Geothermal Power Generation Market Overview - Definition, scope, and significance

Geothermal power generation harnesses heat energy from the Earth's core to produce electricity through various technologies. This renewable energy source utilizes steam or hot water reservoirs beneath the Earth's surface to drive turbines connected to generators. The market encompasses technologies including direct dry steam, flash steam, and binary cycle power plants, serving residential, commercial, and industrial end users. Geothermal energy offers a stable, baseload power source with minimal environmental impact, making it increasingly significant in the global transition toward sustainable energy systems.

Geothermal Power Generation Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

Key drivers include increasing demand for clean energy, government incentives for renewable power development, and technological advancements improving efficiency and reducing costs. The growing focus on energy security and reducing carbon emissions also propels market growth. However, high initial capital costs, geographical limitations, and long project development timelines present significant restraints. Challenges include complex regulatory environments, potential environmental concerns such as induced seismicity, and competition from other renewable energy sources. Opportunities exist in technological innovations like enhanced geothermal systems (EGS), expanding applications in industrial heating, and emerging markets in regions with untapped geothermal potential.

Geothermal Power Generation Market Growth Trends - Current and emerging trends shaping the market

The market is witnessing several key trends, including increased investment in enhanced geothermal systems (EGS) technology, which expands viable locations for geothermal development beyond traditional hydrothermal resources. There's a growing trend toward hybrid systems combining geothermal with other renewable sources to improve grid stability. Digitalization and AI integration in geothermal operations are enhancing efficiency and predictive maintenance. The market is also seeing increased focus on direct-use applications for industrial processes and district heating. Additionally, there's a trend toward smaller, modular geothermal plants that can be deployed more quickly and with lower capital requirements.

COVID-19 Impact on the Geothermal Power Generation Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted geothermal power generation projects through supply chain interruptions, labor shortages, and delayed permitting processes. Construction activities faced slowdowns due to social distancing measures and travel restrictions. However, the pandemic also highlighted the importance of energy security and resilient power systems, potentially accelerating interest in reliable baseload renewable sources like geothermal. As economies recover, governments are increasingly including geothermal in their green recovery plans and stimulus packages. The market is expected to rebound as project timelines normalize and pent-up demand for clean energy projects is released.

Geothermal Power Generation Market Competitive Landscape - Major competitors and market consolidation

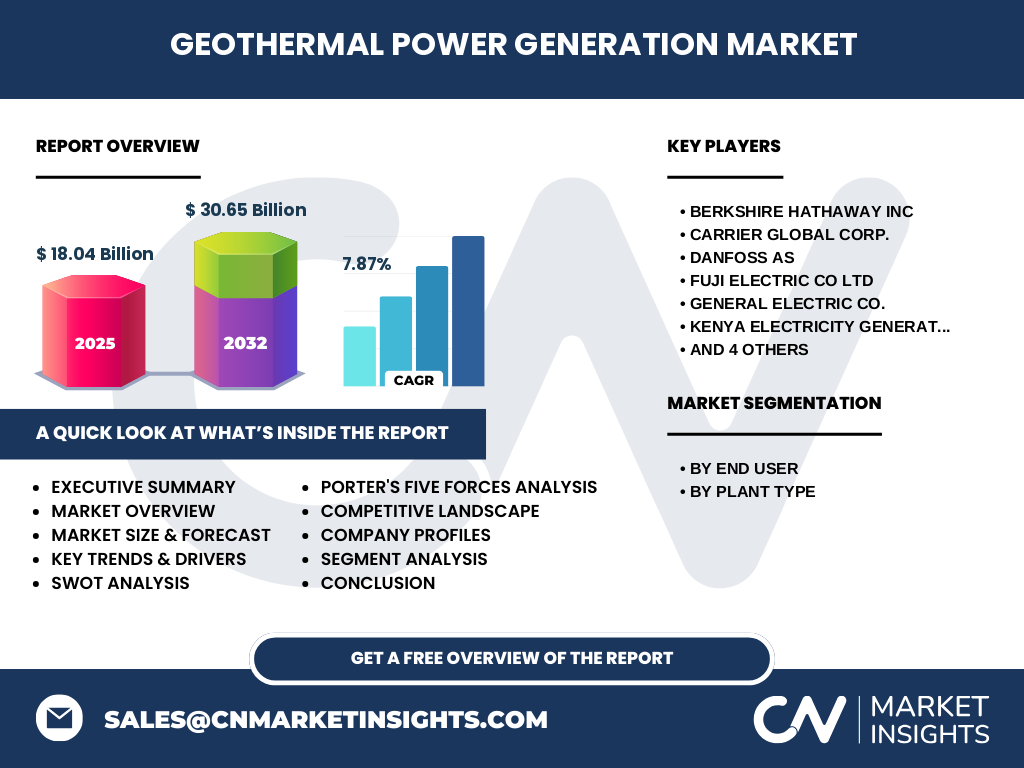

The competitive landscape features a mix of large multinational corporations and specialized geothermal companies. Major players include Berkshire Hathaway Inc., General Electric Co., Toshiba Energy Systems & Solutions Corp, and Fuji Electric Co Ltd, which leverage their extensive technical expertise and financial resources. The market also includes regional players like Kenya Electricity Generating Co Ltd and Northern California Power Agency, which focus on specific geographic markets. Competition is intensifying as companies invest in technological innovations to improve efficiency and reduce costs. Strategic partnerships and collaborations are becoming increasingly common as companies seek to share risks and combine expertise in this capital-intensive industry.

Executive Summary - High-level overview and key findings about Geothermal Power Generation Market

The geothermal power generation market is poised for significant growth, driven by increasing global demand for clean, reliable energy sources. With a projected market size of $18.04 billion by 2026 and expected to reach $30.65 billion by 2033, the market demonstrates strong growth potential with a CAGR of 7.87%. The market is characterized by technological advancements, particularly in enhanced geothermal systems, and a shift toward hybrid renewable energy solutions. While facing challenges such as high initial costs and geographical limitations, the market benefits from strong government support and increasing focus on energy security. The competitive landscape is dynamic, with both established energy giants and specialized geothermal companies vying for market share.

Geothermal Power Generation Market Forecast - Projections for 2025-2032 period

The geothermal power generation market is expected to experience steady growth throughout the forecast period of 2025-2032. Starting from a base of $18.04 billion in 2026, the market is projected to expand to $30.65 billion by 2033, representing a compound annual growth rate (CAGR) of 7.87%. This growth trajectory reflects increasing global investments in renewable energy infrastructure, technological advancements improving project economics, and supportive government policies. The forecast period will likely see accelerated adoption of enhanced geothermal systems (EGS) and increased focus on hybrid renewable energy projects. Market expansion will be driven by both developed markets maturing their geothermal resources and emerging markets exploring new geothermal opportunities.

Geothermal Power Generation Market Size and Share by Segmentation - Breakdown by {segmentData}

The geothermal power generation market is segmented by end user and plant type. By end user, the market serves residential, commercial, and industrial sectors. The industrial segment is expected to dominate due to the high energy demands of manufacturing processes and the potential for direct-use applications. Commercial applications, including district heating and cooling systems, represent a growing segment. The residential segment, while smaller, benefits from increasing adoption of geothermal heat pumps for space heating and cooling. By plant type, direct dry steam plants currently lead the market, utilizing natural steam directly from geothermal reservoirs. Flash steam plants are the second-largest segment, using high-pressure hot water that flashes into steam. Binary cycle plants, which can operate with lower temperature resources, represent the fastest-growing segment due to their versatility and minimal environmental impact.

Global Geothermal Power Generation Market Size and Share by Region - Geographic distribution

The global geothermal power generation market exhibits varied geographic distribution, with significant activity concentrated in regions with favorable geological conditions. The Asia-Pacific region, led by countries like Indonesia, the Philippines, and New Zealand, represents a major market share due to abundant geothermal resources and supportive government policies. North America, particularly the western United States and Canada, maintains a strong market presence with established geothermal projects and ongoing technological innovations. Europe, with countries like Iceland, Italy, and Turkey at the forefront, continues to invest in geothermal development. Latin America, especially Central American countries, shows growing potential. Africa, while currently a smaller market, presents significant untapped opportunities, particularly in the East African Rift Valley region.

Regional Analysis of the Geothermal Power Generation Market - Detailed regional market performance

Regional performance varies significantly across the global geothermal power generation market. The Asia-Pacific region leads in installed capacity and new project development, driven by countries like Indonesia, which has ambitious geothermal expansion plans, and the Philippines, with its long history of geothermal utilization. North America benefits from advanced technology and significant investment, with the United States being the world's largest geothermal producer. Europe's market is characterized by mature projects in Iceland and Italy, alongside emerging opportunities in countries like Turkey and Germany. Latin America shows strong growth potential, particularly in Central American countries that have prioritized geothermal development. Africa's market is in early stages but presents significant opportunities, especially in Kenya and Ethiopia, which are leveraging their geothermal resources to address power shortages and support economic development.

Leading Company Profiles in the Geothermal Power Generation Market - Industry players and strategies

Key players in the geothermal power generation market include Berkshire Hathaway Inc., which operates significant geothermal assets in the United States through its subsidiary CalEnergy Generation. Carrier Global Corp. focuses on geothermal heat pump technologies for residential and commercial applications. Danfoss AS specializes in geothermal heat pump components and systems. Fuji Electric Co Ltd provides geothermal power generation equipment and has a strong presence in the Asia-Pacific market. General Electric Co. offers comprehensive geothermal solutions, including turbines and generators. Kenya Electricity Generating Co Ltd (KenGen) is a leading geothermal developer in Africa, with significant installed capacity. NIBE Industrier AB specializes in heat pump technologies. Northern California Power Agency operates geothermal facilities in California's Geysers field. Toshiba Energy Systems & Solutions Corp provides geothermal power generation systems, particularly in the Asia-Pacific region. Turboden SpA, a Mitsubishi Heavy Industries company, specializes in binary cycle geothermal plants and ORC (Organic Rankine Cycle) systems.

Porter's Five Forces Analysis of the Geothermal Power Generation Market - Competitive forces assessment

The geothermal power generation market exhibits a moderate level of competitive intensity. The threat of new entrants is relatively low due to high capital requirements, complex regulatory environments, and the need for specialized technical expertise. Supplier power is moderate, with a limited number of companies providing specialized geothermal equipment and services. Buyer power varies by region but is generally moderate, with utilities and large industrial consumers having some negotiating leverage. The threat of substitutes is significant, with competition from other renewable energy sources like solar and wind, as well as traditional fossil fuel power generation. Competitive rivalry is moderate to high, with both large multinational corporations and specialized geothermal companies competing for market share through technological innovations and strategic partnerships.

SWOT Analysis of the Geothermal Power Generation Market - Strengths, weaknesses, opportunities, threats

Strengths of the geothermal power generation market include its reliability as a baseload power source, minimal environmental impact compared to fossil fuels, and long operational life of geothermal plants. The market also benefits from technological advancements improving efficiency and expanding viable locations for development. Weaknesses include high initial capital costs, geographical limitations requiring specific geological conditions, and potential environmental concerns such as induced seismicity. Opportunities exist in technological innovations like enhanced geothermal systems (EGS), expanding applications in industrial heating and cooling, and growing demand for clean energy in emerging markets. Threats include competition from other renewable energy sources, potential changes in government policies and incentives, and public perception issues related to geothermal development.

Geothermal Power Generation Market Value Chain Analysis - Industry structure and value flow

The geothermal power generation value chain encompasses several key stages. It begins with resource exploration and assessment, involving geological surveys and test drilling to identify viable geothermal reservoirs. The development phase includes project planning, permitting, and infrastructure construction. Equipment manufacturing and supply form a critical component, with specialized companies producing turbines, generators, and other essential components. Project development and operation involve the actual construction and management of geothermal power plants. The value chain also includes maintenance and service providers, ensuring optimal plant performance throughout its operational life. Finally, the distribution and integration of geothermal power into the electrical grid complete the value chain, connecting this renewable energy source to end users.

Key Investment Insights in the Geothermal Power Generation Market - Strategic investment recommendations

Investors should consider several key insights when evaluating opportunities in the geothermal power generation market. First, focus on companies with strong technological capabilities and a track record of successful project development, particularly those involved in enhanced geothermal systems (EGS) and hybrid renewable projects. Geographic diversification is crucial, with attention to regions offering supportive regulatory environments and abundant geothermal resources. Investment in companies providing equipment and services for the entire value chain can provide exposure to multiple growth areas within the market. Consider the potential of direct-use applications and geothermal heat pump technologies, which are experiencing rapid growth. Lastly, monitor government policies and incentives, as these can significantly impact project economics and market growth in different regions.

Geothermal Power Generation Market Conclusion - Summary and key takeaways

The geothermal power generation market presents a compelling opportunity for growth and investment in the renewable energy sector. With a projected market size of $30.65 billion by 2033 and a CAGR of 7.87%, the market demonstrates strong potential driven by increasing global demand for clean, reliable energy sources. Technological advancements, particularly in enhanced geothermal systems, are expanding the market's reach beyond traditional hydrothermal resources. While facing challenges such as high initial costs and geographical limitations, the market benefits from supportive government policies and increasing focus on energy security. The competitive landscape is dynamic, with both established energy giants and specialized geothermal companies driving innovation and market expansion. As the world transitions toward sustainable energy systems, geothermal power generation is poised to play an increasingly important role in the global energy mix.

Research Methodology - How this research was conducted

This comprehensive market research was conducted using a combination of primary and secondary research methodologies. Primary research involved interviews with industry experts, including geothermal power plant operators, equipment manufacturers, and energy policy specialists. Secondary research encompassed analysis of company reports, industry publications, government databases, and academic journals. Market size and forecast data were derived from historical trends, current market conditions, and projected growth factors. Segmentation analysis was based on industry classifications and market dynamics. Regional analysis incorporated economic indicators, policy frameworks, and resource availability data. The competitive landscape was assessed through company profiles, market share analysis, and strategic developments. Porter's Five Forces and SWOT analyses were conducted to evaluate market dynamics and competitive positioning. Value chain analysis was performed to understand the industry structure and key players at each stage of the geothermal power generation process.

Research Scope - Coverage and limitations

This research report covers the global geothermal power generation market, focusing on key regions including North America, Europe, Asia-Pacific, Latin America, and Africa. The study encompasses market trends, growth drivers, challenges, and opportunities from 2025 to 2032. Segmentation analysis includes end users (residential, commercial, and industrial) and plant types (direct dry steam, flash steam, and binary cycle). The report profiles leading companies in the industry and analyzes the competitive landscape. Limitations of this research include the availability of detailed regional data for certain markets and the rapidly evolving nature of geothermal technologies, which may impact long-term projections. The study focuses on electricity generation and does not extensively cover direct-use applications beyond their impact on overall market growth.

Key Companies and Recent Developments in the Geothermal Power Generation Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Berkshire Hathaway Inc. continues to expand its geothermal portfolio in California's Salton Sea area, with recent investments in new capacity and efficiency improvements. General Electric Co. has announced advancements in its geothermal turbine technology, focusing on improved efficiency for lower-temperature resources. Kenya Electricity Generating Co Ltd (KenGen) recently commissioned new geothermal plants, significantly increasing Kenya's geothermal capacity and supporting the country's renewable energy goals. Toshiba Energy Systems & Solutions Corp has formed strategic partnerships to develop geothermal projects in Japan and Southeast Asia, leveraging its advanced binary cycle technology. Turboden SpA introduced new Organic Rankine Cycle (ORC) systems designed for small to medium-scale geothermal applications, expanding the market for lower-temperature resources. These developments reflect the industry's focus on technological innovation, geographic expansion, and improving the economics of geothermal power generation.