Electronic Health Record Market Overview - Definition, scope, and significance

Electronic Health Records (EHRs) represent a digital transformation of traditional paper-based medical records, serving as comprehensive repositories of patient health information that can be shared across different healthcare settings. These systems encompass a patient's medical history, diagnoses, medications, treatment plans, immunization dates, allergies, radiology images, and laboratory test results in a standardized format. The scope of EHRs extends beyond simple record-keeping to include clinical decision support systems, patient portals, and integrated billing functionalities that streamline administrative workflows. The significance of EHRs lies in their ability to improve healthcare quality, reduce medical errors, enhance patient safety, and facilitate coordinated care delivery across multiple providers and healthcare organizations. As healthcare systems worldwide shift toward value-based care models, EHRs have become essential infrastructure for data-driven clinical decision-making and population health management.

Electronic Health Record Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The EHR market is primarily driven by increasing government initiatives and incentives promoting digital health adoption, rising healthcare expenditure, growing demand for integrated healthcare systems, and the need to reduce medical errors through better documentation. The COVID-19 pandemic has accelerated digital transformation in healthcare, creating unprecedented demand for remote patient monitoring and telehealth integration with EHR systems. However, the market faces significant restraints including high implementation costs, interoperability challenges between different EHR systems, data security and privacy concerns, and resistance from healthcare professionals due to workflow disruption. Key challenges include achieving seamless data exchange across disparate systems, managing the complexity of healthcare regulations, and addressing the shortage of IT professionals with healthcare domain expertise. Opportunities exist in emerging markets with underdeveloped healthcare IT infrastructure, the integration of artificial intelligence and machine learning capabilities, expansion of cloud-based solutions, and the growing demand for mobile EHR applications that support remote care delivery.

Electronic Health Record Market Growth Trends - Current and emerging trends shaping the market

The EHR market is experiencing several transformative trends that are reshaping healthcare delivery and data management. Cloud-based EHR solutions are gaining significant traction due to their scalability, lower upfront costs, and easier maintenance compared to on-premise systems. The integration of artificial intelligence and machine learning is enabling predictive analytics, automated documentation, and clinical decision support that enhances diagnostic accuracy and treatment outcomes. Patient engagement is becoming increasingly important, driving the development of sophisticated patient portals that allow individuals to access their health records, schedule appointments, and communicate with healthcare providers. Interoperability initiatives such as Fast Healthcare Interoperability Resources (FHIR) are gaining momentum to enable seamless data exchange between different healthcare systems and applications. Additionally, the rise of value-based care models is pushing healthcare organizations to adopt EHR systems that can capture quality metrics and support population health management initiatives.

COVID-19 Impact on the Electronic Health Record Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has acted as a catalyst for EHR market growth, accelerating digital transformation initiatives across the healthcare industry. Healthcare providers rapidly adopted EHR systems with telehealth capabilities to maintain continuity of care during lockdowns and social distancing measures. The pandemic highlighted the critical need for real-time data sharing and interoperability, leading to increased investment in EHR infrastructure and digital health solutions. Remote patient monitoring capabilities integrated with EHR systems gained prominence as healthcare organizations sought to manage COVID-19 patients outside traditional hospital settings. While the initial phase saw disruptions in routine healthcare services and delayed EHR implementations, the market demonstrated remarkable resilience and adaptation. The recovery trajectory shows sustained growth as healthcare organizations recognize the importance of digital infrastructure for future pandemic preparedness and the delivery of hybrid care models combining in-person and virtual services.

Electronic Health Record Market Competitive Landscape - Major competitors and market consolidation

The EHR market exhibits a moderately consolidated competitive landscape with several dominant players holding significant market share while numerous smaller vendors serve niche segments. Major competitors include established healthcare IT companies with comprehensive product portfolios and strong customer relationships, as well as specialized EHR vendors focusing on specific healthcare settings or functionalities. The market has witnessed significant consolidation through mergers and acquisitions as larger companies seek to expand their capabilities, enter new geographic markets, and achieve economies of scale. Competition is primarily based on product functionality, ease of use, interoperability, customer support, and total cost of ownership. Vendors are increasingly differentiating themselves through advanced analytics capabilities, user experience design, and integration with emerging technologies such as artificial intelligence and blockchain. The competitive intensity is further heightened by the entry of technology giants into the healthcare IT space, bringing substantial resources and innovation capabilities to challenge traditional EHR providers.

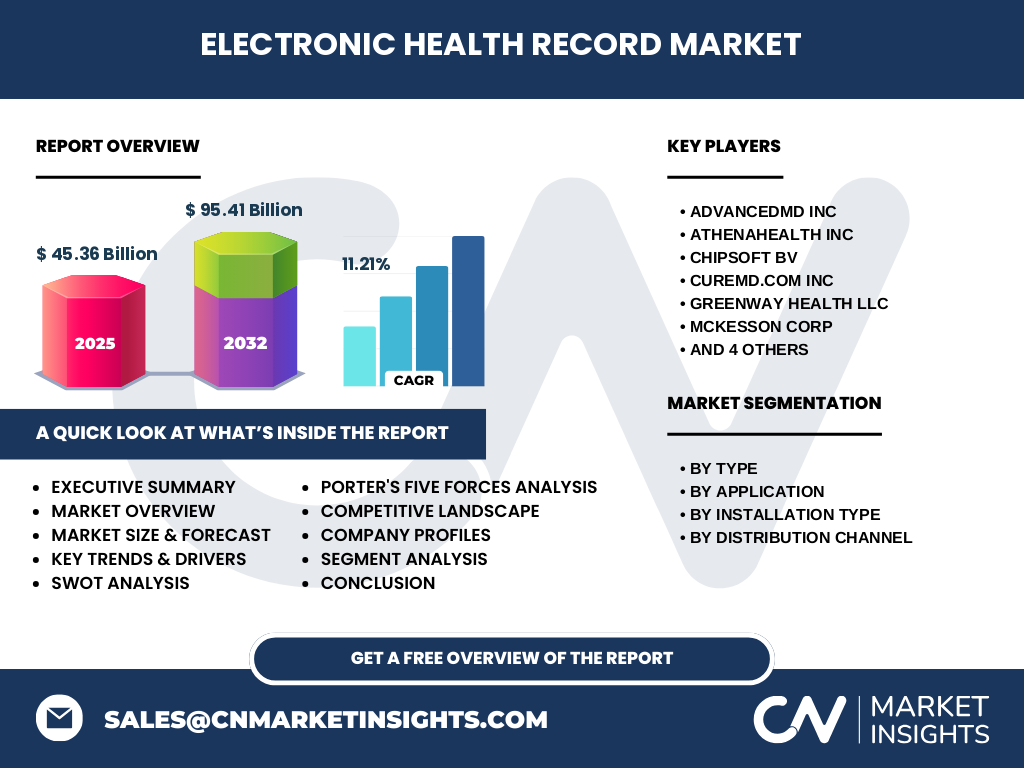

Executive Summary - High-level overview and key findings about Electronic Health Record Market

The global Electronic Health Record market demonstrates robust growth potential with a projected compound annual growth rate of 11.21% from 2025 to 2032, expanding from USD 45.36 billion to USD 95.41 billion. This growth is driven by increasing digitization of healthcare services, government mandates for electronic record-keeping, and the rising demand for integrated healthcare solutions. The market segmentation reveals diverse opportunities across acute care, ambulatory care, and post-acute care settings, with applications spanning clinical records, administrative tasks, physician support, and patient engagement. Cloud-based deployment models are gaining preference due to their flexibility and cost-effectiveness, while hospitals and clinics remain the primary distribution channel. Key market participants are focusing on strategic partnerships, product innovations, and geographic expansion to strengthen their market positions. The market faces challenges related to interoperability, data security, and implementation costs, but emerging technologies and supportive regulatory frameworks are creating new avenues for growth and innovation.

Electronic Health Record Market Forecast - Projections for 2025-2032 period

The EHR market is positioned for substantial growth over the forecast period, with market size expanding from USD 45.36 billion in 2025 to USD 95.41 billion by 2032, representing a compound annual growth rate of 11.21%. This growth trajectory reflects the increasing adoption of digital health solutions across healthcare systems globally, driven by technological advancements, regulatory requirements, and changing care delivery models. The forecast period will likely see accelerated adoption in emerging markets as healthcare infrastructure develops and digital literacy improves. Cloud-based solutions are expected to capture an increasing share of the market due to their scalability and lower total cost of ownership. The integration of advanced technologies such as artificial intelligence, machine learning, and natural language processing will drive the evolution of EHR systems from simple record-keeping tools to intelligent platforms that support clinical decision-making and predictive analytics. Regional variations in growth rates will reflect differences in healthcare system maturity, regulatory environments, and economic conditions.

Electronic Health Record Market Size and Share by Segmentation - Breakdown by {segmentData}

The EHR market segmentation reveals distinct growth patterns across different categories. By type, Acute EHR systems dominate the market due to their comprehensive functionality and adoption in large hospital systems, while Ambulatory EHR solutions are experiencing the fastest growth driven by the expansion of outpatient care services and physician practices. Post-Acute EHR systems are gaining traction as healthcare shifts focus to continuum of care and post-hospitalization management. In terms of application, Clinical Records represent the largest segment as they form the core functionality of EHR systems, while Patient Portal applications are showing the highest growth rate as patient engagement becomes a priority. By installation type, Cloud-Based solutions are rapidly gaining market share due to their flexibility, lower upfront costs, and easier scalability compared to On-Premise deployments. The distribution channel analysis shows Hospitals and Clinics as the primary adopters, accounting for the largest market share, followed by Ambulatory Care Centers and Specialty Care Centers that are increasingly recognizing the benefits of integrated EHR systems for improving care coordination and operational efficiency.

Global Electronic Health Record Market Size and Share by Region - Geographic distribution

The global EHR market exhibits significant regional variations in adoption rates, market maturity, and growth potential. North America currently dominates the global market, driven by advanced healthcare infrastructure, favorable regulatory frameworks such as the HITECH Act, and high healthcare expenditure. The region benefits from strong government support for digital health initiatives and the presence of major EHR vendors. Europe represents the second-largest market, with countries like the UK, Germany, and France leading in EHR adoption through national health service initiatives and interoperability frameworks. The Asia-Pacific region is emerging as the fastest-growing market, fueled by increasing healthcare investments, rising chronic disease burden, and government initiatives to digitize healthcare systems in countries like China, India, and Japan. Latin America and the Middle East & Africa regions are at earlier stages of EHR adoption but present significant growth opportunities as healthcare systems modernize and digital transformation accelerates. Regional differences in regulatory requirements, healthcare funding models, and technology infrastructure create diverse market dynamics that vendors must navigate to achieve global success.

Regional Analysis of the Electronic Health Record Market - Detailed regional market performance

Regional analysis of the EHR market reveals distinct characteristics and growth drivers across different geographies. In North America, the market benefits from well-established healthcare IT infrastructure, strong government incentives for EHR adoption, and a mature ecosystem of technology providers and integration partners. The region's focus on value-based care and population health management drives demand for advanced EHR functionalities. Europe's market is characterized by diverse national healthcare systems, with some countries having comprehensive national EHR programs while others are in earlier stages of implementation. The European Union's focus on cross-border healthcare data exchange and data protection regulations shapes market dynamics. The Asia-Pacific region presents a heterogeneous market with developed markets like Australia and Singapore leading in EHR adoption, while emerging economies are rapidly catching up through government-led digital health initiatives. Cultural factors, language diversity, and varying levels of healthcare infrastructure create unique challenges and opportunities in different Asian markets. Latin America and Middle East & Africa regions are experiencing growing EHR adoption driven by improving healthcare infrastructure, increasing healthcare spending, and the need to address healthcare access challenges in underserved areas.

Leading Company Profiles in the Electronic Health Record Market - Industry players and strategies

The EHR market features a mix of established healthcare IT giants and specialized vendors competing for market share through different strategic approaches. AdvancedMD Inc focuses on ambulatory care practices with user-friendly solutions that integrate practice management and EHR functionalities. Athenahealth Inc leverages its cloud-based platform to serve physician practices and smaller healthcare organizations with scalable solutions. ChipSoft BV specializes in innovative EHR solutions with strong focus on user experience and interoperability. CureMD.com Inc targets small to medium-sized practices with cost-effective, comprehensive EHR systems. Greenway Health LLC emphasizes integrated solutions that combine EHR, practice management, and revenue cycle management. McKesson Corp leverages its position as a major healthcare distributor to offer comprehensive EHR solutions to hospital systems. NEXTGEN HEALTHCARE INFORMATION SYSTEM, LLC focuses on ambulatory care with solutions designed for specialty practices. Oracle Corp brings enterprise technology expertise to healthcare IT through strategic acquisitions and platform development. Veradigm Inc emphasizes data-driven insights and connectivity across the healthcare ecosystem. eClinicalWorks LLC serves a broad customer base with scalable solutions and strong focus on emerging markets. These companies employ various strategies including product innovation, strategic partnerships, geographic expansion, and acquisitions to strengthen their market positions.

Porter's Five Forces Analysis of the Electronic Health Record Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the EHR market. The threat of new entrants remains moderate due to high initial capital requirements, complex regulatory compliance, and the need for extensive healthcare domain expertise. However, technology companies with substantial resources can potentially disrupt the market through innovative approaches. The bargaining power of buyers is increasing as healthcare organizations become more sophisticated in their technology evaluations and demand greater interoperability and value for their investments. The bargaining power of suppliers is relatively low for core EHR functionalities but increases for specialized components such as advanced analytics or integration services. The threat of substitute products is emerging from alternative care delivery models and point solutions that address specific healthcare needs without comprehensive EHR systems. Competitive rivalry is intense with numerous players competing on functionality, price, customer service, and innovation. The market is characterized by ongoing consolidation as larger players acquire smaller vendors to expand capabilities and market reach, while also facing pressure from new technologies and changing care delivery models.

SWOT Analysis of the Electronic Health Record Market - Strengths, weaknesses, opportunities, threats

The EHR market demonstrates several key strengths including the essential nature of electronic records in modern healthcare delivery, established regulatory frameworks supporting adoption, proven benefits in improving care quality and efficiency, and the ability to integrate with emerging technologies. However, the market faces significant weaknesses such as interoperability challenges between different systems, high implementation and maintenance costs, resistance to change from healthcare professionals, and concerns about data security and privacy. Opportunities abound in the form of emerging markets with growing healthcare infrastructure, technological advancements enabling new functionalities, increasing focus on patient engagement and consumer health technologies, and the shift toward value-based care models that require comprehensive data analytics capabilities. The market faces threats from evolving cybersecurity risks, changing regulatory requirements that may increase compliance burdens, potential market saturation in developed regions, and competition from alternative care delivery models and specialized point solutions that may reduce the need for comprehensive EHR systems.

Electronic Health Record Market Value Chain Analysis - Industry structure and value flow

The EHR market value chain encompasses multiple stakeholders and activities that create and deliver value to end-users. At the foundation are technology providers and component suppliers who develop the core software, hardware, and integration tools. EHR vendors transform these components into comprehensive solutions through software development, system integration, and value-added services. Implementation partners and system integrators provide critical services including installation, customization, and workflow optimization to ensure successful EHR deployment. Healthcare providers represent the primary customers who purchase and utilize EHR systems to improve clinical and operational outcomes. Supporting services such as training, maintenance, and technical support ensure ongoing system functionality and user satisfaction. Data analytics and business intelligence companies add value by extracting insights from EHR data to support clinical decision-making and operational improvements. Regulatory bodies and standards organizations influence the value chain through compliance requirements and interoperability standards that shape product development and market dynamics. The value flow is increasingly focused on creating integrated ecosystems that connect patients, providers, payers, and other healthcare stakeholders through seamless data exchange and collaborative care models.

Key Investment Insights in the Electronic Health Record Market - Strategic investment recommendations

Investment opportunities in the EHR market are driven by several compelling factors that suggest strong growth potential and attractive returns. The market's projected compound annual growth rate of 11.21% indicates robust expansion that outpaces many other healthcare IT segments. Strategic investments should focus on cloud-based EHR solutions that offer scalability and lower total cost of ownership, as this segment is expected to capture increasing market share. Companies developing advanced analytics capabilities, artificial intelligence integration, and interoperability solutions present attractive investment targets as these technologies become essential differentiators. Emerging markets in Asia-Pacific, Latin America, and Africa offer significant growth potential as healthcare systems modernize and digital transformation accelerates. Investments in companies with strong intellectual property portfolios, established customer relationships, and proven implementation track records are likely to provide more stable returns. The increasing focus on patient engagement and consumer health technologies creates opportunities for investments in companies developing innovative patient portal and mobile health solutions that integrate with EHR systems. Strategic partnerships and acquisitions that enhance product portfolios and expand geographic reach represent key value creation opportunities in this consolidating market.

Electronic Health Record Market Conclusion - Summary and key takeaways

The Electronic Health Record market presents a compelling growth story characterized by technological innovation, regulatory support, and increasing recognition of digital health's importance in modern healthcare delivery. With market size projected to more than double from USD 45.36 billion in 2025 to USD 95.41 billion by 2032, the industry offers substantial opportunities for vendors, investors, and healthcare organizations. The market's evolution from basic record-keeping systems to intelligent platforms supporting clinical decision-making and population health management reflects broader trends in healthcare transformation. Success in this market requires addressing key challenges including interoperability, data security, and user adoption while capitalizing on opportunities presented by emerging technologies, expanding markets, and changing care delivery models. Companies that can provide comprehensive, user-friendly solutions with strong integration capabilities and demonstrate clear value propositions for healthcare providers and patients will be well-positioned to capture market share in this dynamic and growing industry.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology combining primary and secondary research approaches to ensure accuracy and reliability. Secondary research involved extensive analysis of industry reports, company financial statements, regulatory filings, healthcare databases, and academic publications to establish baseline market data and trends. Primary research included interviews with industry experts, healthcare IT executives, and key opinion leaders to validate findings and gain insights into market dynamics, competitive strategies, and future outlook. Market size and forecast calculations were based on bottom-up analysis considering various market segments, regional factors, and growth drivers. Data triangulation was employed to cross-verify information from multiple sources and ensure consistency. The research methodology incorporated both qualitative and quantitative analysis techniques to provide a comprehensive understanding of market opportunities, challenges, and competitive landscape. Regular updates and validation processes were implemented to maintain the relevance and accuracy of the research findings throughout the study period.

Research Scope - Coverage and limitations

This research focuses on the global Electronic Health Record market, providing comprehensive coverage of market size, growth trends, competitive landscape, and regional analysis. The study encompasses various market segments including different types of EHR systems, applications, installation models, and distribution channels. Geographic coverage includes major regions such as North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with detailed analysis of market dynamics in each region. The research timeframe extends from historical data through current market conditions to future projections covering the period from 2025 to 2032. Key companies profiled include major EHR vendors and emerging players that are shaping market competition. The research scope encompasses both quantitative metrics such as market size and growth rates, as well as qualitative insights into market trends, challenges, and opportunities. Limitations of the research include potential variations in data availability across different regions, the rapidly evolving nature of healthcare technology that may impact long-term projections, and the complexity of accurately measuring market share in a fragmented and dynamic industry landscape.

Key Companies and Recent Developments in the Electronic Health Record Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The EHR market features several prominent companies driving innovation and competition through strategic initiatives. AdvancedMD Inc recently announced enhanced telehealth integration capabilities and AI-powered clinical documentation tools to improve provider efficiency. Athenahealth Inc launched new patient engagement features and expanded its cloud-based platform to support larger healthcare organizations. ChipSoft BV introduced advanced interoperability solutions using FHIR standards to enable seamless data exchange across different healthcare systems. CureMD.com Inc unveiled mobile-first EHR applications designed for small practices and solo practitioners. Greenway Health LLC announced strategic partnerships with major health systems to expand its market presence and enhance its integrated care solutions. McKesson Corp completed the acquisition of a leading EHR vendor to strengthen its hospital-focused solutions and expand its technology portfolio. NEXTGEN HEALTHCARE INFORMATION SYSTEM, LLC launched specialized EHR modules for various medical specialties with enhanced workflow optimization. Oracle Corp, following its acquisition of Cerner, announced plans to integrate EHR data with its enterprise cloud platform to create comprehensive healthcare solutions. Veradigm Inc introduced advanced analytics capabilities and expanded its network connectivity to improve care coordination. eClinicalWorks LLC announced new AI-powered virtual assistant features and expanded its presence in emerging markets through strategic partnerships. These developments reflect the industry's focus on innovation, interoperability, and expanding market reach through both organic growth and strategic acquisitions.