Air Cargo Market Overview - Definition, scope, and significance

The air cargo market represents a critical segment of global logistics, encompassing the transportation of goods via aircraft. This market includes both dedicated cargo aircraft and passenger aircraft belly-hold capacity, serving as a vital link in international trade and supply chain management. Air cargo provides speed and reliability for time-sensitive shipments, making it essential for industries requiring rapid delivery, such as pharmaceuticals, electronics, and perishables. The market's significance extends beyond mere transportation, as it enables just-in-time manufacturing, supports e-commerce growth, and facilitates global commerce by connecting distant markets efficiently.

Air Cargo Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The air cargo market is driven by several key factors including the exponential growth of e-commerce, increasing demand for temperature-sensitive pharmaceuticals, and the expansion of international trade. The rise of cross-border e-commerce platforms and consumer expectations for rapid delivery have significantly boosted demand for air freight services. However, the market faces restraints such as high operational costs, environmental concerns, and capacity constraints. Challenges include volatile fuel prices, geopolitical tensions affecting trade routes, and the need for technological upgrades. Opportunities exist in the form of digital transformation through cargo tracking technologies, sustainable aviation initiatives, and the potential for dedicated freighter fleet expansion to meet growing demand.

Air Cargo Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the air cargo market include the increasing adoption of digital platforms for booking and tracking shipments, the integration of IoT devices for real-time cargo monitoring, and the emergence of specialized cargo handling facilities. The market is witnessing a shift toward dedicated freighter operations as passenger belly-hold capacity remains constrained. Additionally, there is growing interest in sustainable aviation fuel and electric cargo aircraft development to address environmental concerns. The pharmaceutical and healthcare sectors are driving demand for temperature-controlled shipping solutions, while the consumer electronics industry continues to rely on air cargo for just-in-time inventory management.

COVID-19 Impact on the Air Cargo Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the air cargo market through reduced passenger flights and supply chain interruptions. However, the crisis paradoxically accelerated market growth as air cargo became essential for transporting medical supplies, vaccines, and personal protective equipment globally. The pandemic highlighted the critical role of air freight in crisis response and supply chain resilience. As recovery progresses, the market is experiencing a rebound driven by e-commerce growth, with passenger airlines gradually restoring services and freighter operators expanding capacity. The pandemic has also accelerated digitalization and automation trends within the industry, with a focus on contactless operations and enhanced cargo tracking capabilities.

Air Cargo Market Competitive Landscape - Major competitors and market consolidation

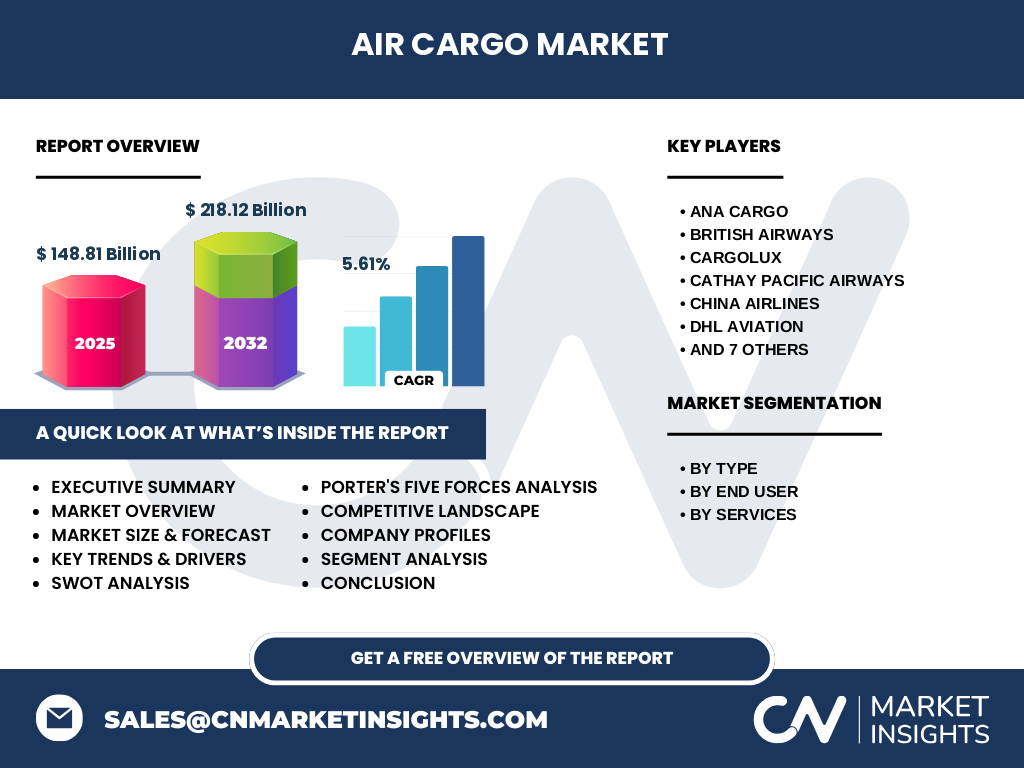

The air cargo market features a competitive landscape dominated by major international airlines and logistics providers, including ANA CARGO, British Airways, Cargolux, Cathay Pacific Airways, China Airlines, DHL Aviation, Emirates, FedEx Express, Korean Air Cargo, Lufthansa, Singapore Airlines Cargo, UPS Airlines, and Zela Aviation. The market exhibits a mix of global carriers with extensive networks and regional specialists serving niche markets. Competition centers on service quality, network coverage, pricing strategies, and technological capabilities. Market consolidation trends include strategic partnerships, joint ventures, and alliances to expand route networks and optimize capacity utilization. The competitive landscape is characterized by the presence of both integrated carriers offering door-to-door services and specialized freight operators focusing on specific cargo types or routes.

Executive Summary - High-level overview and key findings about Air Cargo Market

The air cargo market represents a dynamic and essential component of global logistics, with a projected growth trajectory showing a market size of 148.81 Billion in 2026 and a forecast of 218.12 Billion by 2033, representing a CAGR of 5.61%. Key findings indicate that the market is being driven by e-commerce expansion, pharmaceutical logistics growth, and increasing demand for time-sensitive shipments. The competitive landscape features major international carriers and logistics providers competing on service quality and network coverage. Market segmentation reveals distinct opportunities across different cargo types, end-user industries, and service models. The COVID-19 pandemic has underscored the market's critical role in global supply chains, accelerating trends toward digitalization and specialized cargo handling capabilities.

Air Cargo Market Forecast - Projections for 2025-2032 period

The air cargo market is projected to experience steady growth from 2025 to 2032, with the market size expected to reach 148.81 Billion in 2026 and expand to 218.12 Billion by 2033, representing a compound annual growth rate of 5.61%. This growth trajectory reflects the market's resilience and adaptability in the face of global economic fluctuations and supply chain challenges. The forecast period is expected to see continued expansion in e-commerce-driven cargo volumes, increased pharmaceutical and healthcare shipments, and growing demand for specialized logistics services. Capacity constraints and environmental considerations may influence growth rates, while technological advancements in cargo handling and tracking systems are anticipated to enhance operational efficiency and support market expansion.

Air Cargo Market Size and Share by Segmentation - Breakdown by {segmentData}

The air cargo market segmentation reveals distinct patterns across different categories. By type, the market is divided between air mail and air freight, with air freight dominating due to its broader application in commercial logistics. End-user segmentation shows retail as a major segment, driven by e-commerce growth, while pharmaceutical and healthcare represents a high-value segment requiring specialized handling. The food and beverage sector demands temperature-controlled solutions, and consumer electronics continues to rely on air cargo for just-in-time delivery. Service-based segmentation distinguishes between express services, which command premium pricing for urgent shipments, and regular services offering cost-effective solutions for less time-sensitive cargo. Each segment presents unique growth opportunities and operational requirements.

Global Air Cargo Market Size and Share by Region - Geographic distribution

The global air cargo market exhibits varying dynamics across different regions, reflecting economic development levels, trade patterns, and infrastructure capabilities. Asia-Pacific dominates the market due to strong manufacturing bases, particularly in China, and growing e-commerce activity. North America maintains significant market share driven by technological innovation and robust consumer demand. Europe benefits from extensive trade networks and sophisticated logistics infrastructure. The Middle East serves as a crucial transit hub connecting Asia, Europe, and Africa, while Latin America and Africa represent emerging markets with growing potential. Regional variations in regulatory frameworks, airport infrastructure, and economic conditions influence market dynamics and growth opportunities across different geographic areas.

Regional Analysis of the Air Cargo Market - Detailed regional market performance

Regional analysis of the air cargo market reveals distinct performance patterns and growth drivers across different geographic areas. Asia-Pacific leads in volume and growth rate, driven by manufacturing powerhouses like China and expanding e-commerce markets in Southeast Asia. North America demonstrates strong performance in high-value cargo segments and technological innovation, with major logistics hubs in the United States and Canada. Europe maintains a mature market characterized by sophisticated logistics networks and strong intra-regional trade. The Middle East has emerged as a critical transit region, with hubs like Dubai International Airport becoming major cargo centers. Latin America and Africa, while smaller markets, show promising growth potential driven by increasing trade integration and infrastructure development initiatives.

Leading Company Profiles in the Air Cargo Market - Industry players and strategies

Leading companies in the air cargo market include ANA CARGO, British Airways, Cargolux, Cathay Pacific Airways, China Airlines, DHL Aviation, Emirates, FedEx Express, Korean Air Cargo, Lufthansa, Singapore Airlines Cargo, UPS Airlines, and Zela Aviation. These companies employ diverse strategies to maintain competitive advantage, including fleet modernization, route network expansion, and service differentiation. Major carriers focus on integrating passenger and cargo operations to optimize capacity utilization, while dedicated freighter operators emphasize specialized handling capabilities. Logistics giants like DHL, FedEx, and UPS leverage their extensive ground networks to offer door-to-door solutions. Emirates and other Middle Eastern carriers capitalize on their geographic positioning as global transit hubs. Strategic partnerships and alliances are common strategies to expand market reach and enhance service offerings.

Porter's Five Forces Analysis of the Air Cargo Market - Competitive forces assessment

Porter's Five Forces analysis of the air cargo market reveals a competitive landscape shaped by several key factors. The threat of new entrants remains moderate due to high capital requirements and regulatory barriers, though niche operators can still find opportunities. Bargaining power of buyers is increasing as large shippers consolidate and demand better rates and service quality. Supplier power is significant, particularly for aircraft manufacturers and fuel suppliers, impacting operational costs. The threat of substitutes includes sea freight for non-urgent shipments and emerging technologies like drone delivery for last-mile segments. Competitive rivalry is intense among major carriers, with price competition, service differentiation, and network expansion being key strategies. Overall, the market structure supports reasonable profitability for well-positioned operators despite ongoing cost pressures.

SWOT Analysis of the Air Cargo Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the air cargo market reveals key strategic factors. Strengths include the market's critical role in global supply chains, speed and reliability advantages over other transport modes, and technological advancements in cargo handling and tracking. Weaknesses encompass high operational costs, environmental impact concerns, and vulnerability to economic fluctuations. Opportunities exist in the growing e-commerce sector, pharmaceutical logistics expansion, and emerging markets development. Threats include geopolitical tensions affecting trade routes, regulatory changes impacting operations, and potential economic downturns reducing cargo volumes. The analysis indicates that successful market participants will need to leverage strengths while addressing weaknesses, capitalize on opportunities, and develop strategies to mitigate threats.

Air Cargo Market Value Chain Analysis - Industry structure and value flow

The air cargo market value chain encompasses multiple stages and participants, creating a complex ecosystem of interrelated services. The chain begins with shippers and manufacturers who generate cargo demand, followed by freight forwarders who consolidate shipments and manage documentation. Airlines provide the core transportation service, while ground handlers manage airport operations including loading, unloading, and warehousing. Customs authorities regulate cross-border movements, and final delivery is often handled by logistics providers or postal services. Value is added at each stage through specialized services such as temperature-controlled handling, dangerous goods management, and time-definite delivery. Technology providers contribute through cargo tracking systems, booking platforms, and operational software, while infrastructure providers including airports and ground transportation services enable the physical movement of goods.

Key Investment Insights in the Air Cargo Market - Strategic investment recommendations

Investment insights in the air cargo market highlight several strategic areas for potential returns. Key investment opportunities include dedicated freighter fleet expansion to meet growing demand, particularly for e-commerce and pharmaceutical shipments. Technology investments in cargo tracking, automation, and digital booking platforms offer potential for operational efficiency improvements and cost reduction. Infrastructure development at major cargo hubs and emerging market airports presents long-term growth potential. Sustainable aviation initiatives, including investments in electric cargo aircraft and sustainable fuel technologies, align with environmental trends and potential regulatory requirements. Strategic partnerships and joint ventures can provide market access and operational synergies. Investors should consider the market's cyclical nature and focus on companies with strong balance sheets and diversified service offerings to mitigate risk.

Air Cargo Market Conclusion - Summary and key takeaways

The air cargo market demonstrates robust growth potential with a projected market size of 148.81 Billion in 2026 expanding to 218.12 Billion by 2033 at a CAGR of 5.61%. Key takeaways include the market's critical role in global supply chains, driven by e-commerce growth, pharmaceutical logistics, and increasing demand for time-sensitive shipments. The competitive landscape features major international carriers and logistics providers employing diverse strategies to maintain market position. Regional variations create distinct opportunities, with Asia-Pacific leading growth while other regions offer specialized market segments. Technology adoption, sustainability initiatives, and infrastructure development are shaping the market's evolution. Success in this market requires operational excellence, strategic partnerships, and adaptation to changing customer needs and regulatory requirements.

Research Methodology - How this research was conducted

This research on the air cargo market was conducted using a comprehensive methodology combining primary and secondary data sources. Primary research included interviews with industry experts, logistics operators, and market analysts to gather current market insights and trends. Secondary research involved analysis of industry reports, financial statements, company publications, and government trade data. Market sizing was determined through bottom-up analysis of segment data, regional performance, and company financials. The research methodology employed both qualitative and quantitative approaches to ensure comprehensive coverage of market dynamics, competitive landscape, and growth projections. Data validation was performed through triangulation of multiple sources to ensure accuracy and reliability of findings.

Research Scope - Coverage and limitations

The research scope for this air cargo market analysis encompasses the global market from 2025 to 2032, focusing on key market segments, regional performance, and competitive dynamics. Coverage includes detailed analysis of market size, growth trends, and segmentation by cargo type, end-user industry, and service model. The research examines major geographic regions and profiles leading market participants. Limitations of the research include potential variations in data availability across different regions and market segments, as well as the inherent uncertainty in long-term market projections. The analysis is based on available market data and expert insights but may not capture all local market nuances or emerging trends that could impact future market development.

Key Companies and Recent Developments in the Air Cargo Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Key companies in the air cargo market, including ANA CARGO, British Airways, Cargolux, Cathay Pacific Airways, China Airlines, DHL Aviation, Emirates, FedEx Express, Korean Air Cargo, Lufthansa, Singapore Airlines Cargo, UPS Airlines, and Zela Aviation, have been actively pursuing strategic developments to strengthen their market positions. Recent activities include fleet modernization initiatives with new generation aircraft to improve fuel efficiency and cargo capacity. Companies are expanding route networks to serve emerging markets and e-commerce hubs, with particular focus on Asia-Pacific growth corridors. Strategic partnerships and joint ventures are being formed to enhance service coverage and operational efficiency. Digital transformation efforts include investments in cargo tracking technologies, automated handling systems, and customer-facing booking platforms. Sustainability initiatives are gaining prominence, with companies investing in sustainable aviation fuel programs and exploring electric cargo aircraft development. These strategic developments reflect the industry's adaptation to changing market demands and operational challenges.