Aerospace Forging Market Overview - Definition, scope, and significance

Aerospace forging refers to the manufacturing process of shaping metal components for aircraft and aerospace applications through compressive forces, typically using hammers or presses. This process creates high-strength, durable parts that meet the stringent safety and performance requirements of the aerospace industry. The aerospace forging market encompasses the production of critical components such as turbine discs, shafts, rotors, and fan cases for both commercial and military aircraft. The significance of this market lies in its essential role in ensuring aircraft safety, performance, and reliability, as forged components provide superior mechanical properties compared to other manufacturing methods. With the global aviation industry experiencing steady growth and increasing demand for fuel-efficient aircraft, the aerospace forging market plays a crucial role in supporting the expansion of air travel and aerospace manufacturing worldwide.

Aerospace Forging Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The aerospace forging market is driven by several key factors, including the growing demand for commercial aircraft, increasing military spending, and the need for lightweight, fuel-efficient components. The expansion of the global middle class and rising air passenger traffic continue to fuel demand for new aircraft, directly benefiting the forging industry. However, the market faces restraints such as high initial capital investment requirements, stringent regulatory standards, and the cyclical nature of the aerospace industry. Challenges include maintaining consistent quality standards, managing supply chain complexities, and adapting to evolving material requirements. Opportunities exist in the development of advanced materials like titanium alloys and aluminum composites, as well as in expanding into emerging markets and supporting the growing urban air mobility sector. The increasing focus on sustainability and reduced carbon emissions also presents opportunities for innovation in forging processes and materials.

Aerospace Forging Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the aerospace forging market include the increasing adoption of additive manufacturing techniques in conjunction with traditional forging processes, enabling more complex geometries and reduced material waste. There is a growing trend toward the use of titanium and advanced aluminum alloys to reduce aircraft weight while maintaining structural integrity. The market is also witnessing increased automation and digitalization in forging operations, improving efficiency and quality control. Emerging trends include the development of smart forging technologies with real-time monitoring capabilities, the integration of artificial intelligence for process optimization, and the growing focus on sustainable manufacturing practices. The shift toward electric aircraft and urban air mobility solutions is creating new opportunities for specialized forging applications. Additionally, the trend toward globalization of aerospace supply chains is influencing market dynamics and competitive strategies.

COVID-19 Impact on the Aerospace Forging Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant negative impact on the aerospace forging market, primarily due to the sharp decline in air travel demand and subsequent reduction in aircraft production rates. Airlines grounded fleets, canceled orders, and deferred deliveries, leading to decreased demand for forged components. Manufacturing facilities faced temporary shutdowns, supply chain disruptions, and workforce challenges during the pandemic's peak. However, the market has shown resilience and is on a recovery trajectory as air travel demand gradually returns and aircraft manufacturers resume production at higher rates. The recovery is supported by government stimulus packages, vaccine rollouts, and the industry's adaptation to new safety protocols. Looking ahead, the pandemic has accelerated certain trends such as digitalization and supply chain localization, which may benefit the aerospace forging market in the long term.

Aerospace Forging Market Competitive Landscape - Major competitors and market consolidation

The aerospace forging market features a mix of large multinational corporations and specialized regional players, creating a moderately consolidated competitive landscape. Major competitors include established aerospace manufacturers with forging capabilities, such as Arconic Inc and Bharat Forge Limited, alongside specialized forging companies like All Metals & Forge Group and Somers Forge Ltd. The market has seen some consolidation through mergers and acquisitions as companies seek to expand their capabilities and market presence. Competition is based on factors such as technical expertise, quality certifications, production capacity, and the ability to meet stringent aerospace standards. Companies are increasingly focusing on developing strategic partnerships with aircraft manufacturers and investing in advanced technologies to maintain their competitive edge. The competitive landscape is also influenced by regional dynamics, with certain companies holding strong positions in specific geographic markets.

Executive Summary - High-level overview and key findings about Aerospace Forging Market

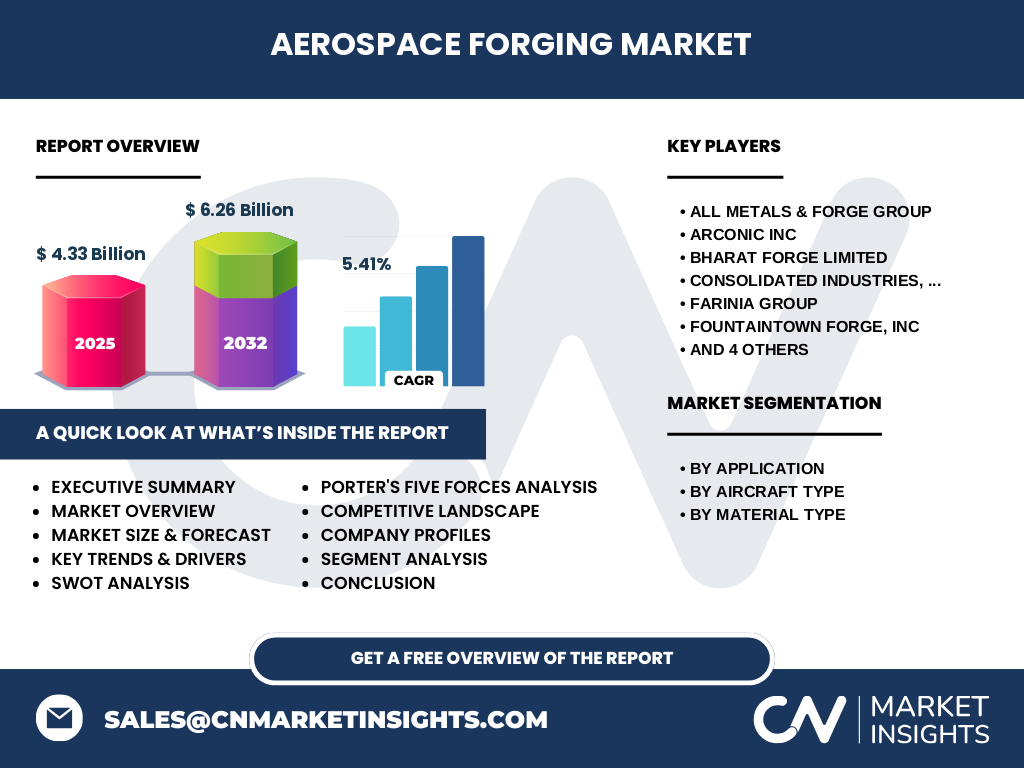

The aerospace forging market represents a critical segment of the aerospace manufacturing industry, providing essential components for aircraft and spacecraft applications. With a market size of $4.33 billion in 2025 and projected growth to $6.26 billion by 2032, the market demonstrates steady expansion driven by increasing aircraft production rates and technological advancements. The market is characterized by its focus on high-strength materials, particularly titanium, stainless steel, and aluminum alloys, serving applications in rotors, turbine discs, shafts, and fan cases. Key trends include the adoption of advanced materials, automation in manufacturing processes, and the integration of digital technologies. Despite challenges posed by the COVID-19 pandemic, the market shows resilience and is on a recovery path. The competitive landscape features both established players and specialized forging companies, with opportunities emerging in new aircraft programs and advanced material applications.

Aerospace Forging Market Forecast - Projections for 2025-2032 period

The aerospace forging market is projected to experience steady growth over the forecast period from 2025 to 2032, with a compound annual growth rate (CAGR) of 5.41%. Starting from a market size of $4.33 billion in 2025, the market is expected to reach $6.26 billion by 2032. This growth is driven by several factors, including the recovery of the commercial aviation sector, increased defense spending, and the introduction of new aircraft programs. The forecast period will likely see continued demand for lightweight materials and advanced forging techniques to meet fuel efficiency requirements. Regional variations in growth rates are expected, with Asia-Pacific and North America leading the expansion due to their strong aerospace manufacturing bases. The market will also be influenced by technological advancements, regulatory changes, and evolving customer preferences for more efficient and environmentally friendly aircraft components.

Aerospace Forging Market Size and Share by Segmentation - Breakdown by {segmentData}

The aerospace forging market can be segmented by application, aircraft type, and material type, each contributing differently to the overall market size and share. By application, the market is divided into rotors, turbine discs, shafts, and fan cases, with turbine discs and shafts typically representing the largest segments due to their critical role in aircraft engines. In terms of aircraft type, the market serves both fixed-wing and rotary-wing aircraft, with fixed-wing aircraft dominating the market share due to the larger commercial aviation sector. By material type, titanium leads the segmentation due to its superior strength-to-weight ratio and corrosion resistance, followed by stainless steel and aluminum alloys. The material choice often depends on the specific application requirements, with titanium being preferred for high-stress components and aluminum alloys for weight-sensitive applications. Each segment's growth rate may vary based on technological advancements and changing industry requirements.

Global Aerospace Forging Market Size and Share by Region - Geographic distribution

The global aerospace forging market exhibits varying growth patterns and market shares across different regions. North America, particularly the United States, holds a significant share of the market due to its strong aerospace manufacturing base, presence of major aircraft manufacturers, and advanced technological capabilities. Europe follows as another major market, driven by its established aerospace industry and increasing defense spending. The Asia-Pacific region is expected to show the highest growth rate during the forecast period, fueled by increasing aircraft production, rising air passenger traffic, and growing defense budgets in countries like China and India. The Middle East and Latin America represent emerging markets with potential for growth, supported by investments in aviation infrastructure and fleet expansion. Regional market dynamics are influenced by factors such as government policies, economic conditions, and the presence of aerospace manufacturing clusters.

Regional Analysis of the Aerospace Forging Market - Detailed regional market performance

Regional analysis of the aerospace forging market reveals distinct characteristics and growth patterns across different geographic areas. North America, led by the United States, maintains its position as a dominant region due to the presence of major aircraft manufacturers like Boeing and a well-established supply chain. The region benefits from advanced technological infrastructure and significant defense spending. Europe, with countries like France, Germany, and the UK, shows steady growth supported by companies like Airbus and a strong focus on aerospace innovation. The Asia-Pacific region demonstrates the most dynamic growth, driven by increasing aircraft orders, expanding commercial aviation sectors in China and India, and growing defense capabilities. Countries like Japan and South Korea contribute through their advanced manufacturing technologies. Emerging regions in the Middle East and Latin America are gradually increasing their market share through investments in aviation infrastructure and the establishment of local aerospace manufacturing capabilities.

Leading Company Profiles in the Aerospace Forging Market - Industry players and strategies

The aerospace forging market features several key players with distinct capabilities and market strategies. Arconic Inc stands out as a major player with extensive experience in titanium and aluminum forging for aerospace applications. Bharat Forge Limited leverages its global presence and advanced manufacturing capabilities to serve both commercial and defense sectors. All Metals & Forge Group specializes in custom forging solutions with a focus on quality and precision. Consolidated Industries, Inc offers a wide range of forged components for various aircraft systems. Farinia Group brings expertise in both closed-die and open-die forging processes. Fountaintown Forge, Inc focuses on high-strength alloy forgings for critical applications. Mettis Aerospace is known for its advanced manufacturing techniques and materials expertise. Pacific Forge Incorporated serves a diverse range of aerospace customers with its comprehensive forging capabilities. Somers Forge Ltd and Victoria Drop Forgings Co. Ltd contribute with their specialized forging services and long-standing industry experience. These companies differentiate themselves through technological innovation, quality certifications, and strategic partnerships.

Porter's Five Forces Analysis of the Aerospace Forging Market - Competitive forces assessment

Porter's Five Forces analysis of the aerospace forging market reveals the competitive dynamics shaping the industry. The threat of new entrants is relatively low due to high capital requirements, stringent regulatory standards, and the need for specialized technical expertise. Bargaining power of suppliers is moderate, as forging companies rely on specialized raw materials and equipment suppliers, but can often switch between multiple sources. The bargaining power of buyers, primarily aircraft manufacturers, is significant due to their large order volumes and ability to influence pricing and quality standards. The threat of substitute products is low, as forged components offer unique advantages in terms of strength and reliability that are difficult to replicate with alternative manufacturing methods. Competitive rivalry within the industry is moderate to high, with companies competing on factors such as quality, delivery times, technical capabilities, and pricing. The analysis indicates that successful companies in this market must focus on technological innovation, quality assurance, and strong customer relationships to maintain their competitive position.

SWOT Analysis of the Aerospace Forging Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the aerospace forging market reveals several key factors influencing its development. Strengths include the essential nature of forged components in aircraft safety and performance, the industry's technical expertise in working with advanced materials, and established quality control systems. Weaknesses involve high production costs, long lead times for complex components, and vulnerability to aerospace industry cycles. Opportunities exist in the development of new materials and manufacturing processes, expansion into emerging markets, and the growing demand for fuel-efficient aircraft components. Threats include intense competition, price pressure from aircraft manufacturers, potential supply chain disruptions, and the risk of technological obsolescence. The market also faces challenges from environmental regulations and the need to reduce carbon emissions in manufacturing processes. Overall, the SWOT analysis suggests that companies focusing on innovation, efficiency, and strategic partnerships are best positioned to capitalize on market opportunities while mitigating potential threats.

Aerospace Forging Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the aerospace forging market reveals a complex network of activities and stakeholders contributing to the final product. The chain begins with raw material suppliers providing high-quality metals such as titanium, aluminum, and steel alloys. These materials are then processed by forging companies using advanced techniques like closed-die forging, open-die forging, and isothermal forging. The forged components undergo rigorous quality control and testing procedures to meet aerospace standards. Distribution channels involve direct relationships with aircraft manufacturers and their tier suppliers, as well as partnerships with distributors for aftermarket components. Value is added at each stage through technological expertise, quality assurance, and customization capabilities. Supporting activities include research and development for new materials and processes, maintenance of specialized equipment, and compliance with industry certifications. The value chain is characterized by close collaboration between stakeholders and a focus on continuous improvement to meet evolving industry requirements.

Key Investment Insights in the Aerospace Forging Market - Strategic investment recommendations

Investment insights in the aerospace forging market suggest several strategic opportunities for stakeholders. Key areas for investment include advanced manufacturing technologies such as automation and digitalization to improve efficiency and quality control. There is significant potential in developing expertise in emerging materials like titanium aluminides and advanced composites to meet future aircraft requirements. Investments in research and development for sustainable forging processes and recycling technologies align with industry trends toward environmental responsibility. Geographic expansion, particularly in high-growth regions like Asia-Pacific, presents opportunities for market penetration and growth. Strategic partnerships and acquisitions can provide access to new technologies and customer bases. Investments in workforce development and training are crucial to maintain technical expertise in this specialized field. Additionally, companies should consider investments in supply chain resilience and localization to mitigate potential disruptions. The market's steady growth projections and technological advancements make it an attractive sector for long-term investment, particularly for those focusing on innovation and sustainability.

Aerospace Forging Market Conclusion - Summary and key takeaways

The aerospace forging market represents a vital component of the global aerospace industry, characterized by steady growth, technological advancement, and increasing demand for high-performance components. With a projected market size of $6.26 billion by 2032 and a CAGR of 5.41%, the industry shows strong potential for continued expansion. Key takeaways include the market's resilience in the face of challenges such as the COVID-19 pandemic, the importance of advanced materials like titanium and aluminum alloys, and the growing focus on sustainability and efficiency in manufacturing processes. The competitive landscape features a mix of established players and specialized companies, with opportunities for growth through innovation and strategic partnerships. Regional variations in market dynamics highlight the importance of understanding local conditions and adapting strategies accordingly. Overall, the aerospace forging market remains a critical enabler of aircraft performance and safety, with significant opportunities for companies that can meet evolving industry requirements and embrace technological advancements.

Research Methodology - How this research was conducted

The research methodology for this aerospace forging market analysis involved a comprehensive approach combining primary and secondary research techniques. Primary research included interviews with industry experts, including executives from leading forging companies, aerospace manufacturers, and material suppliers. These interviews provided insights into market trends, challenges, and future projections. Secondary research involved analysis of industry reports, company financial statements, technical publications, and regulatory documents. Market data was validated through multiple sources to ensure accuracy and reliability. The research also incorporated analysis of patent filings, trade publications, and industry conferences to identify emerging technologies and market developments. Statistical modeling and forecasting techniques were applied to project market growth and segment performance. The methodology aimed to provide a balanced and objective view of the market, considering both quantitative data and qualitative insights from industry participants.

Research Scope - Coverage and limitations

The research scope for this aerospace forging market analysis encompasses a comprehensive examination of the global market, including market size, growth trends, competitive landscape, and regional dynamics. The study covers key segments such as application types (rotors, turbine discs, shafts, fan cases), aircraft types (fixed-wing and rotary-wing), and material types (titanium, stainless steel, aluminum alloy). The research timeframe extends from 2025 to 2032, with historical data and future projections included. Geographic coverage includes major markets in North America, Europe, Asia-Pacific, and emerging regions. The analysis focuses on commercial and military aerospace applications, excluding other industries that may use forging processes. Limitations of the research include the availability of certain proprietary data, potential variations in regional reporting standards, and the inherent uncertainty in long-term market projections. The study aims to provide a comprehensive overview while acknowledging these limitations and focusing on the most relevant and reliable data sources available.

Key Companies and Recent Developments in the Aerospace Forging Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The aerospace forging market features several key companies that have made significant recent developments and strategic moves. Arconic Inc has focused on expanding its titanium forging capabilities and has announced partnerships to develop next-generation aerospace components. Bharat Forge Limited has made strategic investments in advanced manufacturing technologies and has secured major contracts with leading aircraft manufacturers. All Metals & Forge Group has introduced new product lines focusing on lightweight materials for fuel efficiency. Consolidated Industries, Inc has expanded its production capacity to meet growing demand and has implemented advanced quality control systems. Farinia Group has launched innovative forging processes that reduce material waste and improve component performance. Fountaintown Forge, Inc has announced collaborations with research institutions to develop new alloy compositions. Mettis Aerospace has introduced automation technologies to enhance production efficiency and has expanded its global footprint through strategic acquisitions. Pacific Forge Incorporated has focused on developing specialized forging solutions for emerging aircraft programs. Somers Forge Ltd and Victoria Drop Forgings Co. Ltd have both announced investments in sustainable manufacturing practices and have strengthened their positions in niche market segments. These developments reflect the industry's focus on innovation, efficiency, and meeting evolving customer requirements.