Bio-Implants Market Overview - Definition, scope, and significance

Bio-implants are medical devices designed to replace, support, or enhance biological structures within the human body. These devices are typically made from biocompatible materials that can integrate with living tissue without causing adverse reactions. The bio-implants market encompasses a wide range of products including cardiovascular implants, orthopedic implants, dental implants, and ophthalmic implants, each serving critical medical functions. The significance of this market lies in its ability to improve patient quality of life, restore bodily functions, and address various medical conditions that would otherwise require more invasive treatments or result in permanent disability. As medical technology advances, bio-implants have become increasingly sophisticated, offering better integration with human tissue, improved durability, and enhanced functionality that closely mimics natural biological processes.

Bio-Implants Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The bio-implants market is driven by several key factors including the aging global population, increasing prevalence of chronic diseases, and rising healthcare expenditure. Technological advancements in materials science and manufacturing processes have enabled the development of more effective and longer-lasting implants. Additionally, growing awareness about healthcare options and improved access to medical facilities in developing regions contribute to market growth. However, the market faces restraints such as high costs associated with implant procedures, stringent regulatory requirements for approval, and potential complications or rejection of implants by the human body. Challenges include the need for skilled surgeons, limited reimbursement policies in certain regions, and ethical concerns regarding animal-derived materials. Opportunities exist in emerging markets, development of personalized implants using 3D printing technology, and expanding applications in regenerative medicine and tissue engineering.

Bio-Implants Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the bio-implants market include the increasing adoption of minimally invasive surgical techniques, which reduce recovery time and complications for patients. The integration of smart technologies and sensors into implants is emerging as a significant trend, enabling real-time monitoring of patient health and implant performance. There is also a growing demand for biodegradable implants that naturally dissolve in the body over time, eliminating the need for removal surgeries. The market is witnessing a shift towards personalized medicine, with custom-designed implants tailored to individual patient anatomy becoming more common. Additionally, the use of advanced materials such as bioactive glasses and ceramics that promote better integration with bone tissue is gaining traction. The COVID-19 pandemic has accelerated the adoption of telemedicine and remote monitoring technologies, which are increasingly being integrated with bio-implant systems to enhance patient care and follow-up.

COVID-19 Impact on the Bio-Implants Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the bio-implants market, primarily due to the postponement of elective surgeries and the reallocation of healthcare resources to manage the crisis. Many hospitals and clinics worldwide suspended non-emergency procedures, leading to a temporary decline in implant surgeries across all categories. Supply chain disruptions affected the availability of raw materials and components, causing production delays and inventory shortages. However, the market has shown resilience with a gradual recovery as healthcare systems adapt to the new normal. The pandemic has accelerated the adoption of digital health technologies and telemedicine, which are now being integrated with bio-implant monitoring systems. There is also an increased focus on developing antimicrobial and infection-resistant implants in response to heightened awareness about hospital-acquired infections. The market is expected to regain momentum as vaccination rates increase and healthcare services return to pre-pandemic levels, with a projected growth trajectory extending through 2025 and beyond.

Bio-Implants Market Competitive Landscape - Major competitors and market consolidation

The bio-implants market is characterized by the presence of several major players alongside numerous smaller companies and specialized manufacturers. Key competitors include Medtronic, Stryker Corporation, Zimmer Biomet, Smith & Nephew, and DePuy Synthes, which collectively hold significant market shares across various implant categories. These companies compete based on product innovation, technological advancements, and strategic partnerships. The market has witnessed consolidation through mergers and acquisitions, as larger companies seek to expand their product portfolios and geographic presence. For instance, the acquisition of smaller specialized firms allows major players to incorporate novel technologies and enter niche markets. Competition is intense in developed markets, while emerging economies present opportunities for growth and market penetration. Companies are increasingly focusing on research and development to create next-generation implants with improved biocompatibility, durability, and functionality to maintain their competitive edge.

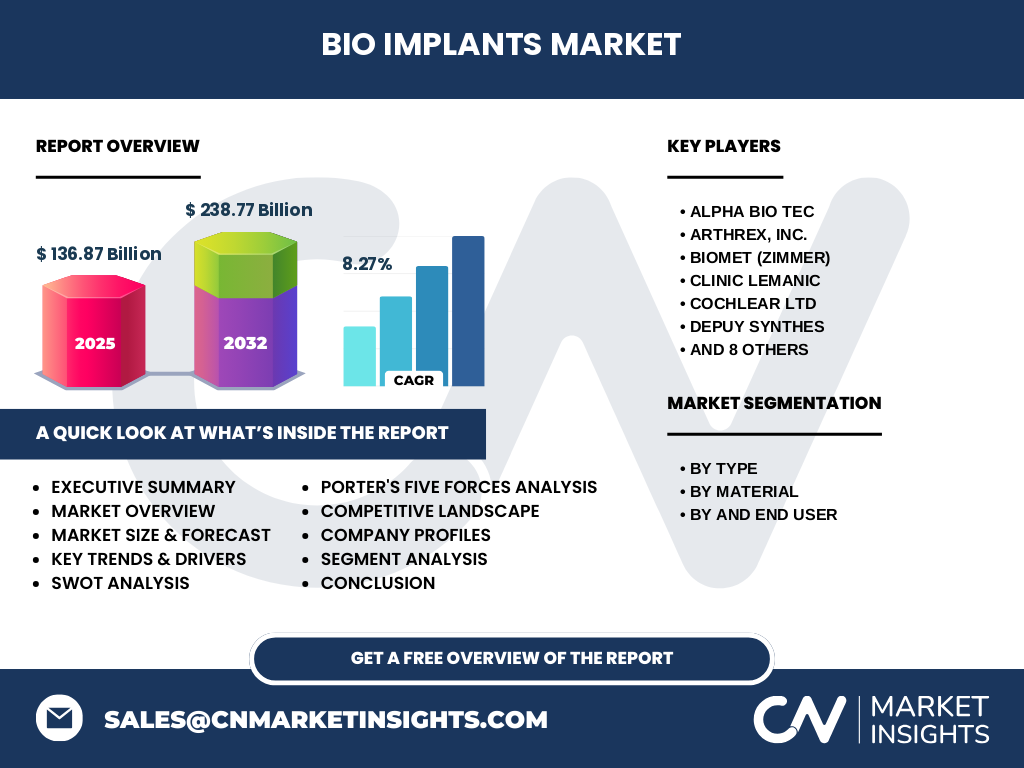

Executive Summary - High-level overview and key findings about Bio-Implants Market

The bio-implants market represents a critical segment of the medical device industry, offering solutions for a wide range of medical conditions across cardiovascular, orthopedic, dental, and ophthalmic applications. With a market size of $136.87 billion in 2025 and a projected growth to $238.77 billion by 2032, the market demonstrates strong potential for expansion at a CAGR of 8.27%. The market is segmented by type, material, and end-user, with cardiovascular and orthopedic implants dominating the product landscape. Hospitals and clinics remain the primary end-users, although ambulatory surgical centers are gaining prominence. The market is driven by demographic trends, technological advancements, and increasing healthcare expenditure, while facing challenges related to regulatory compliance and cost constraints. Key players are focusing on innovation and strategic partnerships to maintain their market positions. The COVID-19 pandemic has temporarily impacted the market but is expected to accelerate certain technological trends and market adaptations.

Bio-Implants Market Forecast - Projections for 2025-2032 period

The bio-implants market is projected to experience substantial growth from 2025 to 2032, with the market size expected to increase from $136.87 billion to $238.77 billion. This growth represents a compound annual growth rate of 8.27% over the forecast period. The cardiovascular implants segment is anticipated to maintain its leading position, driven by the rising prevalence of heart diseases and an aging population. Orthopedic implants are expected to show robust growth due to increasing cases of osteoporosis and arthritis, particularly in developed countries. The dental implants segment is projected to benefit from growing awareness about oral health and cosmetic dentistry. Technological advancements, particularly in materials science and 3D printing, are likely to drive innovation and expand application areas. Emerging markets in Asia-Pacific and Latin America are expected to contribute significantly to growth, supported by improving healthcare infrastructure and rising disposable incomes. The market is also likely to see increased adoption of smart implants with integrated monitoring capabilities.

Bio-Implants Market Size and Share by Segmentation - Breakdown by {segmentData}

The bio-implants market is segmented by type, material, and end-user, each contributing differently to the overall market size and share. By type, cardiovascular implants hold the largest market share due to the high prevalence of cardiovascular diseases globally, followed by orthopedic implants which benefit from an aging population and increasing incidence of bone-related disorders. Dental implants represent a significant and growing segment, driven by increasing awareness about oral health and aesthetic considerations. Ophthalmic implants, while smaller in market share, are experiencing growth due to advancements in cataract surgery and treatment of eye disorders. By material, metals such as titanium and stainless steel dominate the market due to their strength and biocompatibility, while ceramics and polymers are gaining traction for specific applications. By end-user, hospitals and clinics account for the largest share, with ambulatory surgical centers emerging as a growing segment due to the trend towards outpatient procedures and cost-effective treatments.

Global Bio-Implants Market Size and Share by Region - Geographic distribution

The global bio-implants market exhibits varying dynamics across different regions, with North America currently holding the largest market share due to advanced healthcare infrastructure, high healthcare expenditure, and early adoption of innovative technologies. Europe follows as the second-largest market, driven by an aging population and well-established healthcare systems. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, attributed to improving healthcare facilities, rising disposable incomes, and increasing awareness about advanced treatment options in countries like China, India, and Japan. Latin America and the Middle East & Africa regions, while currently smaller in market size, are showing promising growth potential due to improving economic conditions and healthcare investments. Regional differences in regulatory frameworks, reimbursement policies, and cultural attitudes towards medical interventions influence the adoption rates of bio-implants across different geographies.

Regional Analysis of the Bio-Implants Market - Detailed regional market performance

Regional analysis of the bio-implants market reveals distinct characteristics and growth patterns across different geographies. North America, particularly the United States, leads in market share due to its advanced healthcare infrastructure, high per capita healthcare spending, and presence of major market players. The region benefits from favorable reimbursement policies and a strong focus on research and development. Europe, with countries like Germany, France, and the UK at the forefront, shows steady growth driven by an aging population and increasing prevalence of chronic diseases. The Asia-Pacific region, led by China, Japan, and India, is experiencing rapid market expansion due to improving healthcare access, rising middle-class population, and increasing medical tourism. Latin America, with Brazil and Mexico as key markets, is showing gradual growth as healthcare systems modernize. The Middle East & Africa region, while currently smaller, is witnessing increased investment in healthcare infrastructure, particularly in Gulf Cooperation Council countries, creating opportunities for market growth.

Leading Company Profiles in the Bio-Implants Market - Industry players and strategies

The bio-implants market is dominated by several key players, each with distinct strategies and market positions. Medtronic, a global leader, offers a comprehensive portfolio of cardiovascular and orthopedic implants, focusing on innovation and strategic acquisitions to maintain its market leadership. Stryker Corporation has strengthened its position through a diverse product range and emphasis on minimally invasive surgical solutions. Zimmer Biomet specializes in orthopedic and dental implants, leveraging its extensive research capabilities and global distribution network. Smith & Nephew is known for its advanced wound management and orthopedic reconstruction products, with a strong focus on sports medicine. DePuy Synthes, a subsidiary of Johnson & Johnson, offers a wide range of orthopedic and neurological implants, benefiting from the parent company's resources and global reach. Other notable players like Cochlear Ltd, focusing on hearing implants, and Straumann AG, specializing in dental implants, have carved out significant market niches through specialized product offerings and technological expertise.

Porter's Five Forces Analysis of the Bio-Implants Market - Competitive forces assessment

Porter's Five Forces analysis provides insights into the competitive dynamics of the bio-implants market. The threat of new entrants is moderate due to high capital requirements, stringent regulatory approvals, and the need for extensive research and development capabilities. However, technological advancements and emerging markets present opportunities for new players. The bargaining power of buyers, primarily hospitals and healthcare providers, is significant as they seek cost-effective solutions and negotiate based on volume purchases. The bargaining power of suppliers is moderate, with raw material suppliers having some influence, particularly for specialized biocompatible materials. The threat of substitutes is relatively low for established implant categories, but emerging technologies like regenerative medicine and tissue engineering pose potential long-term challenges. Competitive rivalry is intense among major players, characterized by product innovation, strategic partnerships, and geographic expansion. The overall industry attractiveness is moderate to high, driven by market growth potential and technological advancements, despite regulatory challenges and high development costs.

SWOT Analysis of the Bio-Implants Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the bio-implants market reveals several key factors influencing its dynamics. Strengths include advanced technological capabilities, a wide range of product offerings for various medical conditions, and strong distribution networks of major players. The market benefits from increasing healthcare expenditure and growing awareness about treatment options. Weaknesses encompass high costs associated with implant procedures, potential complications and rejection risks, and lengthy regulatory approval processes. The market also faces challenges related to limited reimbursement in certain regions and the need for specialized surgical expertise. Opportunities lie in emerging markets with improving healthcare infrastructure, advancements in personalized medicine and 3D printing technologies, and the development of smart implants with integrated monitoring capabilities. Threats include stringent regulatory requirements, potential economic downturns affecting healthcare spending, and competition from alternative treatment methods or emerging technologies like regenerative medicine. The market must also navigate ethical concerns and potential public perception issues related to certain types of implants.

Bio-Implants Market Value Chain Analysis - Industry structure and value flow

The bio-implants market value chain encompasses several interconnected stages, from raw material sourcing to end-user delivery. The chain begins with raw material suppliers providing biocompatible metals, ceramics, and polymers essential for implant manufacturing. These materials are then processed by component manufacturers who create specialized parts and subassemblies. Medical device manufacturers integrate these components to produce finished implants, incorporating advanced technologies and ensuring compliance with regulatory standards. Distribution networks, including medical distributors and direct sales teams, facilitate the delivery of implants to healthcare providers. Hospitals, clinics, and ambulatory surgical centers serve as the primary end-users, where trained surgeons perform implant procedures. Post-operative care and monitoring represent the final stage of the value chain, with increasing integration of digital health technologies for remote patient monitoring. Value is added at each stage through technological innovation, quality control measures, and the development of specialized expertise. The value chain is characterized by close collaboration between manufacturers, healthcare providers, and research institutions to drive continuous improvement and innovation in implant technologies.

Key Investment Insights in the Bio-Implants Market - Strategic investment recommendations

Investment insights in the bio-implants market suggest several strategic opportunities for stakeholders. The market's projected growth at a CAGR of 8.27% indicates strong potential for long-term investments, particularly in companies with robust research and development capabilities and diverse product portfolios. Emerging technologies such as 3D printing for personalized implants, smart implants with integrated sensors, and advanced biomaterials present attractive investment opportunities. The Asia-Pacific region, with its rapidly growing healthcare sector and increasing adoption of advanced medical technologies, offers significant potential for market expansion and investment. Strategic acquisitions and partnerships can provide access to innovative technologies and new market segments. Investments in digital health integration and telemedicine solutions that complement bio-implant technologies are also promising. However, investors should be mindful of regulatory challenges and the need for substantial capital investment in research and development. Diversification across different implant categories and geographic regions can help mitigate risks associated with market fluctuations and regional economic conditions.

Bio-Implants Market Conclusion - Summary and key takeaways

The bio-implants market represents a dynamic and growing segment of the medical device industry, characterized by technological innovation and increasing demand driven by demographic trends and healthcare advancements. With a market size of $136.87 billion in 2025 and projected growth to $238.77 billion by 2032, the market demonstrates significant potential for expansion. Key drivers include an aging global population, rising prevalence of chronic diseases, and advancements in materials science and manufacturing technologies. While the market faces challenges such as high costs, regulatory hurdles, and potential complications, opportunities in emerging markets and technological innovations present avenues for growth. The competitive landscape is dominated by major players focusing on product innovation and strategic partnerships. The COVID-19 pandemic has temporarily impacted the market but is expected to accelerate certain technological trends. Overall, the bio-implants market is poised for continued growth, driven by ongoing medical advancements and increasing healthcare needs worldwide.

Research Methodology - How this research was conducted

This market research report on the bio-implants market was conducted using a comprehensive methodology that combines primary and secondary research techniques. Primary research involved interviews with industry experts, including medical professionals, researchers, and executives from key market players, to gather insights on market trends, technological developments, and future projections. Secondary research encompassed an extensive review of industry publications, company reports, scientific journals, and regulatory databases to validate and supplement primary findings. Market size and growth projections were derived using both top-down and bottom-up approaches, considering factors such as demographic trends, disease prevalence, and technological advancements. Data triangulation was employed to ensure accuracy and reliability of the information gathered. The research also incorporated Porter's Five Forces analysis and SWOT analysis to provide a comprehensive understanding of the market dynamics. Regional analyses were conducted to account for geographical variations in market performance and growth potential. The methodology ensured a balanced and objective assessment of the bio-implants market, providing stakeholders with reliable insights for decision-making.

Research Scope - Coverage and limitations

The research scope for this bio-implants market report encompasses a comprehensive analysis of the global market, including market size, growth trends, competitive landscape, and regional dynamics. The report covers major implant categories such as cardiovascular, orthopedic, dental, and ophthalmic implants, along with material types and end-user segments. The research includes both established markets in North America and Europe and emerging markets in Asia-Pacific, Latin America, and the Middle East & Africa. The scope extends to analyzing key market drivers, restraints, opportunities, and challenges, as well as providing detailed company profiles of major market players. The research also includes an assessment of technological trends, regulatory frameworks, and investment opportunities within the market. However, the scope is limited to commercially available bio-implants and does not extensively cover experimental or investigational implants still in clinical trials. Additionally, while the report provides regional insights, it may not capture every nuance of local market conditions in all countries. The research focuses on the period from 2025 to 2032, with historical data used for context and trend analysis.

Key Companies and Recent Developments in the Bio-Implants Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The bio-implants market features several key companies that have recently made significant developments and strategic moves. Medtronic has announced advancements in its cardiovascular implant portfolio, including next-generation pacemakers with extended battery life and improved remote monitoring capabilities. Stryker Corporation has launched innovative orthopedic implants incorporating 3D-printed titanium alloys for enhanced osseointegration. Zimmer Biomet has introduced a new line of dental implants featuring surface modifications to promote faster healing and improved bone attachment. Smith & Nephew has expanded its sports medicine portfolio with the acquisition of a specialized implant manufacturer, strengthening its position in minimally invasive surgical solutions. DePuy Synthes has announced a partnership with a leading 3D printing company to develop custom orthopedic implants tailored to individual patient anatomy. Cochlear Ltd has launched its latest hearing implant system with improved sound processing algorithms and wireless connectivity features. Straumann AG has introduced a new range of dental implants with bioactive surface treatments to enhance soft tissue integration. These developments reflect the industry's focus on technological innovation, personalized medicine, and strategic collaborations to maintain competitive advantage and address evolving market needs.