Digital Pathology Market Overview - Definition, scope, and significance

Digital pathology represents the transformation of traditional glass slides into digital images that can be viewed, managed, and analyzed on computer screens. This technology enables pathologists to convert physical specimens into high-resolution digital files, facilitating remote viewing, automated analysis, and integration with other healthcare systems. The market encompasses hardware such as digital scanners, software platforms for image management and analysis, storage solutions, and communication systems that support telepathology services. Digital pathology has become increasingly significant in modern healthcare as it addresses critical challenges in traditional microscopy, including limited accessibility, storage constraints, and the inability to easily share specimens for consultation or education.

Digital Pathology Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The digital pathology market is driven by several key factors including the increasing adoption of artificial intelligence in healthcare, growing demand for telepathology services, and the need for improved diagnostic accuracy and efficiency. The rising prevalence of chronic diseases requiring histopathological examination, along with the growing trend toward personalized medicine, further accelerates market growth. However, the market faces restraints such as high initial implementation costs, concerns about data security and privacy, and the need for significant infrastructure upgrades in healthcare facilities. Challenges include the lack of standardization across different digital pathology systems and the requirement for specialized training for pathologists. Despite these obstacles, significant opportunities exist in emerging markets, the integration of AI and machine learning capabilities, and the expansion of remote diagnostic services.

Digital Pathology Market Growth Trends - Current and emerging trends shaping the market

The digital pathology market is experiencing several notable growth trends, including the increasing integration of artificial intelligence and machine learning algorithms for automated image analysis and diagnosis. The adoption of cloud-based solutions for storage and collaboration is accelerating, enabling seamless sharing of digital slides across geographical boundaries. There is also a growing trend toward the development of whole slide imaging systems with improved resolution and faster scanning capabilities. The market is witnessing increased focus on interoperability standards to ensure compatibility between different digital pathology systems. Additionally, the expansion of telepathology services for remote diagnosis and consultation is becoming more prevalent, particularly in underserved regions. The convergence of digital pathology with other digital health technologies, such as electronic health records and laboratory information systems, is creating more integrated diagnostic workflows.

COVID-19 Impact on the Digital Pathology Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the digital pathology market, initially causing disruptions in routine diagnostic services and research activities. However, the pandemic also accelerated the adoption of digital pathology solutions as healthcare systems sought to minimize physical contact and enable remote work capabilities. The need for remote diagnosis and consultation became more critical during lockdowns, driving increased interest in telepathology solutions. While some hospitals and diagnostic laboratories faced temporary closures or reduced operations, the long-term impact has been positive, with many institutions accelerating their digital transformation initiatives. The pandemic highlighted the importance of digital infrastructure in healthcare, leading to increased investments in digital pathology systems. As healthcare systems recover, the market is expected to maintain its growth trajectory, with many of the digital pathology adoption trends established during the pandemic continuing to drive market expansion.

Digital Pathology Market Competitive Landscape - Major competitors and market consolidation

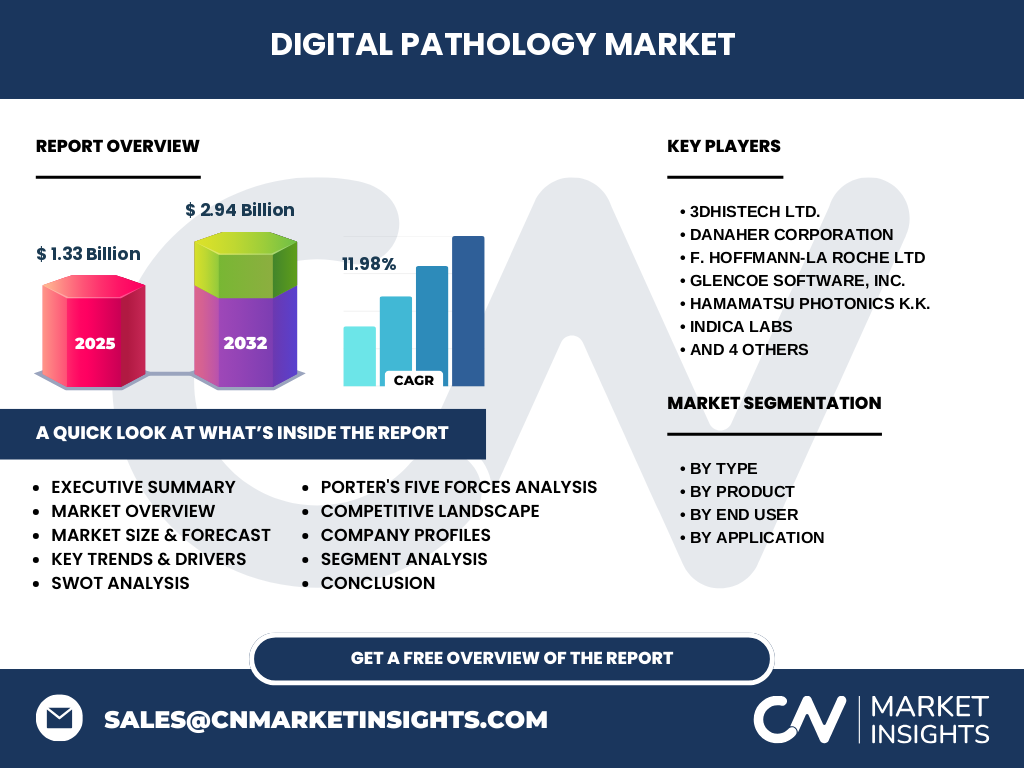

The digital pathology market features a mix of established medical device companies and specialized digital pathology solution providers. Key players include 3DHISTECH Ltd., Danaher Corporation, F. Hoffmann-La Roche Ltd, Glencoe Software, Inc., Hamamatsu Photonics K.K., Indica Labs, Koninklijke Philips N.V., Nikon Corporation, Perkin Elmer, Inc., and Visiopharm A/S. The competitive landscape is characterized by ongoing technological innovation, strategic partnerships, and mergers and acquisitions as companies seek to expand their product portfolios and market presence. Competition is intensifying as companies focus on developing more advanced AI-powered solutions, improving interoperability, and expanding into emerging markets. The market is witnessing consolidation through strategic acquisitions, with larger companies acquiring innovative startups to enhance their technological capabilities and expand their customer base.

Executive Summary - High-level overview and key findings about Digital Pathology Market

The digital pathology market is experiencing robust growth, driven by technological advancements and increasing demand for efficient diagnostic solutions. The market is projected to grow from 1.33 Billion in 2025 to 2.94 Billion by 2032, representing a CAGR of 11.98%. Key growth drivers include the integration of AI and machine learning, the expansion of telepathology services, and the increasing adoption of digital solutions in healthcare. The market is segmented by type (human and veterinary pathology), product (scanners, software, storage, and communication systems), end user (pharma and biotech companies, hospitals, and academics), and application (drug discovery, disease diagnostics, teleconsultation, and training & education). The competitive landscape features both established medical device companies and specialized digital pathology solution providers, with ongoing innovation and strategic partnerships shaping the market dynamics.

Digital Pathology Market Forecast - Projections for 2025-2032 period

The digital pathology market is forecasted to experience substantial growth over the 2025-2032 period, with the market size expected to increase from 1.33 Billion in 2025 to 2.94 Billion by 2032, representing a compound annual growth rate of 11.98%. This growth trajectory reflects the increasing adoption of digital pathology solutions across healthcare institutions, research organizations, and pharmaceutical companies. The forecast period is expected to witness continued technological advancements, particularly in AI integration and cloud-based solutions. Market expansion will be driven by increasing demand for efficient diagnostic workflows, the growing need for remote consultation services, and the rising prevalence of chronic diseases requiring histopathological examination. The forecast also accounts for the ongoing digital transformation in healthcare and the increasing recognition of digital pathology's benefits in improving diagnostic accuracy and efficiency.

Digital Pathology Market Size and Share by Segmentation - Breakdown by {segmentData}

The digital pathology market is segmented across multiple dimensions, with each segment contributing to the overall market growth. By type, the market is divided into human pathology and veterinary pathology, with human pathology representing the larger segment due to higher disease prevalence and greater adoption in clinical settings. In terms of products, the market includes scanners, software, storage solutions, and communication systems, with scanners and software typically representing the largest shares due to their essential role in digital pathology workflows. The end-user segment comprises pharma and biotech companies, hospitals, and academic institutions, with hospitals and pharmaceutical companies being major adopters due to their high diagnostic and research needs. Applications include drug discovery, disease diagnostics, teleconsultation, and training & education, with disease diagnostics and drug discovery being the primary applications driving market demand.

Global Digital Pathology Market Size and Share by Region - Geographic distribution

While specific regional market share data is not provided, the global digital pathology market exhibits varying adoption rates across different geographic regions. North America currently leads the market due to advanced healthcare infrastructure, high adoption of digital technologies, and significant investments in research and development. Europe follows closely, with strong government support for digital health initiatives and well-established healthcare systems. The Asia-Pacific region is expected to witness the fastest growth during the forecast period, driven by increasing healthcare expenditure, growing awareness of digital pathology benefits, and expanding healthcare infrastructure in countries like China, Japan, and India. Latin America and the Middle East & Africa regions are also showing increasing adoption, though at a relatively slower pace due to infrastructure challenges and budget constraints in some areas.

Regional Analysis of the Digital Pathology Market - Detailed regional market performance

The digital pathology market demonstrates distinct regional characteristics and adoption patterns. North America, particularly the United States, leads in market adoption due to advanced healthcare infrastructure, favorable reimbursement policies, and strong presence of key market players. The region benefits from high healthcare expenditure and early adoption of innovative technologies. Europe shows strong market presence with countries like Germany, the UK, and France leading adoption, supported by government initiatives promoting digital health transformation. The Asia-Pacific region presents significant growth opportunities, with countries like China, Japan, and South Korea investing heavily in healthcare digitization. However, varying levels of healthcare infrastructure and regulatory environments across countries in this region create a diverse market landscape. Emerging markets in Latin America and the Middle East & Africa are gradually adopting digital pathology solutions, though progress is influenced by economic factors and healthcare system development.

Leading Company Profiles in the Digital Pathology Market - Industry players and strategies

The digital pathology market features several prominent companies with distinct strategies and market positions. 3DHISTECH Ltd. is known for its comprehensive digital pathology solutions, including scanners and software platforms. Danaher Corporation, through its Leica Biosystems division, offers a wide range of digital pathology products and has been actively involved in strategic acquisitions to strengthen its market position. F. Hoffmann-La Roche Ltd provides advanced digital pathology solutions integrated with AI capabilities through its Ventana Medical Systems division. Hamamatsu Photonics K.K. specializes in high-quality digital slide scanners and imaging solutions. Indica Labs focuses on AI-powered image analysis software, while Koninklijke Philips N.V. offers integrated diagnostic solutions. Nikon Corporation brings its expertise in optical technologies to digital pathology, and Perkin Elmer, Inc. provides comprehensive digital pathology platforms for research and clinical applications. Visiopharm A/S specializes in AI-driven image analysis solutions for pathology.

Porter's Five Forces Analysis of the Digital Pathology Market - Competitive forces assessment

The digital pathology market's competitive landscape is shaped by several key forces. The threat of new entrants is moderate, as the market requires significant technological expertise, regulatory approvals, and substantial capital investment. Bargaining power of buyers is relatively high due to the availability of multiple solution providers and the importance of cost-effectiveness in healthcare decisions. The bargaining power of suppliers is moderate, as key components like imaging sensors and specialized software require specific technical capabilities. The threat of substitute products is low, as traditional microscopy methods are increasingly being replaced by digital solutions. Competitive rivalry is intense, with established players competing on technological innovation, pricing, and comprehensive solution offerings. The market is also influenced by the growing importance of AI integration and the need for interoperability between different systems.

SWOT Analysis of the Digital Pathology Market - Strengths, weaknesses, opportunities, threats

The digital pathology market exhibits several key strengths, including technological advancement, improved diagnostic accuracy, and enhanced collaboration capabilities. The integration of AI and machine learning represents a significant strength, enabling more efficient and accurate analysis. However, weaknesses include high implementation costs, data security concerns, and the need for specialized training. Opportunities abound in emerging markets, the expansion of telepathology services, and the continuous development of more advanced AI algorithms. The market also benefits from increasing healthcare digitization and growing demand for remote diagnostic services. Threats include regulatory challenges, potential data privacy issues, and the need for standardization across different systems. Additionally, the market faces competition from alternative diagnostic technologies and must address concerns about the reliability of AI-powered diagnostic tools.

Digital Pathology Market Value Chain Analysis - Industry structure and value flow

The digital pathology value chain encompasses several key stages, beginning with research and development of hardware and software solutions. Component manufacturers provide essential elements such as imaging sensors, processors, and storage systems. System integrators combine these components to create comprehensive digital pathology solutions, including scanners, software platforms, and storage systems. Value is added through the development of AI algorithms for image analysis and the creation of user-friendly interfaces for pathologists. Distributors and direct sales teams deliver these solutions to end-users, while service providers offer installation, training, and maintenance support. The end-users, including hospitals, diagnostic laboratories, pharmaceutical companies, and academic institutions, derive value through improved diagnostic capabilities, enhanced collaboration, and more efficient workflows. The value chain is supported by regulatory bodies ensuring compliance and standards organizations promoting interoperability.

Key Investment Insights in the Digital Pathology Market - Strategic investment recommendations

Investment opportunities in the digital pathology market are driven by several key factors. The integration of artificial intelligence and machine learning capabilities presents significant investment potential, as these technologies continue to enhance diagnostic accuracy and efficiency. Cloud-based solutions for storage and collaboration represent another attractive investment area, given the growing need for remote access and data sharing. Emerging markets offer substantial growth opportunities as healthcare systems in these regions undergo digital transformation. Investments in interoperability solutions are particularly promising, as the industry moves toward standardized systems. Additionally, the development of specialized applications for specific disease areas or research purposes presents niche investment opportunities. Strategic partnerships between technology providers and healthcare institutions can also create valuable investment prospects, particularly in areas combining digital pathology with other diagnostic technologies.

Digital Pathology Market Conclusion - Summary and key takeaways

The digital pathology market is positioned for significant growth, driven by technological advancements and increasing demand for efficient diagnostic solutions. The market's projected growth from 1.33 Billion in 2025 to 2.94 Billion by 2032, at a CAGR of 11.98%, reflects the strong momentum in adoption across healthcare institutions and research organizations. Key drivers include the integration of AI and machine learning, the expansion of telepathology services, and the growing need for improved diagnostic accuracy and efficiency. While challenges exist in terms of implementation costs and standardization, the market offers substantial opportunities in emerging markets and through technological innovation. The competitive landscape is dynamic, with both established players and specialized solution providers contributing to market growth through continuous innovation and strategic partnerships.

Research Methodology - How this research was conducted

The research methodology for this digital pathology market analysis involved a comprehensive approach combining primary and secondary research sources. Primary research included interviews with industry experts, healthcare professionals, and key opinion leaders in digital pathology. Secondary research encompassed analysis of company annual reports, financial statements, investor presentations, and industry publications. Market data was validated through multiple sources to ensure accuracy and reliability. The research considered various factors influencing market growth, including technological advancements, regulatory landscape, and competitive dynamics. Segmentation analysis was conducted based on available data, considering type, product, end-user, and application categories. Regional analysis incorporated market trends and adoption patterns across different geographic areas. The forecast methodology utilized historical data, current market trends, and future growth projections to estimate market size and growth rates.

Research Scope - Coverage and limitations

This research on the digital pathology market covers the period from 2025 to 2032, with 2025 as the base year. The scope includes comprehensive analysis of market size, growth trends, competitive landscape, and regional dynamics. The research covers key market segments including type (human and veterinary pathology), product (scanners, software, storage, and communication systems), end-user (pharma and biotech companies, hospitals, and academics), and application (drug discovery, disease diagnostics, teleconsultation, and training & education). The analysis includes major market players and their strategies, along with an assessment of market drivers, restraints, and opportunities. However, the research is limited by the availability of specific regional market share data and detailed financial information for some companies. The scope also does not include exhaustive coverage of all potential niche applications or emerging startups in the market.

Key Companies and Recent Developments in the Digital Pathology Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The digital pathology market has witnessed several significant developments from key players in recent years. 3DHISTECH Ltd. has continued to enhance its digital pathology platform with advanced AI capabilities and improved scanning technologies. Danaher Corporation has expanded its digital pathology portfolio through strategic acquisitions and partnerships, strengthening its position in the market. F. Hoffmann-La Roche Ltd has made significant strides in integrating AI-powered image analysis into its digital pathology solutions, particularly through its Ventana Medical Systems division. Hamamatsu Photonics K.K. has introduced new high-resolution slide scanners with improved imaging capabilities. Indica Labs has expanded its AI-powered image analysis software offerings, while Koninklijke Philips N.V. has focused on developing integrated diagnostic solutions combining digital pathology with other medical imaging technologies. Nikon Corporation has leveraged its optical expertise to enhance digital slide scanning capabilities, and Perkin Elmer, Inc. has expanded its comprehensive digital pathology platforms for both research and clinical applications. Visiopharm A/S has continued to advance its AI-driven image analysis solutions for pathology applications. These companies have also engaged in various partnerships and collaborations to expand their market presence and technological capabilities.