Clean Energy Market Overview - Definition, scope, and significance

The Clean Energy Market encompasses technologies and solutions that generate power from renewable and environmentally sustainable sources. This market includes solar, wind, hydro, geothermal, and bioenergy technologies that produce electricity with minimal environmental impact. Clean energy represents a fundamental shift away from fossil fuel-based power generation toward sustainable alternatives that address climate change concerns. The market's significance lies in its potential to reduce greenhouse gas emissions, enhance energy security, and create new economic opportunities. As global awareness of environmental issues grows, clean energy technologies have transitioned from niche alternatives to mainstream energy solutions, driven by both environmental imperatives and economic viability.

Clean Energy Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

Primary drivers of the clean energy market include increasing environmental regulations, declining technology costs, and growing energy demand. Government policies promoting renewable energy adoption, such as tax incentives and renewable portfolio standards, create favorable market conditions. However, restraints include high initial capital costs, intermittent energy generation from sources like solar and wind, and existing infrastructure investments in fossil fuels. Major challenges involve grid integration, energy storage limitations, and the need for skilled workforce development. Significant opportunities exist in emerging markets, technological innovations in energy storage and smart grids, and the electrification of transportation sectors. The market also benefits from growing corporate sustainability commitments and consumer demand for green energy solutions.

Clean Energy Market Growth Trends - Current and emerging trends shaping the market

The clean energy market is experiencing several transformative trends. Decentralization is becoming prominent as distributed energy resources like rooftop solar and community wind projects gain popularity. Energy storage technologies are rapidly advancing, addressing intermittency challenges and enabling greater renewable energy integration. Digitalization through smart grids and IoT applications is optimizing energy management and improving system efficiency. Offshore wind development is accelerating, particularly in Europe and Asia, with larger turbines and floating platforms expanding viable locations. Green hydrogen production is emerging as a promising clean energy carrier for industrial applications and transportation. Corporate power purchase agreements are increasing, allowing businesses to directly invest in renewable energy projects. These trends collectively indicate a market moving toward greater flexibility, resilience, and sustainability.

COVID-19 Impact on the Clean Energy Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the clean energy market through supply chain interruptions, construction delays, and reduced investment activity. Lockdowns and social distancing measures halted many renewable energy projects, particularly those requiring international collaboration or on-site workforce. However, the pandemic also accelerated certain trends, including increased focus on energy independence and resilience. As economies recover, clean energy markets are experiencing renewed momentum driven by stimulus packages that include green energy investments. The pandemic highlighted the importance of reliable, distributed energy systems, potentially accelerating the transition to clean energy. Long-term, COVID-19 may have strengthened the case for clean energy by demonstrating the need for sustainable, resilient infrastructure systems that can withstand global disruptions.

Clean Energy Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape in the clean energy market features a mix of established energy companies diversifying into renewables and specialized clean energy firms. Major utilities are expanding their renewable portfolios while technology companies are entering the market with innovative solutions. The market shows increasing consolidation as larger players acquire smaller, innovative companies to enhance technological capabilities and market reach. Competition is intensifying in key segments like solar panel manufacturing and wind turbine production, where scale economies are becoming increasingly important. Geographic expansion is a key competitive strategy, with companies targeting emerging markets in Asia, Africa, and Latin America. The competitive dynamics vary significantly by technology segment, with some areas showing mature competition while others remain fragmented with numerous small players.

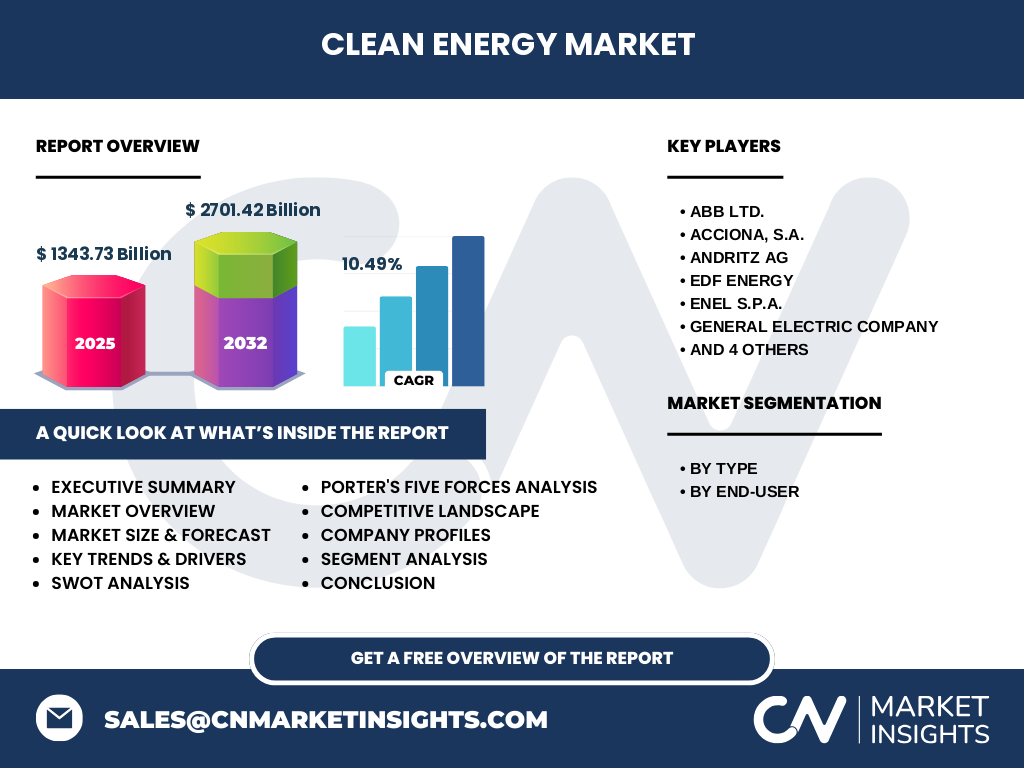

Executive Summary - High-level overview and key findings about Clean Energy Market

The clean energy market is experiencing robust growth driven by environmental concerns, technological advancements, and supportive policies. With a market size of $1,343.73 billion in 2025 and projected to reach $2,701.42 billion by 2032 at a CAGR of 10.49%, the sector demonstrates compelling investment potential. Key trends include declining costs across technologies, increasing energy storage deployment, and growing electrification of transportation and heating sectors. The market faces challenges including grid integration and policy uncertainty, but opportunities abound in emerging markets and technological innovation. Competition is intensifying as traditional energy companies and new entrants vie for market share. The COVID-19 pandemic initially slowed growth but has ultimately reinforced the importance of resilient, sustainable energy systems. Overall, the clean energy market represents a fundamental transformation of global energy systems with significant economic and environmental implications.

Clean Energy Market Forecast - Projections for 2025-2032 period

The clean energy market is projected to experience substantial growth from 2025 to 2032, expanding from $1,343.73 billion to $2,701.42 billion. This represents a compound annual growth rate of 10.49%, indicating strong market momentum across all segments. Solar energy is expected to maintain its position as the fastest-growing segment, driven by continued cost reductions and efficiency improvements. Wind energy will see significant expansion, particularly in offshore installations. Energy storage technologies will experience explosive growth as they become essential for grid stability and renewable integration. The industrial sector will likely lead adoption, followed by commercial and residential segments. Geographic growth will be strongest in Asia-Pacific, driven by China and India's ambitious renewable targets, while North America and Europe will see steady expansion supported by policy frameworks and corporate commitments.

Clean Energy Market Size and Share by Segmentation - Breakdown by {segmentData}

The clean energy market segmentation reveals distinct growth patterns across different categories. By type, solar energy currently represents the largest market share, followed by wind energy and hydro power. Solar installations continue to grow rapidly due to falling photovoltaic costs and improved efficiency. Wind energy shows strong growth in both onshore and offshore segments, with offshore wind gaining particular momentum in coastal regions. Bioenergy maintains steady growth, particularly in industrial applications and developing economies. Geothermal energy, while representing a smaller share, shows consistent growth in geologically favorable regions. By end-user, the industrial segment dominates market share due to large-scale manufacturing and processing facilities adopting renewable energy solutions. Commercial applications are growing rapidly as businesses seek to reduce operational costs and meet sustainability goals. Residential adoption continues to expand, driven by rooftop solar installations and supportive policies.

Global Clean Energy Market Size and Share by Region - Geographic distribution

The global clean energy market exhibits significant regional variations in adoption rates, policy frameworks, and market maturity. Asia-Pacific dominates the market, accounting for the largest share due to massive investments in China, India, and Japan. China alone represents a substantial portion of global clean energy capacity, driven by aggressive renewable energy targets and manufacturing capabilities. Europe shows strong adoption rates, particularly in countries like Germany, Denmark, and the UK, supported by comprehensive policy frameworks and high environmental awareness. North America demonstrates steady growth, with the United States leading in wind and solar installations while Canada focuses on hydro and emerging technologies. Latin America shows promising growth, particularly in solar and wind energy, with Brazil and Chile emerging as key markets. The Middle East and Africa, while currently representing a smaller share, are experiencing rapid growth driven by abundant solar resources and increasing energy demand.

Regional Analysis of the Clean Energy Market - Detailed regional market performance

Regional analysis reveals distinct market dynamics across different geographies. In Asia-Pacific, China's dominance in solar panel manufacturing and installation creates a unique market ecosystem, while India's ambitious renewable targets drive rapid capacity additions. Japan's focus on offshore wind and hydrogen technologies represents a different development path. Europe's mature market shows sophisticated policy frameworks, with countries like Denmark and Germany leading in wind energy integration and smart grid technologies. The region's carbon pricing mechanisms create additional market incentives. North America demonstrates regional variations, with California and Texas leading U.S. installations while Canada leverages its hydroelectric resources. Latin America benefits from excellent solar and wind resources, with Chile's Atacama Desert becoming a solar hub and Brazil expanding wind capacity. Africa's clean energy market, though smaller, shows potential for leapfrogging traditional energy infrastructure through distributed renewable solutions.

Leading Company Profiles in the Clean Energy Market - Industry players and strategies

Leading companies in the clean energy market employ diverse strategies to capture market share. ABB Ltd. focuses on power grid technologies and automation solutions that enable renewable energy integration. Acciona, S.A. leverages its Spanish heritage to dominate wind and solar projects across Europe and Latin America. Andritz AG specializes in hydro power solutions and biomass technologies, maintaining strong positions in Europe and Asia. EDF Energy combines traditional utility expertise with aggressive renewable expansion in Europe. Enel S.p.A. has transformed from a traditional utility to a global clean energy leader through strategic acquisitions and innovative business models. General Electric Company maintains significant wind turbine manufacturing capabilities while developing hybrid renewable solutions. Iberdrola SA. pursues aggressive international expansion, particularly in offshore wind. Siemens Energy AG focuses on grid technologies and hybrid power plants. Voith GmbH & Co. KGaA specializes in hydro power and digital grid solutions. Xcel Energy Inc. demonstrates successful utility-scale renewable integration in North America.

Porter's Five Forces Analysis of the Clean Energy Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the clean energy market. The threat of new entrants remains moderate due to high capital requirements and regulatory complexities, though technology advancements are lowering barriers in some segments. Bargaining power of suppliers varies by technology, with solar panel and wind turbine manufacturers holding significant leverage due to concentrated supply chains. The bargaining power of buyers is increasing as large corporations and utilities negotiate better terms and demand higher quality standards. Threat of substitutes exists from both traditional energy sources and competing renewable technologies, creating ongoing competitive pressure. Industry rivalry is intense, particularly in mature markets, with companies competing on price, technology, and service quality. Overall, the competitive landscape is characterized by moderate to high intensity, driving innovation and efficiency improvements while maintaining attractive growth prospects.

SWOT Analysis of the Clean Energy Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the clean energy market reveals key strategic insights. Strengths include declining technology costs, improving efficiency, and growing environmental awareness. The market benefits from strong policy support in many regions and increasing corporate commitments to sustainability. Weaknesses encompass intermittency issues, high initial capital costs, and grid integration challenges. The market also faces skilled workforce shortages and supply chain vulnerabilities. Opportunities abound in emerging markets, technological innovations in energy storage and smart grids, and the electrification of transportation sectors. Growing demand for green hydrogen and sustainable industrial processes presents additional growth avenues. Threats include policy uncertainty, competition from fossil fuels, and potential supply chain disruptions. Trade tensions affecting critical materials and potential overcapacity in certain technologies also pose risks. Overall, the market's strengths and opportunities significantly outweigh weaknesses and threats, indicating positive long-term prospects.

Clean Energy Market Value Chain Analysis - Industry structure and value flow

The clean energy value chain encompasses multiple interconnected stages from raw materials to end-user consumption. The upstream segment includes component manufacturing for solar panels, wind turbines, and other technologies, along with raw material extraction for critical minerals. Midstream activities involve system integration, project development, and energy storage solutions. Downstream operations include installation, maintenance, and grid connection services. Key players operate across multiple value chain stages, while specialized companies focus on specific segments. The value chain demonstrates increasing complexity as technologies mature and markets expand. Digital technologies are transforming value chain operations through improved monitoring, predictive maintenance, and optimized energy management. Supply chain resilience has become a critical concern, particularly for components sourced from concentrated geographic regions. The value chain continues to evolve with emerging technologies creating new opportunities and disrupting traditional relationships.

Key Investment Insights in the Clean Energy Market - Strategic investment recommendations

Investment insights for the clean energy market highlight several strategic opportunities. Solar energy investments remain attractive due to declining costs and improving efficiency, particularly in emerging markets with high solar irradiance. Energy storage technologies present compelling investment opportunities as they address renewable intermittency and enable greater grid integration. Offshore wind investments offer stable returns in regions with supportive policies and strong wind resources. Green hydrogen production represents a promising long-term investment, particularly for industrial applications and energy storage. Smart grid technologies and digitalization solutions provide opportunities to improve system efficiency and enable higher renewable penetration. Investors should consider geographic diversification, focusing on regions with strong policy support and growing energy demand. Technology diversification across different renewable sources can mitigate risks associated with specific technology developments or policy changes. Overall, the clean energy market offers attractive risk-adjusted returns with significant growth potential over the forecast period.

Clean Energy Market Conclusion - Summary and key takeaways

The clean energy market stands at a pivotal juncture, characterized by robust growth, technological innovation, and increasing mainstream adoption. With a projected market size expanding from $1,343.73 billion in 2025 to $2,701.42 billion by 2032 at a CAGR of 10.49%, the sector demonstrates compelling investment potential. Key drivers include declining technology costs, supportive policies, and growing environmental awareness, while challenges such as grid integration and intermittency are being addressed through technological advancements. The market's segmentation reveals diverse opportunities across different technologies and end-user applications, with regional variations creating distinct investment landscapes. Leading companies are pursuing aggressive expansion strategies, while competitive dynamics continue to evolve. Overall, the clean energy market represents a fundamental transformation of global energy systems, offering significant economic opportunities while addressing critical environmental challenges.

Research Methodology - How this research was conducted

This research employed a comprehensive methodology combining primary and secondary data sources to provide accurate market insights. Primary research involved interviews with industry experts, company executives, and key stakeholders across the clean energy value chain. Secondary research utilized reputable industry reports, government publications, and financial statements to validate findings and establish market trends. Data triangulation techniques were applied to ensure accuracy and reliability of market size calculations and growth projections. The research considered both top-down and bottom-up approaches to estimate market values and segment shares. Geographic analysis incorporated regional policy frameworks, economic indicators, and technology adoption rates. Competitive analysis examined company strategies, market positioning, and recent developments. The methodology also accounted for macroeconomic factors, technological advancements, and regulatory environments to provide a holistic market assessment.

Research Scope - Coverage and limitations

This research covers the global clean energy market from 2025 to 2032, focusing on key technologies including solar, wind, hydro, geothermal, and bioenergy. The scope encompasses market size, growth trends, competitive landscape, and regional analysis across major geographic regions. Market segmentation analysis examines different technologies and end-user applications, while company profiles highlight leading industry players and their strategies. The research also includes strategic analyses such as Porter's Five Forces and SWOT analysis to provide comprehensive market insights. Limitations include potential data availability constraints in certain emerging markets, the rapidly evolving nature of technology affecting long-term projections, and the impact of unforeseen policy changes or global events. The research focuses on commercially viable clean energy technologies and does not cover experimental or niche applications that lack significant market presence.

Key Companies and Recent Developments in the Clean Energy Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Leading companies in the clean energy market continue to drive innovation through strategic developments and partnerships. ABB Ltd. recently announced advancements in grid automation technologies to improve renewable energy integration. Acciona, S.A. expanded its solar portfolio in Latin America through new project developments. Andritz AG launched next-generation hydro turbines with improved efficiency ratings. EDF Energy formed strategic partnerships to accelerate offshore wind development in European markets. Enel S.p.A. announced significant investments in energy storage systems across its global operations. General Electric Company introduced new wind turbine models with larger capacities and improved performance. Iberdrola SA. completed major offshore wind farm projects in European waters. Siemens Energy AG unveiled innovative hybrid power plant solutions combining multiple renewable technologies. Voith GmbH & Co. KGaA launched advanced digital monitoring systems for hydro power plants. Xcel Energy Inc. announced ambitious renewable energy targets and grid modernization initiatives in its North American service territories.