Fiber Cement Siding Market Overview - Definition, scope, and significance

Fiber cement siding is a durable, low-maintenance building material composed of cement, silica, and cellulose fibers that provides an attractive exterior finish for residential and commercial structures. This composite material offers superior weather resistance, fire resistance, and dimensional stability compared to traditional wood or vinyl siding options. The fiber cement siding market encompasses the manufacturing, distribution, and installation of these products across various applications and geographic regions. The significance of this market lies in its ability to address growing demand for sustainable, long-lasting building materials that can withstand diverse climatic conditions while offering aesthetic versatility for modern construction projects.

Fiber Cement Siding Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The fiber cement siding market is primarily driven by increasing construction activities in both residential and commercial sectors, particularly in emerging economies experiencing rapid urbanization. Growing awareness of fire safety regulations and the need for weather-resistant building materials has further accelerated adoption. However, the market faces restraints including higher initial installation costs compared to traditional materials and the requirement for specialized labor for proper installation. Challenges include competition from alternative siding materials and potential environmental concerns related to silica dust during manufacturing and installation. Significant opportunities exist in developing eco-friendly formulations, expanding into emerging markets with rising construction spending, and leveraging technological advancements to create innovative product designs that mimic natural materials while offering superior performance characteristics.

Fiber Cement Siding Market Growth Trends - Current and emerging trends shaping the market

Current market trends indicate a strong shift toward sustainable and energy-efficient building materials, with fiber cement siding positioned as an environmentally responsible choice due to its durability and recyclability. The residential renovation and remodeling segment continues to show robust growth, driven by aging housing stock in developed markets and increasing homeowner preference for low-maintenance exteriors. Emerging trends include the development of ultra-lightweight fiber cement products that reduce installation time and costs, integration of smart building technologies into siding systems, and growing demand for products that replicate the appearance of natural wood or stone while offering enhanced performance. Additionally, manufacturers are increasingly focusing on prefinished and pre-painted options to streamline installation processes and provide consistent quality finishes.

COVID-19 Impact on the Fiber Cement Siding Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the fiber cement siding market through supply chain interruptions, temporary manufacturing shutdowns, and reduced construction activity during lockdowns. However, the market demonstrated remarkable resilience as residential construction and renovation projects accelerated in many regions due to changing lifestyle preferences and increased home improvement spending. The pandemic highlighted the importance of durable, low-maintenance building materials, potentially accelerating long-term adoption of fiber cement siding. As economies recover, the market is experiencing a rebound driven by pent-up demand, government infrastructure stimulus packages, and the continued emphasis on sustainable construction practices. The recovery trajectory suggests sustained growth as construction activities normalize and manufacturers adapt to new operational protocols.

Fiber Cement Siding Market Competitive Landscape - Major competitors and market consolidation

The fiber cement siding market features a mix of global conglomerates and specialized manufacturers competing for market share through product innovation, geographic expansion, and strategic partnerships. Major players include James Hardie Industries Plc, which maintains a dominant position through its extensive product portfolio and strong brand recognition, and Louisiana-Pacific Corporation, known for its comprehensive building solutions. Other significant competitors include CSR Limited, ETEX Group, and Elementia SAB DE CV, each leveraging their regional strengths and manufacturing capabilities. The competitive landscape is characterized by ongoing consolidation through mergers and acquisitions, with larger companies acquiring smaller, innovative firms to expand their technological capabilities and market presence. This consolidation trend is expected to continue as companies seek to achieve economies of scale and strengthen their competitive positions in both mature and emerging markets.

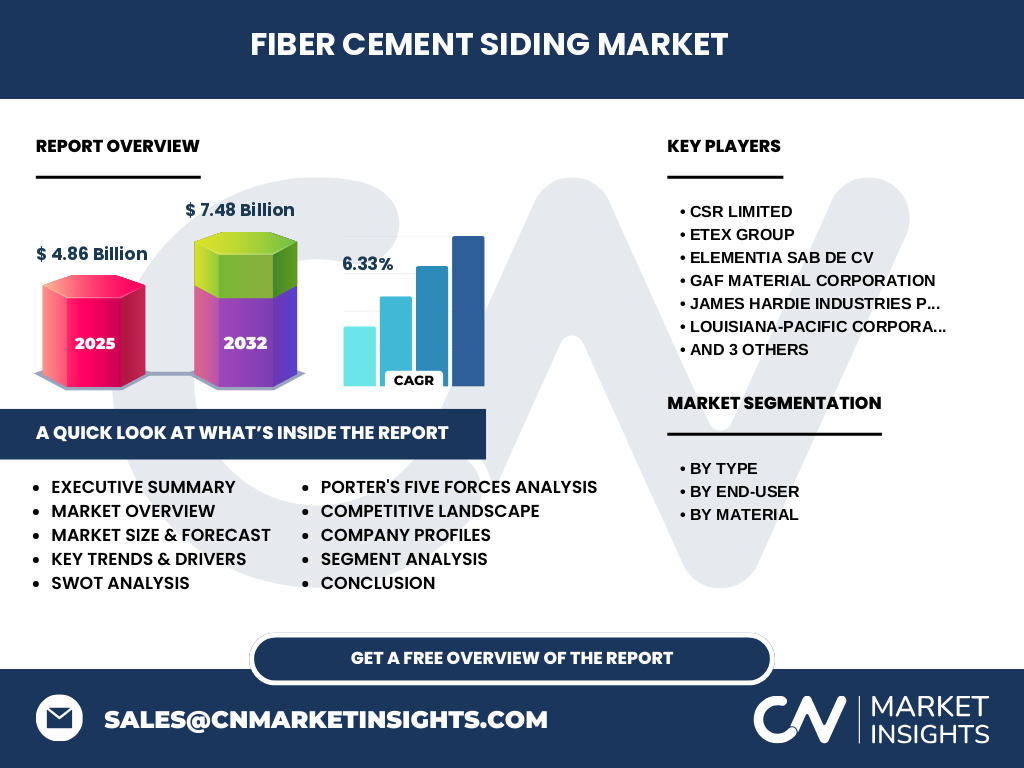

Executive Summary - High-level overview and key findings about Fiber Cement Siding Market

The fiber cement siding market presents a compelling growth opportunity within the construction materials sector, driven by increasing demand for durable, sustainable building solutions across residential and commercial applications. The market is projected to grow from $4.86 billion in 2025 to $7.48 billion by 2032, representing a robust compound annual growth rate of 6.33%. This growth is supported by favorable construction industry trends, stringent building codes, and evolving consumer preferences for low-maintenance, aesthetically versatile exterior finishes. Key market segments include various product types such as clapboard, shingles, and stone or stucco finishes, serving both residential and commercial end-users. The market's competitive landscape features established global players alongside regional manufacturers, creating a dynamic environment for innovation and strategic partnerships.

Fiber Cement Siding Market Forecast - Projections for 2025-2032 period

The fiber cement siding market is poised for substantial growth over the forecast period, with projections indicating expansion from $4.86 billion in 2025 to $7.48 billion by 2032. This represents a compound annual growth rate (CAGR) of 6.33%, reflecting strong underlying demand drivers and favorable market conditions. The forecast period will likely see continued expansion in both developed and emerging markets, with particular emphasis on regions experiencing rapid urbanization and infrastructure development. Key factors influencing this growth trajectory include increasing construction spending, rising awareness of fire safety and weather resistance requirements, and the ongoing shift toward sustainable building materials. The forecast also suggests potential for market expansion through technological innovations, product diversification, and strategic geographic penetration by leading manufacturers.

Fiber Cement Siding Market Size and Share by Segmentation - Breakdown by {segmentData}

The fiber cement siding market exhibits distinct segmentation patterns across multiple dimensions, with each segment contributing uniquely to overall market dynamics. By type, clapboard siding maintains the largest market share due to its widespread adoption in residential applications and versatility in architectural styles. Shingles represent the second-largest segment, driven by demand for traditional and colonial-style aesthetics. Stone or stucco variants are gaining traction in premium and commercial applications. Regarding end-user segmentation, the residential sector dominates market share, accounting for the majority of fiber cement siding installations, while the commercial segment shows steady growth in institutional and industrial applications. Material composition analysis reveals that portland cement-based products constitute the largest share, followed by silica and cellulosic fiber components, with manufacturers increasingly focusing on optimizing material ratios to enhance product performance and sustainability characteristics.

Global Fiber Cement Siding Market Size and Share by Region - Geographic distribution

The global fiber cement siding market demonstrates varied geographic distribution patterns, with developed regions maintaining significant market shares while emerging economies show accelerated growth potential. North America represents a mature market with established infrastructure and stringent building codes driving consistent demand for fiber cement siding products. Europe follows as another significant market, characterized by emphasis on energy efficiency and sustainable construction practices. The Asia-Pacific region exhibits the fastest growth trajectory, driven by rapid urbanization, increasing construction spending, and rising awareness of durable building materials. Latin America and Middle East & Africa regions, while currently representing smaller market shares, present substantial growth opportunities due to expanding construction activities and improving economic conditions. Regional variations in building practices, climate conditions, and regulatory frameworks influence market dynamics and product preferences across different geographic areas.

Regional Analysis of the Fiber Cement Siding Market - Detailed regional market performance

Regional market performance analysis reveals distinct characteristics and growth patterns across major geographic areas. In North America, the market benefits from mature construction industry infrastructure, strict building codes, and high consumer awareness of fiber cement siding benefits. The region's focus on home renovation and remodeling activities provides consistent demand drivers. European markets demonstrate strong emphasis on energy efficiency and sustainability, with fiber cement siding aligning well with these priorities. The Asia-Pacific region represents the most dynamic growth market, driven by rapid urbanization, expanding middle-class populations, and increasing construction spending in countries like China, India, and Southeast Asian nations. Latin American markets show promising growth potential, particularly in Brazil and Mexico, where improving economic conditions support construction industry expansion. Middle East & African markets, while currently smaller, offer significant opportunities as infrastructure development accelerates and building standards evolve.

Leading Company Profiles in the Fiber Cement Siding Market - Industry players and strategies

The fiber cement siding market features several prominent industry players employing diverse strategies to maintain and expand their market positions. James Hardie Industries Plc stands as a global leader, leveraging its extensive product portfolio, strong brand recognition, and continuous innovation in fiber cement technology. Louisiana-Pacific Corporation focuses on integrated building solutions, combining fiber cement siding with complementary products to serve comprehensive construction needs. CSR Limited maintains strong regional presence in Australia and New Zealand, capitalizing on local market knowledge and established distribution networks. ETEX Group pursues global expansion through strategic acquisitions and product diversification, while Elementia SAB DE CV emphasizes its strong position in Latin American markets. Nichiha Co. Ltd. specializes in innovative designs and finishes, targeting premium market segments. These companies collectively shape market dynamics through their competitive strategies, technological investments, and geographic expansion initiatives.

Porter's Five Forces Analysis of the Fiber Cement Siding Market - Competitive forces assessment

Porter's Five Forces analysis reveals a moderately competitive fiber cement siding market with distinct competitive dynamics. The threat of new entrants remains moderate due to significant capital requirements for manufacturing facilities, technical expertise needed for product development, and established brand loyalty among customers. Bargaining power of suppliers is relatively low as raw material suppliers are numerous and fiber cement production requires common industrial materials. Buyer bargaining power varies by region and application, with large construction companies and distributors having more negotiating leverage compared to individual homeowners. The threat of substitute products is moderate, as alternative siding materials like vinyl, wood, and engineered wood compete on price and aesthetics, though fiber cement's superior durability and fire resistance provide competitive advantages. Competitive rivalry is intense among established players, driving continuous innovation, price competition, and strategic partnerships to capture market share.

SWOT Analysis of the Fiber Cement Siding Market - Strengths, weaknesses, opportunities, threats

The fiber cement siding market exhibits distinct strengths including superior durability, excellent fire resistance, and low maintenance requirements that appeal to both residential and commercial customers. The material's versatility in mimicking natural wood or stone aesthetics while offering enhanced performance characteristics represents another significant strength. However, weaknesses include higher initial installation costs compared to alternative materials and the need for specialized labor, which can limit market penetration in price-sensitive segments. Opportunities abound in emerging markets with growing construction activities, potential for product innovation in lightweight and eco-friendly formulations, and expanding applications in renovation and remodeling projects. Threats include intense competition from substitute materials, potential regulatory changes regarding silica dust exposure during manufacturing and installation, and economic downturns that could reduce construction spending and delay infrastructure projects.

Fiber Cement Siding Market Value Chain Analysis - Industry structure and value flow

The fiber cement siding market value chain encompasses multiple stages from raw material sourcing to end-user installation, with each segment contributing to the overall market dynamics. Raw material suppliers provide essential components including portland cement, silica, and cellulosic fibers, which are then processed by manufacturers into various siding products through specialized production techniques. Distributors and building material suppliers play a crucial intermediary role, connecting manufacturers with contractors, builders, and retail customers. Professional contractors and installers represent the critical link between product availability and end-user adoption, as proper installation significantly impacts product performance and customer satisfaction. End-users span residential homeowners, commercial property developers, and institutional clients, each with distinct requirements and purchasing behaviors. Value addition occurs throughout the chain through product innovation, quality improvements, distribution efficiency, and installation expertise, with manufacturers increasingly focusing on integrated solutions that streamline the entire process from selection to installation.

Key Investment Insights in the Fiber Cement Siding Market - Strategic investment recommendations

Strategic investment opportunities in the fiber cement siding market center on several key areas that promise attractive returns and market growth potential. Manufacturing capacity expansion in high-growth regions, particularly Asia-Pacific and Latin America, offers significant opportunities as construction activities accelerate in these markets. Investment in research and development for innovative product formulations, including ultra-lightweight and eco-friendly variants, can capture premium market segments and address environmental concerns. Distribution network enhancement through strategic partnerships and digital platforms can improve market reach and customer accessibility. Additionally, investments in installation training programs and certification can address the skilled labor shortage while creating competitive advantages through quality assurance. The market's projected growth trajectory and increasing demand for sustainable building materials make it an attractive investment destination for both established players seeking expansion and new entrants looking to capitalize on emerging opportunities.

Fiber Cement Siding Market Conclusion - Summary and key takeaways

The fiber cement siding market presents a compelling growth story within the construction materials sector, characterized by robust demand drivers, technological innovation, and expanding geographic reach. With the market projected to grow from $4.86 billion in 2025 to $7.48 billion by 2032 at a CAGR of 6.33%, the industry demonstrates strong fundamentals and attractive investment potential. Key success factors include product innovation, strategic geographic expansion, and the ability to address evolving customer preferences for sustainable, low-maintenance building materials. The market's competitive landscape, while intense, offers opportunities for differentiation through quality, design innovation, and comprehensive service offerings. As construction activities continue to expand globally and building standards evolve toward greater sustainability and durability requirements, fiber cement siding is well-positioned to capture significant market share and deliver value to stakeholders across the value chain.

Research Methodology - How this research was conducted

The research methodology employed for this fiber cement siding market analysis combines comprehensive primary and secondary research approaches to ensure accuracy and reliability of findings. Primary research involved interviews with industry experts, manufacturers, distributors, and end-users to gather firsthand insights on market dynamics, challenges, and growth opportunities. Secondary research encompassed extensive review of industry publications, company annual reports, trade associations data, and government construction statistics to validate market trends and projections. Market size calculations utilized both top-down and bottom-up approaches, triangulating data from multiple sources to ensure accuracy. The research also incorporated Porter's Five Forces framework and SWOT analysis to provide strategic insights into market competitiveness and growth potential. Data validation processes included cross-referencing multiple sources and expert consultations to ensure the highest level of research integrity.

Research Scope - Coverage and limitations

This research scope encompasses comprehensive analysis of the global fiber cement siding market, covering market size, growth trends, competitive landscape, and regional dynamics from 2025 through 2032. The study includes detailed segmentation by product type, end-user applications, and material composition, providing granular insights into market structure and growth patterns. Geographic coverage extends across major regions including North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with analysis of regional market characteristics and growth drivers. The research focuses on both residential and commercial applications, examining market dynamics across different construction segments. Limitations of the study include potential variations in regional data availability and the inherent challenges in forecasting long-term market trends in a dynamic industry environment. The scope also acknowledges the impact of external factors such as economic conditions, regulatory changes, and technological disruptions that may influence market outcomes.

Key Companies and Recent Developments in the Fiber Cement Siding Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The fiber cement siding market features several key companies driving innovation and market growth through strategic initiatives and product development. James Hardie Industries Plc continues to lead with recent announcements of expanded product lines featuring enhanced weather resistance and aesthetic options, along with strategic investments in manufacturing capacity to meet growing demand. Louisiana-Pacific Corporation has launched new fiber cement siding products with improved installation efficiency and has formed partnerships with major home builders to increase market penetration. CSR Limited recently announced expansion of its Australian manufacturing facilities and introduced eco-friendly product variants to address sustainability concerns. ETEX Group has pursued strategic acquisitions to strengthen its European market position and launched innovative pre-finished siding solutions. Elementia SAB DE CV has expanded its Latin American presence through new distribution partnerships and product line extensions. These companies, along with other market participants, continue to shape the industry through ongoing product innovation, geographic expansion, and strategic collaborations aimed at capturing emerging market opportunities.