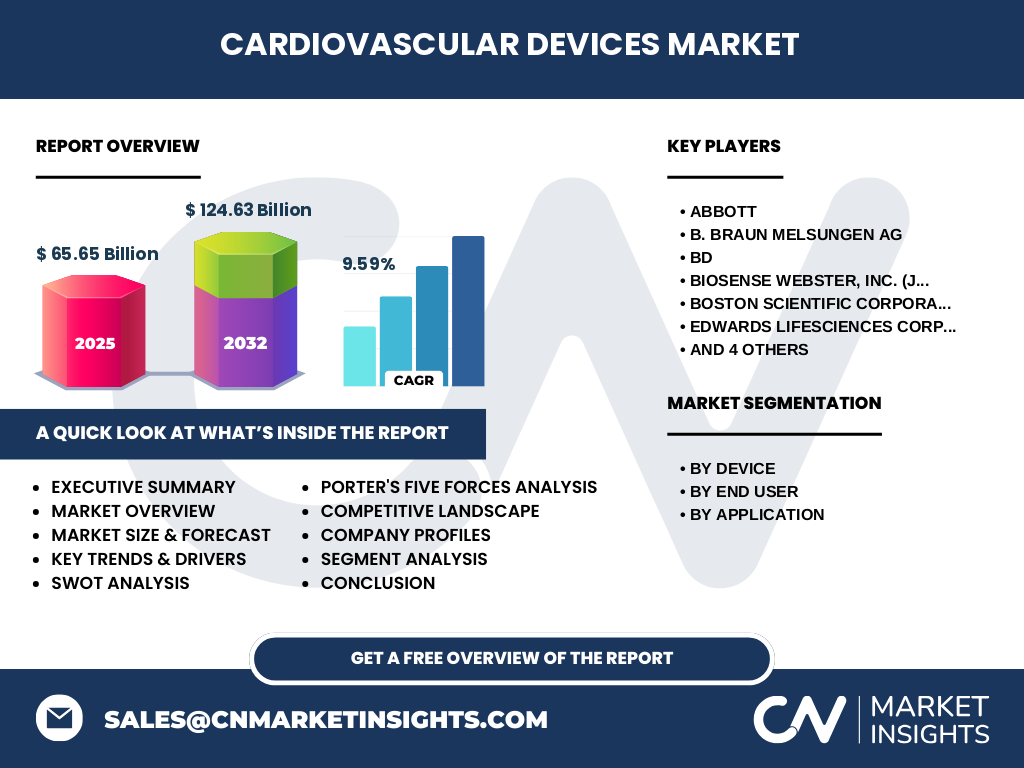

Cardiovascular Devices Market Overview - Definition, scope, and significance

Cardiovascular devices encompass a broad range of medical instruments, equipment, and implants designed for the diagnosis, monitoring, treatment, and management of cardiovascular diseases and disorders. This market includes devices for coronary artery disease, heart failure, arrhythmias, and other cardiac conditions. The significance of this market lies in its critical role in addressing the global burden of cardiovascular diseases, which remain the leading cause of mortality worldwide. With the global cardiovascular devices market valued at $65.65 billion in 2025 and projected to reach $124.63 billion by 2032, growing at a CAGR of 9.59%, this sector represents a vital component of modern healthcare infrastructure and medical technology innovation.

Cardiovascular Devices Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The cardiovascular devices market is primarily driven by the increasing prevalence of cardiovascular diseases globally, coupled with an aging population and rising obesity rates. Technological advancements in minimally invasive procedures, artificial intelligence integration, and wearable cardiac monitoring devices present significant opportunities for market expansion. However, the market faces restraints including high device costs, stringent regulatory requirements, and reimbursement challenges. Key challenges include the need for skilled professionals to operate advanced devices and concerns regarding device-related complications. The market also faces opportunities in emerging economies where healthcare infrastructure is rapidly developing and demand for advanced cardiac care is growing.

Cardiovascular Devices Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the cardiovascular devices market include the increasing adoption of minimally invasive procedures, which reduce recovery times and hospital stays. The integration of digital health technologies and remote monitoring capabilities is transforming cardiac care delivery. There is a notable shift toward personalized medicine approaches, with devices being tailored to individual patient needs. The market is also witnessing increased demand for home-based cardiac monitoring solutions, driven by the COVID-19 pandemic's impact on healthcare delivery. Emerging trends include the development of bioresorbable stents, advanced imaging technologies for cardiac procedures, and the incorporation of artificial intelligence for predictive analytics in cardiac care management.

COVID-19 Impact on the Cardiovascular Devices Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the cardiovascular devices market, causing disruptions in elective procedures and routine cardiac care. Many hospitals postponed non-emergency cardiac procedures to prioritize COVID-19 patients, leading to a temporary decline in device utilization. Supply chain disruptions affected device manufacturing and distribution. However, the pandemic also accelerated the adoption of telemedicine and remote cardiac monitoring solutions. As healthcare systems recover, there is pent-up demand for cardiac procedures, driving market recovery. The pandemic has also highlighted the importance of cardiovascular health, potentially increasing awareness and driving long-term market growth. The market is expected to witness a strong recovery trajectory with accelerated adoption of digital health solutions.

Cardiovascular Devices Market Competitive Landscape - Major competitors and market consolidation

The cardiovascular devices market features a competitive landscape dominated by major global medical device companies. Key players include Abbott, B. Braun Melsungen AG, BD, Biosense Webster (Johnson and Johnson), Boston Scientific Corporation, Edwards Lifesciences Corporation, General Electric Company, Koninklijke Philips N.V, Medtronic, and Siemens AG. The market is characterized by intense competition, with companies focusing on product innovation, strategic partnerships, and mergers and acquisitions to strengthen their market position. Competition is particularly fierce in segments such as stents, pacemakers, and cardiac monitoring devices. Companies are investing heavily in research and development to introduce technologically advanced products and maintain their competitive edge in this rapidly evolving market.

Executive Summary - High-level overview and key findings about Cardiovascular Devices Market

The cardiovascular devices market represents a critical segment of the global medical device industry, with a market size of $65.65 billion in 2025 and projected growth to $124.63 billion by 2032, reflecting a robust CAGR of 9.59%. This growth is driven by the increasing prevalence of cardiovascular diseases, technological advancements, and rising demand for minimally invasive procedures. The market encompasses various device categories including electrocardiography, pacemakers, stents, defibrillators, and cardiac catheters, serving hospitals, ambulatory surgery centers, and cardiac centers. Key applications include coronary heart disease, sudden cardiac arrest, stroke, and cerebrovascular heart disease. The competitive landscape features major global players investing in innovation and strategic partnerships to capture market share in this rapidly expanding sector.

Cardiovascular Devices Market Forecast - Projections for 2025-2032 period

The cardiovascular devices market is projected to experience substantial growth from 2025 to 2032, with the market size expected to increase from $65.65 billion in 2025 to $124.63 billion by 2032, representing a compound annual growth rate of 9.59%. This forecast reflects the increasing global burden of cardiovascular diseases, technological advancements in device development, and growing adoption of minimally invasive procedures. The forecast period is expected to witness significant investments in research and development, leading to innovative product launches and expanded applications. Emerging markets are anticipated to contribute substantially to this growth, driven by improving healthcare infrastructure and rising healthcare expenditure. The forecast also accounts for the recovery from COVID-19 related disruptions and the increasing integration of digital health technologies in cardiac care.

Cardiovascular Devices Market Size and Share by Segmentation - Breakdown by {segmentData}

The cardiovascular devices market is segmented by device type, end user, and application. By device, key segments include electrocardiography, pacemaker, stent, defibrillator, cardiac catheter, guidewire, heart valve, and event monitor. The stent segment currently holds a significant market share due to the high prevalence of coronary artery disease and the widespread adoption of percutaneous coronary interventions. By end user, hospitals represent the largest segment, followed by ambulatory surgery centers and cardiac centers, reflecting the concentration of complex cardiac procedures in hospital settings. In terms of applications, coronary heart disease accounts for the largest share, followed by sudden cardiac arrest, stroke, and cerebrovascular heart disease. Each segment presents unique growth opportunities and challenges, with varying adoption rates across different regions and healthcare systems.

Global Cardiovascular Devices Market Size and Share by Region - Geographic distribution

While specific regional market share data is not provided, the global cardiovascular devices market exhibits varying growth patterns across different geographic regions. North America, particularly the United States, represents a significant portion of the market due to advanced healthcare infrastructure, high healthcare expenditure, and the prevalence of cardiovascular diseases. Europe follows as a major market, with countries like Germany, France, and the UK contributing substantially. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, driven by improving healthcare infrastructure, rising awareness about cardiovascular health, and increasing disposable incomes in countries like China and India. Latin America and the Middle East & Africa regions are also showing promising growth potential, albeit from a smaller base, as healthcare systems in these regions continue to develop and modernize.

Regional Analysis of the Cardiovascular Devices Market - Detailed regional market performance

The cardiovascular devices market demonstrates distinct characteristics across different regions, influenced by factors such as healthcare infrastructure, disease prevalence, economic conditions, and regulatory environments. North America leads in market size and technological adoption, with a well-established healthcare system and high rates of cardiovascular disease. Europe shows steady growth, supported by advanced medical research and favorable reimbursement policies. The Asia-Pacific region is experiencing rapid market expansion, driven by large patient populations, improving healthcare access, and increasing government healthcare spending. Countries like China and India are emerging as significant markets due to their large populations and growing middle class. Latin America and the Middle East & Africa regions are gradually increasing their market share as healthcare infrastructure improves and awareness about cardiovascular health grows. Each region presents unique opportunities and challenges for market players.

Leading Company Profiles in the Cardiovascular Devices Market - Industry players and strategies

The cardiovascular devices market is dominated by several key players, each with distinct strategies and market positions. Abbott is known for its innovative stent technologies and comprehensive cardiac care portfolio. B. Braun Melsungen AG focuses on catheter-based interventions and vascular access solutions. BD (Becton, Dickinson and Company) specializes in vascular access and diagnostic products. Biosense Webster, a Johnson and Johnson company, leads in electrophysiology and mapping technologies. Boston Scientific Corporation is a major player in interventional cardiology with a strong presence in stent and balloon catheter markets. Edwards Lifesciences Corporation specializes in heart valve technologies and critical care monitoring. General Electric Company offers advanced imaging solutions for cardiac care. Koninklijke Philips N.V provides integrated diagnostic and monitoring solutions. Medtronic is a leader in cardiac rhythm management and structural heart devices. Siemens AG focuses on diagnostic imaging technologies for cardiovascular applications. These companies are continuously innovating and expanding their product portfolios to maintain competitive advantages.

Porter's Five Forces Analysis of the Cardiovascular Devices Market - Competitive forces assessment

The cardiovascular devices market exhibits characteristics that can be analyzed through Porter's Five Forces framework. The threat of new entrants is moderate due to high capital requirements, stringent regulatory approvals, and the need for extensive R&D capabilities. Bargaining power of buyers is relatively high, particularly in developed markets with multiple supplier options and price sensitivity. The bargaining power of suppliers is moderate, as key raw materials and components are available from multiple sources, though specialized components may have fewer suppliers. The threat of substitute products is low to moderate, as cardiovascular devices often have specific clinical applications with limited alternatives. Competitive rivalry is intense, with numerous global players competing on technology, price, and service. The market is characterized by rapid technological advancements, making innovation a key differentiator. Regulatory pressures and reimbursement challenges add complexity to the competitive landscape.

SWOT Analysis of the Cardiovascular Devices Market - Strengths, weaknesses, opportunities, threats

The cardiovascular devices market exhibits several key strengths, including advanced technological capabilities, a strong pipeline of innovative products, and a well-established global presence of major players. The market benefits from increasing awareness about cardiovascular health and the growing adoption of minimally invasive procedures. However, weaknesses include high device costs, complex regulatory requirements, and potential complications associated with device implantation. Opportunities abound in emerging markets, the integration of digital health technologies, and the development of personalized medicine approaches. The market also has potential for growth through strategic partnerships and acquisitions. Threats include intense competition, pricing pressures, and potential reimbursement cuts. Additionally, the market faces challenges from economic uncertainties, supply chain disruptions, and the need for continuous innovation to stay ahead in a rapidly evolving technological landscape.

Cardiovascular Devices Market Value Chain Analysis - Industry structure and value flow

The cardiovascular devices market value chain encompasses several key stages, from research and development to end-user delivery. The chain begins with raw material suppliers providing specialized components and materials for device manufacturing. This is followed by component manufacturers who produce specific parts used in cardiovascular devices. Original Equipment Manufacturers (OEMs) then assemble these components into finished devices, incorporating advanced technologies and ensuring regulatory compliance. Distributors and suppliers play a crucial role in delivering these devices to healthcare providers. End-users include hospitals, ambulatory surgery centers, and cardiac centers where the devices are utilized for patient care. Supporting services such as clinical training, technical support, and maintenance form an integral part of the value chain. The flow of value is driven by continuous innovation, quality assurance, and the ability to meet evolving clinical needs while navigating complex regulatory landscapes.

Key Investment Insights in the Cardiovascular Devices Market - Strategic investment recommendations

The cardiovascular devices market presents attractive investment opportunities driven by strong growth projections and technological advancements. Key investment insights include focusing on companies with robust R&D pipelines and a strong presence in high-growth segments such as minimally invasive devices and digital health integration. Investments in emerging markets, particularly in the Asia-Pacific region, offer significant growth potential due to improving healthcare infrastructure and increasing cardiovascular disease prevalence. Strategic acquisitions and partnerships can provide access to innovative technologies and expand market reach. Investors should also consider companies that are diversifying their product portfolios to address multiple cardiovascular conditions and those investing in artificial intelligence and machine learning applications for cardiac care. The market's resilience and essential nature in healthcare make it an attractive long-term investment, though careful consideration of regulatory risks and competitive dynamics is essential.

Cardiovascular Devices Market Conclusion - Summary and key takeaways

The cardiovascular devices market represents a dynamic and rapidly growing sector within the global medical device industry. With a market size of $65.65 billion in 2025 and projected to reach $124.63 billion by 2032, growing at a CAGR of 9.59%, the market demonstrates strong growth potential driven by increasing cardiovascular disease prevalence, technological advancements, and expanding healthcare access. The market encompasses a wide range of devices serving various applications and end-users, with significant opportunities in emerging markets and innovative technologies. Key players are focusing on product innovation, strategic partnerships, and geographic expansion to maintain competitive advantages. While the market faces challenges such as regulatory complexities and pricing pressures, the overall outlook remains positive, driven by the essential nature of cardiovascular care and continuous technological advancements in the field.

Research Methodology - How this research was conducted

The research methodology for this cardiovascular devices market analysis involved a comprehensive approach combining primary and secondary research methods. Primary research included interviews with industry experts, healthcare professionals, and key opinion leaders to gather insights on market trends, technological developments, and future projections. Secondary research involved extensive analysis of industry reports, company annual reports, regulatory databases, and scientific publications. Market size and growth projections were derived using both top-down and bottom-up approaches, considering factors such as disease prevalence, device adoption rates, and healthcare expenditure trends. The analysis also incorporated Porter's Five Forces framework and SWOT analysis to provide a comprehensive understanding of the market dynamics. Data triangulation was employed to validate findings and ensure accuracy across different data sources and methodologies.

Research Scope - Coverage and limitations

The research scope for this cardiovascular devices market analysis encompasses the global market with a focus on key regions, device types, end-users, and applications. The study covers the period from 2025 to 2032, with 2025 as the base year. The analysis includes major device categories such as electrocardiography, pacemakers, stents, defibrillators, and cardiac catheters, among others. End-user segments covered include hospitals, ambulatory surgery centers, and cardiac centers. Applications analyzed encompass coronary heart disease, sudden cardiac arrest, stroke, and cerebrovascular heart disease. The research provides insights into market size, growth trends, competitive landscape, and key player strategies. Limitations of the study include the exclusion of certain niche device categories and regional markets with limited available data. Additionally, the analysis may not fully capture the impact of unforeseen global events or rapid technological disruptions that could significantly alter market dynamics.

Key Companies and Recent Developments in the Cardiovascular Devices Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The cardiovascular devices market features several leading companies that have recently made significant announcements and strategic moves. Abbott has been focusing on expanding its structural heart portfolio, with recent approvals for advanced transcatheter heart valve technologies. B. Braun Melsungen AG has announced partnerships to enhance its vascular access solutions and expand its presence in emerging markets. BD has been investing in digital health integration for its vascular access products, with new smart IV catheter systems. Biosense Webster (Johnson and Johnson) has launched next-generation mapping systems for electrophysiology procedures, incorporating artificial intelligence capabilities. Boston Scientific Corporation has received regulatory approvals for its latest drug-eluting stent technologies and has announced strategic acquisitions to strengthen its position in the atherectomy market. Edwards Lifesciences Corporation has expanded its critical care monitoring portfolio with new hemodynamic monitoring solutions. General Electric Company has announced advancements in cardiac imaging technologies, integrating AI for improved diagnostic accuracy. Koninklijke Philips N.V has launched integrated cardiac care solutions combining imaging and monitoring capabilities. Medtronic has received approvals for its next-generation pacemaker technologies and has announced partnerships for remote patient monitoring solutions. Siemens AG has introduced advanced cardiac MRI systems with improved workflow efficiency. These developments reflect the industry's focus on innovation, digital integration, and expanding treatment options for cardiovascular diseases.