Electronic Design Automation Market Overview - Definition, scope, and significance

Electronic Design Automation (EDA) refers to the category of software tools used for designing electronic systems such as integrated circuits and printed circuit boards. The EDA market encompasses a comprehensive suite of applications that enable engineers to design, simulate, verify, and manufacture complex electronic components and systems. These tools are essential for the development of semiconductors, microprocessors, and other electronic devices that power modern technology. The significance of the EDA market lies in its critical role in enabling the semiconductor industry's rapid advancement, supporting innovations in artificial intelligence, 5G communications, automotive electronics, and consumer devices. As electronic devices become increasingly complex and miniaturized, EDA tools have become indispensable for managing the design complexity and ensuring the functionality and reliability of electronic systems.

Electronic Design Automation Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Electronic Design Automation market is primarily driven by the increasing complexity of semiconductor designs, the growing demand for consumer electronics, and the rapid adoption of advanced technologies such as 5G, AI, and IoT. The automotive industry's shift toward electric and autonomous vehicles is creating substantial demand for sophisticated electronic systems, further fueling EDA market growth. However, the market faces restraints including the high cost of EDA tools and the need for specialized expertise to operate these complex software solutions. Challenges include the continuous need for innovation to keep pace with Moore's Law and the integration of emerging technologies into existing EDA frameworks. Opportunities abound in the form of cloud-based EDA solutions, which offer scalability and cost-effectiveness, and in emerging applications such as quantum computing and advanced packaging technologies that require new design methodologies.

Electronic Design Automation Market Growth Trends - Current and emerging trends shaping the market

The Electronic Design Automation market is experiencing several transformative trends that are shaping its evolution. Cloud-based EDA solutions are gaining significant traction, offering designers greater flexibility, collaboration capabilities, and cost efficiency. The integration of artificial intelligence and machine learning into EDA tools is revolutionizing design optimization, enabling faster time-to-market and improved design quality. There is a growing trend toward system-level design and verification, reflecting the increasing complexity of electronic systems that span multiple domains. The market is also witnessing a shift toward open-source EDA tools, driven by the need for customization and cost reduction. Additionally, the emergence of advanced packaging technologies such as 2.5D and 3D ICs is creating new requirements for EDA tools, pushing vendors to develop specialized solutions for these complex design challenges.

COVID-19 Impact on the Electronic Design Automation Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a mixed impact on the Electronic Design Automation market. Initially, the market experienced disruptions due to supply chain interruptions and temporary closures of semiconductor manufacturing facilities. However, the pandemic also accelerated digital transformation across industries, leading to increased demand for electronic devices and, consequently, for EDA tools. The shift to remote work created new opportunities for cloud-based EDA solutions, as design teams needed to collaborate virtually. The recovery trajectory has been robust, with the market showing strong growth as semiconductor foundries and design houses ramped up production to meet the surging demand for electronics in areas such as remote work infrastructure, healthcare technology, and automotive electronics. The pandemic has underscored the critical importance of EDA tools in enabling the rapid development of electronic solutions for emerging challenges.

Electronic Design Automation Market Competitive Landscape - Major competitors and market consolidation

The Electronic Design Automation market is characterized by a relatively concentrated competitive landscape, with a few major players dominating the industry. The market is led by established companies such as Cadence Design Systems, Synopsys, and Mentor Graphics (now part of Siemens), which collectively hold a significant market share. These companies compete on the basis of technological innovation, comprehensive tool suites, and strong customer relationships. The competitive landscape is marked by strategic acquisitions and partnerships, as companies seek to expand their product portfolios and technological capabilities. For instance, the acquisition of Mentor Graphics by Siemens in 2017 was a significant consolidation move that reshaped the competitive dynamics of the market. Other notable players include Keysight Technologies, Zuken, and Aldec, which compete in specific niches or geographic regions. The market also sees competition from emerging players and open-source initiatives, particularly in specialized application areas.

Executive Summary - High-level overview and key findings about Electronic Design Automation Market

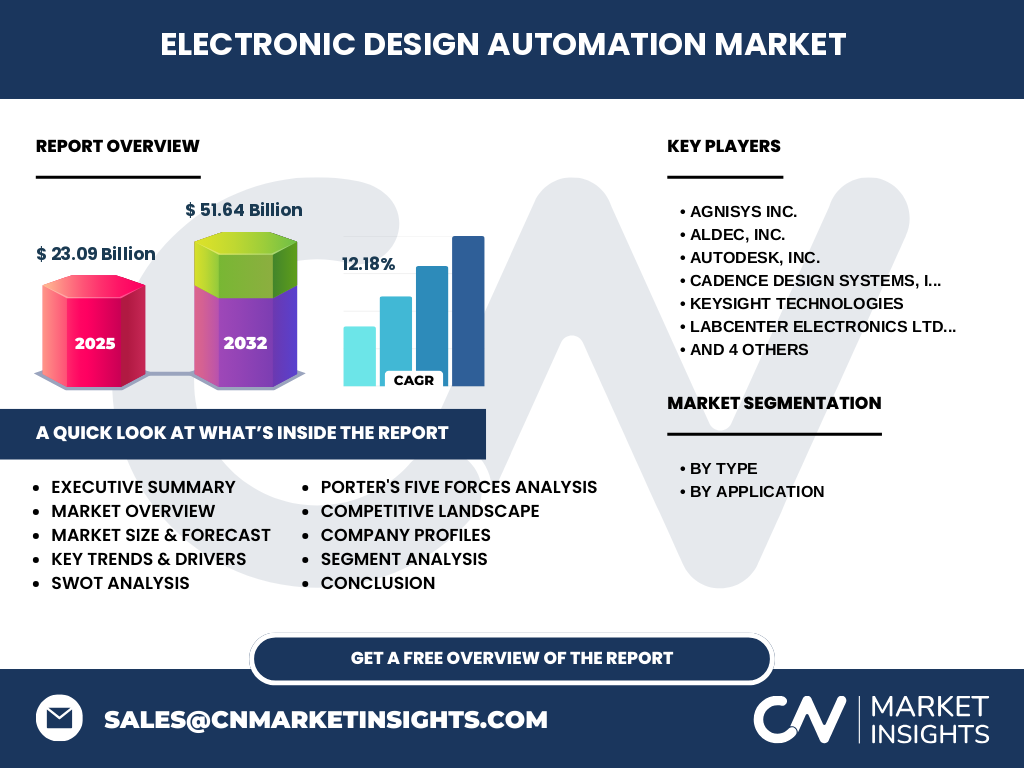

The Electronic Design Automation market is experiencing robust growth, driven by the increasing complexity of electronic systems and the rapid advancement of semiconductor technology. With a market size of $23.09 billion in 2025 and projected to reach $51.64 billion by 2032, the market is growing at a compound annual growth rate of 12.18%. This growth is fueled by the expanding applications of electronics across industries, from consumer devices to automotive and aerospace sectors. The market is segmented by type into CAE, SIP, IC Physical Design & Verification, and PCB & MCM, and by application into aerospace & defense, consumer electronics, telecom, automotive, and industrial sectors. Key players in the market include industry leaders such as Cadence Design Systems, Synopsys, and Mentor Graphics, along with specialized companies like Agnisys and Labcenter Electronics. The market is characterized by technological innovation, strategic partnerships, and a shift toward cloud-based and AI-enhanced solutions, positioning it for continued growth in the coming years.

Electronic Design Automation Market Forecast - Projections for 2025-2032 period

The Electronic Design Automation market is projected to experience substantial growth over the forecast period from 2025 to 2032, with the market size expected to increase from $23.09 billion in 2025 to $51.64 billion by 2032. This represents a compound annual growth rate (CAGR) of 12.18%, indicating a strong and sustained expansion of the market. The forecast is underpinned by several factors, including the continuous advancement of semiconductor technology, the proliferation of electronic devices across industries, and the increasing complexity of electronic systems that require sophisticated design tools. The growth trajectory is expected to be supported by emerging technologies such as 5G, artificial intelligence, and the Internet of Things, which are driving demand for advanced semiconductor designs. Additionally, the shift toward electric and autonomous vehicles is creating new opportunities for EDA tools in the automotive sector. The forecast period is likely to see continued innovation in EDA solutions, with a focus on cloud-based platforms, AI integration, and support for advanced packaging technologies.

Electronic Design Automation Market Size and Share by Segmentation - Breakdown by {segmentData}

The Electronic Design Automation market is segmented by type and application, each contributing differently to the overall market size and share. By type, the market is divided into Computer-Aided Engineering (CAE), Semiconductor Intellectual Property (SIP), IC Physical Design & Verification, and PCB & MCM. CAE tools, which include simulation and analysis software, represent a significant portion of the market due to their critical role in ensuring design functionality and performance. SIP, which provides pre-designed and pre-verified circuit elements, is also a substantial segment, driven by the need for faster time-to-market in semiconductor design. IC Physical Design & Verification tools are essential for the layout and verification of integrated circuits, while PCB & MCM tools cater to the design of printed circuit boards and multi-chip modules. By application, the market serves aerospace & defense, consumer electronics, telecom, automotive, and industrial sectors. The consumer electronics segment is expected to hold a significant share due to the high volume of devices requiring sophisticated electronic designs, followed by the automotive sector, which is experiencing rapid growth due to the electrification and digitalization of vehicles.

Global Electronic Design Automation Market Size and Share by Region - Geographic distribution

The global Electronic Design Automation market exhibits distinct regional characteristics, with varying levels of market size and share across different geographic areas. The Asia-Pacific region, particularly countries like Taiwan, South Korea, China, and Japan, represents a significant portion of the EDA market due to the concentration of semiconductor manufacturing facilities and design houses in these countries. North America, led by the United States, is another major market for EDA tools, driven by the presence of leading EDA companies, a strong semiconductor industry, and significant investments in advanced technologies such as AI and 5G. Europe also contributes substantially to the global EDA market, with countries like Germany, the UK, and France having strong automotive and industrial electronics sectors that drive demand for sophisticated design tools. The rest of the world, including regions like Latin America and the Middle East, while smaller in market size, are experiencing growing adoption of EDA tools as their electronics and semiconductor industries develop. The regional distribution of the EDA market is influenced by factors such as the concentration of semiconductor foundries, the presence of electronics manufacturing hubs, and the level of technological advancement in each region.

Regional Analysis of the Electronic Design Automation Market - Detailed regional market performance

The Electronic Design Automation market demonstrates varied performance across different regions, reflecting the unique characteristics and dynamics of each geographic area. In the Asia-Pacific region, the market is experiencing robust growth, driven by the presence of major semiconductor foundries in Taiwan, South Korea, and China. This region benefits from a strong electronics manufacturing ecosystem, significant government investments in semiconductor technology, and a large consumer electronics market. North America, particularly the United States, is characterized by a mature EDA market with a high concentration of leading EDA companies and a strong focus on innovation. The region's market is driven by advanced applications in aerospace, defense, and high-performance computing. Europe's EDA market is closely tied to its automotive and industrial sectors, with countries like Germany leading in automotive electronics design. The region is also seeing growth in areas such as IoT and industrial automation. Japan maintains a strong position in the EDA market, supported by its advanced semiconductor industry and focus on cutting-edge technologies. Emerging markets in regions like Southeast Asia and India are showing increasing adoption of EDA tools, driven by the growth of their electronics manufacturing sectors and government initiatives to boost domestic semiconductor production.

Leading Company Profiles in the Electronic Design Automation Market - Industry players and strategies

The Electronic Design Automation market is dominated by several key players, each with distinct strategies and market positions. Cadence Design Systems is a leading provider of EDA software, hardware, and services, known for its comprehensive suite of design and verification tools. The company focuses on innovation in areas such as system design enablement and computational software. Synopsys, another major player, offers a wide range of EDA tools and services, with a strong emphasis on silicon design and verification. The company's strategy includes strategic acquisitions to expand its product portfolio and technological capabilities. Mentor Graphics, now part of Siemens, provides a broad spectrum of EDA solutions, particularly strong in PCB and electrical systems design. The company's integration into Siemens has enhanced its position in the industrial automation and automotive sectors. Keysight Technologies specializes in electronic design and test solutions, with a focus on high-frequency and high-speed design. Zuken is known for its expertise in PCB and electrical design software, particularly in the automotive and industrial electronics sectors. Other notable players include Aldec, which specializes in FPGA design and verification tools, and Agnisys, known for its register automation solutions. These companies compete on the basis of technological innovation, comprehensive tool suites, and strong customer relationships, while also exploring new areas such as cloud-based solutions and AI integration.

Porter's Five Forces Analysis of the Electronic Design Automation Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the Electronic Design Automation market. The threat of new entrants is relatively low due to the high barriers to entry, which include the need for significant R&D investment, complex technological expertise, and established relationships with semiconductor companies. The bargaining power of buyers, primarily semiconductor companies and electronics manufacturers, is moderate to high, as they have the option to choose from a limited number of major EDA vendors and can influence pricing and product development. The bargaining power of suppliers is generally low, as EDA companies primarily rely on their own intellectual property and software development capabilities. The threat of substitute products is minimal, given the specialized nature of EDA tools and the lack of viable alternatives for complex electronic design tasks. However, the intensity of competitive rivalry among existing players is high, as the market is dominated by a few major companies that compete aggressively on technological innovation, product features, and customer support. This intense competition drives continuous innovation but also puts pressure on pricing and profit margins.

SWOT Analysis of the Electronic Design Automation Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Electronic Design Automation market reveals several key factors influencing its dynamics. Strengths of the market include the critical importance of EDA tools in semiconductor design, the presence of established players with strong technological capabilities, and the growing demand for advanced electronic systems across industries. The market also benefits from continuous innovation and the integration of emerging technologies such as AI and cloud computing into EDA solutions. However, weaknesses exist, including the high cost of EDA tools, which can be a barrier for smaller companies, and the complexity of these tools, which requires specialized expertise to operate effectively. Opportunities for the market are abundant, including the expansion of electronics into new applications such as electric vehicles and IoT devices, the potential for cloud-based EDA solutions to democratize access to design tools, and the growing demand for advanced packaging technologies. Threats to the market include the cyclical nature of the semiconductor industry, which can lead to fluctuations in demand for EDA tools, and the potential for open-source alternatives to challenge the dominance of established EDA vendors. Additionally, geopolitical tensions and trade restrictions could impact the global supply chain and market dynamics.

Electronic Design Automation Market Value Chain Analysis - Industry structure and value flow

The value chain of the Electronic Design Automation market encompasses several key stages, each contributing to the creation and delivery of EDA solutions. At the foundation of the value chain are the semiconductor foundries and electronics manufacturers, who are the primary customers for EDA tools. These companies require sophisticated design software to create complex integrated circuits and electronic systems. The next stage involves the EDA software developers, such as Cadence, Synopsys, and Mentor Graphics, who create and maintain the design tools. These companies invest heavily in research and development to innovate and improve their product offerings. The value chain also includes semiconductor IP providers, who supply pre-designed and pre-verified circuit elements that can be integrated into larger designs. System integrators and design service companies play a crucial role in implementing EDA solutions for end-users, often providing customization and support services. The distribution of EDA tools is typically handled directly by the software vendors or through authorized resellers. Finally, the value chain extends to educational institutions and training providers, who equip engineers with the skills needed to effectively use EDA tools. This interconnected value chain ensures the continuous flow of innovation and expertise in the EDA market, enabling the development of increasingly complex electronic systems.

Key Investment Insights in the Electronic Design Automation Market - Strategic investment recommendations

The Electronic Design Automation market presents several compelling investment opportunities for stakeholders looking to capitalize on the growth of the semiconductor and electronics industries. Investors should consider focusing on companies that are at the forefront of technological innovation in EDA, particularly those developing solutions for emerging applications such as AI, 5G, and advanced packaging technologies. The shift toward cloud-based EDA solutions represents a significant investment opportunity, as this trend is expected to democratize access to design tools and create new revenue streams for EDA vendors. Investments in companies that are integrating artificial intelligence and machine learning into their EDA offerings could yield substantial returns, as these technologies are poised to revolutionize design optimization and automation. Additionally, the growing demand for EDA tools in the automotive sector, driven by the electrification and digitalization of vehicles, presents a strategic investment opportunity. Investors should also consider the potential of emerging markets, particularly in Asia, where the expansion of semiconductor manufacturing capabilities is creating new demand for EDA solutions. However, it's important to note that investments in the EDA market should be approached with an understanding of the cyclical nature of the semiconductor industry and the intense competition among established players.

Electronic Design Automation Market Conclusion - Summary and key takeaways

The Electronic Design Automation market is poised for significant growth, driven by the increasing complexity of electronic systems and the rapid advancement of semiconductor technology. With a projected market size of $51.64 billion by 2032, growing at a CAGR of 12.18%, the market presents substantial opportunities for both established players and new entrants. The market is characterized by technological innovation, with trends such as cloud-based solutions, AI integration, and advanced packaging technologies shaping its evolution. The competitive landscape is dominated by major players like Cadence, Synopsys, and Mentor Graphics, but also includes specialized companies catering to specific niches. The market's growth is supported by strong demand across various applications, including consumer electronics, automotive, and telecommunications. However, challenges such as the high cost of tools and the need for specialized expertise must be addressed. Overall, the EDA market remains a critical enabler of technological progress in the electronics industry, with a promising outlook for continued expansion and innovation in the coming years.

Research Methodology - How this research was conducted

The research for this Electronic Design Automation market report was conducted using a comprehensive methodology that combines both primary and secondary research techniques. Primary research involved interviews with industry experts, including executives from leading EDA companies, semiconductor manufacturers, and technology analysts. These interviews provided valuable insights into market trends, competitive dynamics, and future outlook. Secondary research was conducted through an extensive review of industry reports, company financial statements, press releases, and technical publications. Market data and statistics were gathered from reputable sources such as industry associations, government publications, and market research databases. The research methodology also included a detailed analysis of patent filings and academic research to identify emerging technologies and innovation trends in the EDA sector. Data triangulation techniques were employed to validate findings and ensure the accuracy of market size and growth projections. The research team also conducted a thorough competitive analysis, examining the strategies and product portfolios of key market players. This multi-faceted approach to research ensures a comprehensive and reliable assessment of the Electronic Design Automation market.

Research Scope - Coverage and limitations

The research scope for this Electronic Design Automation market report encompasses a comprehensive analysis of the global EDA market, including market size, growth trends, competitive landscape, and regional dynamics. The report covers the period from 2025 to 2032, with 2025 as the base year, providing both historical context and future projections. The scope includes detailed segmentation of the market by type (CAE, SIP, IC Physical Design & Verification, PCB & MCM) and by application (aerospace & defense, consumer electronics, telecom, automotive, industrial). The research covers major geographic regions, including North America, Europe, Asia-Pacific, and the rest of the world, providing insights into regional market performance and growth opportunities. The report also includes in-depth profiles of leading companies in the EDA market, along with an analysis of market drivers, restraints, opportunities, and challenges. However, it's important to note that the research scope does not extend to detailed analysis of specific EDA tool functionalities or technical specifications, as these are subject to rapid change and can vary significantly between different product offerings. Additionally, while the report provides a comprehensive overview of the market, it does not include granular data on individual company financials or market share percentages beyond the general competitive landscape.

Key Companies and Recent Developments in the Electronic Design Automation Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Electronic Design Automation market is characterized by continuous innovation and strategic developments among its key players. Cadence Design Systems has been focusing on expanding its system design enablement platform, with recent announcements including advancements in computational software and AI-driven design tools. The company has also formed strategic partnerships to enhance its offerings in areas such as system-on-chip (SoC) design and verification. Synopsys has been actively investing in AI and machine learning technologies, with recent product launches including AI-enhanced design optimization tools and advanced verification solutions. The company has also made strategic acquisitions to strengthen its position in silicon design and security. Mentor Graphics, now part of Siemens, has been leveraging its integration to offer comprehensive solutions for electrical systems design, particularly in the automotive and industrial sectors. Recent developments include enhanced PCB design tools and collaborations with automotive manufacturers to address the growing complexity of vehicle electronics. Keysight Technologies has been focusing on high-frequency and high-speed design solutions, with recent announcements including advanced RF and microwave design tools to support 5G and beyond technologies. Zuken has been expanding its offerings in electrical and wire harness design, with recent product launches aimed at addressing the increasing complexity of automotive and aerospace electrical systems. Aldec has been strengthening its position in FPGA design and verification, with recent developments including enhanced support for emerging FPGA architectures and integration with industry-standard design flows. These companies continue to drive innovation in the EDA market through a combination of organic development, strategic partnerships, and selective acquisitions, ensuring they remain at the forefront of technological advancements in electronic design.