Military Vehicle & Aircraft Protection Systems Market Overview - Definition, scope, and significance

Military Vehicle & Aircraft Protection Systems represent a critical segment of the defense industry, encompassing technologies designed to safeguard military assets from various threats including ballistic projectiles, explosive devices, and hostile fire. These systems include armor plating, reactive armor, active protection systems, ballistic shields, and specialized materials engineered to withstand extreme conditions. The market covers both ground vehicles such as tanks, armored personnel carriers, and tactical vehicles, as well as aircraft including transport planes, helicopters, and combat aircraft. The significance of this market lies in its direct impact on military personnel safety, mission success rates, and the overall effectiveness of defense operations across global military forces.

Military Vehicle & Aircraft Protection Systems Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers for this market include escalating global geopolitical tensions, increasing defense budgets in emerging economies, and the growing sophistication of modern warfare threats. Technological advancements in materials science, such as composite armor and nanotechnology-based solutions, are creating new opportunities for enhanced protection capabilities. However, the market faces significant restraints including high research and development costs, lengthy procurement cycles, and strict regulatory compliance requirements. Challenges include the need to balance protection levels with weight constraints, particularly for aircraft where additional armor affects fuel efficiency and payload capacity. Opportunities exist in the development of modular protection systems, integration of artificial intelligence for threat detection, and the expansion of unmanned vehicle protection solutions.

Military Vehicle & Aircraft Protection Systems Market Growth Trends - Current and emerging trends shaping the market

The market is experiencing several notable growth trends, including the increasing adoption of active protection systems that can intercept incoming threats before impact. There is a strong shift toward lightweight composite materials that provide superior protection while minimizing weight penalties. Another emerging trend is the integration of smart sensors and real-time threat assessment capabilities into protection systems. The market is also seeing growing demand for multi-threat protection solutions that can defend against a wide range of attack vectors simultaneously. Additionally, there is increasing focus on retrofitting existing military assets with modern protection systems rather than developing entirely new platforms, driven by cost considerations and the need to extend the service life of current equipment.

COVID-19 Impact on the Military Vehicle & Aircraft Protection Systems Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the Military Vehicle & Aircraft Protection Systems market through supply chain interruptions, manufacturing delays, and temporary production halts at defense facilities. Defense budgets in some regions were temporarily reallocated toward pandemic response efforts, affecting planned procurement of protection systems. However, the pandemic also highlighted the importance of military readiness and homeland security, potentially accelerating certain modernization programs in the long term. The market has shown resilience due to the essential nature of defense contracts and the strategic importance of military capabilities. Recovery has been steady, with manufacturers adapting to new operational protocols and supply chain diversification strategies to mitigate future disruptions.

Military Vehicle & Aircraft Protection Systems Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape of this market is characterized by a mix of large defense contractors and specialized protection system manufacturers. Major players include multinational corporations with diverse defense portfolios alongside niche companies focusing exclusively on protection technologies. Competition is intense, with companies competing on technological innovation, cost-effectiveness, and ability to meet specific military requirements. The market has seen some consolidation through mergers and acquisitions, particularly as larger companies seek to acquire specialized technologies. Geographic presence and established relationships with military procurement agencies provide significant competitive advantages. Companies are increasingly forming strategic partnerships to combine complementary technologies and expand their market reach.

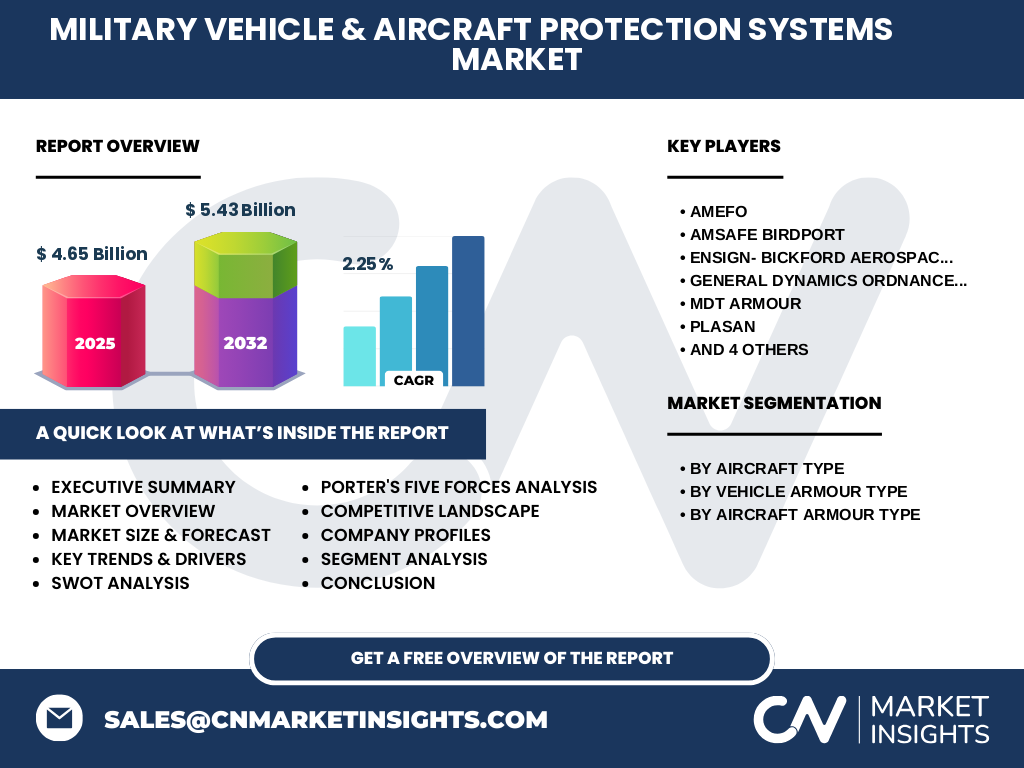

Executive Summary - High-level overview and key findings about Military Vehicle & Aircraft Protection Systems Market

The Military Vehicle & Aircraft Protection Systems market represents a vital segment of the global defense industry, valued at approximately 4.65 billion with a projected growth to 5.43 billion by 2033, reflecting a CAGR of 2.25%. This market encompasses a wide range of protection technologies for both ground vehicles and aircraft, driven by increasing global security concerns and technological advancements. Key segments include RPG nets, reactive armor for vehicles, and various aircraft protection systems such as cockpit and floor protection. The market is characterized by high barriers to entry due to technical complexity and regulatory requirements, with major players including AMEFO, General Dynamics, Rheinmetall AG, and others. Growth is being fueled by modernization programs, emerging threat landscapes, and the need for enhanced survivability of military assets.

Military Vehicle & Aircraft Protection Systems Market Forecast - Projections for 2025-2032 period

Looking ahead to the 2025-2032 period, the Military Vehicle & Aircraft Protection Systems market is expected to experience steady growth, reaching approximately 5.43 billion by 2033 with a compound annual growth rate of 2.25%. This growth trajectory reflects sustained defense spending, particularly in regions experiencing geopolitical tensions. The forecast period will likely see increased investment in next-generation protection technologies, including active protection systems and advanced composite materials. Market expansion will be driven by ongoing modernization efforts in established military powers and increasing defense capabilities in emerging economies. The aircraft protection segment is expected to show particularly strong growth as military forces worldwide upgrade their air fleets with enhanced survivability features.

Military Vehicle & Aircraft Protection Systems Market Size and Share by Segmentation - Breakdown by {segmentData}

The market segmentation reveals distinct patterns in demand across different protection system types. In the aircraft segment, transport aircraft and helicopters represent the largest share, driven by their widespread use in both military operations and humanitarian missions. For vehicle protection, RPG nets and reactive armor systems dominate due to their effectiveness against common threats faced by ground vehicles. Within aircraft armor protection, cockpit protection commands significant market share as pilot survivability remains a top priority. Pilot seat protection systems also represent a substantial segment, reflecting the critical importance of protecting personnel in high-risk environments. The market demonstrates varied growth rates across segments, with active protection systems showing particularly strong momentum due to their advanced threat mitigation capabilities.

Global Military Vehicle & Aircraft Protection Systems Market Size and Share by Region - Geographic distribution

Geographic distribution of the Military Vehicle & Aircraft Protection Systems market shows significant variation across regions, influenced by factors such as defense spending, military modernization programs, and regional security dynamics. North America, led by the United States, represents the largest market share due to substantial defense budgets and ongoing modernization initiatives. Europe follows as a major market, with countries investing in both NATO commitments and national defense capabilities. The Asia-Pacific region is experiencing the fastest growth rate, driven by increasing defense expenditures in countries like China, India, and Japan. The Middle East represents a significant market due to ongoing regional conflicts and substantial oil-wealth-funded military modernization. Latin America and Africa show more modest but growing demand, primarily focused on counter-insurgency and border security applications.

Regional Analysis of the Military Vehicle & Aircraft Protection Systems Market - Detailed regional market performance

Regional analysis reveals distinct market characteristics and growth patterns across different geographic areas. In North America, the market is characterized by advanced technological capabilities and substantial government procurement, with a focus on next-generation protection systems. European markets emphasize interoperability with NATO standards and sustainable defense solutions. The Asia-Pacific region shows rapid adoption of indigenous protection technologies alongside imports from established suppliers, with particular emphasis on maritime and border security applications. Middle Eastern markets prioritize systems capable of withstanding asymmetric warfare threats, while Latin American countries focus on cost-effective solutions for internal security operations. African markets, though smaller, are growing steadily with increasing focus on peacekeeping and counter-terrorism capabilities.

Leading Company Profiles in the Military Vehicle & Aircraft Protection Systems Market - Industry players and strategies

The market features several prominent companies with diverse strategies and specializations. AMEFO focuses on innovative armor solutions with particular expertise in composite materials. Amsafe Birdport specializes in aircraft protection systems with strong emphasis on pilot safety. Ensign-Bickford Aerospace & Defense Company brings extensive experience in energetic materials and protection technologies. General Dynamics Ordnance & Tactical Systems leverages its broad defense portfolio to offer integrated protection solutions. MDT Armour concentrates on vehicle armor with advanced manufacturing capabilities. PLASAN provides specialized protection systems with focus on lightweight solutions. QinetiQ North America emphasizes research-driven approaches to protection technology. RUAG AG combines Swiss precision engineering with military applications. Rheinmetall AG offers comprehensive protection solutions backed by German engineering excellence. Tencate Advanced Armor specializes in advanced materials for both vehicle and aircraft applications.

Porter's Five Forces Analysis of the Military Vehicle & Aircraft Protection Systems Market - Competitive forces assessment

Applying Porter's Five Forces analysis to this market reveals a moderately competitive landscape. The threat of new entrants is relatively low due to high capital requirements, regulatory barriers, and the need for specialized technical expertise. Supplier power is moderate, as companies rely on specialized materials and components, though large manufacturers can exert significant influence. Buyer power is relatively low given the concentrated nature of military procurement and the critical nature of protection systems. The threat of substitutes is minimal as protection systems have unique requirements that cannot be easily replaced. Competitive rivalry is intense among established players, with competition based on technological superiority, cost-effectiveness, and ability to meet specific military requirements. The market shows characteristics of an oligopoly, with a few large players dominating the landscape.

SWOT Analysis of the Military Vehicle & Aircraft Protection Systems Market - Strengths, weaknesses, opportunities, threats

The SWOT analysis of this market reveals several key factors. Strengths include advanced technological capabilities, strong intellectual property portfolios, and established relationships with military procurement agencies. Weaknesses encompass high development costs, lengthy certification processes, and vulnerability to budget fluctuations. Opportunities exist in emerging markets, technological innovations such as AI integration, and the growing demand for unmanned vehicle protection systems. Threats include increasing cyber warfare capabilities that may bypass physical protection, geopolitical instability affecting international sales, and the emergence of new threat types that current systems may not address. The market's ability to adapt to evolving threats while managing costs and regulatory requirements will be crucial for continued success.

Military Vehicle & Aircraft Protection Systems Market Value Chain Analysis - Industry structure and value flow

The value chain in this market encompasses several key stages, beginning with raw material suppliers providing specialized metals, composites, and energetic materials. Research and development activities focus on creating innovative protection solutions, often involving significant investment in testing and certification. Manufacturing processes require specialized facilities and skilled labor to produce high-quality protection systems. Distribution involves complex logistics to deliver systems to military bases and operations worldwide. Installation and integration services ensure proper deployment of protection systems on vehicles and aircraft. After-sales support includes maintenance, upgrades, and technical assistance. Each stage adds value through technological advancement, quality assurance, and specialized expertise, with the highest value typically added during the R&D and manufacturing phases.

Key Investment Insights in the Military Vehicle & Aircraft Protection Systems Market - Strategic investment recommendations

Strategic investment insights for this market point toward several promising areas. Investors should consider opportunities in companies developing next-generation protection technologies, particularly those focusing on active protection systems and advanced materials. The growing demand for unmanned vehicle protection systems represents a significant investment opportunity as military forces expand their use of autonomous platforms. Companies with strong R&D capabilities and intellectual property portfolios are particularly attractive investment targets. Geographic diversification is recommended, with particular attention to rapidly growing markets in the Asia-Pacific region. Additionally, investments in companies that can provide modular and scalable protection solutions offer potential advantages as military forces seek flexible and cost-effective options. The market's steady growth trajectory and essential nature of protection systems make it an attractive long-term investment opportunity.

Military Vehicle & Aircraft Protection Systems Market Conclusion - Summary and key takeaways

The Military Vehicle & Aircraft Protection Systems market represents a critical and growing segment of the global defense industry, valued at 4.65 billion with projected growth to 5.43 billion by 2033. The market is characterized by technological sophistication, high barriers to entry, and strong demand driven by global security concerns. Key segments include RPG nets, reactive armor, and various aircraft protection systems, with transport aircraft and helicopters representing significant market share. The competitive landscape features established players with diverse strategies, while regional analysis shows varying growth patterns across different geographic areas. Despite challenges including high development costs and regulatory requirements, the market offers substantial opportunities in emerging technologies and expanding geographic markets. The steady growth trajectory and essential nature of protection systems position this market as a vital component of military modernization efforts worldwide.

Research Methodology - How this research was conducted

This research was conducted through a comprehensive methodology combining primary and secondary data sources. Primary research involved interviews with industry experts, defense contractors, and military procurement officials to gather insights on market trends, technological developments, and future projections. Secondary research included analysis of financial reports, government defense budgets, industry publications, and patent filings to understand market dynamics and competitive positioning. Market size and forecast figures were derived from a combination of bottom-up analysis of individual segments and top-down assessment of regional markets. The research methodology also incorporated competitive analysis frameworks and trend identification techniques to provide a holistic view of the market landscape. Data triangulation was employed to ensure accuracy and reliability of the findings presented in this report.

Research Scope - Coverage and limitations

This research covers the global Military Vehicle & Aircraft Protection Systems market from 2025 to 2033, with a focus on key market segments, geographic regions, and competitive dynamics. The scope includes analysis of protection systems for both ground vehicles and aircraft, encompassing armor technologies, active protection systems, and specialized materials. Coverage extends to major market players, their strategies, and recent developments in the industry. The research examines market drivers, restraints, opportunities, and challenges, providing a comprehensive view of the market landscape. Limitations of this research include the confidential nature of some military procurement data, the rapidly evolving nature of protection technologies, and potential geopolitical factors that may impact market dynamics beyond the forecast period. The research provides a detailed analysis while acknowledging that certain sensitive information may not be publicly available.

Key Companies and Recent Developments in the Military Vehicle & Aircraft Protection Systems Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The key companies in this market have demonstrated significant activity through various strategic initiatives. AMEFO has focused on developing advanced composite armor solutions with enhanced multi-threat protection capabilities. Amsafe Birdport recently announced new aircraft protection systems incorporating smart sensor technology for real-time threat assessment. Ensign-Bickford Aerospace & Defense Company has expanded its product line with innovative energetic materials for enhanced protection. General Dynamics Ordnance & Tactical Systems launched a new modular protection system adaptable to multiple vehicle platforms. MDT Armour secured a major contract for RPG net systems for armored vehicles. PLASAN introduced lightweight protection solutions using advanced polymer materials. QinetiQ North America announced research collaboration on AI-enhanced protection systems. RUAG AG expanded its European manufacturing capabilities for aircraft armor components. Rheinmetall AG unveiled next-generation active protection systems with improved interception capabilities. Tencate Advanced Armor launched new ballistic materials offering superior protection-to-weight ratios. These developments reflect the industry's focus on innovation, strategic partnerships, and meeting evolving military requirements.