Knee Implant Market Overview - Definition, scope, and significance

Knee implants, also known as knee prostheses, are medical devices surgically implanted to replace damaged or diseased knee joints, primarily due to osteoarthritis, rheumatoid arthritis, or traumatic injuries. The knee implant market encompasses a range of products including total knee replacements, partial knee replacements, and revision procedures, utilizing various materials such as cemented and non-cemented implants, as well as fixed and mobile bearing prostheses. This market plays a crucial role in improving quality of life for millions of patients worldwide by restoring mobility, reducing pain, and enabling active lifestyles. With an aging global population and increasing prevalence of joint-related conditions, the knee implant market has become a significant segment within the broader orthopedic devices industry, representing a critical intersection of medical innovation, surgical expertise, and patient care.

Knee Implant Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The knee implant market is driven by several key factors, including the rising geriatric population, increasing prevalence of osteoarthritis and obesity-related joint issues, and technological advancements in implant materials and surgical techniques. The growing demand for minimally invasive procedures and the expansion of healthcare infrastructure in emerging markets present significant opportunities for market growth. However, the market faces restraints such as the high cost of knee replacement surgeries, potential complications and revision surgeries, and stringent regulatory requirements for medical devices. Challenges include the need for skilled surgeons, limited reimbursement policies in certain regions, and the impact of alternative treatments like regenerative medicine. Despite these obstacles, opportunities exist in developing cost-effective implants, expanding into untapped markets, and leveraging digital technologies for personalized implant solutions and improved surgical outcomes.

Knee Implant Market Growth Trends - Current and emerging trends shaping the market

The knee implant market is experiencing several notable growth trends that are reshaping the industry landscape. One significant trend is the increasing adoption of patient-specific and custom-designed implants, enabled by advanced imaging technologies and 3D printing capabilities. This personalization approach aims to improve implant fit, longevity, and patient outcomes. Another emerging trend is the integration of smart technologies and sensors into knee implants, allowing for real-time monitoring of implant performance and patient recovery. The market is also witnessing a shift towards less invasive surgical techniques, such as robotic-assisted surgery and computer-navigated procedures, which promise improved precision and faster recovery times. Additionally, there is growing interest in the development of more durable and biocompatible materials to extend the lifespan of knee implants and reduce the need for revision surgeries. The trend towards outpatient knee replacement procedures is also gaining traction, driven by advancements in anesthesia and pain management techniques.

COVID-19 Impact on the Knee Implant Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the knee implant market, causing disruptions across the entire value chain. During the peak of the pandemic, many elective surgeries, including knee replacements, were postponed or cancelled to prioritize COVID-19 patients and conserve healthcare resources. This led to a sharp decline in knee implant procedures and sales in 2020. However, as healthcare systems adapted to the new normal and vaccination efforts progressed, the market began to show signs of recovery in 2021. The pandemic also accelerated certain trends, such as the adoption of telemedicine for pre- and post-operative consultations, and increased focus on infection control measures in surgical settings. Looking ahead, the knee implant market is expected to rebound strongly, driven by pent-up demand for procedures and the continued aging of the global population. The industry is likely to see a shift towards more resilient supply chains and increased investment in digital health technologies to better manage future disruptions.

Knee Implant Market Competitive Landscape - Major competitors and market consolidation

The knee implant market is characterized by a highly competitive landscape with several major players dominating the industry. Key competitors include global medical device giants such as Zimmer Biomet Holdings Inc., Stryker Corporation, and Johnson & Johnson's DePuy Synthes, which together hold a significant market share. These companies compete on factors such as product innovation, technological advancements, and extensive distribution networks. The market has seen a trend towards consolidation, with larger companies acquiring smaller, innovative firms to expand their product portfolios and technological capabilities. For instance, Zimmer Biomet's acquisition of Embody and Stryker's purchase of Orthosensor have strengthened their positions in the market. Other notable players include Smith & Nephew plc, Medtronic plc, and Conmed Corporation, each bringing unique strengths and specialized products to the competitive landscape. The intense competition has led to increased focus on research and development, strategic partnerships, and geographic expansion to maintain market share and drive growth.

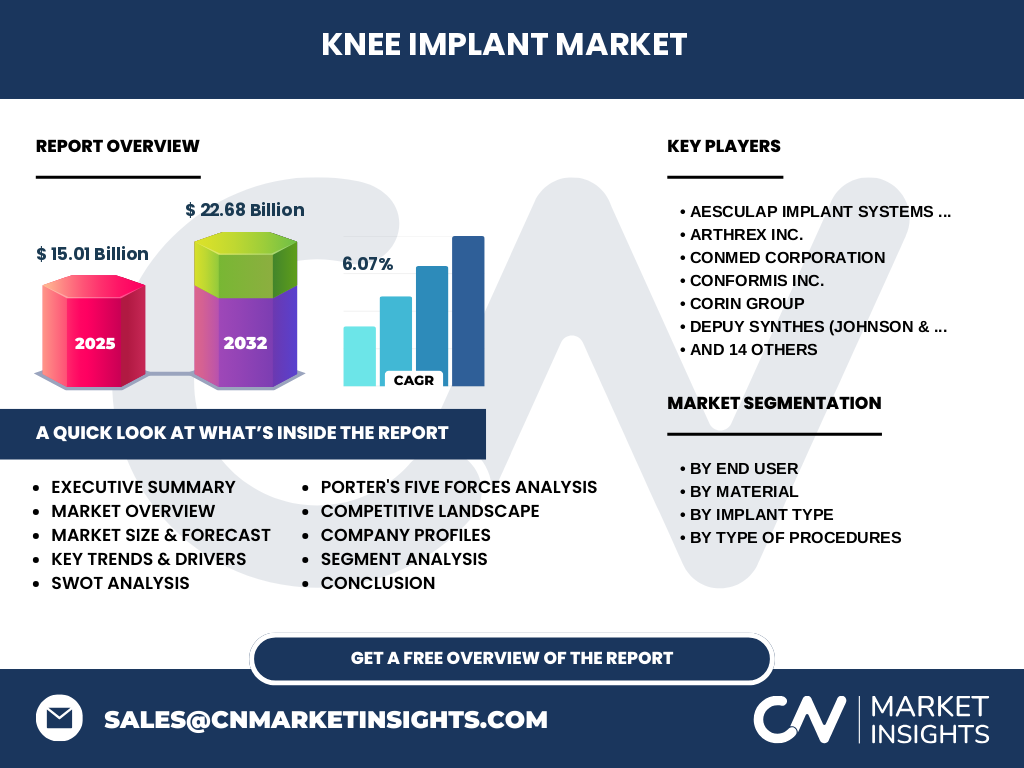

Executive Summary - High-level overview and key findings about Knee Implant Market

The global knee implant market is poised for substantial growth, with projections indicating an increase from USD 15.01 billion in 2025 to USD 22.68 billion by 2032, representing a compound annual growth rate (CAGR) of 6.07%. This growth is primarily driven by the aging global population, rising prevalence of osteoarthritis, and technological advancements in implant materials and surgical techniques. The market is segmented by end user (hospitals, orthopedic clinics, ambulatory surgical centers, and others), material (cemented and non-cemented), implant type (fixed and mobile bearing prostheses), and procedure type (total, partial, and revision knee replacements). Key players in the market include industry leaders such as Zimmer Biomet, Stryker, and DePuy Synthes, alongside innovative companies like Conformis Inc. and THINK Surgical Inc. The COVID-19 pandemic initially disrupted the market but has since accelerated trends towards digital health integration and personalized implant solutions. As the market recovers and evolves, opportunities lie in emerging markets, cost-effective implant development, and the integration of smart technologies for improved patient outcomes.

Knee Implant Market Forecast - Projections for 2025-2032 period

The knee implant market is projected to experience steady growth over the forecast period from 2025 to 2032, with the market size expected to increase from USD 15.01 billion in 2025 to USD 22.68 billion by 2032, representing a compound annual growth rate (CAGR) of 6.07%. This growth trajectory is underpinned by several factors, including the continued aging of the global population, particularly in developed markets, and the increasing prevalence of obesity and related joint issues in both developed and emerging economies. The forecast period is likely to see accelerated adoption of advanced implant technologies, such as patient-specific implants and smart knee replacements with integrated sensors. The market is also expected to benefit from expanding healthcare infrastructure in emerging markets, particularly in Asia-Pacific and Latin American regions. However, growth may be moderated by factors such as pricing pressures, reimbursement challenges in certain regions, and the potential impact of alternative treatments. Overall, the knee implant market is positioned for robust growth, driven by technological innovation, demographic trends, and increasing awareness of joint health and mobility solutions.

Knee Implant Market Size and Share by Segmentation - Breakdown by {segmentData}

The knee implant market can be segmented based on end user, material, implant type, and procedure type. By end user, hospitals dominate the market due to their comprehensive infrastructure and ability to handle complex cases, followed by orthopedic clinics and ambulatory surgical centers. The material segment is divided into cemented and non-cemented implants, with cemented implants traditionally holding a larger share due to their long-standing use and proven effectiveness. However, non-cemented implants are gaining traction, especially in younger patients with better bone quality. In terms of implant type, fixed bearing prostheses currently account for the majority of the market share, attributed to their cost-effectiveness and widespread use. Nevertheless, mobile bearing prostheses are experiencing growth due to their potential for improved range of motion and reduced wear. Regarding procedure types, total knee replacements represent the largest segment, driven by the aging population and increasing prevalence of severe osteoarthritis. Partial knee replacements and revision surgeries form smaller but significant segments, with revision procedures expected to grow as the installed base of older implants requires replacement.

Global Knee Implant Market Size and Share by Region - Geographic distribution

The global knee implant market exhibits distinct regional variations in terms of market size and share, influenced by factors such as healthcare infrastructure, demographic trends, and economic conditions. North America currently holds the largest market share, driven by a well-established healthcare system, high healthcare expenditure, and a large aging population. The United States, in particular, accounts for a significant portion of the North American market due to its advanced medical technology adoption and favorable reimbursement policies. Europe follows as the second-largest market, with countries like Germany, France, and the UK leading in terms of knee implant procedures and market size. The Asia-Pacific region is expected to witness the fastest growth during the forecast period, fueled by improving healthcare infrastructure, rising disposable incomes, and increasing awareness of joint health in countries such as China, India, and Japan. Latin America and the Middle East & Africa regions, while currently smaller markets, are also showing promising growth potential due to expanding healthcare access and growing middle-class populations.

Regional Analysis of the Knee Implant Market - Detailed regional market performance

The knee implant market demonstrates varied performance across different regions, reflecting diverse healthcare landscapes and demographic profiles. In North America, the market is characterized by high adoption rates of advanced implant technologies and a strong focus on minimally invasive surgical techniques. The region benefits from robust healthcare infrastructure and favorable reimbursement policies, although pricing pressures and cost-containment measures pose challenges. Europe's market is marked by a mix of mature healthcare systems and varying economic conditions across countries. Western European nations lead in terms of market size and technological adoption, while Eastern European markets are catching up with improving healthcare access. The Asia-Pacific region presents a dynamic growth story, with countries like China and India emerging as key markets due to their large populations and improving healthcare infrastructure. However, the region also faces challenges such as varying quality standards and affordability issues. Latin America's market is driven by Brazil and Mexico, with growing middle-class populations and increasing healthcare investments. The Middle East & Africa region, while currently smaller, shows potential for growth, particularly in Gulf Cooperation Council (GCC) countries with their focus on developing advanced healthcare systems.

Leading Company Profiles in the Knee Implant Market - Industry players and strategies

The knee implant market is dominated by several key players, each employing distinct strategies to maintain and expand their market positions. Zimmer Biomet Holdings Inc. stands out as a global leader, leveraging its extensive product portfolio and strong research and development capabilities to drive innovation in knee implant technologies. Stryker Corporation is another major player, known for its focus on advanced materials and patient-specific implant solutions. Johnson & Johnson's DePuy Synthes division maintains a significant market presence through its broad range of knee replacement systems and strong global distribution network. Smith & Nephew plc differentiates itself through its emphasis on minimally invasive surgical techniques and advanced bearing materials. Medtronic plc, while traditionally strong in other medical device segments, has been expanding its presence in the knee implant market through strategic acquisitions and product development. Companies like Conformis Inc. and THINK Surgical Inc. represent the innovative edge of the market, focusing on personalized implant solutions and robotic-assisted surgery technologies. These leading companies are increasingly investing in digital health integration, artificial intelligence for surgical planning, and partnerships with healthcare providers to strengthen their market positions and drive growth.

Porter's Five Forces Analysis of the Knee Implant Market - Competitive forces assessment

Applying Porter's Five Forces analysis to the knee implant market reveals a complex competitive landscape. The threat of new entrants is moderate, as the market requires significant capital investment, regulatory approvals, and established distribution networks. However, technological advancements and the potential for disruptive innovations create opportunities for new players to enter niche segments. The bargaining power of buyers, primarily hospitals and healthcare systems, is relatively high due to the commoditization of certain implant types and the availability of multiple suppliers. This has led to increased price negotiations and a focus on cost-effective solutions. Suppliers of raw materials and components have moderate bargaining power, although this can vary depending on the uniqueness of the materials and the company's supply chain diversification. The threat of substitute products is low to moderate, with alternative treatments like regenerative medicine and non-surgical interventions posing some competition, but not significantly impacting the overall demand for knee implants. The intensity of competitive rivalry is high, characterized by the presence of large multinational corporations, continuous product innovations, and aggressive marketing strategies. This intense competition drives companies to focus on technological differentiation, strategic partnerships, and expansion into emerging markets to maintain their competitive edge.

SWOT Analysis of the Knee Implant Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the knee implant market reveals a dynamic industry with distinct strengths, weaknesses, opportunities, and threats. Strengths include the market's resilience to economic downturns due to the essential nature of knee replacement procedures, the presence of established players with strong R&D capabilities, and the continuous technological advancements improving implant longevity and patient outcomes. Weaknesses encompass the high cost of procedures limiting accessibility in certain regions, the potential for post-surgical complications and revision surgeries, and the long product development cycles required for regulatory approvals. Opportunities abound in the form of expanding into emerging markets with growing healthcare infrastructure, developing cost-effective implant solutions for price-sensitive regions, and leveraging digital technologies for personalized implant designs and improved surgical planning. Threats to the market include increasing pricing pressures from healthcare payers, potential disruptions from alternative treatments like regenerative medicine, and the risk of product recalls or safety issues impacting market confidence. Additionally, the market faces challenges from changing regulatory landscapes and the need to address the skilled surgeon shortage in certain regions.

Knee Implant Market Value Chain Analysis - Industry structure and value flow

The knee implant market value chain encompasses several interconnected stages, from raw material sourcing to post-operative patient care. The chain begins with material suppliers providing specialized metals, polymers, and ceramics used in implant manufacturing. These materials are then processed by component manufacturers who produce the individual parts of knee implants, such as femoral components, tibial trays, and polyethylene inserts. Medical device companies integrate these components into complete implant systems, often incorporating advanced technologies like 3D modeling and patient-specific designs. The finished products are distributed through medical supply chains to hospitals, orthopedic clinics, and ambulatory surgical centers. Surgeons and healthcare professionals perform the implant procedures, while post-operative care providers manage patient recovery and rehabilitation. Throughout this value chain, various stakeholders add value through technological innovations, quality control measures, and service offerings. The integration of digital technologies is increasingly influencing the value chain, with companies leveraging data analytics for product improvement, surgical planning software for enhanced precision, and remote monitoring solutions for improved patient outcomes. This complex value chain is characterized by high regulatory standards, significant R&D investments, and a focus on improving both clinical outcomes and cost-effectiveness.

Key Investment Insights in the Knee Implant Market - Strategic investment recommendations

The knee implant market presents several compelling investment opportunities for stakeholders looking to capitalize on the industry's growth trajectory. Key investment insights include focusing on companies that are at the forefront of technological innovation, particularly those developing patient-specific implants, smart knee replacements with integrated sensors, and advanced bearing materials that promise improved longevity. Investors should also consider companies with strong presence in emerging markets, as these regions are expected to drive significant growth in the coming years due to improving healthcare infrastructure and rising disposable incomes. Strategic partnerships and collaborations between implant manufacturers and healthcare providers represent another attractive investment avenue, as these alliances can drive innovation and improve market penetration. Additionally, companies investing in digital health integration, including AI-powered surgical planning tools and robotic-assisted surgery systems, are well-positioned for future growth. However, investors should be mindful of potential risks such as regulatory challenges, pricing pressures, and the impact of alternative treatments. A diversified investment approach across different segments of the value chain, including material suppliers, component manufacturers, and service providers, may help mitigate these risks while capturing the market's growth potential.

Knee Implant Market Conclusion - Summary and key takeaways

The global knee implant market is on a robust growth path, projected to expand from USD 15.01 billion in 2025 to USD 22.68 billion by 2032, driven by a CAGR of 6.07%. This growth is underpinned by demographic trends, technological advancements, and expanding healthcare access across regions. The market's segmentation reveals diverse opportunities across different end users, materials, implant types, and procedures, with total knee replacements and fixed bearing prostheses currently dominating the landscape. While North America leads in market share, the Asia-Pacific region is poised for the fastest growth, presenting significant opportunities for market expansion. The competitive landscape is characterized by the presence of global giants and innovative startups, all vying for market share through product differentiation and strategic partnerships. Despite challenges such as pricing pressures and the threat of alternative treatments, the market's fundamental drivers remain strong. As the industry continues to evolve, success will likely favor companies that can balance innovation with cost-effectiveness, leverage digital technologies, and adapt to the changing needs of an aging global population.

Research Methodology - How this research was conducted

This comprehensive market research on the knee implant industry was conducted using a robust methodology that combines primary and secondary research techniques to ensure accuracy and reliability. The research process began with an extensive review of existing literature, including industry reports, academic journals, and company publications, to establish a foundational understanding of the market landscape. Primary research was then conducted through interviews with key industry stakeholders, including knee implant manufacturers, orthopedic surgeons, healthcare administrators, and regulatory experts. These interviews provided valuable insights into market trends, technological advancements, and future growth prospects. Data on market size, segmentation, and regional distribution was gathered from multiple sources, including financial reports of major companies, industry databases, and government healthcare statistics. The forecast projections were developed using advanced statistical models that take into account historical growth patterns, demographic trends, and potential market disruptors. The research methodology also incorporated a thorough analysis of the competitive landscape, utilizing tools such as Porter's Five Forces and SWOT analysis to provide a comprehensive view of the market dynamics. Throughout the research process, data triangulation techniques were employed to validate findings and ensure the accuracy of the conclusions drawn.

Research Scope - Coverage and limitations

This research report on the knee implant market provides a comprehensive analysis of the global industry, covering key aspects such as market size, growth trends, competitive landscape, and regional dynamics. The scope of the research encompasses the period from 2025 to 2032, with historical data and future projections included to provide a complete market picture. The report segments the market based on end user (hospitals, orthopedic clinics, ambulatory surgical centers, and others), material (cemented and non-cemented), implant type (fixed and mobile bearing prostheses), and procedure type (total, partial, and revision knee replacements). Regional analysis covers major markets including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The research also includes detailed profiles of key market players and an assessment of recent developments in the industry. However, it's important to note some limitations of this research. The report focuses primarily on the commercial aspects of the knee implant market and may not cover all nuances of clinical outcomes or patient-specific factors. Additionally, while efforts have been made to include the most recent data available, rapid market changes may result in slight discrepancies between the report findings and the current market situation. The research also does not delve into highly specialized or emerging implant technologies that are still in early development stages.

Key Companies and Recent Developments in the Knee Implant Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The knee implant market is characterized by the presence of several key players who are driving innovation and shaping the industry's future through strategic developments. Zimmer Biomet Holdings Inc. has been at the forefront of technological advancements, recently announcing the launch of its Persona IQ, the world's first smart knee replacement with embedded sensor technology for post-operative monitoring. Stryker Corporation has strengthened its market position through the acquisition of Orthosensor, enhancing its capabilities in sensor-integrated implant systems. Johnson & Johnson's DePuy Synthes division introduced the Attune Knee System, featuring advanced bearing surfaces and a unique tibial baseplate design for improved stability. Smith & Nephew plc has focused on personalized solutions, launching the LEGION CONCELOC cemented revision knee system with patient-matched capabilities. Medtronic plc expanded its knee implant portfolio through the acquisition of Medicrea, bringing advanced spinal surgery technologies to its offerings. Conformis Inc. continues to innovate in patient-specific implants, recently receiving FDA clearance for its iTotal CR customized cruciate-retaining knee replacement. THINK Surgical Inc. has made strides in robotic-assisted surgery, announcing partnerships with several leading hospitals to implement its TSolution One system. These developments reflect the industry's focus on personalization, smart technologies, and improved surgical outcomes, setting the stage for continued growth and innovation in the knee implant market.