North America and Europe Car Audio Market Overview - Definition, scope, and significance

The North America and Europe Car Audio Market encompasses the design, manufacturing, and distribution of audio systems specifically engineered for automotive applications in these two regions. This market includes both factory-installed (OEM) and aftermarket audio solutions, ranging from basic sound systems to premium, high-fidelity audio setups. The significance of this market lies in its direct connection to consumer preferences for in-vehicle entertainment and the growing integration of audio systems with vehicle infotainment platforms. As vehicles become increasingly connected and autonomous driving features advance, the demand for sophisticated audio experiences continues to rise, making car audio an essential component of the modern driving experience.

North America and Europe Car Audio Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

Key drivers for the North America and Europe Car Audio Market include the rising consumer demand for enhanced in-vehicle entertainment experiences, increasing vehicle production, and the growing trend of premiumization in automotive audio systems. The integration of advanced technologies such as voice recognition and smartphone connectivity also fuels market growth. However, restraints include the high cost of premium audio systems, which can limit adoption among price-sensitive consumers, and the increasing complexity of installation in modern vehicles with integrated electronics. Challenges include intense competition among established players and the need for continuous innovation to meet evolving consumer expectations. Opportunities exist in the development of personalized audio experiences, the integration of artificial intelligence for sound optimization, and the expansion of aftermarket solutions for older vehicles seeking audio upgrades.

North America and Europe Car Audio Market Growth Trends - Current and emerging trends shaping the market

The North America and Europe Car Audio Market is experiencing several significant growth trends. The shift towards voice-recognized audio systems is gaining momentum, as consumers increasingly prefer hands-free operation for safety and convenience. Smartphone-controlled audio systems are becoming standard, reflecting the broader trend of mobile device integration in vehicles. Premium and branded audio systems are seeing higher adoption rates as consumers seek superior sound quality and brand recognition. Additionally, the market is witnessing a growing demand for component upgrades, with consumers investing in individual components like amplifiers and speakers to enhance their existing systems. The emergence of electric vehicles presents new opportunities for specialized audio solutions that complement the quiet cabin environment characteristic of EVs.

COVID-19 Impact on the North America and Europe Car Audio Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the North America and Europe Car Audio Market through supply chain interruptions, factory closures, and a temporary decline in vehicle production and sales. Consumer spending priorities shifted during lockdowns, with many postponing non-essential vehicle upgrades and purchases. However, the market demonstrated resilience as pent-up demand emerged during recovery phases. The pandemic accelerated certain trends, such as the preference for private vehicle use over public transportation, which indirectly supported the car audio market. As economies reopened, the market experienced a recovery trajectory marked by increased consumer spending on vehicle personalization and entertainment features, with a particular focus on premium audio experiences as part of the overall vehicle ownership experience.

North America and Europe Car Audio Market Competitive Landscape - Major competitors and market consolidation

The North America and Europe Car Audio Market features a competitive landscape dominated by established global players alongside regional specialists. Major competitors include Alpine Electronics, Inc., Blaupunkt GmbH, Bose Corporation, Clarion Co., Ltd., Delphi Automotive PLC, HARMAN International, JL Audio Corporation, JVC Kenwood Corporation, Panasonic Corporation, Pioneer Corporation, and Sony Corporation. The market shows signs of consolidation as larger companies acquire smaller innovators to expand their technology portfolios and market reach. Competition is intense across all segments, with companies differentiating themselves through sound quality, technological innovation, brand partnerships with vehicle manufacturers, and aftermarket presence. The competitive dynamics are further shaped by the balance between OEM supply relationships and direct-to-consumer aftermarket sales strategies.

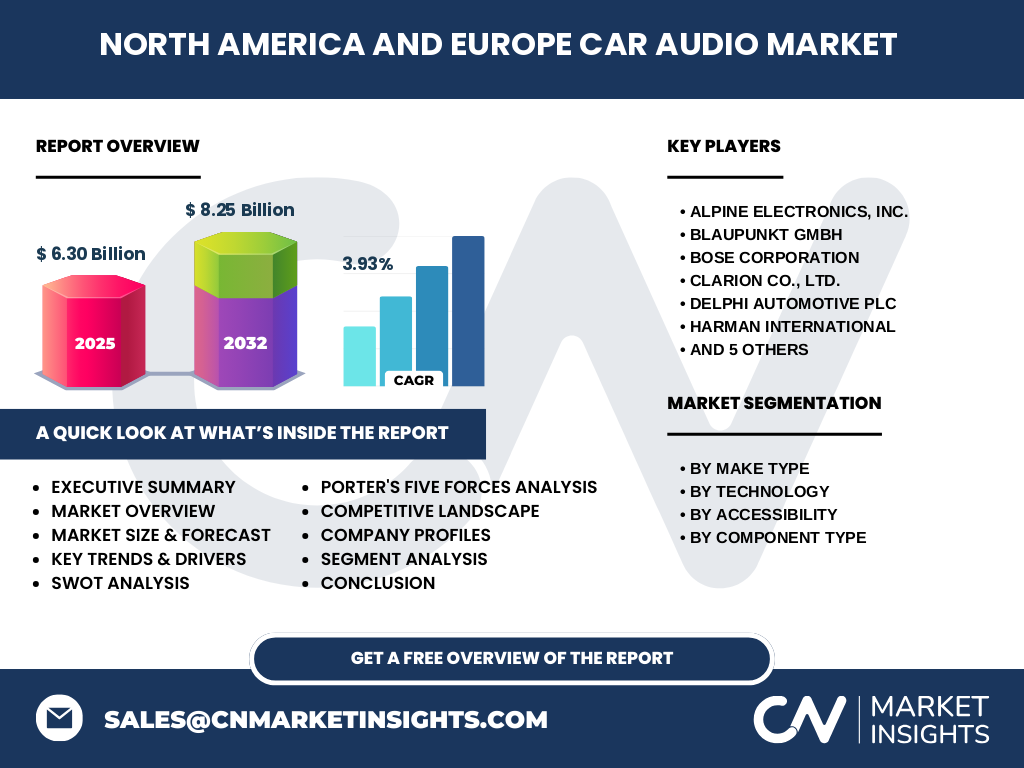

Executive Summary - High-level overview and key findings about North America and Europe Car Audio Market

The North America and Europe Car Audio Market is positioned for steady growth, with the market size expected to increase from 6.30 Billion in 2025 to 8.25 Billion by 2032, representing a CAGR of 3.93%. This growth is driven by technological advancements, particularly in voice recognition and smartphone integration, alongside the rising consumer preference for premium audio experiences. The market segmentation reveals distinct opportunities across branded versus non-branded systems, voice versus non-voice recognized technologies, smartphone versus manual control options, and various component types including speakers, head units, audio visual systems, and amplifiers. The competitive landscape is characterized by established players investing in innovation and strategic partnerships to maintain market positions. Regional dynamics show varying growth patterns, with North America and Europe presenting unique consumer preferences and regulatory environments that shape market development.

North America and Europe Car Audio Market Forecast - Projections for 2025-2032 period

The North America and Europe Car Audio Market is projected to experience consistent growth from 2025 to 2032, with the market value increasing from 6.30 Billion to 8.25 Billion. This represents a compound annual growth rate of 3.93% over the forecast period. The forecast reflects steady demand across all market segments, with particular strength expected in premium branded audio systems and advanced technology integrations such as voice recognition. The growth trajectory is supported by ongoing vehicle production in both regions, the increasing average age of vehicles creating aftermarket opportunities, and the continuous evolution of consumer expectations for in-vehicle entertainment. Regional variations in growth rates are anticipated, influenced by economic conditions, vehicle ownership patterns, and technological adoption rates in North America versus Europe.

North America and Europe Car Audio Market Size and Share by Segmentation - Breakdown by {segmentData}

The North America and Europe Car Audio Market segmentation reveals distinct patterns across different categories. By make type, branded/premium audio systems command a significant market share, reflecting consumer willingness to invest in recognized quality and performance, while non-branded systems serve the value-conscious segment. In terms of technology, voice-recognized systems are gaining market share as hands-free operation becomes increasingly important for safety and convenience, though non-voice recognized systems continue to maintain substantial presence. Accessibility preferences show a clear trend toward smartphone-controlled systems, aligning with broader mobile device integration trends, while manual controlled systems still hold relevance in certain vehicle segments. Component type analysis indicates that speakers and head units represent the largest market shares, with amplifiers and audio visual components showing strong growth potential as consumers seek to upgrade their audio experiences.

Global North America and Europe Car Audio Market Size and Share by Region - Geographic distribution

The North America and Europe Car Audio Market demonstrates distinct geographic distribution patterns between these two major regions. North America, characterized by a large vehicle parc, strong consumer spending power, and preference for premium audio experiences, represents a significant portion of the market. The region's mature automotive industry and high aftermarket modification culture contribute to sustained demand across all segments. Europe, while smaller in overall market size, presents unique characteristics including diverse consumer preferences across different countries, strong environmental regulations that influence vehicle design, and a robust premium vehicle market that drives demand for high-end audio systems. The geographic distribution reflects varying economic conditions, vehicle ownership rates, and technological adoption speeds between North America and Europe, with each region offering distinct opportunities and challenges for market participants.

Regional Analysis of the North America and Europe Car Audio Market - Detailed regional market performance

The regional analysis of the North America and Europe Car Audio Market reveals differentiated performance patterns. In North America, the market benefits from a large and aging vehicle fleet, creating substantial aftermarket opportunities, alongside strong demand for premium factory-installed systems in new vehicles. The region's consumer culture emphasizes personalization and entertainment, driving consistent demand for audio upgrades and replacements. European markets show more diverse patterns, with Western European countries demonstrating higher adoption rates for premium branded systems and advanced technologies, while Eastern European markets present growth opportunities as vehicle ownership increases and consumer spending power rises. Regulatory differences, such as stricter noise regulations in Europe and varying safety standards, influence product development and market strategies in each region. The aftermarket segment shows particular strength in North America due to longer vehicle ownership periods, while Europe's focus on new vehicle sales creates opportunities in OEM partnerships.

Leading Company Profiles in the North America and Europe Car Audio Market - Industry players and strategies

The North America and Europe Car Audio Market is served by several leading companies, each with distinct strategic approaches. Alpine Electronics, Inc. focuses on premium aftermarket solutions and maintains strong relationships with vehicle manufacturers for OEM supply. Blaupunkt GmbH leverages its heritage brand to offer both traditional and smart audio solutions across multiple price points. Bose Corporation, known for its acoustic expertise, partners with luxury vehicle manufacturers to provide integrated premium audio systems. Clarion Co., Ltd. emphasizes technological innovation in connectivity and user interface design. HARMAN International, through its subsidiary brands, offers a comprehensive portfolio spanning OEM and aftermarket segments. JL Audio Corporation specializes in high-performance aftermarket solutions for enthusiasts. JVC Kenwood Corporation combines traditional audio expertise with modern connectivity features. Panasonic Corporation leverages its broad electronics capabilities to provide integrated solutions. Pioneer Corporation maintains strong aftermarket presence with innovative features. Sony Corporation brings its consumer electronics expertise to automotive audio applications. These companies employ strategies ranging from vertical integration and technology partnerships to brand positioning and geographic expansion to maintain competitive advantages.

Porter's Five Forces Analysis of the North America and Europe Car Audio Market - Competitive forces assessment

The Porter's Five Forces analysis of the North America and Europe Car Audio Market reveals the following competitive dynamics. The threat of new entrants is moderate, as established brand recognition, manufacturing capabilities, and OEM relationships create barriers to entry, though opportunities exist for innovative startups in niche segments. The bargaining power of suppliers is relatively low due to the availability of multiple component suppliers and the ability of large manufacturers to integrate vertically. Buyers, including both vehicle manufacturers and end consumers, have moderate bargaining power, particularly in the aftermarket segment where price sensitivity influences purchasing decisions. The threat of substitute products is low, as specialized car audio systems offer unique advantages over general consumer electronics in terms of integration, durability, and vehicle-specific optimization. Competitive rivalry is high among existing players, characterized by price competition, technological innovation races, and brand differentiation efforts. The overall intensity of competitive forces creates a dynamic market environment requiring continuous innovation and strategic positioning.

SWOT Analysis of the North America and Europe Car Audio Market - Strengths, weaknesses, opportunities, threats

The SWOT analysis of the North America and Europe Car Audio Market reveals several key factors. Strengths include established brand recognition of major players, advanced technological capabilities particularly in connectivity and sound optimization, strong relationships with vehicle manufacturers, and a large installed base of vehicles requiring audio systems. Weaknesses encompass high development costs for new technologies, dependency on vehicle production cycles, potential supply chain vulnerabilities, and the challenge of differentiating products in a mature market. Opportunities exist in the growing demand for premium audio experiences, the expansion of electric vehicles creating new audio requirements, the potential for personalized sound profiles using AI, and the increasing integration of audio systems with broader vehicle infotainment platforms. Threats include economic downturns affecting consumer spending on vehicle upgrades, rapid technological changes potentially rendering current products obsolete, intense price competition, and regulatory changes that may impact system design or installation requirements.

North America and Europe Car Audio Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the North America and Europe Car Audio Market reveals a complex structure involving multiple stakeholders and value-adding activities. The chain begins with component suppliers providing raw materials, semiconductors, speakers, and electronic components. These feed into manufacturers who design, engineer, and assemble audio systems, incorporating both hardware and software elements. For OEM systems, manufacturers work closely with vehicle manufacturers during the design and integration phase, ensuring compatibility with vehicle architecture and meeting specific acoustic requirements. Aftermarket suppliers and distributors then provide products directly to consumers through retail channels, online platforms, and installation centers. Value is added at each stage through technological innovation, quality improvements, design optimization, and service enhancements. The aftermarket segment particularly emphasizes value addition through customization, installation expertise, and ongoing support services. The flow of value is influenced by factors such as brand reputation, technological differentiation, pricing strategies, and distribution efficiency.

Key Investment Insights in the North America and Europe Car Audio Market - Strategic investment recommendations

Strategic investment insights for the North America and Europe Car Audio Market highlight several key areas for potential returns. Investment in research and development of voice recognition and AI-driven audio optimization technologies presents significant opportunities as consumer demand for hands-free operation and personalized sound experiences grows. The premium and branded audio system segment offers attractive margins for companies able to deliver superior sound quality and brand differentiation. Investments in smartphone integration technologies and app-based control interfaces align with consumer expectations for seamless connectivity. The aftermarket segment presents opportunities for companies offering upgrade solutions for the large installed base of existing vehicles, particularly those providing plug-and-play systems that minimize installation complexity. Strategic partnerships with vehicle manufacturers for OEM supply can provide stable revenue streams and market access, while investments in sustainable manufacturing processes and materials may offer competitive advantages as environmental considerations become increasingly important to consumers and regulators.

North America and Europe Car Audio Market Conclusion - Summary and key takeaways

The North America and Europe Car Audio Market presents a dynamic landscape characterized by steady growth, technological innovation, and evolving consumer preferences. With the market projected to grow from 6.30 Billion in 2025 to 8.25 Billion by 2032 at a CAGR of 3.93%, the industry offers substantial opportunities for both established players and new entrants. Key trends including the shift toward voice recognition, smartphone integration, and premium audio experiences are reshaping the competitive dynamics. The market's segmentation reveals distinct opportunities across different product types and technologies, while regional variations between North America and Europe create diverse strategic considerations. Success in this market requires a balanced approach combining technological innovation, strong brand positioning, strategic partnerships, and responsiveness to changing consumer expectations. The ongoing transformation of vehicles toward greater connectivity and autonomy further emphasizes the importance of sophisticated audio systems in the overall driving experience.

Research Methodology - How this research was conducted

This research on the North America and Europe Car Audio Market was conducted using a comprehensive methodology combining multiple data sources and analytical approaches. Primary research included interviews with industry experts, manufacturers, distributors, and end-users to gather firsthand insights into market dynamics, technological trends, and consumer preferences. Secondary research involved extensive review of company annual reports, industry publications, market databases, and regulatory documents to validate findings and establish historical context. Data triangulation was employed to cross-verify information from multiple sources, ensuring accuracy and reliability. Market sizing was performed using both top-down and bottom-up approaches, considering factors such as vehicle production volumes, aftermarket penetration rates, and component pricing across different segments. The forecast methodology incorporated trend analysis, regression modeling, and consideration of macroeconomic factors affecting both regions. Special attention was given to technological developments, regulatory changes, and competitive dynamics that could impact future market performance.

Research Scope - Coverage and limitations

The research scope for the North America and Europe Car Audio Market encompasses a comprehensive analysis of the industry from 2025 to 2032, focusing on both regions as defined geographic markets. The study covers all major market segments including branded versus non-branded systems, voice versus non-voice recognized technologies, smartphone versus manual control options, and component types such as speakers, head units, audio visual systems, and amplifiers. The research includes both OEM and aftermarket channels, examining the full spectrum of car audio solutions from basic factory-installed systems to premium aftermarket upgrades. Coverage extends to major market players, competitive dynamics, and regulatory environments affecting both regions. Limitations of the research include the exclusion of certain emerging technologies still in early development stages, potential variations in regional economic conditions that could affect growth projections, and the inherent challenges in forecasting consumer preference shifts in a rapidly evolving technological landscape.

Key Companies and Recent Developments in the North America and Europe Car Audio Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The North America and Europe Car Audio Market features several key companies driving innovation and competition. Alpine Electronics, Inc. recently announced advancements in their Halo9 multimedia receiver series, featuring enhanced smartphone integration and voice control capabilities. Blaupunkt GmbH launched a new line of smart speakers with AI-powered sound optimization for both OEM and aftermarket applications. Bose Corporation expanded its partnership with electric vehicle manufacturers to develop specialized audio systems optimized for the unique acoustic environments of EVs. Clarion Co., Ltd. introduced a new generation of head units with advanced connectivity features and over-the-air update capabilities. HARMAN International, through its JBL brand, launched premium audio systems with personalized sound profiles using machine learning algorithms. JL Audio Corporation announced the release of their FiX Signal Processing and Integration products, designed to simplify aftermarket audio upgrades. JVC Kenwood Corporation expanded its smartphone integration technologies with enhanced wireless connectivity options. Panasonic Corporation revealed developments in their Technics audio brand for automotive applications, focusing on high-resolution audio reproduction. Pioneer Corporation launched a new series of multimedia receivers with advanced voice recognition and smartphone integration. Sony Corporation introduced their latest XAV-AX8500 media receiver featuring enhanced voice control and smartphone connectivity features. These developments reflect the industry's focus on connectivity, personalization, and enhanced user experiences across both regions.