Bone Cement Market Overview - Definition, scope, and significance

Bone cement is a critical medical material used primarily in orthopedic procedures to secure prosthetic implants to bone tissue. These materials, typically composed of polymethyl methacrylate (PMMA) or other bioactive compounds, serve as a bonding agent that facilitates the attachment of artificial joints, plates, and other orthopedic devices to the skeletal structure. The bone cement market encompasses various formulations including PMMA-based cements, calcium phosphate cements, and glass polyalkenoate cements, each designed for specific clinical applications. This market plays a vital role in modern orthopedic surgery, enabling successful joint replacements, spinal procedures, and trauma fixation surgeries that significantly improve patient mobility and quality of life.

Bone Cement Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The bone cement market is driven by several key factors including the rising geriatric population, increasing prevalence of osteoporosis and arthritis, and growing demand for minimally invasive surgical procedures. Technological advancements in cement formulations that improve biocompatibility and reduce complications have also accelerated market growth. However, the market faces restraints such as stringent regulatory requirements for medical devices, potential complications associated with cement use including bone necrosis and thermal damage, and the emergence of cementless implant alternatives. Challenges include maintaining product quality consistency, managing the risk of infection, and addressing the learning curve for surgeons adopting new cement technologies. Opportunities exist in developing bioactive cements with enhanced osteoconductive properties, expanding applications in emerging markets, and creating specialized formulations for specific patient demographics.

Bone Cement Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the bone cement market include the increasing adoption of antibiotic-loaded bone cements to reduce infection risks, particularly in joint replacement surgeries. There is a notable shift toward the development of bioactive cements that promote bone regeneration and integration, moving beyond purely mechanical fixation. The market is witnessing growing demand for premixed and ready-to-use cement formulations that improve surgical efficiency and reduce preparation time. Additionally, the integration of imaging technologies with cement application procedures is enhancing surgical precision. Emerging trends include the development of smart bone cements with controlled drug release capabilities, the use of nanotechnology to improve cement properties, and the exploration of biodegradable cement alternatives that gradually transfer load to newly formed bone tissue.

COVID-19 Impact on the Bone Cement Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the bone cement market, primarily through the temporary suspension of elective surgeries during lockdowns and the reallocation of healthcare resources to pandemic response. This led to a substantial decline in demand for bone cement products during 2020 and early 2021, particularly affecting joint replacement procedures and elective orthopedic surgeries. However, the market demonstrated resilience with a strong recovery trajectory as healthcare systems adapted to pandemic conditions and resumed non-emergency procedures. The pandemic also accelerated certain trends, including the adoption of telemedicine for pre-operative consultations and the increased focus on infection control measures in surgical settings. The recovery has been supported by pent-up demand for delayed procedures and the gradual normalization of healthcare services across regions.

Bone Cement Market Competitive Landscape - Major competitors and market consolidation

The bone cement market features a moderately consolidated competitive landscape with several established multinational medical device companies dominating the market. Major players include Zimmer Biomet, Stryker Corporation, DePuy Synthes, Smith & Nephew, and Heraeus Holding GmbH, which collectively hold significant market share through their extensive product portfolios and global distribution networks. These companies compete based on product innovation, quality, pricing, and customer relationships with healthcare providers. The market has witnessed strategic initiatives including mergers, acquisitions, and partnerships aimed at expanding product offerings and geographic presence. Smaller specialized companies like Tecres S.p.A and Teknimed maintain competitive positions through niche product innovations and focus on specific clinical applications. The competitive dynamics are characterized by continuous product development efforts and strategic collaborations to enhance technological capabilities.

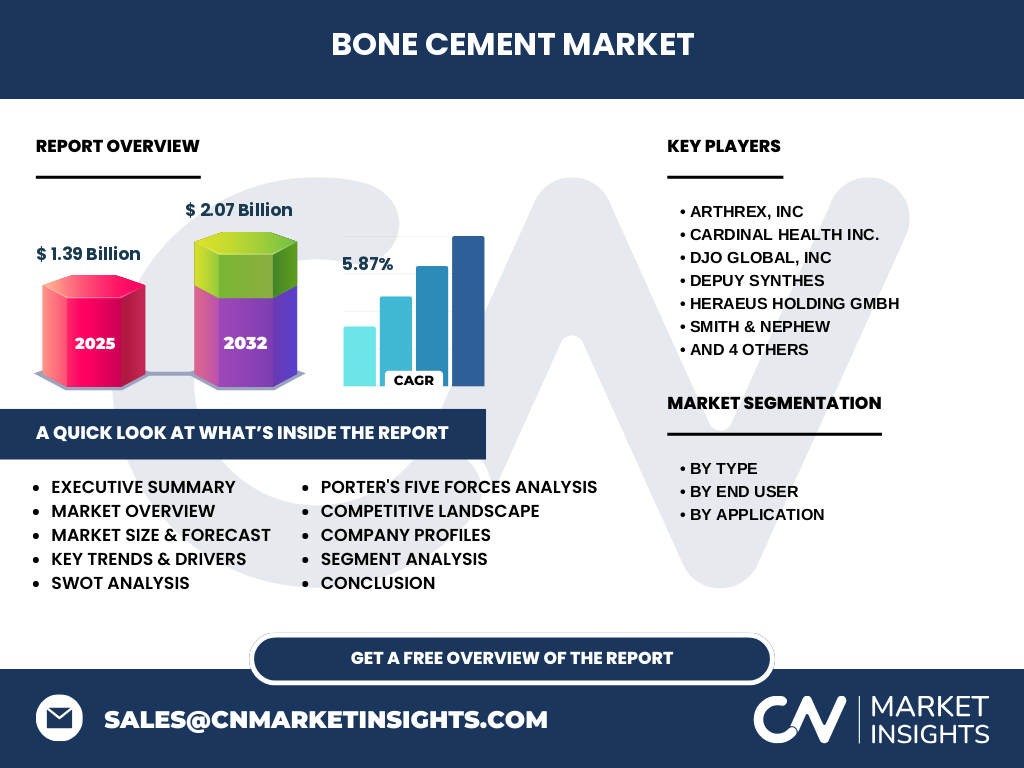

Executive Summary - High-level overview and key findings about Bone Cement Market

The global bone cement market is experiencing steady growth driven by demographic shifts, technological advancements, and expanding clinical applications. With a market size of $1.39 billion in 2025 and projected to reach $2.07 billion by 2032, the market demonstrates a healthy compound annual growth rate of 5.87%. PMMA-based cements continue to dominate the market due to their proven clinical efficacy and cost-effectiveness, while emerging cement types are gaining traction in specialized applications. Hospitals remain the primary end-users, accounting for the largest share of demand, though ambulatory surgery centers are experiencing rapid growth due to the trend toward outpatient procedures. The market's future growth will be shaped by innovation in bioactive materials, expanding applications in spinal procedures, and increasing adoption in emerging markets with growing healthcare infrastructure.

Bone Cement Market Forecast - Projections for 2025-2032 period

The bone cement market is projected to grow from $1.39 billion in 2025 to $2.07 billion by 2032, representing a compound annual growth rate of 5.87% during the forecast period. This growth trajectory reflects sustained demand across key application areas including arthroplasty, kyphoplasty, and vertebroplasty procedures. The PMMA segment is expected to maintain its market leadership due to established clinical protocols and cost advantages, while calcium phosphate and glass polyalkenoate cements are anticipated to experience higher growth rates as their clinical benefits become more widely recognized. Geographic expansion will be driven by increasing healthcare expenditure in emerging economies and the growing adoption of advanced orthopedic procedures. The forecast also accounts for continued technological innovations that enhance product performance and expand clinical indications for bone cement applications.

Bone Cement Market Size and Share by Segmentation - Breakdown by {segmentData}

The bone cement market segmentation reveals distinct patterns across types, end users, and applications. By type, polymethyl methacrylate (PMMA) cements dominate the market due to their long-standing clinical track record and cost-effectiveness, capturing the largest market share. Calcium phosphate cements represent the fastest-growing segment, driven by their bioactive properties and potential for bone regeneration. Glass polyalkenoate cements, while representing a smaller segment, are gaining traction in specific applications due to their unique properties. By end user, hospitals constitute the largest segment, accounting for the majority of bone cement consumption due to their comprehensive surgical capabilities and high patient volumes. Ambulatory surgery centers represent the fastest-growing end-user segment, reflecting the trend toward outpatient procedures. By application, arthroplasty leads the market, driven by the high volume of joint replacement surgeries, followed by kyphoplasty and vertebroplasty procedures for spinal conditions.

Global Bone Cement Market Size and Share by Region - Geographic distribution

The global bone cement market exhibits varying dynamics across different geographic regions. North America represents the largest regional market, driven by advanced healthcare infrastructure, high healthcare expenditure, and a large patient population requiring orthopedic interventions. Europe follows as the second-largest market, characterized by established medical device regulations and significant adoption of advanced surgical techniques. The Asia-Pacific region is emerging as the fastest-growing market, fueled by improving healthcare access, rising disposable incomes, and increasing prevalence of orthopedic conditions in aging populations. Latin America and the Middle East & Africa regions represent smaller but growing markets, with growth driven by expanding healthcare infrastructure and increasing awareness of treatment options. Regional variations in regulatory frameworks, reimbursement policies, and surgical practices influence market penetration and growth rates across different geographies.

Regional Analysis of the Bone Cement Market - Detailed regional market performance

Regional market performance varies significantly across different geographies, reflecting diverse healthcare systems, economic conditions, and demographic profiles. In North America, particularly the United States, the market benefits from advanced healthcare infrastructure, favorable reimbursement policies, and high adoption rates of innovative medical technologies. The region's aging population and high prevalence of osteoarthritis drive consistent demand for bone cement products. Europe's market is characterized by stringent regulatory standards and a strong emphasis on product quality, with countries like Germany, France, and the UK leading in adoption rates. The Asia-Pacific region presents substantial growth opportunities, with China and India experiencing rapid market expansion due to improving healthcare access and increasing healthcare spending. Japan's mature market is driven by its elderly population and advanced medical technology adoption. Latin American markets, particularly Brazil and Mexico, are growing steadily with improving healthcare infrastructure, while Middle Eastern markets are expanding through healthcare modernization initiatives.

Leading Company Profiles in the Bone Cement Market - Industry players and strategies

The bone cement market is dominated by several key players with distinct strategic approaches and market positions. Zimmer Biomet leverages its comprehensive orthopedic portfolio and global distribution network to maintain market leadership, focusing on product innovation and strategic acquisitions to expand its offerings. Stryker Corporation emphasizes technological advancement and clinical evidence generation to support its product lines, while maintaining strong relationships with key opinion leaders in orthopedic surgery. DePuy Synthes (Johnson & Johnson) benefits from its parent company's resources and global reach, with a strategy centered on integrated solutions and comprehensive surgical systems. Smith & Nephew focuses on premium product positioning and customer-centric solutions, particularly in sports medicine and joint reconstruction. Heraeus Holding GmbH specializes in high-quality PMMA bone cements with a strong presence in European markets. Smaller players like Tecres S.p.A and Teknimed differentiate through specialized product innovations and focus on specific clinical niches, while maintaining agility in responding to market needs.

Porter's Five Forces Analysis of the Bone Cement Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the bone cement market. The threat of new entrants is moderate due to high regulatory barriers, significant capital requirements for manufacturing facilities, and the need for extensive clinical validation. Supplier bargaining power is relatively low as raw material suppliers are numerous and switching costs are manageable for manufacturers. Buyer bargaining power is moderate to high, particularly for large hospital systems and group purchasing organizations that can negotiate favorable terms based on volume purchases. The threat of substitutes is moderate, with cementless implant technologies and emerging biodegradable alternatives presenting competitive challenges. Competitive rivalry is intense among established players, characterized by price competition, product innovation, and strategic partnerships. The overall industry attractiveness is moderate, with growth opportunities balanced against regulatory challenges and competitive pressures.

SWOT Analysis of the Bone Cement Market - Strengths, weaknesses, opportunities, threats

The bone cement market exhibits distinct strengths including established clinical efficacy, wide range of applications, and continuous technological advancements that enhance product performance. The market benefits from strong demand drivers including aging populations and increasing orthopedic procedures globally. However, weaknesses exist in the form of potential complications associated with cement use, including thermal necrosis and embolism risks, as well as the environmental concerns related to PMMA production and disposal. Opportunities are abundant in developing bioactive cements with enhanced osteoconductive properties, expanding applications in emerging markets, and creating specialized formulations for specific patient demographics. Threats include increasing regulatory scrutiny, competition from alternative fixation methods, and potential supply chain disruptions affecting raw material availability. The market's future success will depend on addressing weaknesses while capitalizing on emerging opportunities in the evolving healthcare landscape.

Bone Cement Market Value Chain Analysis - Industry structure and value flow

The bone cement market value chain encompasses multiple stages from raw material procurement to end-user delivery. The upstream segment involves suppliers of key raw materials including methyl methacrylate monomer, prepolymerized PMMA beads, and various additives and stabilizers. Manufacturing companies transform these materials into finished bone cement products through specialized production processes that ensure sterility and quality control. The midstream segment includes distribution networks, medical device distributors, and healthcare group purchasing organizations that facilitate product delivery to healthcare facilities. The downstream segment comprises hospitals, ambulatory surgery centers, and clinics that utilize bone cement in orthopedic procedures. Value is added at each stage through product innovation, quality assurance, regulatory compliance, and clinical support services. The value chain is characterized by strong quality control requirements, regulatory oversight, and the need for continuous product development to meet evolving clinical needs.

Key Investment Insights in the Bone Cement Market - Strategic investment recommendations

Strategic investment opportunities in the bone cement market are driven by several key factors that warrant consideration. The market's projected growth rate of 5.87% through 2032 presents attractive returns for investors focused on the medical device sector. Investment opportunities exist in companies developing next-generation bioactive cements with enhanced osteoconductive properties and controlled drug release capabilities. The expanding applications in minimally invasive spinal procedures represent another promising investment area, particularly as kyphoplasty and vertebroplasty procedures gain wider adoption. Geographic expansion in emerging markets offers significant growth potential, with healthcare infrastructure development creating new demand for advanced orthopedic solutions. Investors should also consider companies with strong research and development capabilities, established regulatory compliance frameworks, and strategic partnerships with healthcare providers. The market's resilience during economic downturns, driven by essential medical procedures, provides additional investment stability.

Bone Cement Market Conclusion - Summary and key takeaways

The bone cement market presents a compelling growth story supported by demographic trends, technological advancements, and expanding clinical applications. With a projected market size of $2.07 billion by 2032 and a steady CAGR of 5.87%, the industry demonstrates robust fundamentals and resilience. PMMA cements continue to dominate due to their proven efficacy and cost-effectiveness, while emerging cement types offer specialized solutions for specific clinical needs. The market's future will be shaped by innovation in bioactive materials, expansion into emerging markets, and the development of smart cement technologies with enhanced functionality. Despite challenges including regulatory requirements and competition from alternative fixation methods, the fundamental drivers of market growth remain strong. Success in this market requires a balanced approach combining product innovation, strategic partnerships, and geographic expansion to capture emerging opportunities while addressing clinical and regulatory challenges.

Research Methodology - How this research was conducted

This comprehensive market research was conducted using a rigorous methodology combining primary and secondary research approaches. Primary research involved interviews with key industry stakeholders including medical device manufacturers, orthopedic surgeons, hospital procurement managers, and regulatory experts to gather firsthand insights into market dynamics and trends. Secondary research encompassed extensive review of company annual reports, financial statements, industry publications, medical journals, and market databases to validate findings and establish market size estimates. Data triangulation techniques were employed to cross-verify information from multiple sources, ensuring accuracy and reliability. The research methodology included detailed analysis of market segmentation, competitive landscape assessment, and regional market dynamics. Statistical modeling and forecasting techniques were applied to project market growth trajectories, incorporating macroeconomic factors, demographic trends, and industry-specific variables to generate comprehensive market insights.

Research Scope - Coverage and limitations

This research provides comprehensive coverage of the global bone cement market, focusing on key market segments, regional dynamics, competitive landscape, and growth projections through 2032. The scope encompasses major bone cement types including PMMA, calcium phosphate, and glass polyalkenoate cements, along with their respective applications in arthroplasty, kyphoplasty, and vertebroplasty procedures. Regional coverage includes North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with detailed analysis of market drivers and challenges in each geography. The research addresses key market participants, their strategies, and recent developments in the industry. Limitations of this research include the availability of public financial data for private companies, potential variations in regional reporting standards, and the impact of unforeseen market disruptions. The analysis is based on information available up to the research cutoff date and may not reflect subsequent market developments or regulatory changes.

Key Companies and Recent Developments in the Bone Cement Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The bone cement market features several prominent companies driving innovation and market growth through strategic initiatives. Zimmer Biomet recently announced the expansion of its cement portfolio with enhanced antibiotic-loaded formulations designed to reduce surgical site infections. Stryker Corporation launched a new bioactive bone cement system incorporating growth factors to promote bone regeneration and improve implant integration. DePuy Synthes introduced an advanced PMMA cement with improved handling characteristics and extended working time for complex surgical procedures. Smith & Nephew formed a strategic partnership with a biotechnology company to develop next-generation bone cements with controlled drug release capabilities. Heraeus Holding GmbH expanded its manufacturing capacity in Europe to meet growing demand for high-quality PMMA bone cements. Tecres S.p.A launched a new vertebroplasty cement system with enhanced radiopacity and controlled viscosity for improved clinical outcomes. These developments reflect the industry's focus on product innovation, infection prevention, and enhanced surgical outcomes to maintain competitive advantage in the evolving market landscape.