Breast Reconstruction Market Overview - Definition, scope, and significance

Breast reconstruction is a surgical procedure performed to rebuild the shape and appearance of a breast following mastectomy or lumpectomy due to cancer treatment or as a risk-reduction measure. This market encompasses various reconstructive techniques, implant types, surgical procedures, and related medical devices designed to restore breast symmetry and enhance patient quality of life. The significance of this market extends beyond medical necessity, addressing psychological well-being, body image concerns, and the comprehensive recovery journey for breast cancer survivors and individuals at high risk for breast cancer.

Breast Reconstruction Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The breast reconstruction market is driven by several key factors including the rising global incidence of breast cancer, increasing awareness about reconstruction options, advancements in surgical techniques and implant technologies, and growing insurance coverage for reconstructive procedures. Additionally, the expanding middle-class population with higher disposable incomes and improved access to healthcare services contributes to market growth. However, the market faces restraints such as high procedural costs, potential complications associated with implants, stringent regulatory requirements, and the availability of alternative reconstruction methods. Challenges include managing patient expectations, addressing long-term safety concerns, and navigating complex reimbursement policies. Opportunities exist in developing innovative implant materials, expanding into emerging markets, integrating digital technologies for surgical planning, and offering personalized reconstruction solutions tailored to individual patient needs.

Breast Reconstruction Market Growth Trends - Current and emerging trends shaping the market

The breast reconstruction market is experiencing several notable growth trends that are reshaping the industry landscape. One prominent trend is the increasing preference for immediate reconstruction procedures performed simultaneously with mastectomy, driven by improved surgical techniques and better patient outcomes. Another significant trend is the growing adoption of autologous tissue reconstruction methods alongside implant-based approaches, offering patients more comprehensive options. The market is also witnessing a shift toward anatomically shaped implants and cohesive gel technologies that provide more natural-looking results. Digital transformation is emerging as a key trend, with 3D imaging and virtual surgical planning becoming integral to preoperative assessments. Additionally, there is growing interest in regenerative medicine approaches, including tissue engineering and stem cell therapies, which could revolutionize future reconstruction methods. The trend toward personalized medicine is also influencing the market, with surgeons increasingly tailoring reconstruction approaches to individual patient anatomy, lifestyle, and aesthetic preferences.

COVID-19 Impact on the Breast Reconstruction Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the breast reconstruction market, causing widespread disruptions in surgical procedures, supply chains, and patient care delivery. During the peak pandemic periods, many elective surgeries, including breast reconstruction procedures, were postponed or canceled to prioritize COVID-19 patient care and conserve medical resources. This led to a temporary decline in market growth and revenue for manufacturers and healthcare providers. The pandemic also disrupted global supply chains, causing shortages of surgical implants and medical devices. However, the market demonstrated resilience as healthcare systems adapted to new safety protocols and telemedicine solutions emerged for preoperative consultations. As vaccination rates increased and healthcare systems stabilized, the market began recovering, with pent-up demand driving procedure volumes. The pandemic also accelerated certain trends, including the adoption of digital technologies for surgical planning and patient education. Looking forward, the market is expected to follow a V-shaped recovery trajectory, with growth rates potentially exceeding pre-pandemic levels as deferred procedures are completed and awareness about breast reconstruction options continues to expand.

Breast Reconstruction Market Competitive Landscape - Major competitors and market consolidation

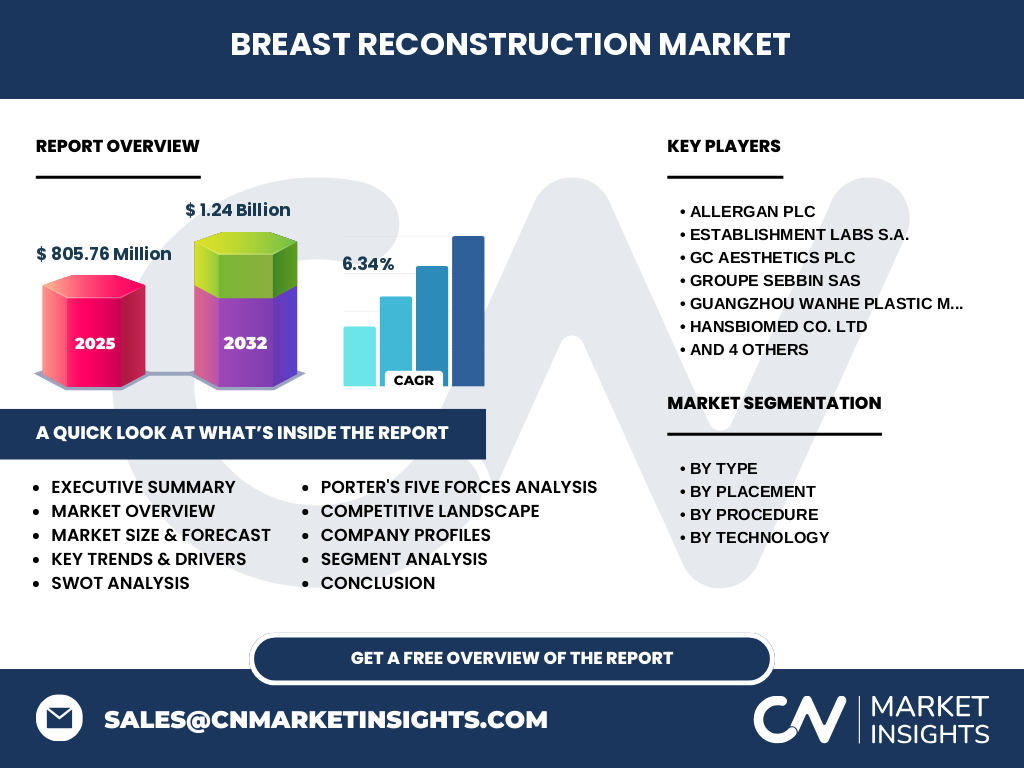

The breast reconstruction market features a moderately consolidated competitive landscape dominated by several key players who collectively hold significant market share. Major competitors include Allergan Plc, Mentor Worldwide LLC (a subsidiary of Johnson & Johnson), and Sientra Inc., which are recognized for their comprehensive product portfolios and established market presence. Other notable players include Establishment Labs S.A., GC Aesthetics PLC, and Groupe Sebbin SAS, each offering specialized implant technologies and reconstruction solutions. The competitive dynamics are characterized by continuous product innovation, strategic partnerships, and geographic expansion initiatives. Market consolidation has been evident through mergers, acquisitions, and strategic alliances aimed at expanding product offerings and market reach. Companies are increasingly focusing on developing next-generation implant materials, improving surgical techniques, and enhancing patient outcomes to maintain competitive advantage. The market also sees competition from regional players in emerging markets, particularly in Asia-Pacific and Latin America, who offer cost-effective alternatives while maintaining quality standards. This competitive environment drives ongoing innovation and creates opportunities for both established players and new entrants to differentiate their offerings.

Executive Summary - High-level overview and key findings about Breast Reconstruction Market

The global breast reconstruction market is positioned for substantial growth, with market size projected to increase from 805.76 Million in 2025 to 1.24 Billion by 2032, representing a compound annual growth rate (CAGR) of 6.34%. This growth is primarily driven by the rising prevalence of breast cancer worldwide, increasing awareness about reconstruction options, and technological advancements in implant materials and surgical techniques. The market is characterized by diverse segmentation across implant types, placement methods, procedural approaches, and technological innovations, providing multiple avenues for growth and specialization. Key market segments include breast implants, implant accessories, various placement techniques such as dual-plane, subglandular, and submuscular insertion, along with procedural categories spanning immediate, delayed, and revision procedures. The market also benefits from technological diversity through inframammary, peri-areolar, trans-axillary, and transumbilical approaches. Despite challenges posed by the COVID-19 pandemic, the market demonstrates resilience and is on a recovery trajectory, with pent-up demand expected to drive accelerated growth in the coming years. The competitive landscape remains dynamic, with established players and emerging companies driving innovation through product development, strategic partnerships, and geographic expansion initiatives.

Breast Reconstruction Market Forecast - Projections for 2025-2032 period

The breast reconstruction market is projected to experience steady and robust growth throughout the 2025-2032 forecast period, with market value expected to increase from 805.76 Million in 2025 to 1.24 Billion by 2032. This represents a compound annual growth rate (CAGR) of 6.34%, indicating healthy market expansion driven by multiple factors. The forecast period will likely see accelerated growth in emerging markets, particularly in Asia-Pacific and Latin America, where improving healthcare infrastructure and rising disposable incomes are creating new opportunities. Technological advancements in implant materials, surgical techniques, and digital planning tools are expected to drive premiumization trends, with patients increasingly opting for advanced reconstruction options. The market will also benefit from demographic factors, including aging populations in developed markets and increasing breast cancer awareness globally. However, growth may be moderated by factors such as regulatory challenges, pricing pressures, and the need for long-term clinical data on new technologies. The forecast suggests that immediate reconstruction procedures will continue to gain market share over delayed procedures, while revision procedures will maintain steady demand due to the long-term nature of implant usage. Overall, the market outlook remains positive, with innovation and expanding access to care serving as primary growth drivers.

Breast Reconstruction Market Size and Share by Segmentation - Breakdown by {segmentData}

The breast reconstruction market exhibits distinct segmentation patterns across multiple dimensions, each contributing uniquely to overall market dynamics. By type, breast implants represent the dominant segment, commanding the largest market share due to their widespread adoption and technological advancements in implant materials. Implant accessories form a significant supporting segment, encompassing surgical tools, positioning devices, and post-operative care products. In terms of placement, dual-plane insertion techniques have gained substantial market share owing to their ability to provide natural-looking results and reduce complications. Submuscular insertion remains popular for its lower capsular contracture rates, while subglandular placement appeals to specific patient demographics seeking less invasive options. By procedure type, immediate reconstruction procedures are experiencing the fastest growth rate, driven by improved surgical techniques and better patient outcomes. Delayed procedures maintain steady demand, particularly among patients who require extensive cancer treatment before reconstruction. Revision procedures represent a consistent market segment due to the long-term nature of implant usage and evolving patient preferences. Technologically, inframammary approaches dominate due to their versatility and surgeon familiarity, while trans-axillary and transumbilical techniques are gaining traction for their scarless advantages, albeit with more limited adoption due to technical complexity.

Global Breast Reconstruction Market Size and Share by Region - Geographic distribution

The global breast reconstruction market demonstrates significant regional variations in market size, growth rates, and adoption patterns. North America currently represents the largest regional market, driven by high healthcare expenditure, advanced medical infrastructure, and widespread insurance coverage for reconstruction procedures. The United States, in particular, accounts for a substantial portion of the North American market due to high breast cancer incidence rates and strong patient awareness about reconstruction options. Europe represents the second-largest regional market, with countries like Germany, France, and the United Kingdom leading in terms of procedure volumes and technological adoption. The Asia-Pacific region is emerging as the fastest-growing market, with countries such as China, Japan, and South Korea experiencing rapid market expansion due to improving healthcare infrastructure, rising disposable incomes, and increasing breast cancer awareness. Latin America shows steady growth potential, particularly in Brazil and Mexico, where medical tourism and improving healthcare access are driving market development. The Middle East and Africa region, while currently representing a smaller market share, is expected to witness significant growth during the forecast period as healthcare systems modernize and patient awareness increases. Regional differences in regulatory frameworks, cultural attitudes toward cosmetic procedures, and reimbursement policies significantly influence market dynamics across different geographic areas.

Regional Analysis of the Breast Reconstruction Market - Detailed regional market performance

Regional analysis of the breast reconstruction market reveals distinct performance patterns and growth opportunities across different geographic areas. North America maintains its position as the dominant regional market, characterized by high procedure volumes, advanced technological adoption, and comprehensive insurance coverage. The region benefits from a well-established healthcare infrastructure, high breast cancer awareness, and strong presence of major market players. Europe follows as a mature market with steady growth, driven by universal healthcare systems in many countries and increasing acceptance of reconstruction procedures. The region shows particular strength in countries with high healthcare standards and patient advocacy for breast cancer survivors. Asia-Pacific emerges as the most dynamic regional market, with double-digit growth rates in several countries. China and India represent particularly promising markets due to their large populations, improving healthcare infrastructure, and rising middle-class demographics. Japan maintains a sophisticated market with high technological adoption rates, while South Korea shows strong growth driven by medical tourism and advanced surgical techniques. Latin America presents mixed regional performance, with Brazil leading in procedure volumes due to medical tourism and improving healthcare access, while other countries show varying levels of market development. The Middle East and Africa region, though currently representing a smaller market share, demonstrates increasing potential as healthcare systems develop and patient awareness grows, particularly in Gulf Cooperation Council countries and South Africa.

Leading Company Profiles in the Breast Reconstruction Market - Industry players and strategies

The breast reconstruction market features several prominent companies that have established strong market positions through innovative product portfolios, strategic partnerships, and comprehensive market approaches. Allergan Plc stands as a market leader with its extensive range of breast implants and reconstruction solutions, leveraging its global presence and strong research and development capabilities. Mentor Worldwide LLC, a subsidiary of Johnson & Johnson, maintains a significant market share through its diverse product portfolio and strong distribution network across multiple regions. Establishment Labs S.A. has gained recognition for its Motiva implants, which incorporate advanced silicone gel technology and innovative surface texturing. GC Aesthetics PLC focuses on developing high-quality implant solutions with an emphasis on natural aesthetics and patient safety. Groupe Sebbin SAS specializes in European markets with its comprehensive range of breast reconstruction products. Guangzhou Wanhe Plastic Materials Co., Ltd. has established a strong presence in the Asia-Pacific region, offering cost-effective solutions while maintaining quality standards. HANSBIOMED CO. LTD represents the growing influence of Korean manufacturers in the global market, known for their innovative approaches to implant design. IDEAL IMPLANT INCORPORATED has differentiated itself through its unique dual-lumen saline implant technology. POLYTECH Health & Aesthetics GmbH serves European markets with its comprehensive product range, while Sientra Inc. has built a strong reputation in North American markets through its focus on quality and innovation. These companies employ various strategies including product innovation, geographic expansion, strategic partnerships, and acquisitions to strengthen their market positions and drive growth.

Porter's Five Forces Analysis of the Breast Reconstruction Market - Competitive forces assessment

The breast reconstruction market exhibits distinct competitive dynamics when analyzed through Porter's Five Forces framework. The threat of new entrants remains moderate due to high barriers to entry, including stringent regulatory requirements, substantial capital investment needs, and the necessity for extensive clinical validation. However, the market does see periodic entry from regional players, particularly in emerging markets, who can compete on price while maintaining acceptable quality standards. The bargaining power of buyers, primarily hospitals and surgical centers, is moderate as they can compare products across multiple suppliers but are often constrained by established relationships and reimbursement requirements. Individual patients have limited direct bargaining power but influence market dynamics through their preferences and choices. Supplier bargaining power is relatively low due to the availability of multiple raw material sources and the presence of established supply chains, though specialized components may command higher prices. The threat of substitute products is moderate, with alternative reconstruction methods such as autologous tissue reconstruction and emerging regenerative medicine approaches providing competition to traditional implant-based solutions. Competitive rivalry within the industry is intense, characterized by ongoing product innovation, aggressive marketing strategies, and price competition, particularly in mature markets. The presence of major multinational players alongside regional competitors creates a dynamic competitive environment that drives continuous innovation and market development.

SWOT Analysis of the Breast Reconstruction Market - Strengths, weaknesses, opportunities, threats

The breast reconstruction market demonstrates a complex interplay of strengths, weaknesses, opportunities, and threats that shape its overall dynamics. Key strengths include advanced technological capabilities in implant design and materials, strong presence of established market players with comprehensive product portfolios, and growing patient awareness about reconstruction options. The market also benefits from supportive regulatory frameworks in many regions and increasing insurance coverage for reconstruction procedures. However, weaknesses exist in the form of high procedural costs that limit accessibility in some markets, potential complications associated with long-term implant usage, and the need for revision surgeries that can impact patient satisfaction. Opportunities abound in emerging markets with improving healthcare infrastructure, technological innovations in implant materials and surgical techniques, and the potential for personalized reconstruction solutions. The market can also benefit from expanding applications beyond traditional breast cancer reconstruction into preventive procedures and gender affirmation surgeries. Threats include stringent regulatory requirements that can delay product approvals, pricing pressures in mature markets, competition from alternative reconstruction methods, and potential negative publicity from implant safety concerns. Additionally, economic downturns and changes in healthcare policies could impact market growth, while the emergence of new competitors in developing markets may challenge established players' market positions.

Breast Reconstruction Market Value Chain Analysis - Industry structure and value flow

The breast reconstruction market value chain encompasses multiple interconnected stages, each contributing to the delivery of comprehensive reconstruction solutions to patients. The chain begins with raw material suppliers who provide specialized silicones, polymers, and other materials essential for implant manufacturing. These materials flow to component manufacturers who produce specialized parts and accessories for reconstruction procedures. Medical device manufacturers then transform these components into finished implants and surgical instruments, incorporating advanced technologies and quality control measures. Distribution networks, including medical distributors and direct sales teams, facilitate the movement of products from manufacturers to healthcare providers. Healthcare providers, primarily hospitals and specialized surgical centers, serve as the primary interface with patients, performing reconstruction procedures and providing post-operative care. Research and development activities span the entire value chain, driving innovation in materials, designs, and surgical techniques. Supporting services, including regulatory affairs, clinical trials, and medical education, provide essential infrastructure for market operations. The value chain also includes insurance companies and reimbursement agencies that influence market accessibility and patient adoption rates. Technology providers contribute digital solutions for surgical planning and patient education, while marketing and communication firms help build awareness and educate both healthcare providers and patients about available options. This complex value chain requires effective coordination and collaboration among all participants to ensure optimal patient outcomes and market growth.

Key Investment Insights in the Breast Reconstruction Market - Strategic investment recommendations

The breast reconstruction market presents compelling investment opportunities driven by strong growth projections and technological innovation potential. Strategic investments should focus on companies developing next-generation implant materials with improved safety profiles and natural aesthetics, as these innovations are likely to capture premium market segments. Digital health technologies, including 3D imaging, virtual surgical planning, and patient education platforms, represent attractive investment targets given their potential to improve surgical outcomes and patient satisfaction. Emerging markets in Asia-Pacific and Latin America offer significant growth potential for both established players and new entrants, particularly those offering cost-effective solutions while maintaining quality standards. Investments in regenerative medicine and tissue engineering approaches could yield substantial returns as these technologies mature and gain regulatory approval. Companies with strong research and development capabilities, comprehensive product portfolios, and established distribution networks are particularly attractive investment targets due to their ability to weather market fluctuations and capitalize on growth opportunities. Strategic partnerships and acquisitions that expand geographic presence or technological capabilities represent another avenue for value creation. However, investors should be mindful of regulatory risks, potential liability issues, and the need for long-term clinical data to support new technologies. Diversification across different market segments and geographic regions can help mitigate risks while maximizing exposure to growth opportunities in this dynamic market.

Breast Reconstruction Market Conclusion - Summary and key takeaways

The breast reconstruction market presents a compelling growth story characterized by technological innovation, expanding patient awareness, and improving access to care. With market size projected to grow from 805.76 Million in 2025 to 1.24 Billion by 2032 at a CAGR of 6.34%, the market demonstrates strong fundamentals and resilience despite challenges posed by the COVID-19 pandemic. Key growth drivers include rising breast cancer incidence rates, technological advancements in implant materials and surgical techniques, and increasing insurance coverage for reconstruction procedures. The market's diverse segmentation across implant types, placement methods, procedural approaches, and technological innovations provides multiple avenues for growth and specialization. While challenges exist in the form of regulatory requirements, pricing pressures, and potential complications, the overall market outlook remains positive. The competitive landscape features established multinational players alongside emerging regional competitors, driving continuous innovation and market development. Investment opportunities abound in next-generation technologies, digital health solutions, and emerging markets, while strategic partnerships and geographic expansion offer pathways for value creation. As the market continues to evolve, success will depend on companies' ability to innovate, adapt to changing patient needs, and navigate complex regulatory environments while maintaining focus on patient safety and outcomes.

Research Methodology - How this research was conducted

This comprehensive market research was conducted using a rigorous, multi-faceted methodology designed to ensure accuracy, reliability, and actionable insights. The research process began with extensive secondary research, including analysis of industry reports, academic publications, regulatory documents, and company financial statements. Primary research formed a crucial component, involving interviews with key opinion leaders, surgeons, industry executives, and market participants to validate findings and gain qualitative insights. Data triangulation techniques were employed to cross-verify information from multiple sources, ensuring consistency and reliability of the research findings. Market size and growth projections were derived using both top-down and bottom-up approaches, considering factors such as procedure volumes, pricing trends, and regional market dynamics. Segmentation analysis was conducted based on extensive market data, customer surveys, and industry expert consultations. The research also incorporated competitive analysis through detailed profiling of key market players, assessment of their product portfolios, and evaluation of their strategic initiatives. Special attention was given to emerging trends, technological developments, and regulatory changes that could impact market dynamics. The research methodology was designed to provide a comprehensive view of the market while maintaining objectivity and analytical rigor throughout the research process.

Research Scope - Coverage and limitations

This research provides comprehensive coverage of the global breast reconstruction market, encompassing all major segments, geographic regions, and market dynamics. The scope includes detailed analysis of market size and growth projections, segmentation by implant types, placement methods, procedural approaches, and technological innovations. Geographic coverage extends across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa regions, with detailed regional analysis of market performance and growth opportunities. The research examines competitive landscape dynamics, including profiling of major market players and their strategic initiatives. However, certain limitations should be acknowledged. The research focuses primarily on commercially available reconstruction solutions and may not fully capture emerging technologies still in development or clinical trials. Market data availability varies across different regions, potentially affecting the granularity of regional analysis in some areas. The research also concentrates on the medical aspects of breast reconstruction and may not fully address broader socio-economic factors that influence market dynamics. Additionally, while comprehensive in scope, the research may not capture every niche player or regional market variation. Despite these limitations, the research provides a robust framework for understanding market dynamics and identifying key growth opportunities in the breast reconstruction industry.

Key Companies and Recent Developments in the Breast Reconstruction Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The breast reconstruction market features several key companies that have made significant recent developments, product launches, and strategic moves to strengthen their market positions. Allergan Plc has continued to expand its Natrelle implant portfolio with new product innovations focused on improved safety and natural aesthetics. The company has also strengthened its global distribution network and invested in digital surgical planning tools. Mentor Worldwide LLC, under Johnson & Johnson's ownership, has launched enhanced implant technologies with improved gel cohesiveness and introduced comprehensive patient education platforms. Establishment Labs S.A. has gained regulatory approvals for its Motiva implants in multiple new markets and expanded its manufacturing capabilities to meet growing global demand. GC Aesthetics PLC has focused on product portfolio optimization and strategic partnerships to enhance its market presence in key regions. Groupe Sebbin SAS has introduced new texturing technologies and expanded its European market presence through targeted acquisitions. Guangzhou Wanhe Plastic Materials Co., Ltd. has increased its research and development investments and obtained additional international certifications to support its export growth. HANSBIOMED CO. LTD has launched innovative implant designs incorporating advanced silicone technologies and expanded its presence in Asian markets. IDEAL IMPLANT INCORPORATED has continued to promote its unique dual-lumen saline technology and obtained new regulatory clearances in additional countries. POLYTECH Health & Aesthetics GmbH has introduced new product lines and strengthened its European distribution network. Sientra Inc. has focused on quality improvements and obtained additional regulatory approvals for its implant portfolio. These companies have also engaged in various strategic partnerships, clinical research collaborations, and marketing initiatives to drive market growth and enhance their competitive positions.