solutions.

How is the value chain structured in the Data Center Generator Market?

The value chain begins with high-grade raw materials and advanced engine component manufacturing, moving to generator assembly. Specialized distributors and system integrators customize and install these backup systems inside the facilities. The chain is completed by long-term service contracts and technical maintenance, which are critical for ensuring the immediate performance of Tier 3 and Tier 4 backup power.

What are the key strategic investment recommendations for the Data Center Generator Market?

Investors should target opportunities in natural gas backup generators and systems designed for high-availability setups like Tier 3 and Tier 4. Furthermore, investing in high-capacity generator units (Greater than 2 MW) offers strong strategic benefits, as cloud providers and enterprise data centers continue to build out massive, high-density computing campuses.

What is the general conclusion and key takeaway of this Data Center Generator Market study?

In conclusion, the Data Center Generator Market is on a clear upward trajectory, set to increase from 5.84 Billion in 2026 to 8.60 Billion by 2033 at a CAGR of 5.69%. Balancing absolute backup operational reliability with emerging green energy initiatives will remain the critical factor for success as the global digital infrastructure market continues to expand.

What research methodology was used to compile this Data Center Generator Market study?

This study was conducted using a rigorous methodology combining primary and secondary research. Primary research involved structured interviews and insights from industry experts, market participants, and data center operators. Secondary research included analyzing company financial filings, technical documents, and reliable industry databases to validate historical trends and baseline forecasts.

What is the precise research scope and boundary of this Data Center Generator Market report?

The scope of this report focuses on standby and backup generators installed within global data center networks. It analyzes market trends, segmenting the market by Tier (Tier 1 and 2, Tier 3, Tier 4), capacity (Below 1 MW, 1-2 MW, Greater than 2 MW), and product types (Diesel, Natural Gas). The forecast covers the period from 2027 to 2033, utilizing 2026 as the base valuation year.

Who are the key companies, and what are their recent developments in the Data Center Generator Market?

Key players in the market include ABB, Atlas Copco AB, Caterpillar, Cummins Inc., DEUTZ AG, Generac Power Systems, Inc., HITEC Power Protection, Kirloskar, Kohler Co., and MITSUBISHI MOTORS CORPORATION. Recent developments focus on high-efficiency generator product launches, strategic service contracts, and the design of eco-certified diesel and natural gas models to meet hyperscaler sustainability goals.