Additive Manufacturing Market Overview - Definition, scope, and significance

Additive Manufacturing (AM), also known as 3D printing, is a transformative approach to industrial production that enables the creation of lighter, stronger parts and systems. This technology builds three-dimensional objects layer by layer from digital models, fundamentally changing how products are designed, developed, and manufactured. The scope of additive manufacturing extends across various industries, including aerospace, automotive, healthcare, and industrial manufacturing, where it offers unprecedented design freedom, reduced waste, and the ability to produce complex geometries that would be impossible with traditional manufacturing methods. The significance of this market lies in its potential to revolutionize supply chains, enable mass customization, reduce time-to-market, and create new business models centered around on-demand production and distributed manufacturing networks.

Additive Manufacturing Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The additive manufacturing market is driven by several key factors, including the increasing demand for customized products, the need for rapid prototyping, and the growing adoption of 3D printing in end-use applications. Industries are recognizing the potential for cost reduction, weight optimization, and supply chain simplification that AM offers. However, the market faces restraints such as high initial equipment costs, limited material options compared to traditional manufacturing, and the need for specialized expertise. Challenges include quality control issues, certification requirements for critical applications, and the slow production speeds for large-scale manufacturing. Despite these obstacles, significant opportunities exist in emerging applications such as bioprinting, construction, and electronics, as well as in the development of new materials and multi-material printing capabilities that could expand the technology's reach and impact.

Additive Manufacturing Market Growth Trends - Current and emerging trends shaping the market

The additive manufacturing market is experiencing several notable growth trends that are reshaping the industry landscape. One prominent trend is the shift from prototyping to production, with more companies adopting AM for end-use parts rather than just design validation. Another significant trend is the integration of AM with traditional manufacturing processes, creating hybrid systems that combine the benefits of both approaches. The market is also seeing increased investment in metal additive manufacturing, particularly for aerospace and medical applications where high-performance materials are critical. Emerging trends include the development of larger build volumes to accommodate bigger parts, improvements in printing speeds through parallel processing and advanced hardware, and the growing use of artificial intelligence and machine learning to optimize designs and printing parameters. Additionally, there is a trend toward more sustainable manufacturing practices, with AM's ability to reduce material waste and enable localized production contributing to environmental goals.

COVID-19 Impact on the Additive Manufacturing Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the additive manufacturing market, initially causing disruptions in supply chains and manufacturing operations. However, the crisis also highlighted the agility and resilience of AM technology, as companies rapidly pivoted to produce critical medical supplies such as ventilator parts, face shields, and nasopharyngeal swabs. This accelerated adoption demonstrated AM's potential for distributed manufacturing and on-demand production, leading to increased interest from industries seeking to build more resilient supply chains. The pandemic also spurred investment in digital manufacturing technologies and remote collaboration tools, which complemented AM's capabilities. As the market recovers, we're seeing a renewed focus on reshoring and nearshoring production, with AM playing a crucial role in enabling localized manufacturing. The healthcare sector's experience with AM during the pandemic is likely to drive continued innovation and adoption in medical applications, from personalized implants to pharmaceutical manufacturing.

Additive Manufacturing Market Competitive Landscape - Major competitors and market consolidation

The additive manufacturing market features a diverse competitive landscape with a mix of established industrial companies, specialized AM firms, and emerging startups. Key players include 3D Systems, Stratasys, EOS, and Materialise, which have been instrumental in developing and commercializing AM technologies. The market is witnessing increased consolidation as larger companies acquire innovative startups to expand their technology portfolios and market reach. For instance, Desktop Metal's acquisition of EnvisionTEC and Markforged's purchase of Digital Metal demonstrate this trend toward market consolidation. Competition is intensifying in specific segments, particularly in metal additive manufacturing, where companies like 3D Systems and Stratasys are challenging established players like EOS and SLM Solutions. The competitive landscape is also being shaped by the entry of major technology companies such as HP and Siemens, which bring significant resources and expertise to the market. This dynamic environment is driving rapid innovation, with companies competing on factors such as print speed, material quality, build volume, and software capabilities.

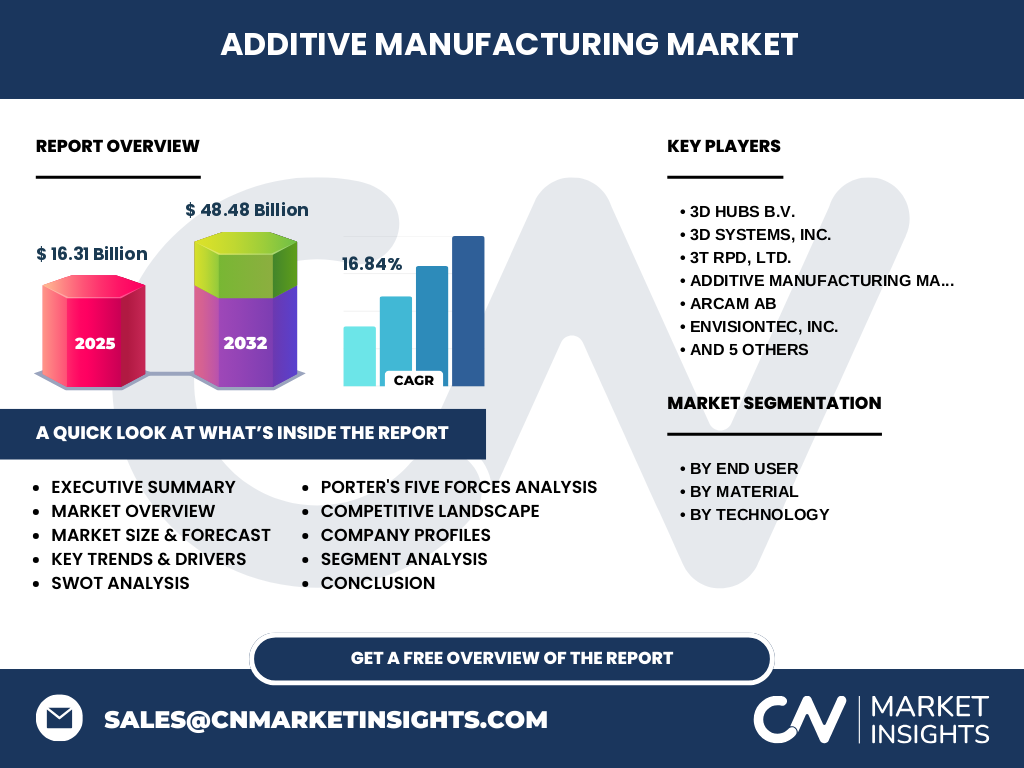

Executive Summary - High-level overview and key findings about Additive Manufacturing Market

The additive manufacturing market is at a critical juncture, transitioning from a technology primarily used for prototyping to a viable production solution across multiple industries. With a market size of $16.31 billion in 2026 and a projected growth to $48.48 billion by 2033, representing a robust CAGR of 16.84%, the industry is experiencing rapid expansion driven by technological advancements and increasing adoption. Key findings indicate that the healthcare and aerospace sectors are leading adopters, leveraging AM for customized medical implants and lightweight aircraft components respectively. The market is characterized by ongoing innovation in materials science, with significant developments in metal and high-performance polymers expanding application possibilities. However, challenges remain in terms of production speed, cost-effectiveness for mass production, and the need for standardized quality control processes. The competitive landscape is evolving, with traditional manufacturing giants entering the space and strategic partnerships becoming increasingly common as companies seek to leverage complementary strengths in software, hardware, and materials.

Additive Manufacturing Market Forecast - Projections for 2025-2032 period

The additive manufacturing market is poised for substantial growth over the forecast period of 2025-2032, with projections indicating a significant expansion from the current market size. Starting from a base of $16.31 billion in 2026, the market is expected to reach $48.48 billion by 2033, reflecting a compound annual growth rate (CAGR) of 16.84%. This growth trajectory is underpinned by several factors, including the increasing adoption of AM in production applications, advancements in printing technologies, and the expansion of material options. The forecast period will likely see a continued shift towards metal additive manufacturing, driven by demand from aerospace, automotive, and medical industries. Software and services segments are also expected to grow as the industry matures, with an increasing focus on workflow optimization and post-processing solutions. Regional growth will vary, with Asia-Pacific expected to show the highest growth rates due to increasing industrialization and government support for advanced manufacturing technologies. The forecast also suggests a growing trend towards integrated AM solutions, where hardware, software, and materials are offered as a comprehensive package by single providers.

Additive Manufacturing Market Size and Share by Segmentation - Breakdown by {segmentData}

The additive manufacturing market can be segmented by end user, material, and technology, each showing distinct growth patterns and market shares. By end user, the aerospace and healthcare sectors are expected to dominate, driven by the need for lightweight components and customized medical devices respectively. The automotive industry is also a significant contributor, utilizing AM for both prototyping and production of complex parts. In terms of materials, plastics currently hold the largest market share due to their versatility and cost-effectiveness, but metals are the fastest-growing segment, particularly in high-performance applications. The technology segment is led by selective laser sintering (SLS) and stereolithography (SLA), which offer high precision and material versatility. Fused deposition modeling (FDM) remains popular for its accessibility and ease of use, particularly in desktop applications. The market share distribution is dynamic, with emerging technologies like binder jetting and directed energy deposition gaining traction in specific applications. As the market evolves, we expect to see increased segmentation based on specific industry needs, with customized solutions becoming more prevalent.

Global Additive Manufacturing Market Size and Share by Region - Geographic distribution

The global additive manufacturing market exhibits varying growth rates and adoption levels across different regions, reflecting diverse industrial landscapes and technological readiness. North America currently leads the market, driven by strong adoption in aerospace, defense, and healthcare sectors, as well as significant R&D investments. Europe follows closely, with countries like Germany, the UK, and France showing high adoption rates, particularly in automotive and industrial manufacturing. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by rapid industrialization, government initiatives supporting advanced manufacturing, and the presence of large consumer electronics and automotive industries in countries like China, Japan, and South Korea. Emerging economies in Southeast Asia are also showing increased interest in AM technologies as part of their industrial development strategies. Latin America and the Middle East & Africa regions, while currently smaller markets, are expected to see gradual growth as awareness and capabilities in AM technologies expand. The regional distribution of market share is likely to evolve, with Asia-Pacific potentially challenging North America's dominance by the end of the forecast period.

Regional Analysis of the Additive Manufacturing Market - Detailed regional market performance

A detailed regional analysis of the additive manufacturing market reveals distinct patterns of adoption and growth across different geographic areas. In North America, the United States leads the market, driven by strong demand from aerospace and defense contractors, as well as a robust ecosystem of AM service bureaus and research institutions. Canada is also making significant strides, particularly in metal additive manufacturing for the automotive and aerospace sectors. Europe shows a diverse landscape, with Germany emerging as a leader in industrial AM applications, particularly in automotive and industrial machinery. The UK and France are strong in aerospace and medical applications, while Scandinavian countries are notable for their adoption of metal AM in various industries. In the Asia-Pacific region, China is rapidly expanding its AM capabilities, supported by government initiatives and a growing domestic market. Japan and South Korea are leveraging their strengths in electronics and automotive manufacturing to drive AM adoption. India is showing increasing interest in AM for its aerospace and healthcare sectors. Each region faces unique challenges, from regulatory environments to access to skilled workforce, which influence the pace and nature of AM adoption and market growth.

Leading Company Profiles in the Additive Manufacturing Market - Industry players and strategies

The additive manufacturing market is characterized by a mix of established industrial giants and specialized AM companies, each employing distinct strategies to capture market share. 3D Systems, one of the pioneers in the field, continues to innovate across multiple AM technologies, focusing on expanding its materials portfolio and enhancing software capabilities. Stratasys, another key player, has strengthened its position through strategic acquisitions and a focus on production-oriented solutions. EOS GmbH, a leader in industrial metal AM, emphasizes high-quality metal printing systems and comprehensive customer support. Desktop Metal has gained attention with its office-friendly metal 3D printers and recent acquisition of EnvisionTEC, expanding its technology offerings. Materialise stands out for its software solutions and medical AM applications, while companies like Arcam AB (now part of GE Additive) specialize in electron beam melting technology for metal parts. These companies are pursuing various strategies, including vertical integration, partnerships with material suppliers, and expansion into new geographic markets. The competitive landscape is further shaped by the entry of major corporations like HP and Siemens, which bring significant resources and cross-industry expertise to the AM market.

Porter's Five Forces Analysis of the Additive Manufacturing Market - Competitive forces assessment

Applying Porter's Five Forces analysis to the additive manufacturing market reveals a dynamic competitive environment. The threat of new entrants is moderate to high, given the continuous technological advancements and relatively low barriers to entry in some segments, particularly for desktop 3D printing. However, industrial-grade AM systems require significant R&D investment and expertise, creating a barrier for some potential competitors. The bargaining power of suppliers is increasing as the demand for specialized materials grows, though large AM companies are mitigating this through vertical integration and long-term supplier agreements. Buyers' bargaining power varies; large aerospace and automotive companies can negotiate favorable terms due to their volume, while smaller businesses may have less leverage. The threat of substitutes is moderate, as traditional manufacturing methods still dominate for many applications, but AM's unique capabilities in producing complex geometries and customized parts provide a competitive edge. Competitive rivalry is intense, with companies competing on technology, materials, software, and services. The market is also seeing increased collaboration between competitors and with end-users, blurring traditional competitive boundaries and creating a more complex industry structure.

SWOT Analysis of the Additive Manufacturing Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the additive manufacturing market reveals several key factors shaping its current state and future prospects. Strengths of the market include the technology's ability to produce complex geometries impossible with traditional methods, reduced material waste compared to subtractive manufacturing, and the potential for mass customization. The growing ecosystem of materials, software, and services also strengthens the market's foundation. However, weaknesses persist, such as limited production speeds for large-scale manufacturing, high initial equipment costs, and the need for specialized expertise to operate and maintain AM systems effectively. Opportunities abound in emerging applications like bioprinting, construction, and electronics, as well as in the development of new materials and multi-material printing capabilities. The market also has the opportunity to capitalize on trends towards reshoring and distributed manufacturing. Threats to the market include potential regulatory hurdles, especially in medical and aerospace applications, the risk of technological obsolescence as new methods emerge, and economic uncertainties that could impact investment in new manufacturing technologies. Additionally, the market faces challenges from intellectual property concerns and the need to establish industry standards for quality and certification.

Additive Manufacturing Market Value Chain Analysis - Industry structure and value flow

The additive manufacturing market value chain is a complex ecosystem involving multiple stakeholders and processes, from initial design to final product delivery. At the beginning of the value chain, original equipment manufacturers (OEMs) develop and produce 3D printers, while material suppliers provide the raw materials in various forms such as powders, filaments, or resins. Software companies contribute crucial design and simulation tools, including computer-aided design (CAD) software and print preparation applications. Service bureaus and in-house production facilities form the next link, operating the printers and managing the production process. Post-processing companies specialize in improving the surface finish and mechanical properties of printed parts through various techniques like heat treatment or surface coating. Distribution channels, including direct sales and partnerships with industrial distributors, connect manufacturers with end-users. At the end of the value chain, a diverse range of industries, from aerospace to healthcare, utilize AM for prototyping, tooling, and production of end-use parts. The value flow is characterized by continuous innovation, with each segment of the chain contributing to improvements in speed, quality, and material options. As the market matures, we're seeing increased integration across the value chain, with companies offering comprehensive solutions that combine hardware, software, and materials.

Key Investment Insights in the Additive Manufacturing Market - Strategic investment recommendations

Investment in the additive manufacturing market presents numerous opportunities, but also requires careful consideration of market dynamics and technological trends. Strategic investments should focus on companies and technologies that address key industry challenges, such as improving print speeds, expanding material options, and enhancing post-processing capabilities. The metal additive manufacturing segment offers significant growth potential, particularly for applications in aerospace, automotive, and medical industries where high-performance materials are critical. Software and services represent another attractive investment area, as the industry moves towards more integrated solutions and the need for specialized expertise grows. Investors should also consider opportunities in emerging applications like bioprinting and electronics, which could represent significant growth areas in the coming years. Strategic partnerships and vertical integration are becoming increasingly important in the AM market, suggesting that companies with strong collaboration capabilities or those offering comprehensive solutions may be particularly valuable investment targets. Additionally, investments in companies developing sustainable AM technologies or those addressing supply chain resilience could benefit from growing environmental and geopolitical concerns. As with any emerging technology market, investors should be prepared for volatility and carefully assess the competitive positioning and technological differentiation of potential investment targets.

Additive Manufacturing Market Conclusion - Summary and key takeaways

The additive manufacturing market stands at the forefront of a manufacturing revolution, offering unprecedented opportunities for innovation across industries. With a projected market size of $48.48 billion by 2033 and a robust CAGR of 16.84%, the industry is poised for significant growth driven by technological advancements, expanding material options, and increasing adoption in production applications. Key takeaways from this analysis include the market's transition from prototyping to production, the growing importance of metal additive manufacturing, and the increasing integration of AM with traditional manufacturing processes. The competitive landscape is dynamic, with both specialized AM companies and traditional manufacturing giants vying for market share through innovation and strategic partnerships. While challenges remain in terms of production speed, cost-effectiveness, and standardization, the opportunities in emerging applications and the potential for supply chain transformation present compelling reasons for continued investment and development in the field. As the market matures, success will likely depend on companies' ability to offer comprehensive solutions that address the full spectrum of AM needs, from design and materials to production and post-processing.

Research Methodology - How this research was conducted

This comprehensive market research on the additive manufacturing industry was conducted using a rigorous methodology combining both primary and secondary research approaches. Primary research involved interviews with industry experts, including executives from leading AM companies, material suppliers, and end-users across various sectors such as aerospace, automotive, and healthcare. These interviews provided valuable insights into market trends, technological developments, and future outlook. Secondary research encompassed a thorough review of industry reports, company financial statements, press releases, and relevant academic publications. Market size and growth projections were derived from a combination of top-down and bottom-up analyses, considering factors such as historical growth rates, technological advancements, and macroeconomic indicators. The segmentation analysis was based on data from industry associations, government publications, and company reports. Regional analysis incorporated economic data, industrial production statistics, and technology adoption rates specific to each geographic area. The competitive landscape assessment was developed through a detailed review of company strategies, product portfolios, and market positioning. Throughout the research process, data triangulation was employed to ensure accuracy and consistency of findings, with particular attention paid to validating key market figures and trends against multiple reliable sources.

Research Scope - Coverage and limitations

The scope of this research encompasses a comprehensive analysis of the global additive manufacturing market, covering key segments including end-user industries, materials, and technologies. The study focuses on the period from 2025 to 2032, with particular attention to market size, growth trends, and competitive dynamics. Coverage includes major geographic regions such as North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with detailed analysis of key countries within these regions. The research examines various AM technologies including selective laser sintering, stereolithography, and fused deposition modeling, as well as emerging technologies. Material analysis covers plastics, metals, and ceramics, with a focus on their applications and market potential. The study also explores the value chain, investment landscape, and future outlook of the AM industry. However, it's important to note certain limitations. The research does not cover every niche application of AM technology, and some emerging technologies may not be fully represented due to their nascent stage. Additionally, while efforts were made to obtain the most current data, rapid technological changes in the AM field may result in some information becoming outdated quickly. The study also does not delve into the technical specifications of individual AM systems in great detail, focusing instead on market-level analysis and trends.

Key Companies and Recent Developments in the Additive Manufacturing Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The additive manufacturing market is characterized by the presence of several key players, each contributing to the industry's growth through innovative products, strategic partnerships, and technological advancements. 3D Systems, a pioneer in the field, has recently announced the expansion of its metal additive manufacturing portfolio with new systems designed for production applications. Stratasys has made headlines with its acquisition of Origin, a move aimed at strengthening its position in polymer AM and expanding its materials capabilities. EOS GmbH continues to lead in industrial metal AM, with recent developments including the launch of its next-generation AM systems featuring improved productivity and reliability. Desktop Metal, following its acquisition of EnvisionTEC, has introduced new metal and polymer 3D printing systems targeting office and production environments. Materialise has focused on software innovations, releasing updates to its Magics software platform to enhance workflow efficiency. HP has entered the metal AM market with its Metal Jet technology, targeting high-volume production applications. GE Additive, through its Arcam EBM and Concept Laser DMLM technologies, continues to push the boundaries of metal AM for aerospace and medical applications. These companies, along with others like SLM Solutions, 3T RPD, and ProtoCAM, are driving the industry forward through continuous innovation, strategic partnerships, and expansion into new application areas. Recent trends include increased focus on sustainability, development of larger build volumes, and advancements in multi-material and composite printing capabilities.