Optical Transceiver Market Overview - Definition, scope, and significance

An optical transceiver is a critical networking device that combines both a transmitter and receiver of optical signals into a single module. These devices convert electrical signals to optical signals for transmission over fiber optic cables and vice versa, enabling high-speed data communication across various network infrastructures. The market encompasses a wide range of form factors, data rates, and applications, serving industries from telecommunications to data centers. As digital transformation accelerates globally, optical transceivers have become essential components for enabling the high-bandwidth, low-latency connections required by modern networks.

Optical Transceiver Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The optical transceiver market is primarily driven by the exponential growth in data traffic, increasing demand for high-speed internet connectivity, and the rapid expansion of cloud computing services. The proliferation of 5G networks, IoT devices, and AI applications creates substantial demand for higher bandwidth solutions. However, the market faces challenges including high initial costs, complex installation requirements, and compatibility issues across different network architectures. Opportunities abound in emerging technologies like silicon photonics, coherent optics, and the development of transceivers supporting data rates exceeding 400 Gbps. The transition toward disaggregated network architectures also presents significant growth potential for modular optical solutions.

Optical Transceiver Market Growth Trends - Current and emerging trends shaping the market

The optical transceiver market is experiencing several transformative trends that are reshaping the industry landscape. There is a clear migration toward higher data rate transceivers, with 400G and 800G solutions gaining traction in data centers and telecom networks. The adoption of pluggable coherent optics is accelerating, enabling more flexible network architectures. Additionally, there is growing demand for energy-efficient transceivers as sustainability becomes a priority. The market is also witnessing increased integration of advanced signal processing capabilities and the emergence of AI-driven network optimization. Form factor innovation continues with the development of smaller, more efficient designs like OSFP and QSFP-DD that support higher port densities.

COVID-19 Impact on the Optical Transceiver Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the optical transceiver supply chain due to factory closures, logistics challenges, and workforce limitations. However, the crisis paradoxically accelerated demand in certain segments, particularly data center interconnects and broadband infrastructure, as remote work and digital services surged. The market demonstrated resilience with a V-shaped recovery pattern, driven by the essential nature of digital connectivity. Looking forward, the pandemic has permanently elevated the importance of robust digital infrastructure, creating sustained demand for optical transceivers. Companies have adapted by diversifying supply chains and increasing automation to mitigate future disruptions.

Optical Transceiver Market Competitive Landscape - Major competitors and market consolidation

The optical transceiver market features a mix of established networking giants and specialized optical component manufacturers competing for market share. The competitive landscape is characterized by continuous innovation, strategic partnerships, and occasional mergers and acquisitions. Companies are differentiating through technological leadership in areas like silicon photonics integration, power efficiency, and form factor innovation. The market shows signs of consolidation as larger players acquire specialized technology firms to enhance their product portfolios. Competition is particularly intense in the high-growth segments of 400G+ transceivers and coherent optics, where technological barriers to entry remain significant.

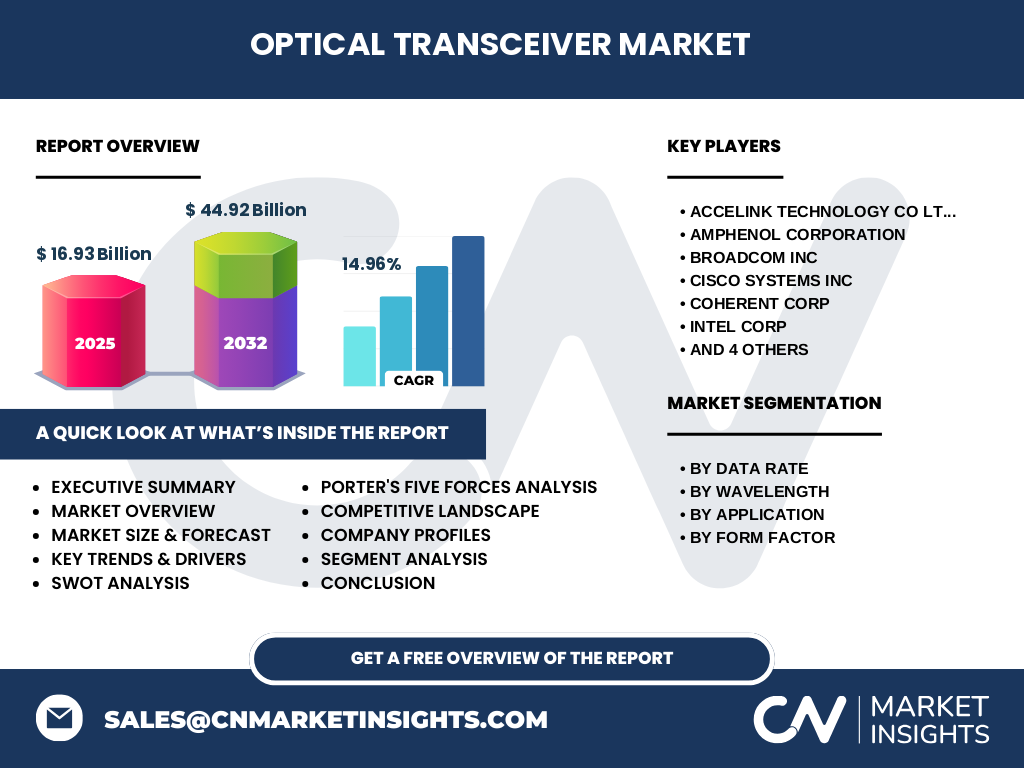

Executive Summary - High-level overview and key findings about Optical Transceiver Market

The optical transceiver market is positioned for substantial growth, with market value projected to increase from 16.93 Billion in 2025 to 44.92 Billion by 2032, representing a robust CAGR of 14.96%. This growth is driven by the escalating demand for high-speed data transmission across telecommunications, data centers, and enterprise networks. The market is witnessing a clear shift toward higher data rate solutions, with transceivers exceeding 100 Gbps gaining prominence. Data centers represent the largest application segment, while the QSFP series dominates the form factor category. The Asia-Pacific region leads in market share, supported by strong telecommunications infrastructure development and data center expansion.

Optical Transceiver Market Forecast - Projections for 2025-2032 period

The optical transceiver market is forecasted to experience significant expansion during the 2025-2032 period, growing from 16.93 Billion to 44.92 Billion. This represents a compound annual growth rate of 14.96%, indicating strong and sustained market momentum. The forecast reflects continued demand across all major segments, with particular emphasis on higher data rate solutions and advanced form factors. The telecommunications sector is expected to show robust growth alongside data centers, driven by 5G deployment and cloud infrastructure expansion. Regional growth will be led by Asia-Pacific, followed by steady expansion in North America and Europe, while emerging markets present new opportunities for market participants.

Optical Transceiver Market Size and Share by Segmentation - Breakdown by {segmentData}

The optical transceiver market segmentation reveals distinct growth patterns across different categories. By data rate, the 41 Gbps to 100 Gbps segment currently dominates, though the more than 100 Gbps category is experiencing the fastest growth. In terms of wavelength, the 1550 nm band holds the largest share due to its prevalence in long-haul telecommunications. Data centers represent the largest application segment, accounting for significant market share driven by cloud service provider demand. The QSFP series leads the form factor segment due to its versatility and widespread adoption across various network applications. These segmentation dynamics highlight the market's evolution toward higher performance and more specialized solutions.

Global Optical Transceiver Market Size and Share by Region - Geographic distribution

The global optical transceiver market exhibits distinct regional characteristics, with Asia-Pacific commanding the largest market share due to extensive telecommunications infrastructure and data center development in countries like China, Japan, and South Korea. North America follows as the second-largest region, driven by substantial cloud service provider presence and advanced network infrastructure. Europe represents a mature but steady-growth market, while Latin America and the Middle East & Africa are emerging markets showing increasing adoption of optical networking solutions. The regional distribution reflects varying stages of digital infrastructure development, with developed regions focusing on capacity expansion and emerging markets prioritizing initial network buildouts.

Regional Analysis of the Optical Transceiver Market - Detailed regional market performance

Regional market dynamics vary significantly across different geographies. Asia-Pacific leads with the highest growth rate, fueled by massive investments in 5G networks, data centers, and broadband infrastructure. China dominates this region, accounting for a substantial portion of market demand. North America shows steady growth driven by cloud computing expansion and advanced telecommunications networks, with the United States representing the primary market. Europe demonstrates stable growth with a focus on network modernization and digital transformation initiatives. Emerging regions including Latin America, Middle East, and Africa are experiencing accelerated adoption as governments prioritize digital infrastructure development, though from a smaller base compared to mature markets.

Leading Company Profiles in the Optical Transceiver Market - Industry players and strategies

The optical transceiver market features several prominent players with distinct strategic approaches. Cisco Systems leverages its extensive networking ecosystem to integrate optical solutions across its product portfolio. Intel focuses on silicon photonics innovation to drive performance improvements. Lumentum Holdings emphasizes advanced manufacturing capabilities and R&D investment. Sumitomo Electric Industries leverages its materials science expertise to develop high-performance optical components. Broadcom pursues a comprehensive portfolio strategy across networking semiconductors. These companies differentiate through technological innovation, vertical integration, and strategic partnerships to maintain competitive advantages in this rapidly evolving market.

Porter's Five Forces Analysis of the Optical Transceiver Market - Competitive forces assessment

The optical transceiver market exhibits moderate to high competitive intensity across Porter's Five Forces framework. The threat of new entrants remains moderate due to significant capital requirements and technical expertise needed for optical component manufacturing. Supplier bargaining power is relatively high given the specialized nature of optical components and limited supplier base for certain materials. Buyer bargaining power varies, with large cloud service providers wielding significant influence while smaller enterprises have less negotiating leverage. The threat of substitutes exists but is limited, as fiber optic solutions remain superior for high-speed, long-distance transmission. Competitive rivalry is intense, with numerous players competing on performance, price, and innovation.

SWOT Analysis of the Optical Transceiver Market - Strengths, weaknesses, opportunities, threats

The optical transceiver market demonstrates several key strengths including essential role in digital infrastructure, continuous technological advancement, and established industry standards. Weaknesses include high development costs, complex manufacturing processes, and supply chain vulnerabilities. Significant opportunities exist in emerging applications like 5G backhaul, data center interconnect, and coherent optics for metro networks. Threats include economic downturns affecting infrastructure spending, technological disruption from alternative technologies, and geopolitical tensions impacting global supply chains. The market's fundamental strength lies in the irreplaceable nature of optical solutions for high-speed data transmission, providing a solid foundation for continued growth despite challenges.

Optical Transceiver Market Value Chain Analysis - Industry structure and value flow

The optical transceiver value chain encompasses multiple stages from raw material suppliers through to end-users. The chain begins with suppliers of specialized materials including semiconductors, optical components, and packaging materials. These feed into manufacturing facilities where optical engines, transceivers, and modules are produced. Component manufacturers supply original equipment manufacturers who integrate these into complete systems. Distributors and system integrators then deliver solutions to end-users across telecommunications, data centers, and enterprise networks. Value is added at each stage through technological innovation, performance optimization, and service integration, with the highest value concentration occurring in advanced module manufacturing and system integration.

Key Investment Insights in the Optical Transceiver Market - Strategic investment recommendations

Strategic investment opportunities in the optical transceiver market center on several key areas. Investors should focus on companies developing next-generation technologies including silicon photonics, coherent optics, and transceivers supporting 800G and beyond. The data center segment presents particularly attractive investment potential given sustained cloud infrastructure expansion. Geographic diversification into high-growth regions like Asia-Pacific offers exposure to emerging market opportunities. Vertical integration strategies that combine component manufacturing with system integration provide competitive advantages. Additionally, investments in companies with strong R&D capabilities and intellectual property portfolios are well-positioned to capture value from technological advancements driving market growth.

Optical Transceiver Market Conclusion - Summary and key takeaways

The optical transceiver market is experiencing robust growth driven by escalating demand for high-speed data transmission across telecommunications, data centers, and enterprise networks. With market value projected to nearly triple from 16.93 Billion to 44.92 Billion by 2032 at a CAGR of 14.96%, the industry presents significant opportunities for stakeholders. Key trends include migration toward higher data rates, particularly solutions exceeding 100 Gbps, and the dominance of the QSFP form factor. Data centers represent the largest application segment, while Asia-Pacific leads regional growth. Success in this market requires continuous innovation, strategic partnerships, and the ability to address evolving customer requirements for performance, power efficiency, and form factor optimization.

Research Methodology - How this research was conducted

This market research was conducted through a comprehensive methodology combining primary and secondary research approaches. Primary research involved interviews with industry experts, manufacturers, and end-users to gather firsthand insights on market dynamics, technological trends, and growth drivers. Secondary research encompassed analysis of industry reports, company financial statements, technical publications, and market databases to validate findings and establish quantitative metrics. The research employed both top-down and bottom-up approaches to estimate market size and forecast growth across different segments and regions. Data triangulation techniques were used to ensure accuracy and reliability of the findings presented in this report.

Research Scope - Coverage and limitations

This research report covers the global optical transceiver market from 2025 to 2032, focusing on key segments including data rate, wavelength, application, and form factor. The scope encompasses major geographic regions with detailed analysis of market dynamics, competitive landscape, and growth trends. Limitations include the availability of certain proprietary data from private companies and potential variations in regional reporting standards. The forecast period extends through 2032, providing a comprehensive view of market evolution. While the report provides extensive coverage of market segments and key players, it focuses primarily on commercially available technologies and does not extensively cover experimental or emerging technologies still in development phases.

Key Companies and Recent Developments in the Optical Transceiver Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The optical transceiver market features several leading companies driving innovation and market development. Cisco Systems continues to expand its optical portfolio with new 400G and 800G solutions optimized for data center and service provider applications. Intel has made significant progress in silicon photonics integration, announcing advancements in manufacturing processes that improve performance and reduce power consumption. Lumentum Holdings recently launched next-generation tunable transceivers with enhanced wavelength flexibility. Sumitomo Electric Industries introduced new CFP2 solutions supporting higher data rates for long-haul applications. These companies, along with others in the market, are actively pursuing strategic partnerships and technological innovations to strengthen their market positions and address evolving customer requirements for higher performance and efficiency.